Are you dealing with debt from Phoenix Financial Services? Thinking of calling them to resolve it? Please don’t. It’s in your best interest to know a few things before you even consider that call.

Phoenix Financial Services, LLC was a third-party debt collection agency that focused on collecting medical debt. They worked with healthcare providers, hospitals, and medical facilities all over the country. Here is what we have in our case file on the company:

They are not an unknown entity.

Phoenix Financial Services has more than 1,100 complaints registered with the Consumer Financial Protection Bureau. They have been named in over 60 federal lawsuits. They just paid $1.675 million in federal penalties and are now permanently closed. Between 2017 and 2020, the company handled 54.4 million accounts.

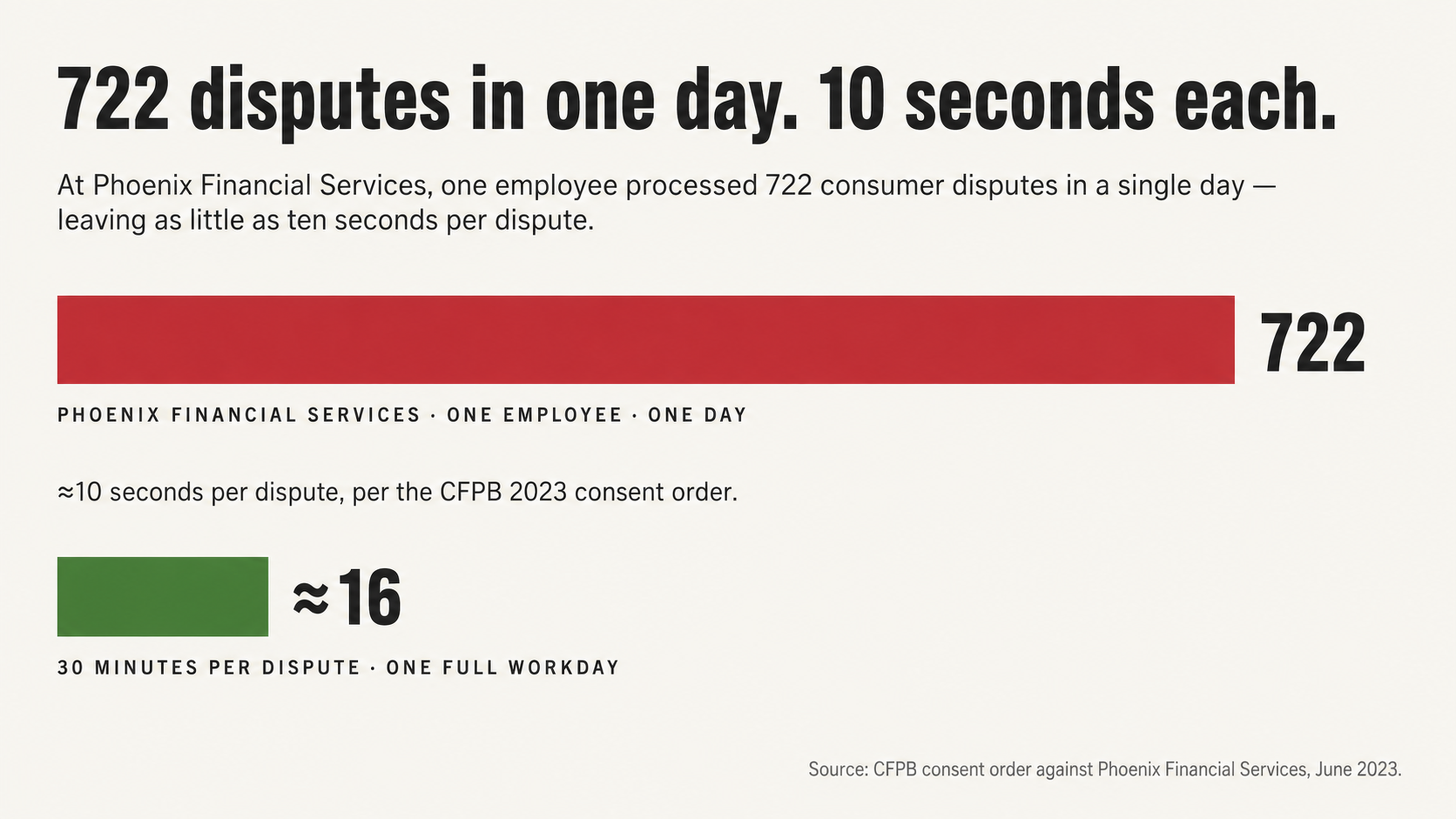

At one point, one employee processed 722 consumer disputes in a single day. They may have spent as few as 10 seconds on each dispute.

The Better Business Bureau revoked the accreditation of Phoenix Financial Services. They cited the company’s failure to resolve complaints and government action taken against them. When the Better Business Bureau revokes a collection agency’s accreditation, that’s a sign that there are systemic issues rather than one-off problems.

In 2018 and 2019, Phoenix Financial Services appeared on the Indianapolis Business Journal’s Fast 25 list. They had 114 percent revenue growth. In 2018, revenue totaled $21.6 million. All of this explosive growth occurred during the period when the company failed to comply with federal regulations.

Here is what we found out from our case file.

The CFPB took action against Phoenix Financial Services in June 2023. The resulting consent order reads like a roadmap of what went wrong. Between January 2017 and March 2021, up to 83 percent of direct consumer disputes received no response at all. When consumers disputed debts directly to Phoenix Financial Services, the company largely ignored them.

The company sent about 30 percent of indirect disputes to an automated system. No human being reviewed these disputes at all. When they did look at disputes, the company performed a superficial investigation, at best. The CFPB found that Phoenix used circular, cursory processes to investigate disputes. Instead of verifying debts, the company merely compared information from the consumer dispute with the data they already possessed from clients.

The consent order requires Phoenix Financial Services to issue refunds to consumers who paid amounts on unverified debts. Those debts date back to January 1, 2017. We now know what consumer advocates have long suspected. Many consumers paid debts that Phoenix Financial Services could not verify.

Phoenix Financial Services also faces allegations in federal court. The company violated the Telephone Consumer Protection Act. They made autodialed calls to cell phones. They also violated the Fair Credit Reporting Act. They furnished inaccurate information to credit bureaus.

In multiple class actions, Phoenix Financial Services faces allegations of systematic violations rather than isolated incidents. The cases against them stretch across Indiana, New York, Florida, Texas, Arizona, and New Jersey.

Consumer reviews on WalletHub, ConsumerAffairs, and the Better Business Bureau all tell the same story. The company has a rating of 2.0 out of 5 stars on WalletHub. A staggering 71 percent of reviews are one-star reviews. ConsumerAffairs gives the company a rating of 1.0 out of 5 stars.

One consumer reviewed Phoenix Financial Services on WalletHub in March 2024. “These people continue to call, sometimes more than once a day. Sometimes they will just call, let it ring half a ring, and then hang up. I returned one call one day, and after finding out what they wanted, I asked them to send an invoice, though it seems they don’t have one.”

Consumers who review the company describe the same experience. The company demands payment without providing documentation.

Another consumer reviewing the company on the Better Business Bureau website reported, “When asked for proof of unpaid debt, they hung up on me. Called back, same conversation, hung up on again. They speak to you like you are trash.” These consumer reviews corroborate the federal findings that Phoenix Financial Services mishandled disputes.

Why should you dispute this account?

There are several reasons why you may want to challenge a collection account from Phoenix Financial Services.

The Error Rate

Credit reports are not as accurate as you might think. In fact, a study from U.S. PIRGs found that 79 percent of credit reports contain errors or other serious mistakes. When a company processes a dispute in 10 or 30 seconds, errors do not get fixed. They multiply.

Phoenix Financial Services collected medical debt. Medical debt is infamous for its billing complexity. Insurance adjustments, facility charges, and provider fees all create opportunities for error. A debt may look valid on the surface, but it could include charges that insurance already covered. It could include charges for services never rendered. It could include balances that belong to someone else altogether.

The CFPB found that Phoenix Financial Services continued to collect debts that were not verified after consumers disputed them. In fact, this may have occurred in at least thousands of instances. That means the company continued to pursue debts it could not verify were legitimate, accurate, or owed by the correct consumer.

Payment Can Backfire

When you see a collection account, you may feel like you should just pay it and make it go away. In many cases, that approach will backfire. Paying a collection account will update its status from “unpaid” to “paid.” However, the negative mark will still remain on your credit report. It will stay there for seven years from the original delinquency date.

Some newer credit scoring models treat paid collections more favorably than unpaid collections. However, many lenders still use the older scoring models. With those models, a paid collection can damage your credit score almost as much as an unpaid collection. Actually paying a collection can also restart the clock on certain state statutes of limitations for debt collection.

If you dispute an account and it contains errors, you force the collection agency to verify the debt. If it cannot verify the debt, it must remove the account from your credit report. Given the inadequacies of Phoenix Financial Services’ verification process, it’s likely that many accounts will not survive a proper challenge.

The situation is more complicated now that the company has closed. Since there is no longer an operational entity to respond to disputes, credit bureaus may struggle to verify accounts. If they cannot verify accounts, they must remove them under federal law. This may create a unique window of opportunity for consumers.

Understanding the Debt Collection Game

Debt collectors make money when consumers pay debts. To get you to pay, debt collectors use urgency and fear. They demand immediate payment. They threaten legal action. They threaten credit damage. In most cases, there is no legitimate need for the urgency communicated in these letters.

The federal court record shows that Phoenix Financial Services faced class action allegations. The company operated a zombie debt collection scheme. They attempted to collect debts beyond the statute of limitations without proper disclosure. When debt collectors pursue debts that are no longer enforceable under the law, the urgency they attempt to create is particularly misleading.

The phone number on a collection letter serves one purpose. It allows you to request validation of the debt. It is not an invitation to negotiate payment before you know what you owe or whether you owe it at all. Any information you provide over the phone can strengthen the debt collector’s position against you.

Debt buyers purchase delinquent debts at a discount. They may pay mere pennies on the dollar for portfolios of consumer debt. If a debt collector paid $50 for a $1,000 debt, the collector has plenty of room to negotiate. They can still turn a profit.

When a debt collector offers to settle a debt for a fraction of the balance, that tells you something. The balance showing on your credit report is not concrete. It’s not necessarily accurate. If the debt was worth every penny of the balance, the debt collector would not accept less. The fact that they are willing to negotiate shows there is flexibility for consumers to use to their advantage.

Debt that gets purchased in bulk often lacks documentation. The original account agreements, payment histories, and verification materials may not transfer with the debt. This creates an opening for consumers who properly dispute accounts through the credit bureaus or request debt validation.

What to Do Next

Your first contact should never be direct.

Consumers are at an informational disadvantage when dealing with collection agencies. The collection agency has records of the debt. They have experience collecting debts. They understand their legal rights. When you call a collector before you understand your options and your rights, you put yourself at a disadvantage.

Professional credit repair specialists understand what debt collectors have to do. They understand the documentation they need to provide. They understand the timelines they need to meet. They understand the defenses that may be available to consumers.

Once you dispute a debt, you create a 30-day window for investigation. That window usually favors the consumer. The longer the dispute remains unresolved, the less likely it is that the debt collector can continue pursuing the debt. Professionals understand how to make this dynamic work for consumers.

You need to focus on documentation rather than communication.

When you dispute accounts through the credit bureaus, you create a formal record. You create legal obligations for the debt collector. They must investigate and respond within specific timelines or the account must be removed. When you communicate with a debt collector over the phone, none of those obligations exist.

According to the CFPB, Phoenix Financial Services sent collection letters to consumers who disputed debts within 30 days. They did this without first verifying the debts. This occurred in at least hundreds of instances.

That is a clear violation of the Fair Debt Collection Practices Act. Even with the protections of the FDCPA, a debt collector may ignore your rights if you do not enforce them properly.

Professional credit repair specialists ensure your disputes get documented properly. They ensure deadlines get met. They ensure responses from debt collectors meet legal obligations. When you handle your own dispute, you may not recognize when a debt collector’s response fails to meet verification standards.

The stakes here are high. An improperly placed collection account can decrease your credit score by 100 points or more. That can impact your mortgage rate. It can impact the terms of your auto loan. It can impact your insurance premiums. It can even impact your employment prospects. Professional help disputing questionable accounts is an investment in your financial rehabilitation.

Closing

Where do you go from here?

Phoenix Financial Services is now permanently closed. The company closed in December 2024, less than 19 months after the CFPB consent order and $1.675 million in penalties. Just because the company closed, that does not mean collection accounts from Phoenix Financial Services will disappear from consumer credit reports. In fact, these tradelines may still exist.

Now, they are essentially orphaned. There is no longer a company to respond to disputes.

We know the company failed to comply with federal regulations. We know they failed to properly respond to consumer disputes.

Given their history, many of the accounts on credit reports may contain errors that were never properly investigated. If you received collection communications from Phoenix Financial Services and paid amounts on unverified debts between January 1, 2017 and June 8, 2023, you may be entitled to a refund under the federal consent order.

Our case file on Phoenix Financial Services shows a debt collector that processed disputes in seconds rather than minutes. It shows a debt collector that ignored 83 percent of direct consumer disputes. It shows a debt collector that continued to collect debts it could not verify. All of this creates opportunities for consumers to challenge accounts that may be improperly placed on their credit reports.

Now what?

If you see Phoenix Financial Services on your credit report, do not contact the collection agency or their successors directly. Given the history of this debt collector and their failure to respond to disputes, these accounts deserve professional review before you consider paying them.

FightCollections.com specializes in analyzing collection accounts. We identify errors that may warrant removal. Our specialists understand the documentation you need. They understand the timelines you need to meet. They understand the strategies you need to pursue. We fight the collectors so you do not have to navigate this process alone.

Contact us today for a free consultation. We will review your credit report and discuss your options. The leverage points we found in the Phoenix Financial Services case file may apply to your situation.

Professional analysis costs you nothing up front and may save you from paying a debt that cannot be verified or may not even be yours.