If you are dealing with a collection account from Suttell & Hammer on your credit report, you likely feel frustrated and anxious about how to resolve it. You may be embarrassed or feeling overwhelmed by the emotional consequences of dealing with collection accounts.

These feelings are valid, but you should know that these reactions are what the collection agency is counting on when they report this information to the credit bureaus. A collection account is an effective way to keep a low credit score for years, which limits your credit options.

We can show you the best way to deal with Suttell & Hammer so that you can feel secure in the knowledge that you are doing everything possible to take care of the situation.

Who is Suttell & Hammer, P.S.?

Suttell & Hammer, P.S. (also known as Suttell, Hammer & White, P.S.) is a debt collection law firm based in Washington. The law firm collects consumer debts on behalf of major clients including:

- Discover Bank

- Bank of America

- Capital One

- Citibank

- American Express

- Chase

Their practice focuses on credit card debt, auto loan debt, mortgage debt, and consumer banking debt, typically collecting debts through litigation.

What is Suttell & Hammer, P.S.’s Customer Rating?

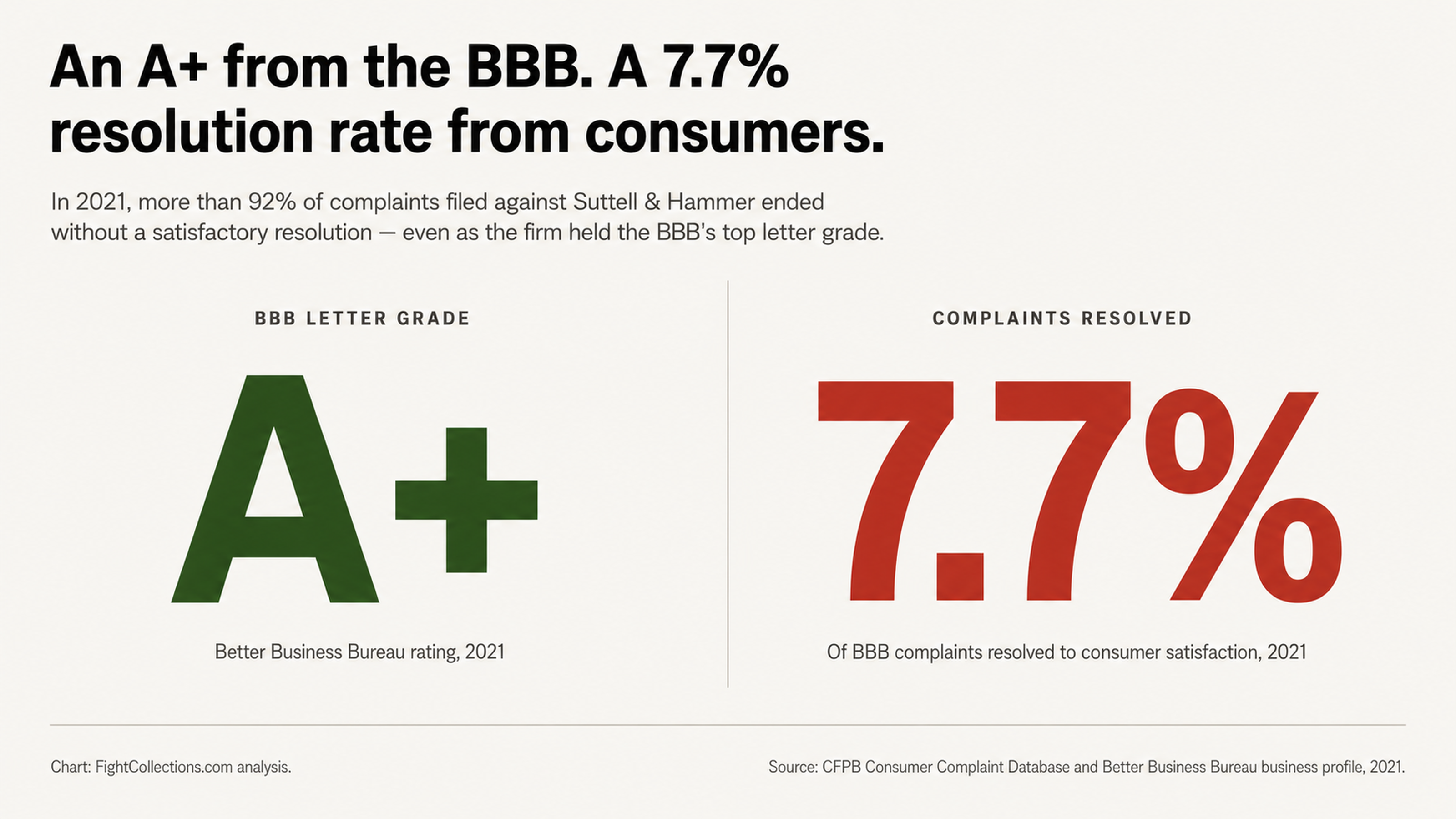

While Suttell & Hammer, P.S. is A+ rated by the Better Business Bureau, they have an abysmal rating from their former clients, with an average of only 1-star. While this is a concerning discrepancy between these two ratings, it does not necessarily imply wrongdoing or bad faith.

However, the CFPB received 12 complaints about Suttell & Hammer, P.S. in 2021, which puts them in the top 1000 most complained about financial institutions of that year. This is concerning because in the same year, they only successfully resolved 7.7% of the complaints that the BBB received about them.

This means that over 92% of the people who complained about Suttell & Hammer, P.S. did not receive a satisfactory resolution to their issue.

Why Should I Care if Suttell & Hammer is on My Credit Report?

The collection account on your credit report might be more than just a pesky little reminder of something you already knew about: an old debt you owed and were unable to pay. When this collection account is on your credit report, it can actually harm your credit score.

This is why Suttell & Hammer, P.S. may have reported the collection account to the credit bureaus. It allows them to extort money from you by placing pressure on your credit score and threatening to leave it on your report for 7 years.

When a potential lender, employer, or landlord reviews your credit report, they can see the collection account. A collection account is viewed as a serious credit issue and will significantly lower your credit score.

In some cases, simply paying the collection account might not even remove it from your credit report. You might still have the same collection account on your credit report for up to 7 years, even after you have paid it.

What’s the Big Deal if Suttell & Hammer Contacts Me?

The anxiety and stress you feel if Suttell & Hammer, P.S. contacts you about a collection account is normal and understandable. However, these feelings of anxiety and stress are exactly what Suttell & Hammer, P.S. is counting on when they contact you.

Debt collection agencies like Suttell & Hammer, P.S. use these feelings to their advantage. They know that if they can scare you into making a payment, then you will likely make that payment. This is why they may call you repeatedly, send you threatening letters and emails, and contact your friends and family members.

They are using these high pressure tactics in an attempt to scare you into making a payment. In many cases, this might actually work. The problem is that if you make a payment, you could be in an even worse position than when you started.

The debt validation letter is the best way to handle a collection account. It puts the burden on the debt collector to prove that you actually owe them money.

Has Suttell & Hammer Been Sued?

Yes, Suttell & Hammer has been sued. They were sued in Federal court in the Eastern District of Washington in November of 2013.

The court found Suttell & Hammer liable for violating the Fair Debt Collection Practices Act. The court awarded the plaintiff $2,000 in statutory damages.

The court found that Suttell & Hammer prepared and filed garnishment papers in a case that had been dismissed. They also made false representations that American Express had an unpaid judgment against the plaintiff, when in fact the original judgment against the plaintiff had been vacated.

As a result of the filing of the garnishment papers by Suttell & Hammer, the plaintiff had their wages garnished and their deposit accounts frozen.

The state court had previously awarded the same plaintiff over $9,000 in attorney fees for the wrongful garnishment.

Suttell & Hammer have also been named in two class action law suits. In the first law suit, entitled Ochoa v. Suttell, Hammer and White, the law firm was accused of sending dunning letters that threatened law suits within 5 days, creating false urgency.

In the second law suit, entitled Bjornsdotter v. Suttell and Hammer, the law firm was accused of claiming that they were entitled to a judgment against the plaintiff, and attempting to collect impermissible fees that were in excess of those allowed by state law.

What Do Consumer Complaints Say About Suttell & Hammer?

A quick review of the complaints filed against Suttell & Hammer, P.S. by consumers shows a pattern of concerning behavior.

In 2021, a consumer in Texas filed a complaint with the CFPB against Suttell & Hammer, P.S. The consumer claimed that Suttell & Hammer, P.S. had their wages garnished without providing them any notice of the collection.

When the consumer contacted Suttell & Hammer, P.S., they were told that Suttell & Hammer, P.S. “does not do any business with any resident in the state of Texas,” and that they would release the garnishment. The debt was reportedly past the statute of limitations in both states.

Another complaint filed with the CFPB describes a consumer who reported: “I got hurt and wasn’t able to work so therefore my wife didn’t pay her credit card bill because rent and food was more important to my family. These people sued us. We paid the full amount. And they still garnished my wife’s paycheck and refuse to send the release papers to her work. They sent the garnishment paperwork to her work before we had our allowed time to respond.”

In another complaint filed with the Better Business Bureau, a consumer described their experience with Suttell and Hammer this way: “After contacting them in attempt to explain hardship, case managers refused to accommodate in any situation. Shortly after our conversation, I started to receive threatening calls from unknown numbers demanding $25k to be paid by end of the week.”

What Are My Rights When Dealing with Debt Collectors?

When dealing with debt collectors like Suttell & Hammer, it’s essential to know your rights. Debt collectors are not allowed to harass you, threaten you with jail time, or mislead you by claiming to be government representatives.

The Fair Debt Collection Practices Act clearly outlines the boundaries for the behavior of debt collectors. If a debt collector has violated your rights under the FDCPA, you may be entitled to statutory damages.

One consumer filed a complaint with the Better Business Bureau after having a negative experience with Suttell & Hammer. The consumer wrote:

“The repeated visits by [process server] to my residence are harassing and inappropriate. Representatives have knocked aggressively and obnoxiously at my door multiple times. They have also spoken to pedestrians and passer by’s as recorded by our home surveillance revealing my personal name asking for my whereabouts which is a clear violation of my right to privacy.”

If a debt collector is harassing you, keep a record of all communication, including voicemails, dates, times, and details about the conversations. This information can be used as evidence if needed.

How Can I Use Debt Validation to Remove the Collection?

If a debt collector is collecting a debt from you, they must be able to verify that debt upon request. Requesting debt validation is a way to challenge the debt collector to prove that you owe them money.

It’s essential to note that debt collectors buy and sell debt frequently. The original documentation for your debt may be missing or non-existent by the time your debt has been transferred to Suttell & Hammer.

In fact, studies have shown that up to 79% of credit reports contain some kind of mistake or error. If a debt collector cannot verify that you owe them money, the debt may not be valid.

How to Remove Suttell & Hammer From Your Credit Report

It can be tempting to simply pay off a collection account and be done with it. However, paying a collection account is not always the best solution. Not only does paying a collection account not guarantee that it will be removed from your credit report, but it may also reset the clock on the statute of limitations for that debt.

Instead, it’s recommended to dispute the collection account with the credit bureau before making any payments.

If the credit bureau cannot verify the accuracy of the information on the credit report, they must remove it. This is true even if the debt is legitimate and you owe money to the creditor.

If you need help disputing a collection account on your credit report, working with a credit repair professional can be a great option. Credit repair professionals know what information to look for on a credit report to dispute and how to dispute that information with the credit bureaus.

Additionally, a credit repair professional may be able to help you avoid having to directly interact with a debt collector, which can be a significant source of stress and anxiety.

Why You Should Look for Other Errors on Your Credit Report

If you have found an error on your credit report with a collection account from Suttell & Hammer, this could indicate that there are other errors on your credit report as well.

Request a copy of your credit report from each of the 3 major credit reporting bureaus and carefully review each item on the report. Dispute any information that you find to be inaccurate or erroneous.

It’s also important to keep in mind that each of the 3 credit reporting bureaus may have different information on your credit report. Just because you have disputed an error with one credit bureau does not mean that the error will automatically be corrected with the other credit bureaus.

Risks of Settling a Collection Account

Some consumers may consider settling a collection account by making a partial payment. However, there are risks involved with this strategy.

Settling a collection account may help or harm your credit score, depending on a variety of factors, including how the account was reported. In most cases, the negative effects of a settled collection account will still remain on your credit report for up to 7 years.

Additionally, settling a collection account may create tax liability. When you settle a debt for less than the full balance, the creditor may report the difference to the IRS as income.

Finally, when you make any type of payment on a debt, you may inadvertently reset the clock on the statute of limitations. This means that even if the debt was previously too old for the creditor to sue you for, you may have given them additional time to pursue legal action against you.

Final Thoughts

Having a collection account from Suttell & Hammer on your credit report can be frustrating and stressful. However, with the right tools and knowledge, you can dispute the collection account with the credit bureau and have it removed from your credit report.

Don’t let a debt collector push you around and intimidate you into making payments on a debt that may not be yours. Know your rights and how to dispute errors on your credit report.

At FightCollections.com, we understand how to deal with collection accounts and how to dispute them with the credit bureaus. Our team is standing by and ready to help you get back on the path to good credit.