Before we dive in here, I want to get straight to the point. Professional Credit Service (PCS) has already paid out $2 million in a class action settlement over illegal wage garnishment fees. That is not a rumor. That is not speculation. That is a fact. It is a fact based on federal court records.

Every time you see a collection account on your report, the instinct is to panic, grab your phone, and start making promises. You assume they are right because you vaguely recognize the amount or you trust the original creditor they claim. You pay money that may not be owed at all and then wonder why your credit score does not really budge.

Stop. You do not owe them an explanation. They owe you one.

Collection agencies like Professional Credit Service deal in volume more than accuracy. That means there are errors in what they report. In fact, research from U.S. PIRGs indicates that 79% of credit reports contain some type of error or inaccuracies. It is not your job to assume they are correct. It is your job to make them prove it.

Who is Professional Credit Service?

Ray Klein, Inc., which does business as (DBA) Professional Credit Service, is a debt collection agency based in Oregon. Here are the details:

The company primarily handles healthcare and municipal debt in the Pacific Northwest. They have additional locations in Vancouver, WA; Bend, OR; Tukwila, WA; and Plymouth, MI. PCS is licensed to collect in states that include Nevada, North Carolina, and New York City.

What the Record Actually Shows

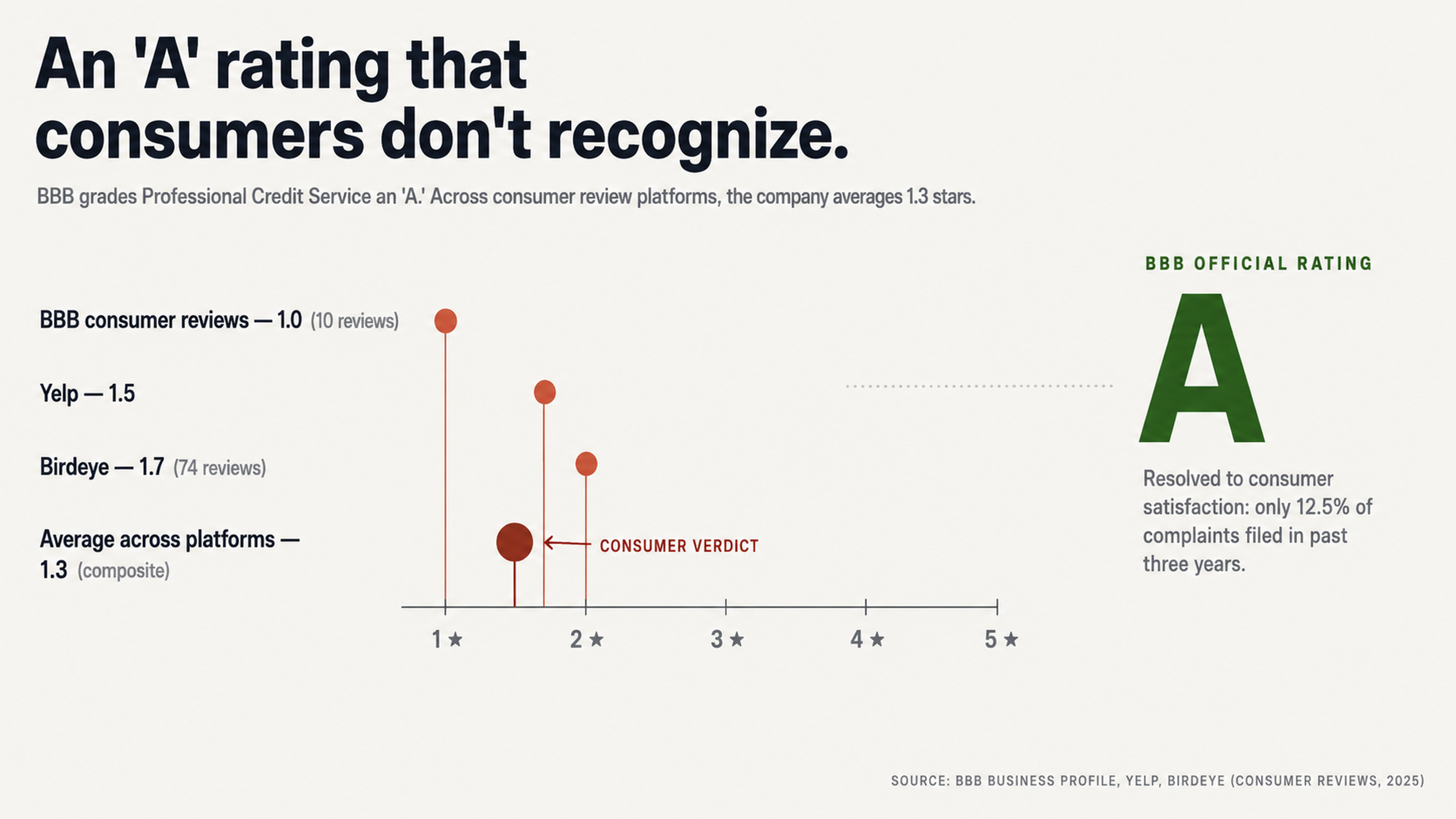

Professional Credit Service has an A rating from the Better Business Bureau. That sounds good, right? Well, here is what that rating does not tell you.

Professional Credit Service averages a 1-star consumer review rating across almost every platform. On the BBB site alone, all 10 reviews give the company a single star. The average on Yelp is 1.5 stars. The company averages 1.7 stars out of 74 reviews on Birdeye. The BBB reports 56 complaints against the company in the past three years. Of those, 12 complaints were closed in the last year alone.

The number to remember here is this: only 12.5% of complaints against this company resulted in resolutions that consumers found satisfactory. In other words, almost nine out of 10 consumers who complained to the BBB about Professional Credit Service walked away without a satisfactory resolution.

If you look at the record from the federal courts, the news gets even worse. According to PACER, Professional Credit Service has been a party in 143 cases. Of those, 55 were civil cases, most of them consumer complaints under the Fair Debt Collection Practices Act (FDCPA). This is not a company that got in trouble once or twice. This is a pattern.

The $2 Million Settlement They Do Not Want You to Know About

Illegal Wage Garnishment Fees

In May of 2022, the U.S. District Court for the District of Oregon approved a $2,000,000 settlement in the case of Russell and McKibben v. Ray Klein, Inc., (Case No. 19-cv-00001-MC). The plaintiffs alleged that Professional Credit Service engaged in systematic violations of Oregon state law governing consumer protections through the imposition of illegal fees.

Here is what happened.

Anytime PCS issued a wage garnishment, the company would tack on an additional $45 to the account for attorney fees. They argued that this was an appropriate charge under Oregon state law. The problem? Ray Klein, Inc. never hired any outside attorneys to issue the garnishments. Instead, they used in-house counsel to process the garnishments and then charged consumers as if the company was being billed for the services of outside counsel.

The class action alleged that this behavior was a violation of the Oregon Uniform Trade Practices Act, the Oregon Unlawful Debt Collection Practices Act, and the FDCPA. While Ray Klein, Inc. denied any wrongdoing as part of the settlement, $2 million says otherwise.

What This Means for Your Dispute

If you have a dispute with Professional Credit Service that involves wage garnishment, look carefully at the fees they are charging you. The settlement in this class action established that the company has engaged in systematic violations of the law. Any attorney fees associated with a garnishment or any other fees are worth challenging.

In a separate class action, McCurdy v. Professional Credit Service, the company paid a settlement over the language it used in debt validation notices. The notice instructed consumers to mail any disputes to a specific post office box address. The plaintiffs argued that this language violated disclosure requirements under the FDCPA. The company settled the class action, which is just another indication that it has a history of violating consumer protection laws.

Why You Should Never Pick Up the Phone

Phone Calls Are Traps

Debt collection agencies train their agents to try to get as much information as possible over the phone and to get you to commit to as much as possible over the phone. Phone calls are a trap for consumers for several reasons:

The conversation leaves no paper trail. The phone call opens the door for miscommunication and misunderstandings. Phone calls put you at a disadvantage. Anything you say on the phone can be used against you. Your statements can be used to restart the clock on the statute of limitations for a debt that might be too old to collect. Your statements can be used to confirm information the collection agency was not even sure it had correctly.

There is a complaint on the BBB website from October 2025 that illustrates this point perfectly: “Professional Credit Services has called me multiple times requesting payment for a debt. I have asked them 4 times to send me some paperwork verifying this, as I have no way to dispute the claim. They have refused to mail me anything at all. I do not trust just anyone calling me on the phone with all the fraud in this world today.”

There are multiple complaints just like this one in which consumers accuse Professional Credit Service of refusing to verify debts. Under 15 U.S.C. 1692g, a debt collector must provide written validation of a debt within five days of the initial contact and must stop collection efforts if the consumer disputes the debt within 30 days until such time as the company provides the requested verification.

When a debt collector is calling and calling but refusing to provide written verification, that is not persistence or an attempt to collect a valid debt. That is potentially a violation of federal law.

Silence is a Strategic Power Play

When debt collectors call you over and over again, they are using urgency and fear to get you to do something that is not in your best interest. When you answer the phone every time they call, you give them another chance to manipulate you into doing something that is not in your best interest. When you refuse to play along and engage in a conversation, you force the debt collector to communicate in writing, where their words can be preserved and used against them if necessary.

Do not call Professional Credit Service. Do not answer your phone when they call. Conduct all communications in writing and keep copies of everything. This is not about shirking responsibility and avoiding obligation. This is about protecting yourself from a debt collection agency with 143 federal cases and a 1-star rating with consumers.

Your Right to Demand Proof

Debt Verification Is Not Optional

Federal law gives you the right to demand proof of any debt a collector claims you owe. That includes the amount, the original creditor, proof that you actually owe this debt, and the date of your last payment. This isn’t a favor they do for you. This is your right.

Professional Credit Service has a documented history of wrong-person debt collection. A November 2025 BBB complaint involved PCS filing suit in Crook County (Case No. 25SC14262) over a St. Charles Health System bill where every signature was someone else’s. The consumer said there was no contract between them and the creditor. PCS agreed to return the account and file satisfaction of judgment, but only after the consumer filed complaints with CFPB and Oregon Division of Financial Regulation.

That consumer had to fight. They had to file multiple regulatory complaints to get resolution. The company didn’t voluntarily correct their mistake. This is why disputing first isn’t just a good idea. It’s essential.

What Proper Verification Looks Like

A legitimate debt verification response includes:

The original signed contract or agreement. A complete payment history that explains how they calculated the current balance. Proof they have the legal authority to collect this debt. Documentation that links you personally to the debt.

A form letter telling you again how much they think you owe isn’t verification.

Collection agencies care more about the quantity of collection attempts than the accuracy of the information. They buy debts in bulk, often without complete or accurate information. They don’t personally verify each account before they report it to the credit bureaus. This creates systemic weaknesses that work to your advantage when you demand documentation.

Understanding Harassment and Your Protections

What Collectors Cannot Legally Do

The Fair Debt Collection Practices Act lays out the rules. A collection agency can’t harass you with too many phone calls. They can’t threaten you with jail time for an unpaid debt. They can’t impersonate a government official or an attorney if they’re not one. They can’t discuss your debt with your neighbors, employer, or family members except under very specific circumstances.

A December 2025 review of Professional Credit Service said the company has a terrible communication system where you never can speak to someone who has any power to do anything. The reviewer called them the worst, most corrupt, incompetent and unorganized debt collector they had ever dealt with. Whether or not those accusations are true, they reflect the customer experience that has resulted in this company’s 1-star rating.

Website Dysfunction as a Red Flag

An October 2025 complaint accused PCS of website dysfunction. The consumer said instructions in collection letters told them to use a web portal to pay, except it was impossible to actually log on to the online pay system. They said they continued to get calls and letters while the pay system was broken, making the whole thing feel like a scam to get personal information.

When a debt collector makes it hard to verify information or pay through legitimate channels and keeps demanding payment anyway, that’s a potential compliance violation. Keep records of every failed log-in attempt, every broken link, every piece of correspondence that doesn’t match their stated policies.

Why Paying First Is Usually the Wrong Move

The Paid Collections Trap

Here’s what debt collectors don’t tell you when they push you to pay now. When you pay a collection account, you change the status from unpaid to paid, but the account remains on your credit report. You still have a negative mark. You still pay the credit consequences. The only thing that changes is you’re out money.

Even worse, when you pay an old debt, you can actually renew the statute of limitations and make yourself vulnerable to a lawsuit that would have been too old otherwise.

One consumer complaint involved a 2015 medical debt that PCS turned into more than $3,000 ten years later by obtaining judgment renewal extensions. The consumer said they had no idea a judgment even existed until that point.

That’s why verification and dispute always come before payment.

Collections Can Be Removed

A collection account can be removed from your credit report if the information is incorrect, erroneous, fraudulent, or cannot be verified within a reasonable amount of time.

Given that collection agencies prioritize volume over accuracy, the chances that you’ll find something disputable are better than you might think.

The key is to dispute it the right way. Credit bureaus have 30 days to investigate a dispute. If they can’t verify the information, they have to remove it. Professional Credit Service and every other debt collector has to be able to show documentation that proves the debt is yours, the amount is right, and they have the legal right to collect it. Many of them can’t when you challenge them properly.

Conclusion

Professional Credit Service has a documented history of legal violations, a $2 million settlement for illegal garnishment fees, 143 federal court cases, and customer satisfaction ratings that hover near the lowest possible rating on every available platform. Their A+ BBB rating comes with a 12.5% complaint resolution rate and repeated accusations of refusing verification and attempting to collect the wrong person’s debt.

That doesn’t mean you can ignore them. That means you shouldn’t trust them to get it right and shouldn’t assume they’ve already verified the debt they’re trying to collect. The information imbalance that usually works in the debt collector’s favor disappears when you understand their weaknesses and assert your legal rights.

Don’t pick up the phone. Don’t make verbal commitments. Don’t pay them a dime until you’ve demanded and received proper verification. And don’t assume you have to do this alone.

Take Action Now

Going up against a debt collector with 143 federal court cases isn’t something you should try without professional help. It takes more than just good intentions. It takes expertise in credit law, dispute procedures, and documentation strategies that most consumers don’t have time to learn.

At FightCollections.com, we specialize in disputing erroneous collection accounts and holding debt collectors to the standards they’re legally supposed to meet. We know how Professional Credit Service works, where their documentation usually falls short, and how to build a dispute case that gets results.

If Professional Credit Service is on your credit report, don’t wait until they garnish your wages or file a lawsuit. Don’t assume that paying them will make it all go away. Contact us today for a free consultation and find out what your options are in your individual case. The longer you wait, the more power they have. It’s time to take that power back.