If you see First Credit Services on your credit report, you probably want to get it removed as quickly as possible. You may consider dialing the phone number on the credit report and paying them off over the phone.

That is what they want you to do. It might be the worst money move you could make. Keep reading to find out why.

The debt collection business relies on two factors: urgency and fear. A debt collection agency wants you to think that paying them off is the only way to get rid of them. They know that if you throw money at the problem, it will probably go away.

What they don't tell you is that paying off the collection does nothing to remove the item from your credit report. It might actually do the opposite.

Before you do anything else, you have to know this one thing about credit reports: Credit reports are full of errors. In fact, a study by U.S. PIRGs found that 79 percent of credit reports contain errors or other mistakes. This fact alone should make you question whether the debt First Credit Services says you owe is accurate, verified, or legitimate at all.

Who is First Credit Services?

First Credit Services, Inc. (doing business as Accounts Receivable Technologies) is a third-party collection agency based in New Jersey. Here is their contact information:

First Credit Services is known for collecting debts in the health, fitness, and wellness industries. If you have a gym membership to a fitness center like Crunch or Planet Fitness, First Credit Services might be calling you about an outstanding balance.

What is the real story behind First Credit Services?

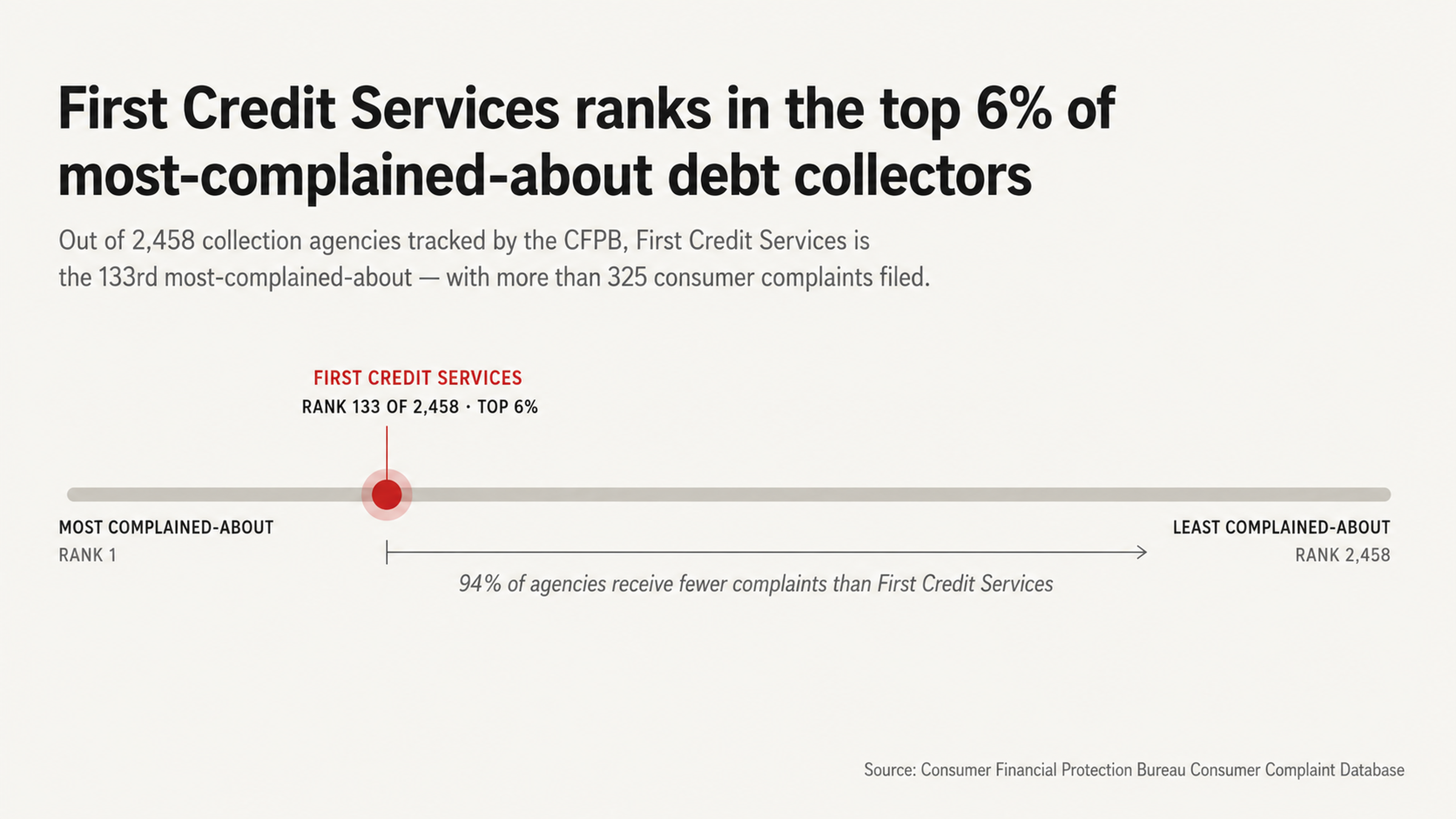

As it turns out, First Credit Services has had over 325 complaints filed with the Consumer Financial Protection Bureau. This number ranks them 133 out of 2,458 other debt collection agencies across the country. That means First Credit Services is in the top six percent of the most complained about debt collection agencies in the U.S.

In addition to CFPB complaints, First Credit Services has been sued over 140 times in federal court. Most of the lawsuits brought against First Credit Services were filed for violating the Fair Debt Collection Practices Act.

The Better Business Bureau has also received close to 200 complaints about First Credit Services. Their two profiles on the site have an average rating of two out of five stars.

What are people saying about First Credit Services?

Most people are saying the same thing: First Credit Services is calling them trying to collect a debt they don't owe. Others are saying that First Credit Services will not validate the debt or stop contacting them.

One person reported to the BBB that First Credit Services called them repeatedly to collect a debt that was already paid three years ago. They sent the company proof that they owed nothing, but the calls continued anyway.

Don't fall for what First Credit Services is telling you

There are several myths that First Credit Services will try to get you to believe.

Myth #1: I have to pay them right now or they will ruin my credit.

Truth: Paying off a debt collection agency like First Credit Services will not fix your credit. When you pay a collection, the account will be updated to show that it is paid. However, the account will stay on your credit report for up to seven years from the original delinquency date.

In some cases, paying off a collection can even hurt your credit score. When you pay or even acknowledge a collection agency, you may inadvertently leave a paper trail that they can use against you. Plus, in some states, paying a collection can reset the statute of limitations on the debt.

That means First Credit Services can legally sue you or continue collecting money from you for years longer than they should.

Myth #2: First Credit Services has verified my debt.

Truth: Debt collection agencies do not verify your debt before they contact you. They buy debt portfolios at a discounted rate, and it is not profitable or practical for them to verify each debt. In fact, many debt collection agencies don't have anything more than a spreadsheet with your name, address, phone number, and the amount that you owe.

The Consumer Financial Protection Bureau's complaint database is full of stories from consumers who were contacted by First Credit Services about debts that they didn't owe.

Some people were being pursued for debts in their name that were the result of identity theft. Others were being pursued for debts related to gym memberships they had canceled. At least one person was pursued for a debt from a gym that was in a different state and had closed years ago. Another person reported that First Credit Services called her about a debt from a gym in Illinois. She lived in Washington and had never set foot inside the gym.

Under federal law, you have the right to request debt validation from a debt collection agency within 30 days of initial contact. Debt validation simply means that the debt collector must provide proof that the debt is yours and that you owe the amount they say you owe. Many times, debt collection agencies can't validate the debt, so they will simply go away.

Why are debt collectors so aggressive?

It's all about the economics of debt collection

Debt collection agencies are incredibly aggressive because their business model demands it. Debt collectors don't make a lot of money on each individual debt. Instead, they make money because they collect on such a high volume of debts.

Debt collection agencies typically purchase debt portfolios for pennies on the dollar. In some cases, they might purchase a debt portfolio for four or five cents on the dollar. They might also purchase a debt portfolio that has been sold several times before. That means the original debt collector didn't collect enough money on the portfolio to make it profitable, so they sold it to someone else. The cycle repeats until the debt is either paid off or the statute of limitations runs out.

Because debt collectors don't make a lot of money on each debt, they have to collect money on as many debts as possible. That means using incredibly aggressive tactics to scare you into paying them money now. If you don't pay them money now, they will just move on to the next person on their list.

Many consumers have complained to the Consumer Financial Protection Bureau that First Credit Services calls them from a different phone number almost daily. This tactic allows First Credit Services to continue contacting consumers without them blocking the phone number. It also makes it very difficult for consumers to keep an accurate count of how many times First Credit Services has called. They're hoping you'll pay them money out of fear or confusion.

When debt collectors threaten you with a lawsuit or wage garnishment, they are hoping to scare you into paying money that you might not even owe. Consumers have reported to the CFPB that First Credit Services representatives have threatened to garnish their wages if they don’t pay. Other consumers have reported that First Credit Services representatives have threatened to sue them if they don't pay.

The reality is that it is not worth it for debt collectors to sue consumers or garnish their wages. For one thing, it is expensive and time consuming to file a lawsuit. First Credit Services would have to pay court filing fees and attorney fees. They would also have to devote staff hours to the process of suing you.

For another thing, most consumers don't have the money to pay a debt collection agency. If First Credit Services sues you and wins, they might be able to garnish your wages.

However, if you don't have disposable income in your budget, there's very little that First Credit Services can take from you. That means it doesn't make sense for First Credit Services to pursue the issue further. Instead, they will just move on to the next consumer on their list.

This is not to say that First Credit Services never sues consumers. However, it is in your best interest to understand that most lawsuits are empty threats designed to scare you into paying money.

The Paper Trail In Your Favor

BBB complaints are more than just a warning. They are evidence of a systemic problem that can be used to dispute the collection. If a collection company has 190 complaints that all say the same thing, it is safe to say they have a problem.

The actual text of complaints filed against First Credit Services details collection of debts not owed, failure to respond to validation requests, and harassing communication that violates the FDCPA.

One consumer even filed a complaint that First Credit Services was calling them from multiple phone numbers but never leaving a message. The consumer had no outstanding debt with First Credit Services and had never done business with the company.

This information is important because it means the mistakes and violations are not isolated incidents. It means that if you have a First Credit Services collection on your report, and you dispute it, you are not crying wolf. You are pointing out a legitimate problem that has happened to hundreds of other people.

What the complaints say about verification issues

The majority of complaints filed against First Credit Services are attempts to collect a debt that is not owed. This includes mistaken identity, debts paid in full, and debts that do not belong to the consumer in question. This is not a simple miscommunication about the amount or a misplaced letter. This is about not verifying whether or not a debt actually exists.

Multiple complaints say First Credit Services reported a debt to credit agencies for a gym membership the consumer said they had cancelled. This could mean First Credit Services does not verify debts before they begin collections or it could mean the creditor client is engaging in problematic behavior that First Credit Services enables. Either way, consumers are being asked to pay debts they don't owe.

If a collector cannot verify the details of a debt, it is not a legitimate credit account. The FCRA says information on your credit report must be accurate and verifiable. If it does not meet that criteria, it can be removed.

Your Rights Under Federal Law

FDCPA

The FDCPA sets out very clear behaviors that debt collectors cannot engage in. Actions considered violations that are detailed in complaints against First Credit Services include harassing phone calls, failure to validate a debt, threatening to sue when they do not have that intention, and continued contact after consumers have made it clear they do not want to be contacted. Each one of these is a potential lawsuit against First Credit Services.

You have the right to ask for a written validation of the debt within 30 days of the first communication. Once you make that request, the collector cannot attempt to collect the debt again until they have provided that proof. Many debts cannot meet that burden.

You have the right to make a written request that a debt collector ceases all contact with you. This does not mean the debt goes away. It means the debt collector cannot harass you over it anymore. They can attempt to collect through a lawsuit, but most debts are not worth the time and money to pursue that way.

FCRA

The FCRA says that anything reported to the credit agencies must be accurate, verifiable, and complete. When you dispute an item on your report, the credit agency must investigate. The furnisher (in this case, First Credit Services) must verify the information or the credit agency must remove it.

Complaints against First Credit Services include allegations that the company reports debts without verifying them, fails to mark disputed accounts as disputed, and continues to report disputed information. All of those actions are violations of the FCRA and grounds for removal.

The key here is that the burden of proof is not on you. It is on the debt collector and the credit agencies to show that the information they are reporting is accurate. If they cannot do that, the account must be removed. This is not a loophole. This is a consumer protection.

How working with a professional changes the equation

Information imbalance

Debt collection agencies do this for a living. They know what documentation will satisfy the dispute. They know what kind of response will trigger additional requirements. They know how to manage the process in their favor. You, on the other hand, will probably only go through this process once or twice in your life and you do not have the advantage of their knowledge.

That information imbalance is why so many consumers simply pay debts they do not owe. They do not know what documentation is required to verify a debt, so they accept the debt collector's representation of the debt at face value. The system is designed to be confusing. Confusion helps the debt collector.

If you work with a professional who is well-versed in federal debt collection law, you have the information you need to level the playing field. If you file a properly formatted dispute that points out specific violations of federal law, the debt collector cannot simply wait for you to get frustrated and give up. The debt collector actually has to respond.

Strategic silence

One of the hardest things for consumers to learn is that silence is golden. Every single time you get on the phone with a debt collector, you risk saying something that acknowledges the debt, provides information the collector can use against you, or keeps you engaged in a process designed to coerce you into paying.

A professional credit repair advocate knows that written communication, properly crafted to assert your rights without exposing you to liability, is always better than a phone call. It does not give the debt collector the opportunity to use high-pressure verbal tactics and it creates a paper trail of your dispute efforts.

When First Credit Services is calling you from all those different phone numbers, the instinct is to pick up the phone and try to make the problem go away. Not picking up the phone and properly disputing the debt in writing takes away one of the debt collector's primary weapons and forces them to play by the rules. That is a game you can win.

Conclusion

Just because First Credit Services is on your credit report does not mean you have to accept what they are saying as fact. The complaint history, the pattern of verification issues, and the harassing behavior detailed by other consumers all say this is a company where mistakes are routine and documentation is often absent.

Debt collectors want you to believe a series of myths: you must pay now, they have verified your debt, they will sue you if you do not pay. All of those myths are designed to keep you from thinking strategically about how to manage the situation. Once you realize you have the legal right to dispute unverified or inaccurate accounts, the dynamic changes.

You can get a collection removed from your report if the information is inaccurate, erroneous, fraudulent, or cannot be verified in a timely manner. Given First Credit Services verified track record on verification and accuracy, there is every reason to believe the information they are reporting about you may not meet that standard.

Take Action With Our Help

You do not have to go through this process alone. FightCollections.com specializes in disputing inaccurate collection accounts and pushing back against debt collector behaviors that violate your rights. We understand the specific behaviors consumers are experiencing with First Credit Services and we understand how to challenge accounts that cannot survive legal scrutiny.

If First Credit Services is on your report, do not call them, do not pay them, and do not assume what they are saying is true. Contact FightCollections.com today for a consultation and find out how we can help you push back against collection accounts that may not belong on your report in the first place.

The debt collection industry thrives on your fear and confusion. Information and professional advocacy are among the most powerful tools you have to protect your credit and your rights.