Cawley and Bergmann are like a bad houseguest: they show up uninvited, and once they appear on your credit report, they can remain on your report for seven years.

They are a debt collection agency in New Jersey that has been collecting debts from consumers for more than 20 years.

However, they are not likely to tell you this: their documentation is often incomplete. Debt collection companies are running a paper-based business, and if you push them to prove that the debt is legitimate, they often lack the documents to back up their claims.

Debt collection agencies rely on consumers who don't dispute debts, and if you turn the tables on them, they may not be able to prove that you owe the debt. According to the U.S. PIRGs, 79 percent of credit reports contain errors or confirmed inaccuracies.

Therefore, it is always in your best interest to push debt collectors to prove their claims.

Who is Cawley and Bergmann?

Cawley and Bergmann, LLC is a debt collection law firm with offices in New Jersey. They were originally founded in 1991 as a corporate law firm, but began to work in debt collection and asset recovery in 1998. They work as agents of several large debt buying companies, including Oliphant Financial, LLC; Cavalry SPV I, LLC; and JHPDE Finance.

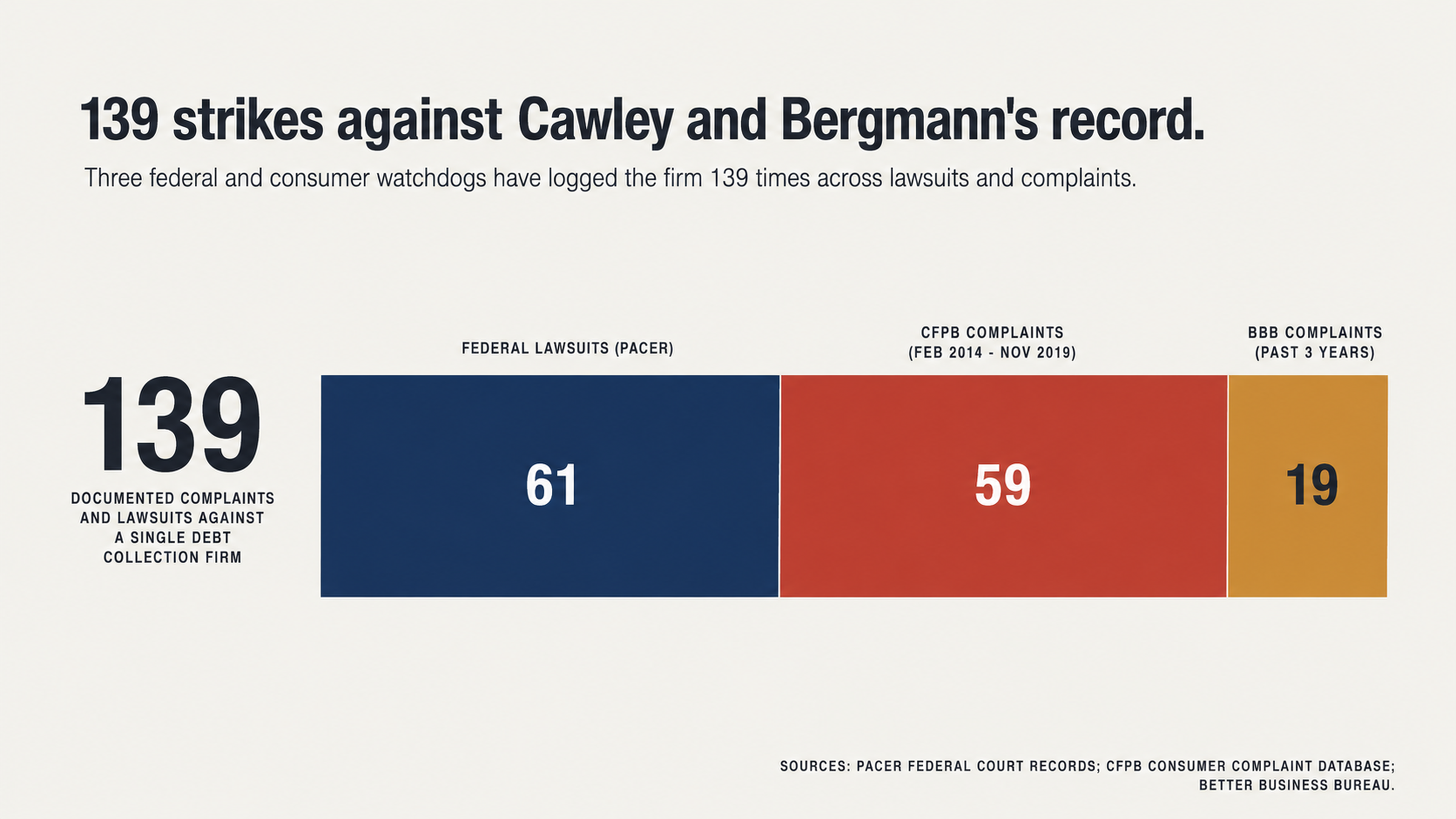

What Our Investigation Found

When we look at the public record for Cawley and Bergmann, there are several items of concern.

First, when we looked at the PACER (Public Access to Court Electronic Records) website for federal court cases, we found at least 61 cases brought against the company by consumers, 47 of them under the name Cawley and Bergmann, LLP, and an additional 10 under the former name, Bronson, Cawley and Bergmann.

When a company has been in business for nearly three decades and still has that many federal lawsuits pending, it is clear that there are ongoing problems.

When we looked at the Consumer Financial Protection Bureau (CFPB) complaint database, we found at least 59 complaints about the company, dating back to February 2014 and running through November 2019. Nearly all of the complaints were "Closed with explanation" rather than "Closed with monetary relief," meaning that consumers who complained to the CFPB got form letters rather than refunds.

Finally, when we looked at the Better Business Bureau (BBB) website, we found that the company has been in business since 1999 but remains unaccredited by the BBB, with a rating of B-minus.

In the past three years, they have closed 19 complaints with the BBB. When a company does not seek accreditation from the BBB and continues to garner complaints over the course of 27 years, it suggests that the company sees consumer complaints as the cost of doing business rather than issues to be resolved.

Your Right to Request Verification

The Burden of Proof is on the Collection Agency

If you have received a letter or call from Cawley and Bergmann, you have the legal right to request verification of the debt. Under the Fair Debt Collection Practices Act (FDCPA), consumers have 30 days from the initial contact from the collection agency to dispute the debt and request verification.

This means that the burden of proof is on the collection agency to provide all documentation related to the debt. You are entitled to request the name of the original creditor, a detailed breakdown of the amount you owe, the date of your last payment, and any documentation that proves the transfer of ownership if the debt has been sold.

Many collection agencies cannot provide the documentation to support the debt, and requesting verification is often an effective way to determine whether a debt is legitimate.

In 2015, Lemberg Law filed a complaint alleging that Cawley and Bergmann used false and misleading representations and threatened to take actions that they did not actually intend to take. This is why it is so important not to take the claims of a debt collection agency at face value.

Why Some Collection Agencies Lack Documentation

When debt buying companies purchase debts, they often buy them in large batches and pay only pennies on the dollar for many of the debts.

For example, when Cavalry SPV I, LLC or Oliphant Financial, LLC purchase debts, they receive spreadsheets with consumer information and balances due, but they may not receive full documentation for each debt. Therefore, when they attempt to collect on those debts, they may not have the documentation to support their claims. This is why requesting verification of a debt can be so effective.

The debt collection business model relies on consumers paying debts without asking questions. When consumers push back and ask the debt collection agency to support their claims, it often costs more in time and money to pursue those debts than they are worth. For example, if a debt collection agency has to spend an hour securing documentation for one debt, that is an hour that they cannot spend making five other consumers pay their debts.

This may explain why many of the lawsuits brought against Cawley and Bergmann are resolved so quickly. For example, the lawsuit in the case of Rodrigues v. Cawley Bergmann was resolved within a month, and the lawsuit in the case of Franklin v. Cawley and Bergmann, LLC was resolved within two months. While there are a variety of reasons why lawsuits may be settled so quickly, one reason may be that it simply costs too much to pursue the debts.

Pressure Tactics from Cawley and Bergmann Documented in Consumer Complaints

Many consumers have reported that Cawley and Bergmann uses high pressure tactics to attempt to secure payment from consumers. For example, one consumer reported the following to the Consumer Financial Protection Bureau:

"The caller said he could go to his manager and 'make a great deal' so I wouldn't get sued, as long as I paid [it] in full today. It was very aggressive and high pressure. He made me feel like if I didn't pay today I would get sued tomorrow."

Another consumer, a disabled veteran, reported that when he called Cawley and Bergmann to ask about the debt they were calling about, the representative would not tell him. Instead, the representative told the consumer that he needed to verify the consumer's identity first.

When the consumer pointed out that debt collection laws require collectors to inform consumers about the debt prior to asking for identification, the representative became aggressive and told the consumer that he couldn't tell a man who had been doing this for 18 years how to do his job.

These pressure tactics are typical of many debt collection agencies. The goal is to use emotion to get consumers to pay debts as quickly as possible. Debt collectors may threaten to sue or claim that consumers could face wage garnishment, liens, or other actions if they do not pay.

In reality, collection agencies often lack the documentation to support the debt, and many will settle for pennies on the dollar if consumers push back.

Why Debt Collectors Rely on Guilt

Debt collectors know that if consumers feel guilty about a debt, they are likely to pay it without asking questions. However, the reality is that debts are simply a business transaction. When the original creditor charged off your debt, they took a tax deduction and wrote off the balance. When a debt buying company purchased your debt, it paid pennies on the dollar for it. There's nothing moral about not paying an invalid debt or requesting that a debt collector provide documentation to support a debt.

If you are receiving calls from Cawley and Bergmann, don't pay them without requesting verification of the debt first. Instead, reach out to Lemberg Law to learn more about your legal options.

Why You Should Never Pay A Collection Account First (Ever)

The Paid Collection Catch 22

When a collection agency reports on your credit report, some people believe that paying the account off is the best course of action. While the logic makes sense, it is a mistake to pay a collection account without disputing it first. Why? Because when you pay a collection account, it will show as a paid collection on your credit report.

But here's the thing – the account will still be listed on your report for 7 years from the original delinquency date. Yes, you read that right. Even if you pay the account, the collection will still remain on your report for the full 7 year period. And it will still be considered a negative item on your report.

Newer FICO credit scoring models (like FICO 9 and VantageScore 3.0) do not count paid collections against you. However, many lenders still use the older models where a paid collection is essentially treated the same as an unpaid collection. So before paying the collection off, you would need to know which credit scoring model a lender uses and whether or not paying the account off would help your credit score.

Disputing First Instead

It makes more sense to dispute the collection first. If the account contains errors, or if the account is the result of identity theft, or if the collector cannot validate the debt properly, the account may be deleted. And when an account is deleted, it no longer has any impact on your credit score at all.

A paid collection will still indicate to future lenders that at one point in time you had an account go to collections. A removed collection will not.

When Can A Collection Be Removed?

A collection account can be removed if it contains errors such as balances, dates or other account information. A collection account can be removed if it is the result of identity theft or fraud. A collection account can be removed if the collector cannot validate the debt properly within the time provided by law.

In 2014, in the case of Marucci v. Cawley and Bergmann, the court denied the defendant's motion to dismiss the case and ruled that the, "plaintiffs have stated sufficient facts to support a claim that defendant's collection letter was misleading under the FDCPA." The court further ruled that both the debt buyer and Cawley and Bergmann could be held jointly liable. So even though the case was not ultimately decided in favor of the plaintiffs, the court did rule that there were sufficient facts to support the claim.

This means that even if the process does not always end in your favor, there are times when you can successfully challenge collection accounts. But it is also important to note that you cannot do it emotionally and reactively. You have to do it proactively and systematically. You have to document every communication. You have to demand validation. You have to know your rights.

What To Say To A Collector

Never, ever talk to a debt collector over the phone. Because anything you say can and will be used against you. If you acknowledge the debt and agree to pay it, or if you provide a collector with your new phone number or place of employment, it can all be used against you. So the less you say the better.

According to CFPB complaints filed against Cawley and Bergmann, one consumer claimed that the collector engaged in caller ID spoofing. The consumer reported that the collector would call from phone numbers that appeared on caller ID as being from local businesses and even once as a job opportunity. The consumer answered the call because they thought it was either from a local business or a job opportunity. So the collector got the consumer on the phone because the consumer did not realize who was calling.

The best way to handle collector phone calls is to simply not answer them. If you need to communicate with them, communicate in writing. Because written communication cannot be misquoted or distorted. It creates a permanent record. And it sets a clear expectation for how the collector is to respond.

Creating A Paper Trail

To effectively deal with a collector, you need to keep a paper trail. Save every letter. Log every phone call, including dates and times. And whenever possible, communicate in writing by using certified mail return receipt requested. That way, when you challenge the collector's practices, you have proof that you followed procedure and they did or did not.

In 2023, a class action lawsuit was filed against Cawley and Bergmann titled Harris v. Cawley and Bergmann Corp. The lawsuit claimed that the collector violated a federal rule by sending email collection letters that did not include instructions on how consumers could opt out of receiving the emails.

Now unless a consumer kept a copy of the email, they would not have known if the email violated a federal rule or not. But because some consumers did save the emails, it became possible to prove that the emails violated a federal rule.

Having a paper trail accomplishes two things. First, it prepares you for a potential battle if you need to escalate the matter. But second, if you signal to the collector that you are organized and prepared, they may change the way they pursue you. Organized consumers are not worth the effort.

Getting Help

If you are dealing with a collection agency, they are professionals who do this for a living. They know the laws, they know the procedures, and they know how to apply pressure. If you are going up against them alone, you are at a disadvantage. Because even when you are in the right, you are at a disadvantage.

Credit repair professionals know exactly what information to request from a collector. They know how to word a challenge letter for maximum impact. And they know when a collector's response falls short of the law. They know patterns and loopholes that a consumer may not recognize. And they know when a collector has violated a law in a way that will help your case.

If you can prove that a debt collector has violated a federal law, such as the FDCPA, you may be entitled to up to $1,000 in statutory damages plus attorney fees. And consumer protection attorneys who specialize in this sort of thing have already recovered judgments from Cawley and Bergmann in several states. Why? Because they know what to look for that a consumer may not know to look for.

The Bottom Line

The bottom line here is that this is not just about a collection account. And it is not just about your credit score. This is about your financial independence. Every single error that you allow to remain on your credit report is costing you money in higher interest rates and reduced opportunities. And it is not just about money. Errors on your report can cost you job opportunities, housing opportunities and insurance rates.

Cawley and Bergmann has been around since 1996. In that time, they have faced 61 federal lawsuits and they have been the subject of dozens of regulatory complaints. But they are still in business because consumers still pay them when they don't have to. Just because they are still in business does not mean you have to pay them.

Information is power. And you have more power than you think you do. You have the power to request information. You have the power to challenge errors. And you have the power to demand documentation. Or you can allow the collector to dictate the terms of the relationship. What's it going to be?

What to Do When You Find Cawley and Bergmann on Your Report

Just because you find Cawley and Bergmann on your credit report does not mean it's the end of the world. In fact, it's just the beginning. Because what it really means is that you have an opportunity to take control of the situation.

And the first thing you need to do is determine if they have the documentation to prove that you owe them the money. Their documentation may be incomplete. Their processes may be flawed. But their leverage only exists if you do nothing.

The dispute process exists because it works. Every day, consumers successfully challenge collection accounts because they cannot be verified or because they contain errors or because the collector fails to respond properly to a validation request. Paying an unverified debt is paying a debt you don't even know you owe to a company that may not be able to prove you owe it to them.

Conclusion

You have the right to an accurate credit report. And you have the right to challenge any information on your report that you do not believe is accurate. When it comes to Cawley and Bergmann, you have the right to make them prove that you owe them money before you pay it.

So if they are reporting on your credit report, don't panic. And whatever you do, don't pay them without making them prove the debt. Because if you don't make them prove it, you may end up paying a debt that isn't yours or paying money to a company that can't even prove you owe them anything.

Instead, reach out to the professionals at FightCollections.com for a free consultation. We specialize in challenging collection accounts and helping consumers recover damages when collectors violate their rights. So why not reach out to us today to see how we can help you?