Getting a credit report only to discover that Cavalry Portfolio Services is reporting a collection account can cause you to freak out.

By its name, you can tell they have an aggressive strategy when it comes to debt collection, and their history proves it. Before you commit an expensive mistake that could affect your credit report for a lifetime, you have to be clear on who is behind that entry, and how you can effectively deal with them.

This is the thing about credit reports that consumers are not telling you. Most people who see an account from Cavalry on their report do one of two things. Either they ignore it or pay the debt.

The problem is that doing any of those things without a clear plan could put you in a worse situation. You are about to learn the top reasons why you should not rush to make a payment without disputing that collection account.

So who exactly are they?

Cavalry Portfolio Services is a debt collection agency based in Greenwich, Connecticut. They act as the collection agent of Cavalry Investments, LLC, which has been in the debt buying industry since 1991. To ensure that you can find all the information you need when dealing with them, here are the company details to note:

They also have other entities such as Cavalry SPV I, LLC and Cavalry SPV II, LLC which are special purpose vehicles that hold portfolios of purchased debt. This is one of the ways in which debt buyers organize themselves. This structure is very common in the debt buying industry and could pose a challenge to you when trying to find out who the owner of the debt is.

What does the track record of this debt collector look like?

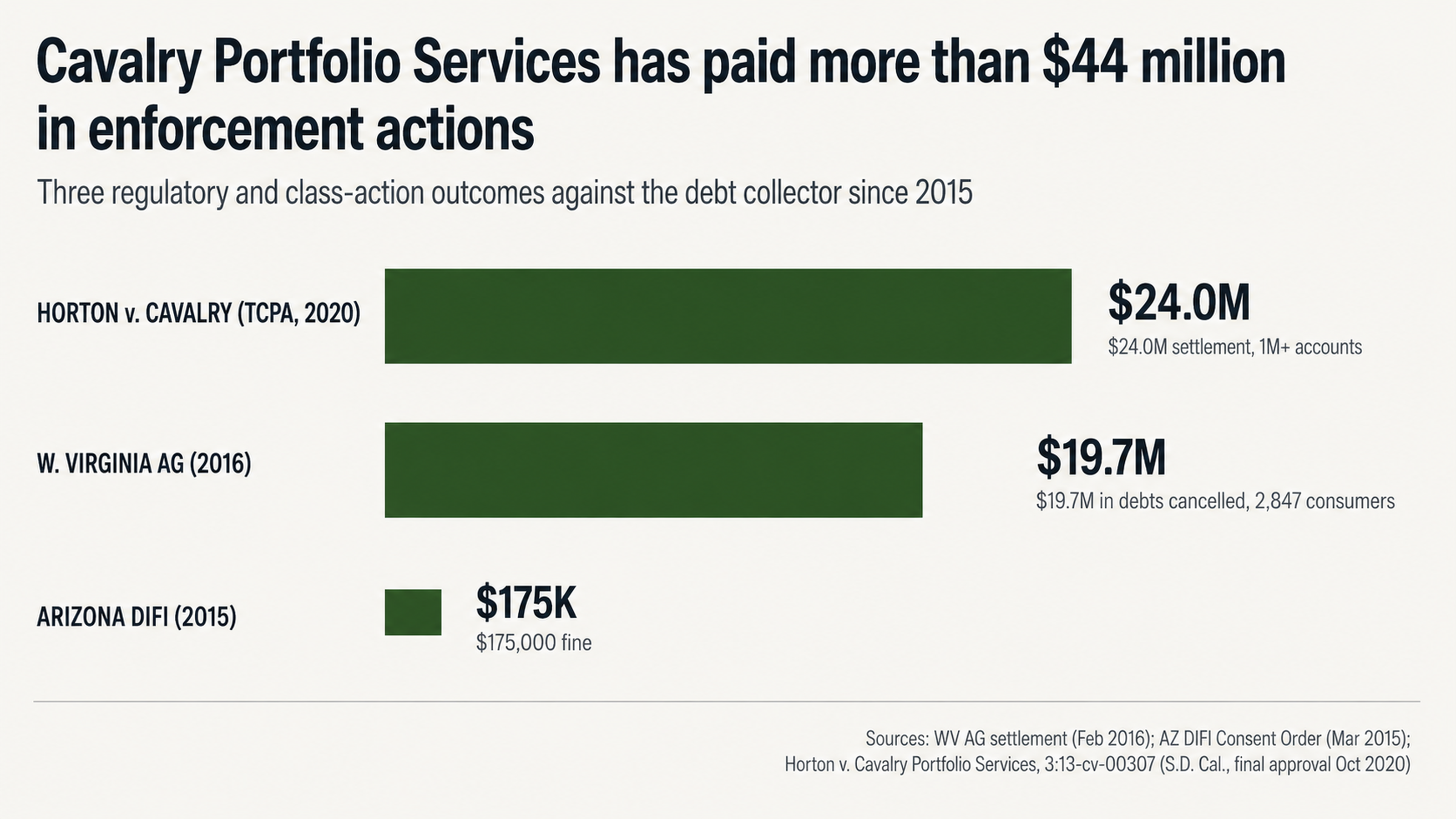

Here is an overview of what they have been up to. In February 2016, the West Virginia Attorney General reached a settlement with Cavalry Portfolio Services which demanded that the company cancel debts amounting to $19.7 million owed by 2,847 consumers. The company was operating in West Virginia without a license or surety bond yet were suing consumers.

In March 2015, the Arizona Department of Financial Institutions imposed a fine of $175,000 on the debt collection agency following an investigation into debt collection practices between 2007 and 2013. The investigation revealed that the company had consistently failed to respond to consumers’ requests for validation of debts yet continued to report disputed debts to credit bureaus.

There was also a class action settlement, Horton v. Cavalry Portfolio Services, in which the debt collection agency agreed to pay $24 million to settle claims that they had made illegal robocalls to over 1 million consumer accounts using automated dialing systems. Class members received payments in January 2021 after years of litigation.

On the Better Business Bureau website, there are 625 complaints that have been filed against Cavalry Portfolio Services in the last 3 years alone. The average rating of the debt collection agency on BBB is 1/5 stars. These complaints point to underlying issues with the way they operate.

What are the things that you are likely to do that will make matters worse?

Here is how most consumers react when they see an account from Cavalry Portfolio Services on their credit reports. If you see a collection account on your report, you will most likely feel obligated to pay it because of how it is making you feel. When you make a decision based on your emotions, you are very likely to make a mistake.

Paying the debt

The biggest mistake you can make when you see a collection account from Cavalry Portfolio Services is to pay it. According to U.S. PIRGs, 79% of credit reports contain errors or other major problems. This means there is a high likelihood that the debt is either not yours or the amount is incorrect.

Paying a collection does not remove it. All it does is change the status of the collection from unpaid to paid. It will still appear on your report for up to 7 years and could affect your credit score.

When you pay a collection, you could also be restarting the clock on the statute of limitations giving the debt collector more time to sue you. When you make a payment on an old debt, you could be acknowledging the debt.

Here is what one consumer experienced with Cavalry Portfolio Services on PissedConsumer: “Last payment to original creditor was December 2011, original creditor sold it to outside collectors and Cavalry obtained illegal judgement in 2018 when original creditor had already fell off national bureaus and numerous disputes and certified return receipt letters of dispute had been sent to them. Long story longer they put a lien on my property.”

Communicating with the debt collector

The other mistake you are likely to make is to call the debt collector and try to negotiate a payment plan. When you communicate with the debt collector directly, you are engaging with a professional who does this for a living. The collector knows exactly what to say to get you to admit that the debt is yours and commit to paying it. The more you talk to the debt collector, the higher your chances of saying something that could be used against you.

Everything you say can and will be used against you

When the debt collector calls you and you start talking, anything you say could be recorded and used against you. It is better to say nothing than to risk saying something that could be misinterpreted.

Here is what one consumer experienced when a debt collector called, according to a complaint filed with the BBB: “Calvary started garnishing my wages July/2024 for an alleged debt from 2009 that I DID NOT make! I had no knowledge of the debt until they garnished my check… Calvary can’t confirm the debt, I’ve requested proof and it’s not on my credit and has never been.”

Do not make a mistake that could put you in a worse situation. Here is what you need to know about your rights when dealing with a debt collector. Under the Fair Debt Collection Practices Act (FDCPA), the burden of proof is on the debt collector to show that you owe them money and the amount is what they are saying it is.

The debt collector must prove that the debt is yours

The FDCPA states that the debt collector must verify that you are indeed the consumer who owes the debt. They must also prove that the debt is not past the statute of limitations and that the amount is correct. The West Virginia settlement against Cavalry Portfolio Services involved debts that were past the statute of limitations yet the company was still filing law suits against consumers.

The debt collector must also prove that they have the right to collect the debt from you. In the Arizona settlement against Cavalry Portfolio Services, the debt collection agency was accused of failing to respond to consumer requests for debt validation yet still reporting the debt to credit bureaus. If the debt collector cannot provide documentation to support the claim, you do not have to pay them.

When you dispute a debt

When you dispute a debt on your credit report, the credit reporting agency must investigate and respond within a certain time frame. They must reach out to the debt collector and verify the information. If the debt collector cannot provide documentation to support the debt, the agency must remove it from your report.

One of the ways that credit reporting agencies verify debts is by sending letters to the debt collector requesting documentation. If the debt collector cannot provide that documentation, they cannot continue reporting the debt to your credit report.

Why you should dispute the debt

The best way to deal with a collection account from Cavalry Portfolio Services is to dispute it. This approach works because debt collectors rarely respond to disputes. The Arizona settlement against Cavalry Portfolio Services notes that the company had a history of ignoring consumer requests for validation and continuing to report the debt.

Most debts cannot be verified

Debt buyers like Cavalry Portfolio Services buy debts for pennies on the dollar.

In most cases, they do not get any documentation when they buy the debt. This means that when consumers dispute the debt, they have nothing to show that the debt is valid. If they cannot verify a debt, they must remove it from your report.

Many consumers do not know this. When they see a collection account, they just pay it even if they are not sure it is valid. It is very common for debt collectors to sell debts to other collectors multiple times. Each time a debt is sold, critical information could get lost. For debts that are very old, the original documentation may no longer be available.

Threats of lawsuits are empty

Debt collectors will always threaten you with a law suit to try and get you to pay a debt. The reality is that it is expensive to file a law suit and there is no guarantee that they will win.

For most debts, especially those that are past the statute of limitations, it does not make sense for the debt collector to file a law suit. They would rather accept a payment than incur the cost of a law suit.

In the West Virginia settlement against Cavalry Portfolio Services, the company was filing law suits against consumers in a state where they were not licensed to operate. They ended up having to cancel debts worth millions of dollars. Debt collectors who file frivolous law suits can end up losing.

Why you need professional help

While you could try to dispute a debt yourself, it is not the best approach. You are dealing with a professional debt collector who does this for a living. They know exactly what to say and do to get you to pay them. Unless you have experience with debt collection laws and practices, you could end up saying something that they could use against you.

Here is how working with a professional could help you. When you hire someone to help you dispute a debt, they act as a buffer between you and the debt collector. You do not have to talk to them or respond to their letters. This takes the emotional element out of the process.

Here is what one consumer experienced with Cavalry Portfolio Services, according to a complaint filed with the BBB: “Calvary started garnishing my wages July/2024 for an alleged debt from 2009 that I DID NOT make! I had no knowledge of the debt until they garnished my check… Calvary can’t confirm the debt, I’ve requested proof and it’s not on my credit and has never been.”

When you are emotional, you could make a mistake. This is why it is better to have a third party intervene.

They also know exactly what your rights are and how to enforce them. Unless you know your rights, you could end up allowing the debt collector to push you around. With professional help, you do not have to worry about saying or doing the wrong thing.

Conclusion

In conclusion, Cavalry Portfolio Services has a history of violating regulations. There have been enforcement actions worth over $44 million against the company. The company has thousands of complaints filed against it. Its history of failing to properly validate debts while still collecting on them provides consumers with an opportunity.

If you pay a collection account or communicate with the debt collector without getting professional help, you could be putting yourself in a worse situation. Instead, you should dispute the account. Here is why this approach works. The debt collector may not respond adequately to the dispute.

If the debt collector cannot verify a debt, they should not be collecting on it. They also cannot report it to your credit report. The best way to approach this is to dispute the account first before you pay it.

Are you ready to get started? Contact us today.