You requested a copy of your credit report, and there it was. A collection account from Progressive Management Systems had been placed on your credit report, which lowered your credit score and ruined your credit history.

The account may have been for a medical bill you never received, a bill you already paid, or for an amount you don't even owe.

Your initial reaction may be to call the agency and try to resolve the situation. Don't do that. Everything you do in the next several days may determine whether this account remains on your credit report for seven years or not.

This article will explain exactly who Progressive Management Systems is, what their business practices indicate, and how you should respond to the situation.

Progressive Management Systems, which also uses the corporate name R. M. Galicia, Inc., is a third-party debt collector that specializes in collecting medical debt. They have been in business since 1978 and are headquartered in California with a second office in Nevada.

What Our Investigation Found

We conducted a thorough investigation of Progressive Management Systems and found information that you should consider when deciding how to respond to this collection agency.

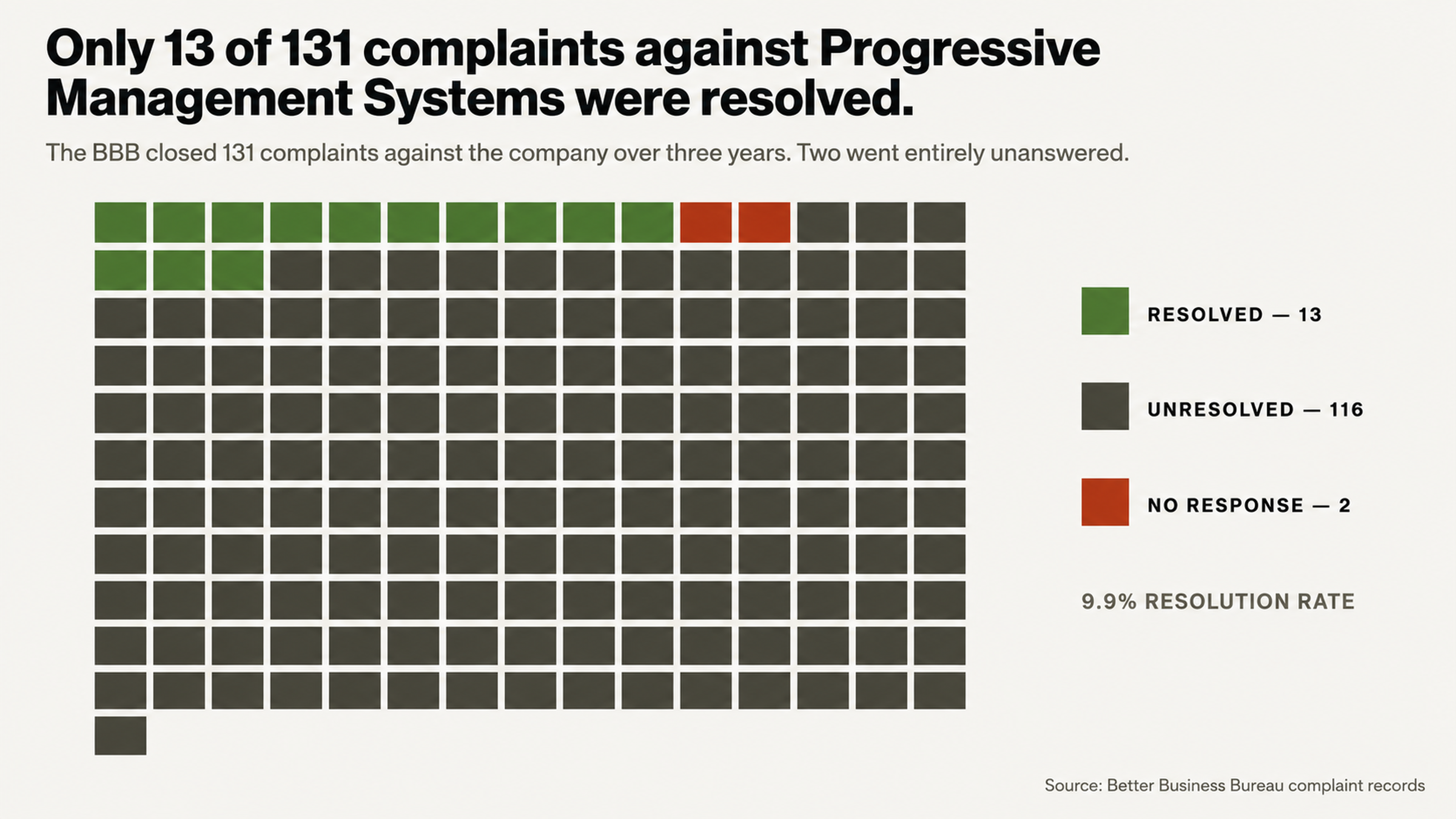

The Better Business Bureau (BBB) currently gives the company an F rating, which is the worst rating they can receive. In the last three years, the BBB has closed 131 complaints against the company, with only 13 of the complaints being resolved to the satisfaction of the consumer. That's a rate of only 9.9%. They didn't even respond to two of the complaints.

In 2018, Progressive Management Systems paid $1.5 million to settle a class action lawsuit (Gutierrez-Rodriguez v. R.M. Galicia, Inc.) in which they were accused of violating the Telephone Consumer Protection Act (TCPA) by placing automated "robocalls" to consumers who hadn't given them permission to do so.

According to the lawsuit, they were using an automated dialing system to call consumers' cell phones using phone numbers they had obtained from an unknown source.

The federal court system reports 94 cases involving R.M. Galicia, Inc., of which 78 were civil cases brought for violating the Fair Debt Collection Practices Act (FDCPA) and the Fair Credit Reporting Act (FCRA).

Why the Collection Account is On Your Credit Report

How Medical Debt Gets Transferred to a Third-Party Collection Agency

If you have medical debt in collections, it didn't get there by magic. The hospital or medical facility you visited was unable to collect the debt after a certain period of time, so they sold or assigned it to a third-party collection agency.

At any point during the transfer process, mistakes could have been made. Perhaps the original bill was incorrect. Maybe the information the hospital transferred to the collection agency was wrong. Maybe they got the wrong person.

In August 2025, one consumer filed a complaint with the BBB against Progressive Management Systems. The consumer indicated that they had requested a copy of their original written agreement with the hospital, which included their signature, but the company wouldn't provide it.

The consumer also stated that PMS wouldn't return the bill to the hospital so it could be processed by their insurance company but were continuing to add interest to the bill even though they couldn't produce a copy of the original agreement.

The Business Model of Debt Collection

Debt collection agencies purchase debt for pennies on the dollar. It's not uncommon for them to pay only $50 to $100 for a debt of $1,000 or more, which is why they're able to make a profit even when they don't collect the full amount of the debt.

The debt collection business model also explains why they use high-pressure tactics. If you know that they paid $50 for your debt, you're unlikely to take them seriously when they're calling you at all hours of the day and night demanding that you pay them $1,000 or more.

An individual who claims to be a former insider at PMS indicated on a consumer forum that the representatives at PMS work on a commission basis and that their phone scripts are designed to coerce people into making a payment, even if it's uncertain whether they actually own the debt.

Why Paying This Collection Will Not Help You

Paying the collection account doesn't mean it will be removed from your credit report. When you pay a collection account, the credit bureaus don't remove it. Instead, they change the status of the account from "unpaid collection" to "paid collection," and it remains on your credit report for the full seven years.

To lenders, a paid collection still indicates that you had an account go to collections, so having a paid collection on your credit report may still result in you being denied a loan or charged a higher interest rate.

For this reason, it's better to dispute any information you believe is inaccurate or unverifiable rather than making a payment. If they cannot verify the debt or if there was an error in the information, you may be able to have the account removed entirely instead of just having the status of the account changed.

Paying a Settlement May Have Unintended Consequences

You may be thinking that the best option is to settle the account for less than you owe. This doesn't always work out the way you expect. While some consumers have indicated that their credit score improved when they settled an account, others have found that their credit score didn't improve or even decreased.

Whether your credit score improves after a settlement depends on a lot of different factors, including your overall credit history and which credit scoring model is being used. When you settle an account, the lender may report the account to the credit bureaus as "paid-settled," which, to some lenders, is just as bad as an unpaid collection account.

In addition, settling an account may have tax implications. Forgiven debt over $600 must be reported to the IRS as income, so you may owe taxes on the amount of debt you didn't pay. Settlement isn't always the solution you think it will be.

Why Disputing is Your First, Best Option

Credit Report Errors are Common

If you believe that your credit report is accurate, you're probably mistaken. According to a study by U.S. Public Interest Research Groups, 79 percent of credit reports have errors or "serious errors". These are not errors like minor spelling mistakes, but real errors that affect your creditworthiness.

Collection accounts are particularly susceptible to error due to the nature of debt resales. Original creditors can report the wrong balances. Collection agencies can assign debts to the wrong consumer. Information can be incomplete or corrupt during the transfer.

A complaint filed against Progressive Management Systems with the CFPB illustrates the risk. While reviewing his credit report as part of a refinance, a man discovered two different Progressive Management Systems collection accounts that both have the same date of reporting. He doesn't know what the collections are for.

Verification Works in Your Favor

Federal law requires that debt collectors verify debt when you dispute it. The FDCPA and FCRA put responsibilities on collectors that are difficult to fulfill, particularly with older or resold debt.

When you dispute a collection through the credit reporting agencies, the collection agency must investigate and verify the information. If they can't provide adequate verification within a reasonable time, the account must be deleted from your report.

Another complaint filed against Progressive Management Systems with the CFPB shows how difficult verification can be for the company. The complainant said they received what they believed to be a computer generated letter but received no contract agreement, no signature, and nothing to verify that the debt was their responsibility. Inadequate documentation is grounds for disputing the debt.

What if I Do Nothing?

The Statute of Limitations Runs Out

No negative marks remain on your credit report forever. The FCRA says that most collection accounts can only remain on your report for 7 years from the original date of delinquency. That clock began ticking before the debt was sold to Progressive Management Systems. This is something to consider in your strategy.

If the collection account is already 5 or 6 years old, it may make sense to ignore it. Making a payment or settling the account could revive it.

Time is on your side in another way, as well. The effect of collection accounts diminishes as they get older. A collection account that's three years old has less impact on your credit score than a newer account. A six year old collection account has very little impact compared to your more recent credit history.

Most Debts Don't Result in a Lawsuit

Many consumers pay debts they could dispute because they are afraid of a lawsuit. However, the reality is that lawsuits are rare. Collectors perform a cost-benefit analysis for every debt. Most debts aren't worth the cost and risk of a lawsuit.

To file a lawsuit, the collector must pay court filing fees and pay an attorney. If they win a judgment, they must spend time and money to enforce it. If the debt is a few thousand dollars or less, the cost of a lawsuit exceeds the potential benefit. It only makes sense to sue people who owe large amounts and have a lot of attachable assets.

While Progressive Management Systems has won judgments against consumers, including one judgment for more than $49,000 in Los Angeles Superior Court, these judgments are against consumers who owe a lot and have attachable assets. The average medical collection doesn't fit either criterion.

The Guilt of Owing People

A debt collector's most effective tool is your sense of guilt at owing money. The guilt that you should pay what you owe, that it's irresponsible not to pay debts, is used against you.

A consumer reviewing Progressive Management Systems for Wallet Hub sums it up perfectly: After being hospitalized and unconscious (therefore not able to refuse their services) and being charged an usurious rate for their services, I would rather die than continue to live owing this debt. This is the way Progressive makes people feel.

Approach the problem clinically, instead. This is a business transaction, not a moral obligation. The collector bought your debt and wants to make a profit on it. You have no obligation other than to proceed according to the law.

Knowledge is Power

Information is a powerful advantage for consumers who must negotiate with debt collectors. The collector may have more information than you do, but that doesn't mean that you are at a disadvantage. Collectors rely on consumers not knowing their rights and not knowing how to dispute a debt.

When you understand that 79 percent of credit reports contain errors, that collectors must verify disputed debts, and that many debts can't be verified, you have power. You're not a victim. You're an informed consumer who can manage the situation.

One man who reviewed Progressive Management Systems on the Chamber of Commerce website said that the company preys on senior citizens and military veterans. After a hospital sold a bill to the company, he didn't receive any notices, had insurance that should have paid the bill, and watched his credit rating drop by 35 points. He didn't know that he should check his credit report, dispute the account, and defend his credit rating.

Conclusion

Progressive Management Systems is a company that has been in business for 48 years. In that time, they have developed a business model based on collecting medical debt. Their F rating with the BBB, $1.5 million TCPA settlement, and 94 federal lawsuits suggest that this is a company with some serious issues. These issues may provide you with leverage when you deal with Progressive Management Systems.

Don't respond by calling the company to negotiate a settlement or by simply paying what they say you owe. Respond by challenging inaccurate, erroneous, or unverifiable information through the proper channels. If they can't verify the debt, they may have to remove it from your report.

Don't forget that ignoring them can be a good strategy, time is on your side, and that the guilt you feel is just a tactic. Approach the situation armed with information instead of fear.

Get Help with Your Credit Report Now

Dealing with a collection agency can be daunting when you're on your own. They have entire staffs dedicated to collecting from you, and the dispute process is complicated. Deadlines are tight, and missed deadlines can have serious consequences.

At FightCollections.com, we know how to dispute collection accounts, including those from Progressive Management Systems. We understand the documentation that they are missing, the verification process, and the procedural flaws that you can exploit to remove the account from your report.

Don't let them push you around and dictate the terms of your credit report. Contact us at FightCollections.com today for a free consultation.