When Marcus pulled his credit report to qualify for a mortgage, he found that an unknown collections agency was harming his credit score by 79 points. The company’s name was Reliant Capital Solutions, and Marcus had no idea who they were or what debt they were trying to collect.

Like thousands of other people every year, Marcus was a victim of the debt collection industry.

Marcus’s gut reaction was to call the phone number listed on his credit report and clear the whole thing up. Fortunately, he didn’t. If he had, it would have ended very badly for him. He didn’t know it, but Reliant Capital Solutions has almost 400 complaints filed with the Consumer Financial Protection Bureau since its inception in 2011, and has been named in over 80 federal lawsuits accusing them of violating consumer’s rights.

This article will take you through Marcus’s journey to understand who Reliant Capital Solutions is, why the collections account may be removed from his credit report, and how he was finally able to remove it and repair his credit.

Who is Reliant Capital Solutions?

Reliant Capital Solutions, LLC is a debt collection agency in Ohio. They collect a wide variety of debt from student loans and medical bills to government debts and auto loans. They are a third-party debt collector, meaning they work with creditors to collect debts owed to other companies, often including state government agencies.

A History of Complaints

Reliant Capital has an A+ rating with the Better Business Bureau (BBB), but that’s where the good news ends. The company has an average rating of just one out of five stars from their customers, with 84 complaints filed in the last three years alone. Only 17 percent of those complaints were successfully resolved by the company.

Almost 400 consumers have complained to the Consumer Financial Protection Bureau (CFPB) about Reliant Capital Solutions since 2011. Common complaints include trying to collect a debt that the consumer did not owe, failing to validate the debt and making false representations about the debt. In 2020, Reliant Capital ranked 392 out of all companies for complaints filed with the CFPB.

Perhaps most troubling is a formal warning on Reliant Capital’s profile with the BBB, which states that, “Complaints to the BBB allege consumers have been contacted by representatives from this company who identified themselves as being from a government entity such as the ‘Attorney General’s office’ in 23 different states.” This appears to be a clear violation of federal law governing debt collection practices.

How does Reliant Capital Solutions get listed on my credit report?

The Debt Buying Industry

Marcus discovered that most debt collection agencies like Reliant Capital acquire debt in one of two ways. They either buy debts outright from the original creditor for pennies on the dollar, or they have a contract with the original creditor to collect the debt for a fee. Either way, when you are contacted by a debt collector the debt has already been passed from hand to hand at least once.

This can cause all sorts of problems for consumers. When debts are sold in batches it’s common for paperwork and documentation not to make the transfer. Account numbers get confused with other accounts and incorrect balances are applied to consumers.

Sometimes consumers are sent bills for debts they never owed in the first place. In fact, 79 percent of credit reports contain some mistake or serious error, according to a study by U.S. Public Interest Research Groups.

That means the collection on Marcus’s credit report may not even be his. It could be a mix-up, a debt he paid ages ago, or a balance that’s been inflated with extra fees he doesn’t owe. Here’s why that may be the case:

Why Reliant Capital’s records may be unreliable

Several lawsuits against Reliant Capital Solutions describe a pattern of unreliable record keeping.

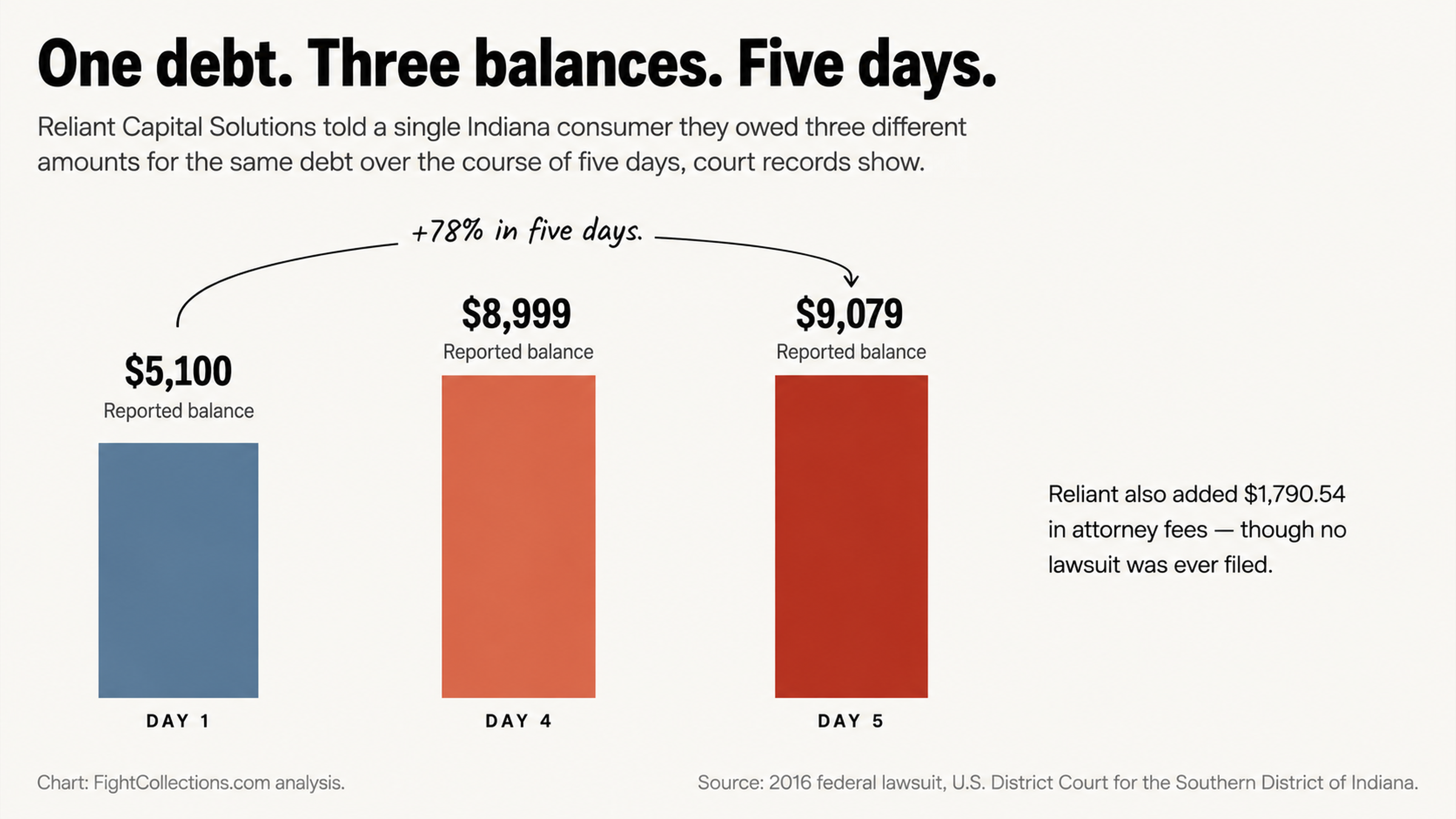

In a 2016 lawsuit filed in Indiana, Reliant Capital Solutions represented that a consumer owed $5,100, then $8,999, and finally $9,079 for the same debt over the course of five days. The company also allegedly tacked on $1,790.54 in attorney fees even though it never filed a lawsuit against the consumer.

A class-action lawsuit filed against the company in 2017 alleged that it improperly added a $75.90 collection fee to the balance of an old debt. The company had no legal or contractual justification to add the fee, according to the lawsuit.

A different class-action filed in 2018 claimed the company sent letters to consumers stating the amount of their debt could increase because of interest and late fees, even though neither Reliant Capital nor the original creditor had the authority to charge those fees.

In December 2024 a consumer filed a complaint with the BBB against Reliant Capital, saying that in response to their request for debt validation they received only a single page with their name and the amount they owed on it. The consumer wondered if the company was actually in possession of any documentation to validate that they owed the debt at all.

Red flags

Government Impersonation

Reliant Capital’s practice of having debt collectors impersonate government agents is a huge red flag. According to a warning posted by the BBB, consumers in 23 states have complained that representatives of the company pose as government agents — specifically representatives of the “Attorney General’s office.”

The Fair Debt Collection Practices Act (FDCPA) prohibits debt collectors from pretending to be associated with any government agency. The law also says debt collectors can’t claim they are going to file a complaint against a consumer when they have no intention of doing so, or neglect to tell consumers that they are debt collectors when they communicate with them.

According to the BBB warning, Reliant Capital Solutions may be doing all three.

Marcus remembered that when he got the initial voicemail about the debt the caller mentioned something about “state collections” but didn’t clearly state they were a debt collector. That kind of murky language can land a debt collector in hot water under the FDCPA.

Failure to Validate Debt

Under federal law consumers have the right to request validation of a debt within 30 days of the initial contact. The debt collector is supposed to suspend collection activities until it provides the validation.

However, many of the complaints about Reliant Capital Solutions describe the company’s failure to provide adequate validation when consumers request it.

In October 2025 a 70-year-old consumer filed a complaint with the BBB against Reliant Capital, saying they receive six to seven calls per week despite asking to be placed on a do not call list. The consumer called the experience “making me physically sick and affecting my mental health.”

Another consumer complained in November 2025 that after they told the company not to contact them about a debt they didn’t owe, a representative from Reliant Capital Solutions started calling their spouse. The consumer had never given the company permission to contact their spouse, a potential violation of the FDCPA rules governing contact with third parties.

Why DIY Disputes Will Never Work If You Represent Yourself: How Do You Really Know Who You’re Dealing With?

At first, Marcus thought he would handle the dispute himself. He found a template online and considered writing a validation request letter to Reliant Capital Solutions. He had no way of knowing that DIY disputes almost never work for the reasons most consumers would never suspect.

Every time you speak with a debt collector, you give them information. You confirm your address, your phone number, and the fact that you’re willing to engage. You may even accidentally acknowledge the debt, which a collector will use against you later. Debt collection representatives are professional negotiators. They have dozens of these conversations every day. You may only have two or three in your entire life.

Watch what happened when a Columbus woman attempted to verify Reliant Capital Solutions was a real company. She visited their office in Gahanna with her driver’s license to verify the company existed. Reliant Capital Solutions called 911 on her. If the company is this hostile when someone merely wants to protect herself, just imagine how they’ll treat you if you attempt to negotiate.

Why Debt Collectors Will Always Get the Better of You

Debt collectors know things you don’t. They understand the laws that apply, the loopholes to exploit, and the pressure tactics that will force you to pay. Unfortunately, most consumers have no idea how much leverage they really have.

The law protects you in ways you can’t imagine, but it does you little good if you don’t know how to use it to your advantage.

You don’t know that most of your income and assets are protected from garnishment by state and federal law. You don’t know that simply disputing an item on your credit report will result in its removal if the collector cannot verify it within the allotted time. You don’t know that anything a debt collector promises you over the phone is essentially meaningless because only written agreements are enforceable.

Just look at Reliant Capital Solutions’ own history to understand why phone calls are a terrible idea. With only 17 percent of their BBB complaints resolved to the customer’s satisfaction and nearly 400 complaints filed with the CFPB, the evidence suggests that consumers who engage with this company over the phone are unlikely to get the outcome they want.

The Secret to Removing a Collection Account

Understanding What’s in Your Power

Marcus eventually discovered that he wasn’t entirely at Reliant Capital Solutions’ mercy. Collection accounts can be removed from your credit report if the information is inaccurate, can’t be verified, or if the collector breaks any laws in the process. Given the documented history of reporting fluctuating balances, tacking on unauthorized fees, and refusing to validate the debt, there are plenty of opportunities for removal.

The most important thing Marcus learned is that your silence is your most effective weapon. Every time you answer the phone or engage in a conversation, you’re giving the debt collector more ammunition. Written communication leaves a paper trail and forces the debt collector to respond in writing as well. Most importantly, it puts the burden of proof back where it belongs: on the company that says you owe it money.

Paying a collection account almost never removes it. The status simply changes from “unpaid collection” to “paid collection,” but it will still be on your credit report for up to seven years. What you need is removal, not payment.

Why Hiring a Pro Always Works

Credit repair professionals understand exactly what documentation a debt collector needs to provide, the deadline by which they must provide it, and which technical violations will result in removal. They understand how to word a dispute letter for maximum effect and how to escalate if the debt collector doesn’t respond correctly.

When a professional disputes a debt on your behalf, the debt collector knows they’re up against someone who understands the law. Over 80 federal lawsuits have been filed against Reliant Capital Solutions. This is a company with major legal exposure, and a professional advocate knows exactly how to use that to your advantage.

Marcus realized that his mortgage application was too important to risk. The stakes were too high to risk making a mistake that would cost him the house of his dreams. He realized that paying for professional help was a drop in the bucket compared to the money he could lose if his credit score was reduced and his mortgage rate went up.

The Bottom Line

Reliant Capital Solutions is everything consumers fear about the debt collection industry. A formal warning from the BBB about alleged government impersonation, nearly 400 complaints filed with the CFPB, over 80 federal lawsuits, and a history of documentation issues are all evidence of a company that cares more about collecting a debt than complying with the law.

If you have a credit report with this company’s name on it, don’t panic. You do have the power to fight back. The same tactics and documentation shortcuts that result in all these complaints also create plenty of opportunities for removal. The information on your credit report must be accurate, verifiable, and reported in compliance with the law. If it’s not, you have recourse.

Marcus learned that the worst thing he could have done was pick up the phone and attempt to negotiate. The smartest thing he did was realize this was a situation where he needed professional help and that the pros who deal with debt collectors like Reliant Capital Solutions every day were in a much better position to advocate for him.

What to Do Next

If Reliant Capital Solutions has placed a collection account on your credit report, don’t fall into the trap of dealing with them directly. Don’t answer their phone calls. Don’t make promises or acknowledge any debt over the phone. You’re only giving them more power and they’re giving you nothing in return.

Instead, contact our office today for a free consultation. We specialize in disputing collection accounts from companies just like Reliant Capital Solutions. We understand their tactics, their weaknesses, and the specific laws they routinely violate. Let us review your situation and map out the best strategy for you.

Your credit report deserves to show accurate information, not unverified claims from a debt collector with a history like this. Take the first step toward removing Reliant Capital Solutions from your credit report and restoring your financial future.