Have you discovered an unrecognizable collection account on your credit report? If the account is under Wilshire Consumer Credit, your initial skepticism is warranted.

There is a regulatory record on this company that you might want to understand before taking any action. You might be able to identify some warning signs embedded in a Wilshire Consumer Credit listing that would help you resolve this issue. Let’s find out what to look for.

Who is Wilshire Consumer Credit?

Wilshire Consumer Credit is a Los Angeles-based auto title lender and debt collector that operates as a subsidiary of Westlake Financial Services. It is a part of the Hankey Group of Companies. The company provides subprime auto financing and title loans to consumers who cannot obtain credit through other means.

Contact Information

Wilshire operates in the following states for title loans: California, Utah, Arizona, New Mexico, Georgia, and South Carolina.

Wilshire offers unsecured personal loans in 35 states. The company is in the business of making high-interest loans to consumers with bad credit.

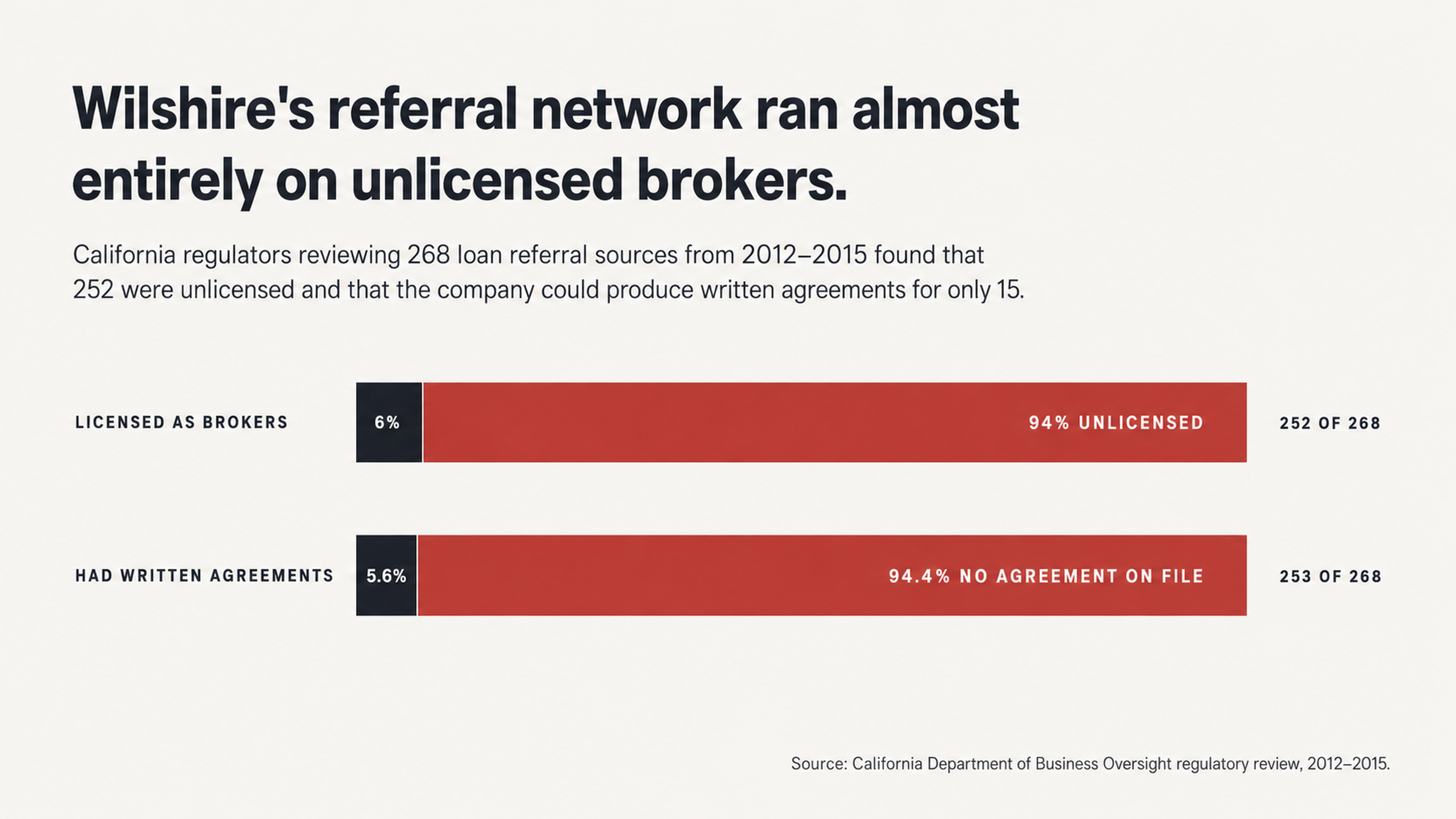

History of Regulatory Actions

In September 2015, the Consumer Financial Protection Bureau (CFPB) ordered Wilshire Consumer Credit and its parent company to pay $48.35 million in penalties and consumer relief.

The reason was that the CFPB investigators found that the company’s debt collectors used a web-based service called 'Skip Tracy' to misrepresent caller ID information. The collectors pretended to be repossession companies, pizza delivery services, flower shops, or even borrowers’ family members. They pretended to be calling from “Investigation Division” or “Enforcement Division” and threatened borrowers with criminal prosecution.

Another regulatory agency, The Department of Justice, found that the company was specifically targeting junior enlisted service members for loans and then repossessing their vehicles without first obtaining a court order as required by law. As a result of these actions, the company agreed to pay $760,788 in 2017 and an additional $225,460 in 2022 after a compliance monitor found ongoing violations.

Regulators in California discovered that from 2012 to 2015, approximately 32 percent of the company’s loans came from unlicensed brokers. Of 268 companies and individuals who were paid for loan referrals, 252 were not licensed as brokers. These failures in basic compliance procedures suggest that there may be issues with the accuracy and verifiability of debts that the company reports.

Warning Signs That Indicate Your Wilshire Consumer Credit Collection Account Is a Problem

Not every collection account is legitimate. According to U.S. PIRGs, 79 percent of credit reports contain errors or other mistakes. We can help you identify some warning signs in a Wilshire Consumer Credit collection account listing that may indicate that you have the basis for a successful dispute.

Inconsistent Dates

You can find the relevant dates on a collection listing. Inconsistent dates on a collection account can point to a problem. Here are the dates you need to check: the date the original account was opened, the date the original account became delinquent, and the date that Wilshire Consumer Credit placed the account for collection.

The dates should tell a coherent story. One common problem with dates on a collection account is the date of first delinquency. This is the date that controls how long the collection account can stay on your credit report. If the date of first delinquency is altered or reported incorrectly, the collection account may appear to be younger than it really is.

In the CFPB’s enforcement action against the company, the Bureau found that the company’s debt collectors were changing the due dates on loans without the borrowers’ knowledge or consent. The change in the due date caused additional interest to accrue.

But the collectors told the borrowers that the change was in their best interest. If the dates on your credit report do not match the dates in your records, that may indicate a problem that is worth exploring.

Lack of or Incomplete Account Information

A legitimate collection listing should contain specific information about the original account. If some of the information is missing or unclear, it may be a sign that the debt collector does not have the information it needs to verify the debt. Here are the pieces of information you need to check: original creditor, exact balance, original account number, and type of debt.

If any of these pieces of information are missing or unclear, the debt collector may have difficulty verifying the debt if you dispute it. In the California regulatory action against the company, the regulators found that the company could only produce agreements for 15 of its 268 loan referral sources.

Consumers who have interacted with the company report that it is difficult to get accurate information about their accounts. One reviewer reports the following: “When you call in to pay off your loan, they purposely leave one payment unpaid. This results in you being unaware of any remaining debt at the end of the term. Then they start adding late fees and interest. They also report you to credit agencies without notice.”

This kind of unclear accounting may create an opportunity to dispute the debt.

The Hidden Danger of Paying This Debt Collector

Paying a debt collector can feel like the best way to get a collection account off your credit report. But paying a collection listing without first verifying its accuracy may be the worst decision you can make.

The Payment Trap

When you pay a collection account, the listing is updated to show that it is a 'paid collection.'

Unfortunately, that is all that happens. The listing does not disappear. You have confirmed that the debt was legitimate. In exchange, you have gained almost nothing. The paid collection listing will stay on your credit report for the full term. It will continue to affect your credit score and harm your ability to get good interest rates on loans and credit cards.

Wilshire Consumer Credit offers interest rates ranging from 34.99 percent to 199.99 percent APR, depending on the state. Some consumers report that despite years of payments, their loan balances never seem to go down.

One consumer reports that when she made a $273 payment, only $5.05 went to principal and $267.96 went to interest. If you pay a debt like that without first challenging its accuracy or the balance, you are confirming that it is a legitimate debt.

In some states, making a payment or even acknowledging a debt can restart the clock on the statute of limitations. That can give a debt collector the ability to sue you again even if the statute of limitations had run. But if you say nothing, the clock continues to run. That is why silence is golden.

What Happens When You Call to Pay

Debt collectors have more information than consumers about the debt they are collecting and about consumers’ rights and options. When you initiate a call to a debt collector to talk about a payment, the debt collector is going to ask you a series of questions. The questions are designed to elicit as much information as possible from you that the debt collector can use against you.

We know that debt collectors from Wilshire Consumer Credit have impersonated others and used fake division names to get borrowers to talk. If you initiate contact with collectors who have those kinds of tactics in their playbook, you put yourself at a disadvantage. But if you remain silent and force the debt collector to verify the debt, you have the advantage.

Instead of calling the debt collector to pay, you can challenge whether the information it is reporting is accurate and verifiable. In some cases, you can get a collection removed because the information is inaccurate, erroneous, fraudulent, or not verifiable within the required amount of time. Instead of just updating the status of the listing, you can force the debt collector to fix the problem.

If you have Wilshire Consumer Credit on your report, don’t panic. However, you should take it very seriously. Here’s what you need to do:

Red Flags For Inaccuracies In The Collection Report

Inaccuracies in collection reports are not anomalies. They are standard operating procedures for an industry that deals with debt as a commodity, often passing debt with partial documentation between buyers. Knowing where to find the anomalies will help you have a better chance of success.

Incorrect Or Missing Documentation

Debt is sold multiple times. With each sale, there is the potential that documentation is lost, destroyed, or altered. Original loan documents, payment records, account statements, etc. may not make it to the next buyer. If you dispute the debt, they may not have the documentation to show that the debt belongs to them or that the amount is correct.

During the California regulators review of Wilshire, the company was not able to provide documentation for the vast majority of its broker relationships. If the company cannot maintain the documentation on their business relationships, how can you trust that the documentation for your account is complete? Missing or incorrect documentation is a common dispute reason.

Inconsistent Information

Take a look at the entry on your report and compare it to the information you have. If you don’t recognize the amount, the account number, or the creditor name, dispute it. This could indicate missing or incorrect documentation.

Wrong Consumer

The collection may not even be on the right report. Many people share the same names, live at the same address, have similar social security numbers, etc. This is not identity theft, but it will have the same impact on your credit. If there is a collection showing up that you don’t recognize, there is a good chance it belongs to someone else.

If the collector cannot verify that you are the actual debtor, they should not report it. If you investigate the debt yourself, you may inadvertently provide them the verification they need. If you hire a third-party company, they will be able to investigate without the risk of verifying the debt. Multiple disputes on the same debt will not hurt your credit report any worse than the original collection account, so there is no risk of using a third-party company.

What To Expect From Wilshire Consumer Credit

Wilshire Consumer Credit is a legitimate collection agency, but they are likely to use every trick in the book to try to get you to pay. Here’s what you can expect:

Wilshire Consumer Credit is a legitimate company. They are not a scam. But, they will be relentless.

Why Use A Professional?

You will likely be unable to match the resources and expertise that a collection company has. However, a professional credit repair company can help.

There is a process to disputing credit report information. A credit repair company will follow this process and ensure that everything is done correctly. A credit repair company will know exactly what your rights are and what the laws are. They will know what information you should provide and what information you should not provide. They will also know what the credit bureaus and the collection agencies are required to do.

A professional will be able to navigate the process better than you can. Using a credit repair company is the best way to get the collection removed. They understand the process, the laws, and your rights.

Don’t Contact Wilshire Consumer Credit Directly

You should never contact Wilshire Consumer Credit directly. This will only lead to you providing more information than you should, which will allow them to verify the information and strengthen their case against you.

By hiring a professional, they will act as an intermediary between you and the collection agency. All communication will be in writing, which will provide a paper trail of everything that happens.

A credit repair company will know exactly what to ask for, and what information should be provided. They will not provide any information that will strengthen the other party’s case. They will focus on finding inaccuracies and ensuring that the creditor follows all applicable laws.

The best way to protect yourself is to hire a professional. They will act as a buffer between you and the other parties. They will ensure that your rights are protected and that the creditor follows the laws.

What’s The Worst That Could Happen?

In the worst-case scenario, if the collection agency can verify the information, it will remain on your report.

However, if you dispute it yourself, you may inadvertently provide the information they need to verify the debt. If you hire a credit repair company, the worst thing that could happen is the information will remain on your report. A credit repair company will be able to verify the information without the risk of providing information that the collection agency needs.

Why Use A Credit Repair Company?

The biggest advantage to using a credit repair company is the knowledge and expertise they have. Here are some other reasons to consider:

They will save you time: Disputing credit report information can be time-consuming. By hiring a credit repair company, they will handle everything for you.

They will save you money: If the credit repair company is successful in removing the derogatory information from your report, it could save you money in the long run.

It will be less stressful: Credit repair companies have the expertise to navigate the process. They will handle the stress for you.

Conclusion

Wilshire Consumer Credit has been fined nearly 50 million dollars for their business practices. If you have an account with them on your report, you need to take it seriously. However, before you pay it, make sure it’s valid. Look for the red flags such as incorrect dates, incorrect balances, missing information, etc. If you find anything, dispute it. Make sure they verify the information.

If you’re not comfortable disputing the information yourself, hire a credit repair company. They have the expertise and the knowledge to navigate the process and ensure that your rights are protected. Don’t contact Wilshire Consumer Credit directly. This will only allow them to strengthen their case against you.

Do you have a Wilshire Consumer Credit collection account on your credit report?

At FightCollections.com, we have extensive experience in removing or repairing collection accounts from companies like Wilshire Consumer Credit. We will investigate to see if this account is legitimate and valid. If the account is not valid, we will work to have it removed.

Let us help you with this and any other credit repair issues that you have.