If you've found FMA Alliance on your credit report, you already know how scary that feels. Debt collectors are counting on that reaction. But there's something important they're not telling you.

The debt collection business relies on a set of assumptions and shortcuts that all too often work against the consumer. If you know how the system really works, you have a lot more leverage against FMA Alliance than you think.

Who is FMA Alliance?

FMA Alliance, Ltd. is a debt collection agency based in Houston, Texas. Founded in 1983, FMA Alliance collects government, medical, educational, and financial debts. Here are the essentials of the business:

FMA Alliance has between 250-500 employees and is licensed to collect debts in Texas, New York, North Carolina, Minnesota, Tennessee, Colorado, Massachusetts, and other states. But there's more to the story than their business card.

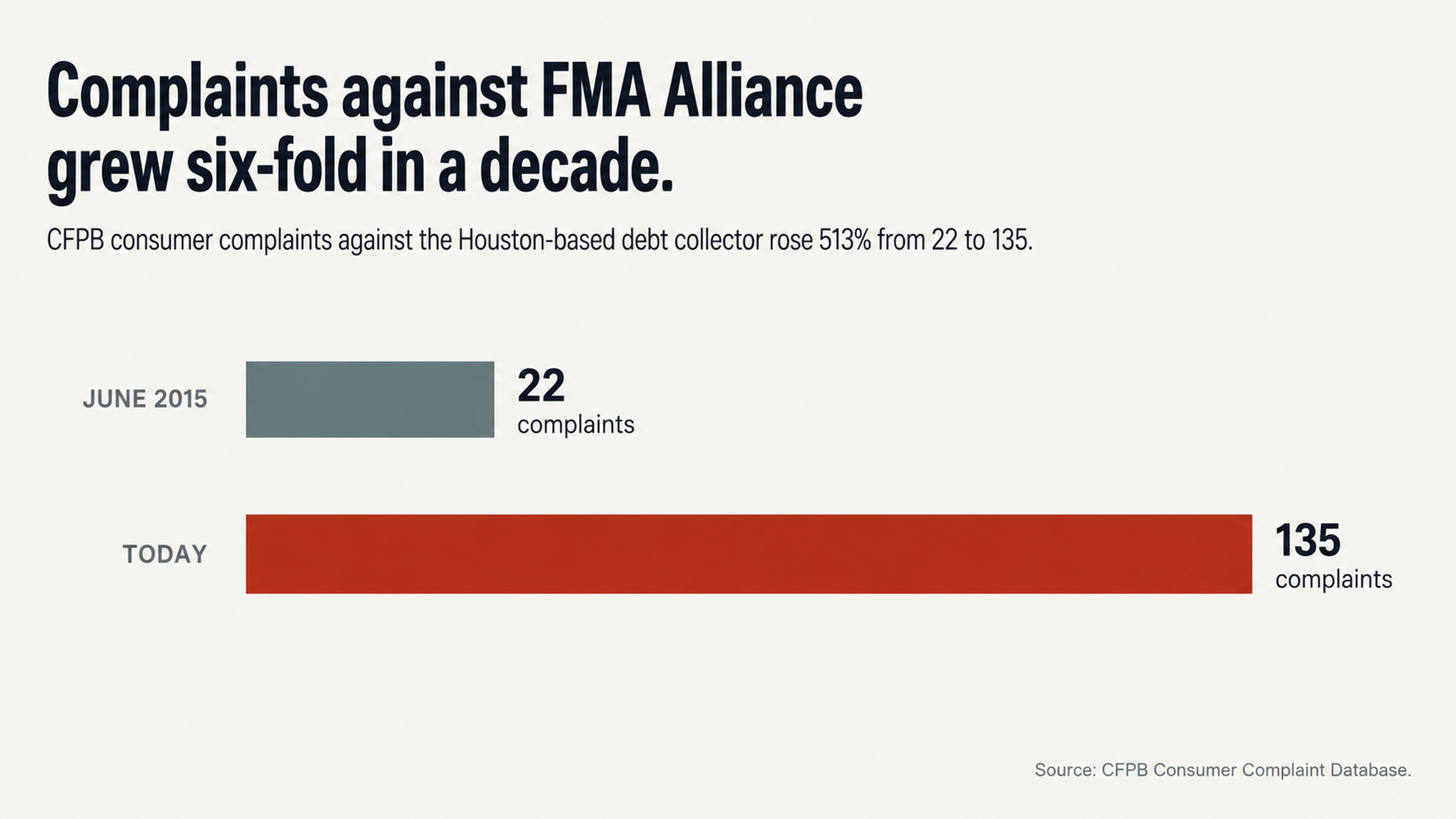

What You Won't Find on the FMA Alliance Website

FMA Alliance has been the subject of 135 complaints filed with the Consumer Financial Protection Bureau (CFPB). Compared to the 22 complaints on file as of June 2015, that's a 513% increase. During the same period, the company didn't grow nearly that fast.

Between 2015 and 2018, at least six class action lawsuits were filed against FMA Alliance for violating the Fair Debt Collection Practices Act (FDCPA). The suits included allegations of failure to validate debts properly, sending deceptive collection notices, and using abusive communication practices.

Overall, FMA Alliance has a 2.1-star rating from consumers, despite its A+ rating with the Better Business Bureau (BBB). That contrast is a reminder that having good industry credentials is no guarantee a company is treating its customers fairly. Keep that in mind as you consider how to deal with a collection account.

The Dirty Little Secret of Debt Collection

Most people don't realize how often errors occur in credit reporting. In fact, a study by U.S. PIRGs found that 79% of credit reports contain either errors or serious errors. That fact fundamentally changes the way you should think about a collection account.

In a system where mistakes are the norm and not the exception, you shouldn't pay a collection account until you've verified that it's accurate. Assuming a debt is valid because it shows up on your credit report ignores the reality of how credit reporting works. Collection agencies are counting on your not challenging the information on your credit report.

Your free annual credit report from each credit bureau isn't just a formality. It's an intelligence report that can help you figure out whether a collection agency is using a mistake to its advantage. That might include reporting the same debt multiple times, or trying to collect a debt you've already paid or doesn't belong to you.

Review your reports carefully, because the information on them is the basis of any effective strategy for dealing with a collection account.

Misconceptions About Paying a Collection Account

When you see an unfamiliar collection account on your credit report, paying it may seem like the most straightforward way to deal with the problem. But before you pay, understand what will happen.

Paying a collection account changes its status on your report from "unpaid collection" to "paid collection." Unfortunately, that doesn't mean it will disappear. A paid collection can still be reported by the credit bureaus for seven years.

In some cases, paying a collection account can even make matters worse. If you pay part of an old debt, you may inadvertently renew the statute of limitations on collecting the debt, exposing yourself to additional legal risk.

In November 2018, a class action was filed against FMA Alliance alleging that it had sent letters attempting to collect time-barred debts without informing consumers that making a payment would revive the statute of limitations. If consumers made payments because of the letters, they may have unknowingly reactivated their liability.

It's understandable that you would feel obligated to pay a debt simply because you feel you owe money. But guilt is a powerful motivator, and collection agencies rely on that. Don't pay a collection account out of a sense of obligation until you have verified that it's a legitimate debt. Otherwise, you may end up paying money you don't owe because of an error on your credit report.

Documented Issues with FMA Alliance

FMA Alliance has a history of alleged Fair Debt Collection Practices Act (FDCPA) violations that every consumer should understand.

In June 2017, a Wisconsin consumer sued FMA Alliance for allegedly violating the FDCPA by sending collection letters that included a settlement offer that was only valid for 15 days, when in fact the consumer could accept the settlement offer at any time. That kind of deadline is a violation of the federal prohibition on using false representations or deceptive means to collect or attempt to collect any debt or to obtain information concerning any consumer.

In November 2017, a class action was filed alleging that FMA's letters stated that consumers should send payments or other correspondence to a physical address. According to the complaint, that implies that consumers who wish to dispute a debt must do so in writing, even though federal law says that consumers can also make disputes over the phone.

These cases suggest that FMA Alliance may be using collection letters that are designed to discourage consumers from exercising their FDCPA rights.

In 2021, another class action (this time with more than 40 proposed class members) was filed alleging that FMA Alliance violated the FDCPA by disclosing consumers' names, addresses, and the details of their debts to a third-party vendor that FMA hired to send letters to consumers. Sharing consumers' personal financial information with an entity that has no legitimate reason to know it is a clear violation of the FDCPA.

A review of complaints filed with the Consumer Financial Protection Bureau (CFPB) and with the Better Business Bureau (BBB) reveals a history of similar behavior by FMA Alliance representatives.

In August 2021, a consumer told the CFPB that FMA Alliance had called saying the consumer owed $40,000 and that the consumer needed to pay $2,000 immediately or FMA Alliance would sue. The consumer said that the actual balance was only $8,300 and that the FMA Alliance representatives were "very rude" and "threatening" and implied that the consumer was not paying his debts.

Unauthorized payment complaints appear repeatedly in the record. One consumer stated in a complaint: Somehow they got into my bank account and wrote themselves a check. I have no idea what its for and its done on a day I was in the ER with my mom.

In March 2024, a consumer filed a complaint with the BBB against FMA Alliance saying that the company was trying to collect a debt that the consumer did not owe:

"Called numerous times to speak with someone about this account, no one will answer my questions, told me they would not provide proof of debt, proof they are licensed to collect it, the consumer wrote. This company is asking for my bank account and asking how much my tax return is. I do not know these people and they are overstepping their boundaries with questions. No one will work with me or talk to me instead they threaten to sue."

How to Deal with an FMA Alliance Collection

Requesting Debt Validation is Powerful

Most collection agencies operate on a business model that requires them to successfully collect on a high percentage of the debts they pursue. That means they can be sensitive if you make them go through the process of validating a debt.

When you challenge FMA Alliance to verify a debt and it can't, you have a strong case for having the listing removed from your credit report. The burden of proof is on FMA Alliance, not on you.

Debts may change hands multiple times before they are referred to a collection agency, and they can lose documentation or incur errors along the way. If you request debt validation, you can expose those errors. If a debt is inaccurate, erroneous, fraudulent, or can't be verified, you can request to have it removed from your credit report.

At least six federal lawsuits have been filed against FMA Alliance alleging that it violated the FDCPA by failing to include all of the information that the FDCPA requires debt collectors to include in their collection notices. That includes the date that the current interest began to accrue, the amount of the interest accrued, an explanation of any fees, and a proper itemization of any charges.

If any of those items are missing from the collection notice that FMA Alliance sent you, you may have grounds for a dispute. But if you don't know what you're looking for, you're unlikely to catch the problem.

The importance of refusing to engage with a debt collector cannot be overstated. When you talk to a debt collector on the phone, you're giving the collector the opportunity to get information from you, to pressure you into acknowledging that you owe a debt, or to persuade you to accept a payment plan you can't afford.

If you communicate in writing, you don't give the debt collector those opportunities — and you also create a paper trail that you can use as evidence if you need to file a complaint.

In addition, if you request in writing that a debt collector communicate with you in writing, the debt collector is not permitted to call you on the phone. If you write to request validation of a debt, the debt collector is not permitted to continue trying to collect the debt until it has provided the validation you requested.

Know Your Rights Under Federal Law

FDCPA Rights You Need to Understand

The Fair Debt Collection Practices Act says what debt collectors can and cannot do when pursuing a debt. Generally, debt collectors may not contact you at an unreasonable time or place, use threats, violence or profane language, claim you owe more than you do, or contact a third party about your debt (other than to obtain your address or phone number).

In 2021, a class action was filed against FMA Alliance alleging that it had violated the FDCPA by disclosing the names and addresses of consumers along with information about their debts to a third-party vendor.

You have the right to dispute a debt and request validation within 30 days of the initial communication from a debt collector. Once you dispute a debt and request validation, the debt collector may not continue to pursue the debt until it provides the validation.

If FMA Alliance is violating your FDCPA rights, you may be entitled to actual damages, statutory damages (up to $1,000), and attorney fees. In recent years, multiple class actions have been filed against FMA Alliance alleging violations of the FDCPA.

FCRA Rights That Help You

The Fair Credit Reporting Act controls how credit reports are compiled and shared. The information on your credit report must be accurate, complete, and verifiable.

If you dispute something that is on your credit report, the credit reporting agency must investigate and correct it within 30 days. Part of the investigation includes requiring the entity that made the error to respond and provide documentation that proves its claim. If the entity doesn't respond or doesn't have documentation to support its claims, the credit reporting agency must delete the disputed information.

When you dispute information that is on your credit report, the credit reporting agency must mark the information as disputed while it completes its investigation. Failure to mark disputed information is a violation of the FCRA.

Given the history of consumers saying that FMA Alliance refuses to verify debts or provide complete documentation to support its claims, it's possible that FMA Alliance could have a hard time responding to a credit reporting agency investigation.

The FCRA provides a number of important rights that can help consumers who are being pursued by debt collectors or dealing with errors on their credit reports. But actually enforcing those rights can be complicated if you haven't been through the process before. In some cases, working with a professional may make the most sense.

Conclusion

FMA Alliance has a substantial history of consumer complaints and has been sued multiple times for allegedly violating federal consumer protection laws. That suggests that the company may have a number of weaknesses you can leverage to your advantage if you are dealing with a collection account.

Instead of paying a collection account when you see it on your credit report, it may make more sense to dispute the information and see whether the collector can validate it. Given the high error rate on credit reports, starting with the assumption that any negative information is accurate can make it harder to clean up your credit report.

The most effective strategy for dealing with a collection account is to approach the problem clinically rather than emotionally. It's understandable that you would feel obligated to pay a debt simply because you feel that you owe money. But allowing that sense of obligation to control your actions can lead you to make choices that aren't in your best interest.

Instead of paying money you may not owe because of an error on your credit report, work through the process systematically to ensure you are actually obligated to pay the debt.

FightCollections.com is a credit repair firm that specializes in working with consumers who are facing debt collection issues or who have errors on their credit reports. Our staff has extensive knowledge about the procedures that collection agencies and credit reporting agencies use and the legal protections you have under federal law. We can help you make a plan to deal with collection accounts and maximize your chances of a good outcome.

Take Action Now

If you see FMA Alliance on your credit report, don't jump to conclusions and don't reach out to the company. Instead, take a step back and evaluate the situation. Given the history of alleged abuses and consumer complaints, you may not want to deal with FMA Alliance directly without support.

At FightCollections.com, we specialize in representing consumers who are dealing with collection accounts or who have errors on their credit reports.

We understand the documentation that you need to validate a debt and the procedures that you must follow to dispute information that is inaccurate or can't be verified. We can help you navigate those procedures in a way that protects your rights and gives you the best chance of a good outcome.

For a free consultation, contact us now.