Seeing BC Services on your credit report is meant to scare you into making a quick payment.

But before you panic, remember that they’ve been in the debt collection business since 1925, which means they’ve had nearly a century to perfect their scare tactics. The Longmont, Colorado-based company has been sued roughly 100 times for violating federal debt collection laws, so they’re clearly not afraid to push the limits. But that’s exactly why you shouldn’t make a move without reading this article.

You may not know it yet, but there are reasons you don’t have to pay BC Services, at least not right away. For one thing, 79% of people have errors on their credit reports, according to a study conducted by U.S. PIRG. You could be one of them, which means you might not actually owe anything to BC Services, even if you do owe something to the original creditor.

Don’t worry if that doesn’t make sense yet. You’ll get a clearer understanding of your options after you finish reading this article.

So, who is BC Services?

What is BC Services?

BC Services, Inc. is a third-generation family-owned debt collection agency. Founded in 1925 as Bonded Collection Service, Inc., they changed their name to BC Services in 1998. They collect mostly medical debt and operate out of Longmont, Colorado. They claim to be one of the largest collection agencies in the country, with annual revenues estimated to be around $54.3 million.

The investigation

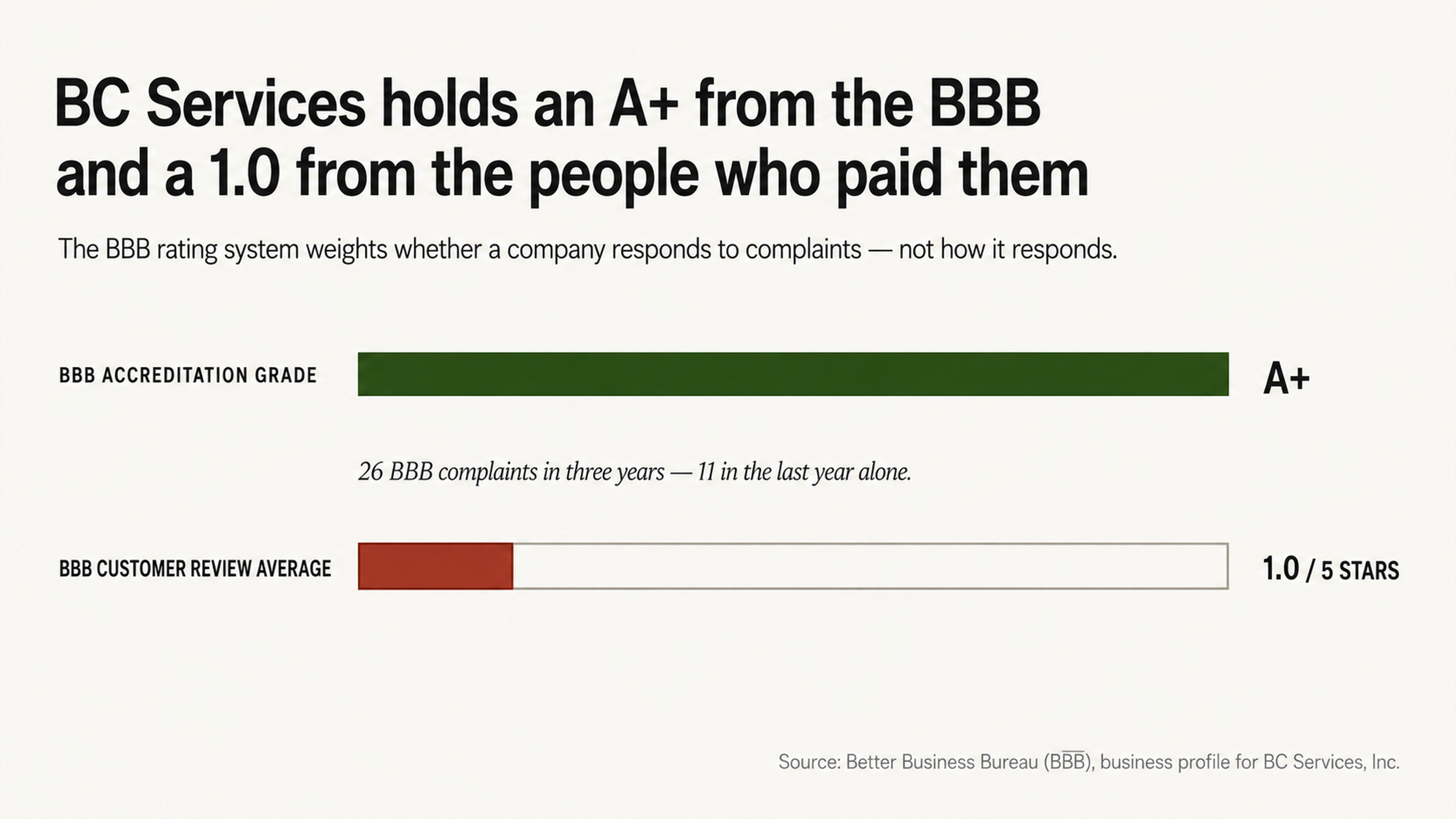

As we dug into BC Services’ business practices, we found they maintain an A+ rating from the Better Business Bureau (BBB), despite only having 1 out of 5 stars based on customer reviews. This disparity is possible because the BBB rating system places more emphasis on whether the company responds to complaints than how the company responds to those complaints.

So, as long as BC Services answers the phone and says something, even if it’s just a form letter, they can maintain a high rating even if their customers hate them.

In the last three years, they’ve had 26 complaints filed against them with the BBB, 11 of which happened in the last year. The majority of complaints involve:

Problems with interest, fees, or other charges (undisclosed interest and fees added to debts)

Issues with communication tactics (texts and robocalls)

Failure to validate debts

Issues with employee conduct

They’ve also been sued roughly 100 times in federal court for violating debt collection laws.

What BC Services is counting on

They expect you to panic and pay

When BC Services shows up on your credit report or calls you on the phone, they expect you to panic. They’re hoping to scare you into paying without asking questions or requesting proof of the debt. The faster you pay, the less likely you are to scrutinize what they’re asking for. Debt collectors make their money by using urgent language and creating a sense of crisis in consumers, hoping they won’t push back.

For instance, a consumer complaint filed with the BBB in March 2025, states that a representative from BC Services told her, she needed to set up a payment plan of no less than $200 a month, and if she couldn’t afford to pay that much she should just set it up anyway, that they would find out where she worked and subpoena her to court.

This threat uses the fear of court action, but lawsuits are extremely rare in debt collection. Credit reporting agencies can only report negative credit information for seven years, so the odds are ever in your favor if you approach the situation logically instead of emotionally.

They assume you won’t verify the debt

If BC Services is trying to collect from you, they expect you to take their word for it. They have no obligation to show you proof of the debt before it gets reported to the credit reporting agencies. In fact, the credit reporting system is designed to operate on the assumption that you owe what the credit report says you owe unless you tell them otherwise.

In November 2025, someone filed a complaint with the BBB saying that BC Services texted her to inform her that she owed them $348. She called to ask for an explanation of the charges (a medical debt), and they increased the amount to $394 and told her they added interest because it was a bill in collections. She never received any letters and the services were from two years prior.

If they’re willing to negotiate the amount they say you owe or tack interest onto the balance, it’s clear that what they initially say you owe might not be entirely accurate. In many cases, the balances are inflated, miscalculated, or even fabricated.

Verifying the debt is not optional — it’s mandatory.

The paper trail problem

Inaccurate or missing documentation

When you owe a debt to the original creditor, it creates a paper trail. However, when the debt gets sold to a collection agency like BC Services, that paper trail often ends. Collection agencies buy debts in bulk — sometimes thousands of accounts at a time — for pennies on the dollar. Once the debt is sold, the original creditor no longer has a vested interest in collecting it, so you shouldn’t feel obligated to pay it.

The debt-buying model means that BC Services may not have access to the contract you signed, statements from your account, or any other paperwork necessary to establish that you owe the debt they’re trying to collect. Without proper documentation, the information they report to the credit reporting agencies may be inaccurate, incomplete, or unverifiable.

In a federal court case (3:20-cv-00863-slc) in the Western District of Wisconsin, the plaintiff alleged that BC Services reported a disputed debt to the credit reporting agencies without indicating that it was in dispute. Under federal law, once you dispute a debt, the credit reporting agencies can’t list it unless the creditor can verify that it’s valid.

In some cases, this means the debt can be removed altogether.

Collecting the wrong debt or collecting from the wrong person

In April 2025, someone filed a complaint with the BBB against BC Services, claiming that a representative from the company called her, identifying himself as being from a children’s hospital. The caller never identified himself as an employee of BC Services but presented himself as an employee of the hospital. When the consumer called both of the hospitals he mentioned, neither of them showed that she owed a balance or that anything had been sent to collections.

Not only does this conduct appear to violate federal debt collection laws, which require debt collectors to identify themselves, but it also demonstrates how frequently collection agencies attempt to collect debts from the wrong people. Whether it’s a mix-up with names, an error in their system, or because you already paid the original creditor, consumers frequently don’t owe debts that collectors are trying to collect.

If BC Services can’t establish that you incurred the specific debt they’re trying to collect, they don’t have a legitimate claim. The burden of proof is on them, not you.

The Secret Power of Not Talking

Why Speaking With Them Directly Hurts Your Case

BC Services is counting on you to make a phone call, give your personal and sensitive information, and negotiate over the phone, which always favors their interests. Every single time you speak with a debt collection agency, they can gather more information from you, restart the clock, or coerce you into agreeing to something that you can’t afford.

Anything you say can be twisted and distorted. Making a partial payment can be considered as admitting that you owe the full amount. Even casual comments about your income or expenses can be used as a gauge for the level of harassment they will inflict.

When you’re on the phone with a debt collector, they always have the upper hand with the information they have, or don’t have. In a written letter, you create a paper trail that protects you. When you don’t say anything about your situation, you maintain the upper hand. When you hire a professional, you guarantee that only the type of communication that is in your best interest will happen.

The Harassment M.O.

According to consumers who have dealt with this agency, BC Services has been accused of contacting consumers in ways that may be illegal. In a complaint filed with the BBB in Sep 2025, the consumer accused them of calling with a robotic autodialer and sending texts even though they never gave permission, and claimed they never received anything in the mail about the debt, and that the agency was violating their rights.

In perhaps the most egregious complaint, in Aug 2025, one consumer claimed that BC Services was calling a crisis hotline for kids and interrupting an emergency hotline. The consumer claimed that they previously informed the agency that they were on a do not call list, and said the collectors don’t seem to hear you and don’t seem to care what they are doing.

These types of complaints show a clear pattern of potentially illegal behavior from the agency. If you’re experiencing this type of abuse, make sure to document everything if you need to prove illegal collection activity.

The Pitfall of Paying

Why Paying a Collection Agency Can Damage Your Credit

The collection agency is hoping you’ll pay them, and once you do, they’re done with you and you’ll never hear from them again.

What most consumers aren’t aware of is that when you pay a collection agency, it does not mean that the account will be deleted from your credit report. The status of the account will be changed from unpaid to paid, but the negative account will still be visible on your credit report for 7 years from the original delinquency date.

In some credit scoring models, when you pay off a collection, it can actually re-age the collection, meaning that the impact of the negative hit is recalculated like it’s a brand new negative hit. You pay them money to appease them, but in return you don’t get the results you’re expecting on your credit report. The collection is still a negative mark, paid or unpaid.

This is why you should always dispute any potential inaccuracies before you consider paying. If the collection can be completely removed because of inaccuracy, error, or non-verification, that is a far better outcome than paying money on a collection that may or may not be accurate.

The Court Summons

BC Services Allegedly Using Court Summons as Intimidation

We’ve seen several documented instances where BC Services is using the threat of a court summons to coerce consumers into paying.

One consumer law firm aggregated a complaint from a consumer who claimed that after speaking with the medical provider who acknowledged that they made an error, and emailing the agency to inform them of the mistake, three months later they received a court summons in the mail, where BC Services claimed that they left five voicemails, which the consumer said was completely untrue, and that the only way to avoid the court was to pay the full amount plus a service fee.

On the BBB website, one consumer claimed that after contacting the agency multiple times to inform them that the medical debt was for their child, the agency sent a police officer to their home to serve them a court summons. The consumer claimed that they filed a complaint with the AG, and that ultimately they paid over $10,000 and were still charged for the court summons.

Threatening to take you to court is just that—a threat. Once you realize that court summons aren’t the end of the world, and that you have rights whenever you end up in court, the agency loses their power.

Why DIY Often Fails

BC Services has been around for nearly a century. They have seen every single letter ever written by consumers. They know exactly what the credit reporting agencies need to consider a dispute valid. They have entire departments dedicated to complying with federal regulations as well as entire law firms on retainer.

When you try to dispute a debt on your own, you’re taking on an entire corporation with nearly a century of experience and over 150 employees whose only job is to collect debts and manage disputes. You’re on your own.

A professional credit repair expert has experience with the language that works in a dispute letter, they know when and how to time disputes, and they know the specific pressure points of collection agencies like BC Services. They know how to use the 100+ federal lawsuits against BC Services as proof that the reason for the removal of the collection is due to a pattern of abuse.

Their Weakness is Your Strength

The lawsuits and complaints filed against BC Services is a blueprint for their weaknesses. They have been sued for failing to validate, misrepresenting their identity, tacking on extra fees, violating communication preferences, and attempting to collect from the wrong person. Each one of these items is a potential point of dispute.

The FDCPA violations that have been alleged in federal court in CO, IL, and WI demonstrate a pattern of behavior that may have happened to you as well. When you have evidence of a pattern of behavior, it helps strengthen your dispute because you can show that you’re not just a single consumer complaining about an individual incident, but rather part of a pattern of behavior.

A credit repair expert will know how to use this information to your advantage, how to demand the proper validation, and how to follow up when the agency’s initial response was insufficient. Instead of the information gap always favoring the debt collector, it now favors the consumer.

In Conclusion

BC Services has almost 100 years of experience in debt collections. They know how to play the game and they expect you to play along. They expect you to be afraid, confused, and cooperative. They expect you to not validate the debt, not know your rights, and not hire a professional. Everything about their business model relies on consumers behaving in a certain way.

But the minute you break the script and behave in a way they don’t expect, you gain the upper hand. When you dispute instead of pay, when you maintain your silence instead of engaging, and when you hire a professional instead of trying to DIY, you are behaving in a way that does not make their business model work.

A collection account can be removed from your credit report if the information is inaccurate, a mistake, a fraud or if they cannot verify the account within a reasonable amount of time. With BC Services’ history of failing to validate, misrepresenting their identity and violating federal and state communication laws, there may be a reason to remove the account that you would never have found without doing an investigation.

What are you waiting for?

Get Help With BC Services

You don’t have to go up against BC Services on your own. At FightCollections.com, we specialize in representing consumers who are being harassed by debt collectors who have placed false or inaccurate information on their credit report. We know the games they play and exactly how to get them to stop.

When you work with a professional, you’re leveling the playing field. Instead of trying to navigate a complex set of consumer protection laws on your own, you have someone in your corner who does this every single day and knows what works and what doesn’t.

Contact us at FightCollections.com today to discuss your BC Services account and find out how a professional credit repair expert can help you with your situation.

The choice is yours. You can continue to react the way BC Services expects you to, or you can respond the way that works to your advantage. Your credit report is far too valuable to leave up to chance.