Credit Management LP is a debt collection company that is no longer in business but still may appear on your credit report if you had dealings with them in the past.

In this article, we will cover:

- What to do if you find Credit Management LP on your credit report

- Why Credit Management LP is a red flag for your credit report

- Contact and other information about the company

- Their history of complaints filed against them

- Where the company tended to have issues

- Common complaints and how you might be able to dispute the debt

Credit Management LP Overview

It is never a good sign when you discover a collection account on your credit report. If the account is from Credit Management LP, it means you’re dealing with a debt collector that racked up one of the highest complaint counts in the industry before quietly ceasing operations. Understanding where the company fell short with consumers shows you exactly how to dispute their credit report entries.

Credit reports are full of errors. In fact, a study from U.S. PIRGs found that 79% of credit reports contain errors or other inaccuracies. Collection accounts are some of the most error-prone entries on credit reports, and the known compliance issues with Credit Management LP suggest you should take a closer look at any of their tradelines on your report.

About Credit Management LP

Credit Management LP is a debt collection agency that served as a subsidiary of the employee-owned company The CMI Group, Inc. Its headquarters was in the Dallas–Fort Worth area. They primarily collected debts for:

- Telecommunications companies including Comcast, Time Warner, Spectrum, Charter Communications, and CenturyLink

- Healthcare providers

- Utility companies

Here is some basic information about the company:

Credit Management LP Complaint History

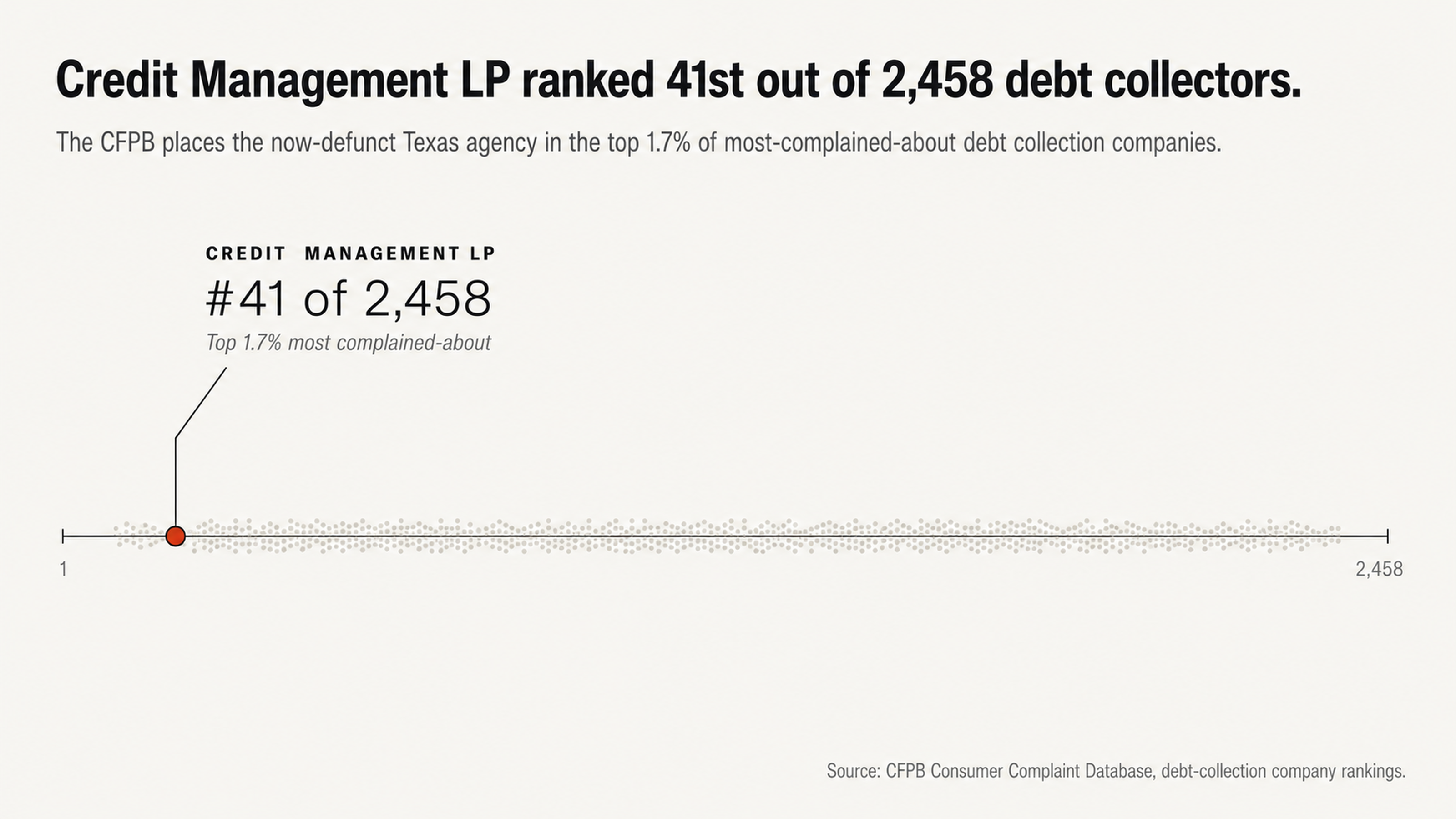

Credit Management LP was no small-time operation. The Consumer Financial Protection Bureau ranked the company 41 out of 2,458 debt collection companies for the sheer volume of complaints it received.

In fact, Credit Management LP ranked in the top 1.7% of most-complained-about debt collection companies in America. We’re not talking about an agency with the occasional blip on its radar. We’re talking about an agency with systemic issues as evidenced by data housed in federal databases.

Over the course of three years, the Better Business Bureau registered 217 complaints against Credit Management LP, and the company’s customer review rating was a dismal 1-star. Of the complaints filed, only 19.4% were resolved to the satisfaction of the consumer. Credit Management LP never achieved accreditation through the BBB, and its Google Reviews gave the company an equally unimpressive 1.7-star rating across 213 reviews.

The company has been party to approximately 26 federal lawsuits. Of those, nearly 15 were filed within a single three-year span and alleged debt collection harassment. These numbers are important because they give you insight into potential patterns and practices that create dispute avenues if you still have a Credit Management LP account on your credit report.

Compliance Analysis

A detailed compliance analysis of Credit Management LP shows repeated patterns of failure throughout the company’s existence. These aren’t theoretical issues. These are real patterns that consumers have successfully leveraged to dispute collection accounts.

According to the Consumer Financial Protection Bureau, Credit Management LP and its parent company have been the subject of over 919 complaints. Of those complaints, 78% resulted in non-monetary relief such as having a debt removed or an account corrected. Zero percent of complaints resulted in monetary relief to consumers, and 10% of complainants expressed dissatisfaction with the company’s response.

Top Reasons for Complaints

The top reasons for complaints against the company tell you exactly where Credit Management LP had issues. Consumers repeatedly complained that the company:

- Tried to collect debts they didn’t owe

- Failed to verify or validate debts

- Engaged in harassment in the form of excessive phone calls

- Made errors in credit reporting

Each of these categories represents a potential dispute avenue available to you under federal law.

One complainant to the CFPB said Credit Management LP informed credit reporting bureaus to delete a tradeline from their report but noted this action would not resolve the debt. Despite this admission, the tradeline remained on the consumer’s credit report. That is why it’s so important to have a third-party expert navigate the dispute process for you.

Identity Verification Issues

The majority of complaints against Credit Management LP revolved around identity verification issues. Consumers reported receiving collection notices for debts belonging to other people, for debts sent to addresses where they never resided, and for debts associated with services they never used.

One complainant represented by counsel said a Credit Management LP account associated with a Comcast debt lowered their credit score by 72 points. However, the complainant had lived in the same residence for over 11 years in an area where Comcast does not provide service.

Another complainant said they received 15 calls in a single week regarding a debt owed by someone named Greg. The complainant had the same phone number since 1999.

A third complainant said they received 19 robocalls to their cellular phone, seven days a week, multiple times per day including Sundays.

These complaints suggest Credit Management LP frequently called the wrong people.

When a debt collection agency can’t establish it has the right person, it can’t validate the debt. Under the Fair Credit Reporting Act, you’re entitled to have any information you dispute and cannot verify removed from your credit report. Known identity verification issues with Credit Management LP create natural dispute avenues for consumers who may have been improperly matched with debts.

Your Rights Under Federal Law

The Fair Debt Collection Practices Act and Fair Credit Reporting Act arm you with rights you may not know you have. Credit Management LP’s compliance history suggests the company frequently fell short of the requirements in these federal regulations.

Debt Validation Rights

Under the FDCPA, you have the right to request proof of any debt for which a collector says you’re responsible. That proof may include:

- The amount you owe

- The name of the original creditor

- Documentation to prove you owe the debt

Collectors who cannot provide that proof are obligated to suspend collection activity until they can validate the debt.

Repeatedly, consumers complained to the CFPB that Credit Management LP failed to validate debts despite a legal obligation to do so.

One complainant requested validation of a debt only to be told they had to pay it unless they could show they’d already paid a bill from seven years prior. That’s a reversal of the legal burden of proof. The burden is on the collector to prove the debt is valid, not on the consumer to prove it’s not.

In reality, many debts that end up at collection agencies like Credit Management LP cannot be validated. The paperwork is lost. The documentation is incomplete. There are gaps in the chain of ownership between the original creditor and the debt collection agency. In an industry infamous for lax record-keeping, challenging the validation of a debt can be a powerful tool.

Predictive Dialer Use and Legal Issues

Credit Management LP’s business records confirm the company used predictive dialers as part of its collection activities. In its Collection Services Agreement, the company said, “Upon receipt of work, CMI will contact customers via mail and predictive dialer.”

Using automated dialers without express consent is a violation of the Telephone Consumer Protection Act.

In the case of Lee v. Credit Management LP, a federal court in the Southern District of Texas allowed consumers’ claims regarding predictive dialer misuse, debt validation failures, and state law violations to survive summary judgment. The court found there was enough evidence for claims under the TCPA, FDCPA, and Texas Debt Collection Practices Act to go to trial. That case demonstrates the activities of Credit Management LP were legally questionable enough to warrant a full jury trial.

Debt collectors try to create a sense of urgency and use fear to motivate consumers to pay a debt without questioning whether they actually owe it. Abusive calling practices are part of that strategy. Understanding that certain calling practices may be against federal law gives you an upper hand in any dispute process.

Why Paying This Collector Could Be A Big Mistake

Before we dive into what you can do to remove this account, it’s important to understand why paying it off could be a mistake. Your instinct might be to simply pay off the account and be done with it. That’s what collectors are counting on. Before you do anything, you should understand why paying this debt could be a terrible idea.

The Dirty Little Secret They Don’t Want You To Know

Paying the account will update it to show as paid, but that’s about it. The account will still be on your report, and it will still show that you had a debt go to collections. That’s what has already damaged your credit, and paying it won’t make that go away.

For example, one complainant on the BBB site paid off the balance they owed to Credit Management, LP, totaling $917.69. Then, they received a call stating they actually owed another $458.85 because the check wasn’t received in time. The consumer called Credit Management, LP and disputed the charge, and was promised a refund.

However, after 60 days, the refund had not been issued, and the consumer was unable to reach customer service. Every time he called, he was sent straight to voicemail.

Furthermore, if you make a payment, you could inadvertently renew the statute of limitations on debts that have passed the statute of limitations. We saw several complaints from consumers that Credit Management, LP was trying to collect on debts from 10 years ago. If you acknowledge the debt by making a payment, you could open yourself up to a lawsuit for a debt you no longer owe.

How Missing Information Can Help You

Credit Management, LP primarily collected on debts for telecommunications and cable companies. These debts get sold and resold, and each time they change hands, the risk of error increases. We found a few complaints where Credit Management, LP didn’t follow procedure. According to one consumer:

Learned today that Credit Management LP does not wait to notify me within 5 days after they receive the file, nor do they wait the full 30 days to allow opportunity to dispute the invalid debt prior to reporting.

This is important because it gives you leverage. If a collector doesn’t have the information to show it followed these procedures, the credit bureaus are legally required to remove the debt until it is verified. That means instead of you having to prove the debt is incorrect, the burden shifts to the collector to prove it did everything right.

Working With A Pro

Removing a collection account from your credit report can be complicated and time-consuming. While you have the legal right to dispute the debt yourself, you may find that your chances of success improve dramatically when you work with a professional.

Why Consumers Rarely Get Results On Their Own

One reason for this is simple: debt collectors have entire teams of people dedicated to responding to disputes. They understand the law and know just what they need to say to verify the debt without having to prove it actually exists. You, on the other hand, are probably not an expert.

One firm that analyzed the behavior of Credit Management, LP noted:

For this debt collection agency, compliance seems to mean ensuring litigation costs are kept to a minimum, not ensuring the consumer protection laws are adhered to. The company employs specialized FDCPA and FCRA defense counsel and has a history of removing state court cases to federal court. This approach disadvantages the individual consumer.

Credit Management, LP is now out of business, which means you may not have any recourse if you send a validation request to the company directly. This can actually work to your advantage, as long as you file your dispute through the proper channels.

What Pros Can Accomplish Instead

When you bring a credit repair expert into the dispute process, you send a clear signal to the collector and to the credit bureaus that you are serious and you know your rights. You make it clear that you will not go away quietly.

Collectors know that credit repair professionals understand the law. They know the professionals will dig for every angle they can use to challenge the debt. And they know the professionals will pursue every option available to them.

We know that Credit Management, LP faced 26 federal lawsuits because consumers pursued professional help and discovered their rights had been violated. We know that in complaints handled through the CFPB, Credit Management, LP was responsible for providing non-monetary relief 78 percent of the time. That means most of the time, the company either removed the debt or corrected the information on the account because properly framed disputes resulted in relief for the consumer.

We also know that persistence pays off. When consumers keep pushing, especially when they keep pushing through the proper channels, they can often get results. Professional representation ensures your dispute gets done right, every step of the way. It ensures you understand and preserve your rights under the law. And it ensures you have the documentation you need if you decide to escalate the situation.

In many cases, the most powerful tool you have in your toolkit is your silence. But when you combine strategic silence with the right kind of action, you can accomplish even more.

Final Thoughts

Credit Management, LP racked up one of the most dismal records of compliance in the debt collection industry. The fact that the company ranked in the top 1.7 percent of most-complained-about debt collection agencies, combined with a pattern of identity verification issues, debt validation issues, and issues with aggressive calling, paints a picture of a company that prioritized collection at any cost.

Now that Credit Management, LP has closed its doors, as of October 2024, you might think you’re in the clear. But if the company still has accounts on your credit report, you are not. In fact, those accounts may still be affecting your credit score and your ability to get approved for a loan.

But the history of non-compliance that Credit Management, LP compiled during its nearly four decades of operation can provide the ammunition you need to finally get results.

Take Action Now

If you still have Credit Management, LP on your credit report, don’t assume you owe the debt or that you have no choice but to pay it. Given the pattern of identity verification issues, improper credit reporting procedures, and debt validation issues, it’s worth challenging any credit report entry from this company.

At FightCollections.com, we specialize in challenging improper collection entries and helping consumers hold debt collectors accountable for their behavior. We understand your rights under federal law and how to use the information in this article to help you craft an effective dispute that will get you results.

Reach out today for a free consultation to find out how we can help.