If you are being sued by Pressler, Felt & Warshaw LLP, the news isn’t good.

Their team represents some of the largest debt buyers in the country and has established a volume-based business model through the filing of thousands of lawsuits each year. They are banking on the vast majority of consumers ignoring their suit and losing by default.

But you are not most consumers. Armed with the knowledge of who they are, what they do, and how they operate, you can beat them in court and have the entire lawsuit dismissed.

Pressler, Felt & Warshaw LLP is a New Jersey-based debt collection law firm that has been in business since 1930. Until 2016, the firm was known as Pressler and Pressler. After being penalized $1 million by a federal agency in 2016, they changed their name to Pressler, Felt & Warshaw LLP.

A History of Regulatory Infractions

In April 2016, the Consumer Financial Protection Bureau took action against the firm after discovering that attorneys were reviewing each lawsuit for as little as four seconds before filing it against consumers. According to the investigation, one attorney filed approximately 69,000 lawsuits in 2011 alone.

In some cases, the attorney was processing as many as 1,000 cases in a single day. Because of the volume, it is clear that most consumers were sued for debts that no one verified as accurate or enforceable.

The CFPB determined that the firm was making false allegations about consumer debts by filing lawsuits that were not supported by the evidence, and without attorneys having reviewed documents related to the debt’s validity. The firm paid $1 million in civil penalties, and their client (the debt buyer) paid an additional $1.5 million in penalties.

At present, you will see a Government Action notice on the Better Business Bureau profile page for the firm.

In another case, the firm participated in a $3.9 million class-action settlement that required them to vacate nearly 48,000 default judgments that had been entered against consumers in New York City.

The settlement in the case of Mayfield et al. v. Asta Funding Inc. et al. also required them to permanently stop trying to collect on debts for more than 60,000 class members. When a court throws out 48,000 judgments, you can be sure there was something systemically wrong in the way those judgments were obtained.

How Does the Firm Operate?

A “Lawsuit Mill”

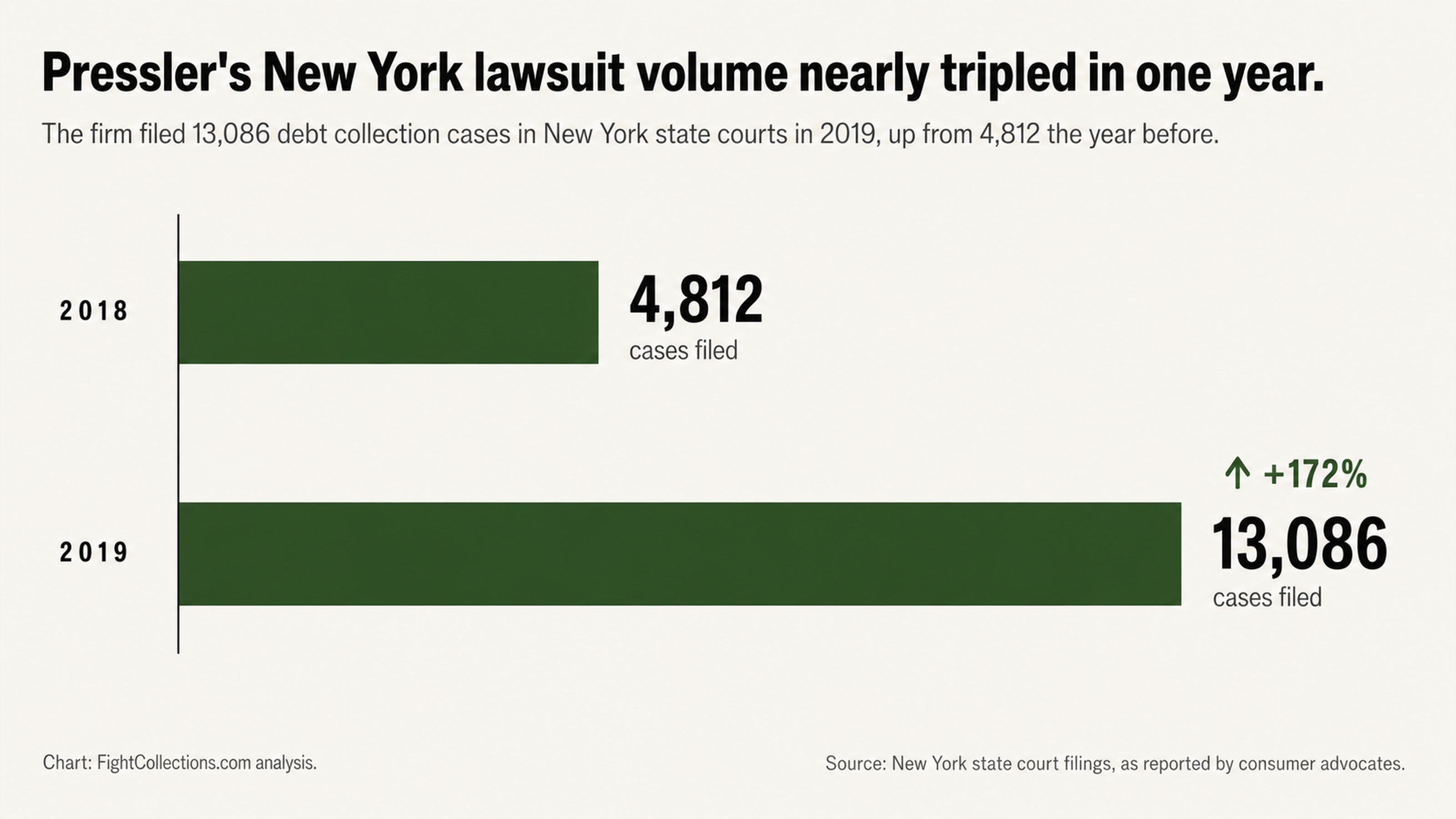

According to consumer advocates, Pressler, Felt & Warshaw LLP is what is known as a “lawsuit mill.” In 2018, the firm filed 4,812 debt collection lawsuits in New York state courts. In 2019, they filed 13,086 cases. According to their website, they have access to more than 1.5 million accounts. This volume is one reason their verification processes have been so poor historically.

The firm represents debt buyers who purchase defaulted accounts from original creditors for pennies on the dollar. In most cases, the debt buyer receives very little documentation when purchasing the accounts. Sometimes, they receive nothing more than a spreadsheet with names, addresses, and balances due. The firm then files lawsuits against consumers based on this documentation, hoping most consumers will ignore the lawsuit or fail to show up in court.

In 2011, 99 percent of defendants being sued by the firm were unrepresented. The firm wins most of their cases by default when consumers fail to show up to court. Once they have a judgment, they will pursue bank account levies, wage garnishment, and other post-judgment collection activities.

Speed is their Enemy

The very factors that make the firm so prolific are also what make them vulnerable. If their attorneys are only reviewing cases for seconds rather than minutes, it’s easy to see why documentation may be missing. If they are filing cases assembly-line fashion, it’s clear why they can’t possibly be verifying the individual accounts. There have been court rulings on their affidavits, documentation of standing, and improper venue.

There are documented court cases where they have sued the wrong people. In one federal case, the court even granted summary judgment in favor of the defendant because the firm continued to send collection letters after they were notified that they were pursuing the wrong person. We see repeated complaints from consumers who say the firm ignores identity theft affidavits and continues to collect from people who don’t owe the debt.

Why You Shouldn’t Pay Before Disputing

The Collection Trap

When you find a collection account on your credit report, your first thought may be to just pay it and move on with your life. That is an understandable thought, but it is also a costly one. When you pay a collection account, you are changing the status of the account from “in collection” to “paid collection.”

But in either case, the account is still considered negative and the credit scoring model will count it against you for the full seven years.

Collectors know this, which is why they are always trying to get consumers to pay without disputing anything. Through letters and lawsuits, they attempt to create a false sense of urgency for consumers to pay before they have time to assess whether the debt is legitimate, whether they actually owe it, or whether the balance is accurate. The entire business model for the debt collection industry is built around consumers not knowing they have a choice.

Further, if a debt collector is willing to negotiate a settlement and accept less than the full balance due, why on earth would you pay the full amount? Their willingness to accept less is a tacit admission that the balance they are pursuing is not accurate or fair.

The Inaccuracy of Credit Reporting

Studies by U.S. Public Interest Research Groups have shown that as many as 79 percent of credit reports contain errors or major mistakes. Given the fact that there is so much inaccuracy built into the system already, it doesn’t make sense to assume any collection account is automatically valid. The onus should be on the collector to prove you owe the debt, not on you to prove you don’t.

Pressler, Felt & Warshaw LLP currently has more than 700 complaints in the CFPB’s Consumer Complaint Database and 163 complaints through the Better B usiness Bureau in the last three years alone.

One consumer wrote: “This law office sued me in court even though I filed identity fraud and sent them proper paperwork, including the identity fraud report with the police station. They told me they were gonna get back to me and they never did every time I called.”

Another consumer wrote: “These people are liars. They couldn’t garnish my mom because she is on disability so they started digging in my bank account the audacity after I paid one debt in full and made payment arrangements. It’s not even my debt.”

These anecdotes, along with the rest, demonstrate a pattern of behavior that suggests verification isn’t a priority for this firm. If they are suing consumers who have already provided identity theft affidavits, why on earth would we assume they have verified the basic information in your account?

Why Debt Validation Matters

More than Simple Verification

Debt validation is more than just a way to verify whether you owe a debt. It is also a way to challenge collectors and force them to prove their case. Under the Fair Debt Collection Practices Act, collectors are required to provide consumers with verification of the debt. This includes documentation to prove the debt is valid, the amount is accurate, and they have the right to collect it.

In many instances, especially with debt that has been purchased multiple times and placed with a law firm like Pressler, Felt & Warshaw LLP, they don’t have the documentation to prove all of those things.

Debt changes hands quickly and often in the collection industry. When it does, documentation tends to get lost in the shuffle. The original creditor may no longer have access to all of the information. There may be gaps in the chain of title (which proves someone owns the debt). They may not be able to access the original contract with the consumer that lays out all of the terms.

Any one of these issues creates grounds for consumers to dispute the debt.

Credit bureaus play the role of impartial third-party in all of this. When a consumer disputes a debt, the credit bureau is required to conduct an investigation and verify the information with the furnisher. This process creates a formal mechanism that bypasses any influence the debt collector may have. It forces them to prove their case through documentation rather than simply asserting their case.

The Strength of Ignoring Collectors

One of the most powerful tools consumers have when dealing with debt collectors is their silence. Engaging directly with a debt collector in any way is fraught with danger. You may inadvertently acknowledge the debt. You may restart a statute of limitations. You may provide them information they can use against you.

But when you ignore them and instead file disputes through the proper channel, you are protecting your rights and forcing them to prove their case.

Debt collectors are trained to get information and commitments from consumers when they get them on the phone. They use urgency and fear to try and force consumers to take action in the moment rather than having time to evaluate their situation and make informed decisions.

When consumers ignore their calls and letters and instead force them to go through the formal dispute process, the balance of power shifts entirely. Instead of the collector dictating the terms and consumers reacting, the collector is forced to come to the consumer and prove their case.

Why You May Need Professional Help

Information Imbalance

Collectors do this for a living. They understand the legal system and process. They understand the credit reporting ecosystem and how leverage is applied. Most consumers only deal with the collection process once or twice in their entire life. This information imbalance creates a power imbalance that is difficult to overcome without help.

Professional credit repair specialists live and breathe this stuff. They understand what types of documentation requests work. They understand which types of disputes are most effective. They understand how to identify legal violations that consumers can use as leverage. They understand the particular weaknesses of high-volume filers like Pressler, Felt & Warshaw LLP and how to exploit them.

The DIY Trap

If you try to handle collections on your own, you will undoubtedly learn a lot about the process. But you will also probably make expensive mistakes along the way. You may not know which types of disputes to file or how to word them. You may not know which pieces of documentation to request. You may miss deadlines that would have preserved your rights. You may engage with the collector in ways that weaken your position.

This is not a minor problem. A collections account can stay on your credit report for seven years. That can dramatically impact your ability to qualify for mortgages, auto loans, apartments, or even jobs. The difference between a successful dispute strategy and an unsuccessful one could be tens of thousands of dollars in interest payments over time.

The Bottom Line

Pressler, Felt & Warshaw LLP only gets as big as it is by counting on consumers not knowing their rights. Through their long history of regulatory infractions, defective documentation, and mistaken identity, it’s clear that their accounts are not always accurate. That means collections accounts from this firm can be disputed and removed if they are inaccurate, if the collector can’t verify the debt, or if they fail to meet their obligations under the law.

The first step toward taking control is recognizing you have options before you pay a collections account. Disputing the account through the proper channel forces the collector to prove their case rather than simply asserting it. Working with professionals who understand the system is the best way to ensure you come out on top.

Don’t let Pressler, Felt & Warshaw LLP push you around.

Contact FightCollections.com today for a free consultation. Our specialists understand the weaknesses of high-volume debt collection law firms like this one and how to dispute their accounts successfully.