Are you seeing Enhanced Recovery Company on your credit report and is it affecting your credit score? Don’t pay them until you read this article.

There are some questions you need to ask yourself and if you find out that the answers point to certain things then you can dispute the account and potentially get it removed.

According to U.S. PIRGs, 79% of credit reports have errors or disputes on them. The collection account you are seeing may be an error and not even your debt, or there may be another error on the account that you can dispute. You should first identify who is reporting the account and what their reputation is.

Who is Enhanced Recovery Company?

Enhanced Recovery Company, also known as ERC, is a third-party debt collection agency that operated in Jacksonville, Florida for 24 years until it dissolved in November of 2023. They collected debt from major creditors such as telecommunications companies, utilities, and banks.

Here is some general information about the company:

What does their reputation say about them?

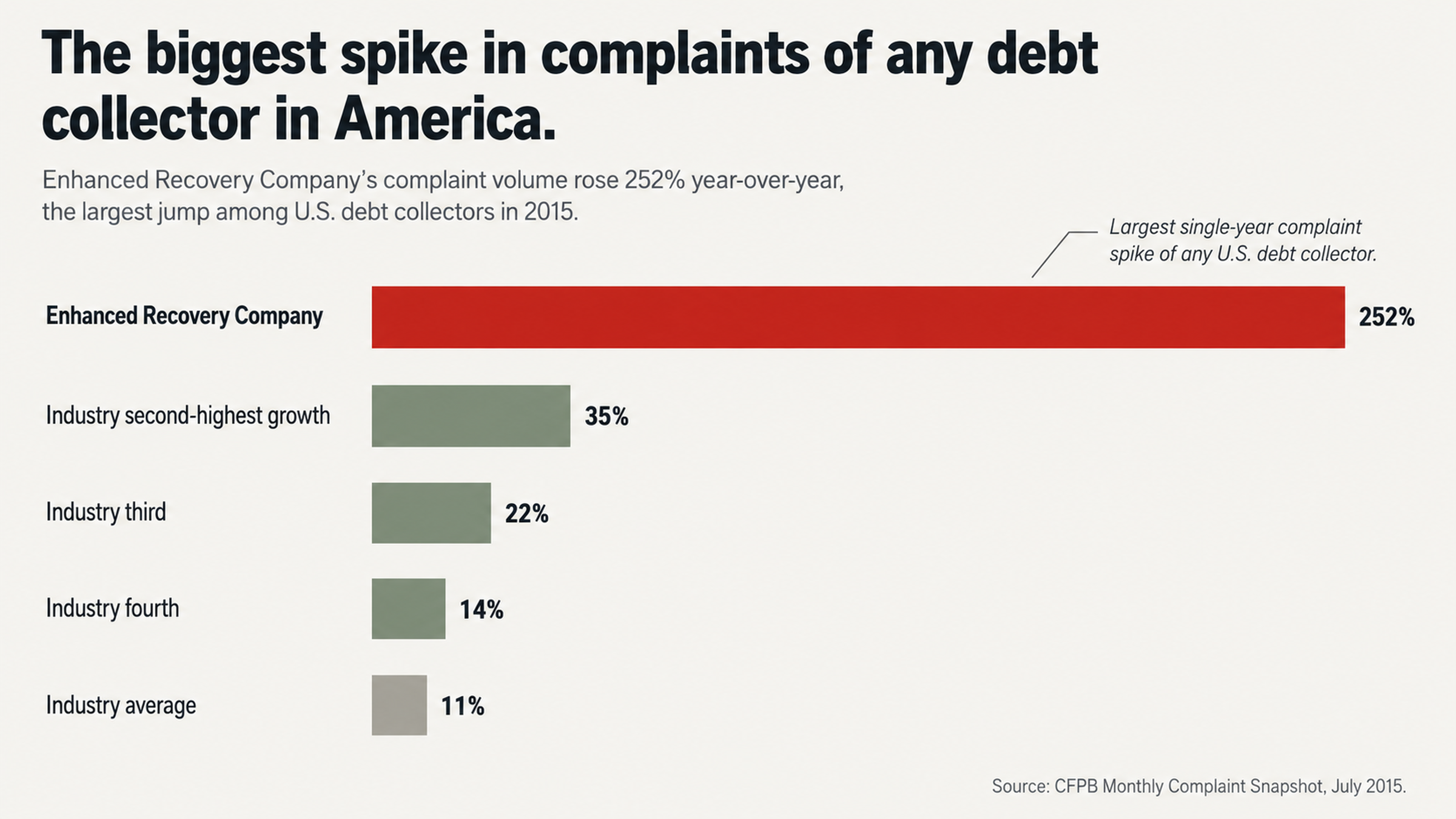

In July 2015, the Consumer Financial Protection Bureau officially declared Enhanced Recovery Company the most complained-about debt collector in America in their Monthly Complaint Snapshot. In fact, complaints against ERC increased 252 percent year-over-year, the largest percentage increase among debt collectors.

ERC racked up between 6,229 and 10,418 complaints filed with the CFPB, depending on the date, plus more than 900 federal lawsuits and a $450,000 class-action settlement over allegations it was sending deceptive and misleading collection letters.

In January 2021, the California Department of Financial Protection and Innovation subpoenaed ERC as part of an investigation into potentially unfair, deceptive, or abusive acts or practices (UDAAPs) related to debt collection activities.

This is relevant because having this many complaints and lawsuits against them shows that they are a company with a history of problems. If they have had this many issues then it is likely that your specific account may have issues with it as well.

Do you actually owe this debt?

The first thing you should figure out is if the debt that ERC has placed on your credit report is actually your debt. This isn’t a trick question. Many consumers have complained about Enhanced Recovery Company trying to collect debts from the wrong person.

How often does this happen?

In January 2017, a consumer told ConsumerAffairs that ERC contacted them to collect a debt from Comcast even though they’d never lived in an area where Comcast offered service.

When the consumer called to discuss the error, ERC admitted it had contacted the wrong person and assured them it wouldn’t affect their credit report. Instead, ERC went ahead and contacted all three credit reporting agencies, which led to a drop in the consumer’s credit score.

We see similar stories repeated throughout ERC’s complaint history: consumers saying the company is trying to collect the wrong debt then refusing to correct the credit reporting agencies when they find out their mistake.

This is a big deal because the Fair Credit Reporting Act (FCRA) says that any information reported to the credit bureaus must be accurate. If a debt collector is reporting a debt that isn’t yours, they’re breaking federal law, and you may have grounds to dispute the debt and get it removed.

If the debt isn’t yours, you already have grounds to dispute it. Remember, the burden of proof isn’t on you: the burden is on the collector to show that the debt is yours and that they have a right to collect it. If they can’t do that, the account should be removed.

Is this identity theft or a mixed file?

If you didn’t apply for the debt showing up on your report, it’s possible that you’re a victim of identity theft or a mixed file error, where someone else’s information gets mixed up with yours. Both are more common than you might realize, and both can be grounds to dispute and remove a collection account.

Do you recognize the original creditor listed on the collection account? Did you ever have an account with that company? Does the amount look familiar? If none of those things sound right, you may be looking at either fraud or a credit reporting error.

Can the debt collector prove you owe the money?

Even if the debt was yours at some point, that doesn’t mean the collector can prove it. Debt gets sold and resold so many times that documentation is often lost along the way. So the real question isn’t, “Did you owe money at some point?” The question is, “Does this debt collector have the documentation it needs to prove that you owe this debt?”

What happens when debts get resold?

When original creditors sell debts to debt buyers or assign debts to collection agencies, they often do it in bulk spreadsheets with minimal documentation. The signed contracts, account statements, and payment records that would establish the debt is valid typically aren’t transferred with the debt.

The Fair Debt Collection Practices Act (FDCPA) says you have the right to request debt validation, which means the collector has to provide documentation establishing that: You owe the debt. The amount is correct. They have the right to collect the debt.

Many collectors, especially ones with troubled track records like ERC, can’t provide that documentation when consumers ask for it. Remember that ERC paid a $450,000 settlement in a class-action lawsuit that claimed the company was sending deceptive and misleading collection letters that didn’t make it clear if paying a settlement would actually resolve the debt.

If ERC couldn’t manage to communicate the terms of a settlement clearly, it seems likely that they could have a hard time documenting the debts they’re collecting, too.

What are your rights?

The Fair Credit Reporting Act (FCRA) and the Fair Debt Collection Practices Act (FDCPA) aren’t just laws you can use for defense. They give you powerful tools you can use to dispute and remove debts from your credit report. When a collector can’t validate a debt within a reasonable amount of time, or when they report bad information, or when they violate the rules for collection, they’re giving you grounds to remove the debt.

Some consumers don’t realize that these laws impose a lot of affirmative obligations on collectors and credit reporting agencies. The collector is supposed to be able to substantiate their claims. The credit reporting agency is supposed to investigate any disputes within 30 days. And if they can’t do either one of those things, they should delete the disputed account.

Why Paying This Debt Would Be a Mistake

It’s their job as a debt collector to scare you into paying. They might try to convince you that if you don’t pay the debt immediately, your credit will be permanently ruined. Don’t believe them.

Will Paying a Collection Improve My Credit?

There’s no bigger myth in the consumer finance space than paying a collection will improve your credit. Paying a collection simply changes the status of that account from “unpaid” to “paid.” The account will remain on your credit report for the full seven years from the original date of delinquency, and it will continue to hurt your credit score the entire time.

Making a payment can also restart some clocks that were working in your favor. In some states, making a payment or even admitting that you owe a debt will restart the clock on the statute of limitations for a lawsuit. You could actually give a debt collector more power to sue you if you make a payment without knowing your rights.

Are There Any Laws That Protect Me From Debt Collectors?

Debt collectors will often threaten that if you don’t pay, they'll garnish your wages, levy your bank account, or take some other extreme action to collect the debt. What they don’t tell you is that state and federal laws exempt most consumers from all of those actions. You have more protection from debt collectors than you think.

Before you make any decision about how to proceed, you need to understand what a debt collector can and can’t do to you under your state’s laws. The threats and implications in a collection letter or phone call are often exaggerated or don’t apply to your situation at all.

What Should I Do Instead of Paying?

Instead of paying a collection, you should dispute it and never pay unless you’ve confirmed that the debt is both valid and currently collectible, and that you can’t get it removed. That approach flips around the typical process in favor of the consumer. It places the burden of proof where it belongs — on the debt collector.

Why Should I Dispute Instead of Negotiate?

If you negotiate with a debt collector, you’re essentially admitting that you owe a debt, and that the debt collector has the right to collect it from you. You’ve given up your most powerful negotiating tools before the conversation has even started. The debt collector has already accomplished his goal — getting you to admit that you owe the debt — and now he holds all the cards in a potential payment negotiation.

Disputing the debt flips that script entirely. Instead of trying to defend yourself from a debt collector’s pressure tactics, you’re forcing the debt collector to prove his case.

Given ERC’s history of attempting to collect from the wrong people, mis-reporting information to the credit bureaus, and being investigated for unfair and deceptive practices, the chances that any given account has a problem with documentation are pretty high.

The Consumer Financial Protection Bureau has received complaints about ERC refusing to validate debts when they were legally required to do so.

One consumer even complained that after she requested validation of a debt, ERC continued to report that debt to the credit bureaus every month even though it had no documentation to prove the debt. Those practices suggest that ERC may have routine problems with verifying its accounts, which could make disputing ERC accounts a fruitful effort for consumers.

Why Should I Consider Getting Help?

Debt collectors do this for a living. They know all the laws and loopholes and pressure tactics to get consumers to pay up. Most consumers have never dealt with a collection account before, and are at a significant disadvantage.

Credit repair specialists deal with collection accounts every day. They know which types of documentation debt collectors are most likely to have problems with. They know which types of disputes are most likely to succeed. And they know how to navigate the debt validation process to improve the chances that accounts are completely removed.

While you can certainly try to dispute ERC accounts on your own, you may have a better chance of success if you get some help.

The stakes are high — a collection account can cost you 100 points or more on your credit score and will stay there for seven years. Paying for some help may be a lot cheaper than continuing to pay the price for a poor credit score.

What if I Only Find One Inaccuracy?

If you go through the above process and find one inaccuracy with an ERC account on your credit report, don’t stop there. One inaccuracy should cause you to dig even deeper.

Should I Also Dispute Other Items on My Credit Report?

Inaccuracies on credit reports usually aren’t isolated to a single account. If ERC was incorrectly reporting information for one debt you may owe, it’s entirely possible that other debt collectors were incorrectly reporting information for other debts you may owe.

If you pulled your credit reports as part of your investigation of an ERC account, pull them again and scrutinize every negative account. If you see any accounts you don’t recognize or amounts that aren’t accurate or dates that don’t make sense, it’s worth challenging.

How Do I Avoid Problems Like This in the Future?

Once you’ve solved the current problem with the ERC account on your credit report, you can think about how to avoid the problem in the future. That’s an education in how to manage your finances so that you don’t have to deal with debt collectors at all. But for now, we need to focus on cleaning up the damage that’s already been done. (Once we’ve done that, we’d be happy to give you a crash course in how to avoid collection problems going forward.)

The strategies we talked about here can also help you identify and challenge future inaccuracies before they become a problem.

Conclusion

Enhanced Recovery Company had compiled one of the worst reputations of any debt collector in the country before it dissolved in 2023. It was named the worst debt collector in America by the Consumer Financial Protection Bureau. It faced more than 900 federal lawsuits. And it was investigated by regulators in California for potentially unfair or deceptive practices. Any time you see an ERC account on your credit report, you should approach with caution before you do anything else.

The questions you ask in this moment will determine whether that account continues to haunt your credit report for seven years or whether you can get it removed altogether. Do I really owe this debt? Can the debt collector prove it? What are my legal rights that I might not be aware of? The answer to those questions will often tell you that you have a lot more power in this situation than the debt collector wants you to know about.

Take Action Today

You shouldn’t let a debt collector with this kind of history continue to drag down your credit report without putting up a fight. Whether the debt isn’t yours, or whether the account isn’t being reported correctly, or whether the debt collector simply can’t verify that it has the documentation to prove you owe it, you have reason to challenge the account.

At FightCollections.com, we specialize in challenging accounts like this that are inaccurately reported on consumers’ credit reports. We know all of the documentation vulnerabilities that debt collectors face. And we know how to use federal consumer protection laws to help consumers get the outcome they deserve.

Get in touch with us today for a free consultation about the Enhanced Recovery Company account on your credit report. We’ll evaluate your situation. We’ll help identify potential inaccuracies that you might not see on your own. And we’ll walk you through the process to challenge the account and improve your credit report.

The debt collection industry counts on consumers not knowing their rights. It’s time to prove them wrong.