Credence Resource Management might have popped up on your credit report, but you're not the only one. This debt collection agency has been operating out of Dallas, Texas since 2013. They primarily focus on collecting debts for the telecommunications and healthcare industries.

Companies like AT&T, T-Mobile, DirecTV, Dish Network, and several medical providers hire Credence Resource Management to handle debt collection for them. They have call centers in Mumbai and Pune, India, and employ between 2,000 and 2,500 people. As a first- and third-party accounts receivable management company, they don't purchase debts. Instead, they collect debts on behalf of the original creditor. There's a big difference between those two roles, and we'll explain why in a minute.

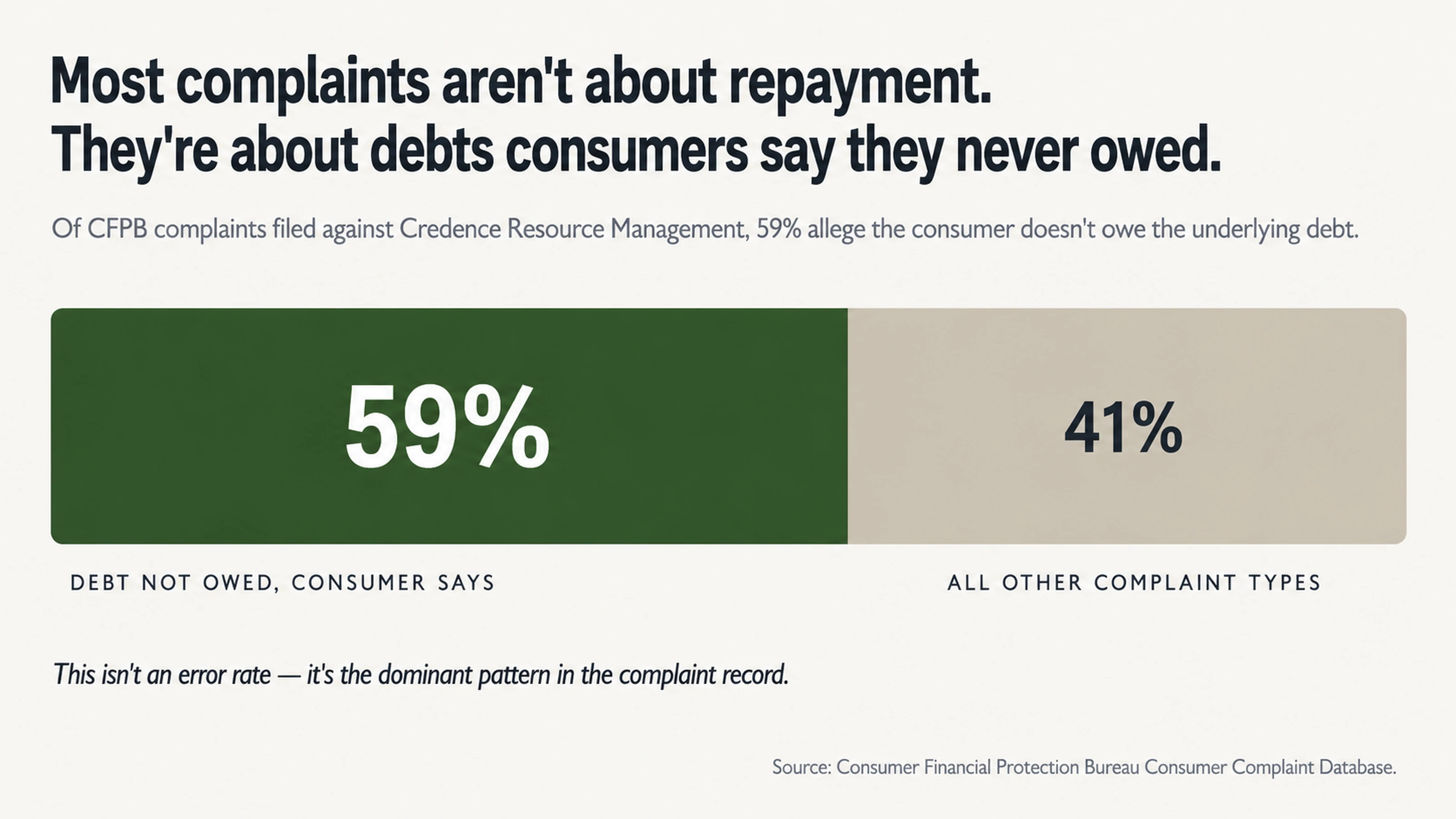

Their Regulatory and Complaint History is Alarming

To be blunt, Credence Resource Management has one of the worst regulatory and complaint records in the industry. In 2016, they were fined up to $50,000 by the Minnesota Department of Commerce. The company was operating without a collection agency license, failed to properly license collectors, and engaged in deceptive, abusive, or unlawful debt collection practices.

Federal court records show that Credence Resource Management has been named as a defendant in over 100 lawsuits across 19 different states. Most of those cases involved violations of the Fair Debt Collection Practices Act, Telephone Consumer Protection Act, and the Fair Credit Reporting Act.

The Better Business Bureau has received 1,969 complaints about this company, with 672 complaints in the last 12 months alone. But here's the statistic that you should pay the most attention to: 59% of the complaints filed with the Consumer Financial Protection Bureau against Credence Resource Management involved attempts to collect debts that consumers claim they never owed in the first place.

That's not an error rate. That's a business model. That's how likely it is that Credence Resource Management has no idea whether the accounts they're pursuing are actually valid.

Paying a Collection is Often a Terrible Idea

The Truth About Credit Scores and Collections

If you see a collection account on your report, your immediate reaction might be to pay the debt and move on with your life. We understand. Nobody wants to deal with this headache. However, the debt collection industry doesn't want you to realize that paying a collection doesn't make it go away.

When you pay a collection, the status is updated from "unpaid collection" to "paid collection." That's it. The account remains on your credit report for the full seven years from the date it first became delinquent, and it continues to affect your credit score. You just paid money for nothing, in terms of your credit score.

This is why the credit score damage is the real issue here, not the moral obligation to pay a debt. Settling the account is just as risky. You might negotiate a lesser balance that you agree to pay. Depending on the way the collection agency reports the account and the way the credit bureaus process that information, you might see some improvement in your credit score. You might see no change at all. In some cases, you might even see another decrease in your credit score. There are too many variables beyond your control to make this a reliable strategy.

The Realities of the Debt Industry

Here's a fact that might change your perspective on this situation. Collection accounts are like baseball cards. Somebody owes a debt to AT&T, so that debt gets bundled with thousands of other similar debts and sold to another company. Eventually, the debt ends up at a company like Credence Resource Management. By the time they receive it, that debt might have changed hands dozens of times.

Every time the debt is sold, transferred, or changes hands in any way, there's a risk that the associated paperwork and documentation get lost. There's a risk that the details of the account get scrambled or altered in some way. There's a risk that errors occur.

That's why 59% of the CFPB complaints against Credence Resource Management involve consumers saying they don't owe the debt. That's why the chain of custody for your financial data is more likely to be broken than it is to be intact.

These aren't sacred debts being passed from company to company with perfect documentation. These are commodities that are traded for pennies on the dollar. The moral obligation that debt collectors place on these debts, the idea that you owe this debt and you must pay it, doesn't always match the reality of how these accounts are traded and sold.

The Smart Way to Handle a Credence Resource Management Collection

Why You Should Dispute the Debt First

According to a study done by U.S. PIRGs, 79% of credit reports contain either errors or serious errors. That's not a typo. Almost four out of every five credit reports contain mistakes. When you combine that error rate with Credence Resource Management's history of pursuing debts that consumers say they don't owe, the odds say you should dispute the debt first.

You don't need to verify a collection account before placing it on somebody's credit report. You can simply report it, and suddenly they have a negative account bringing down their credit score. The onus is entirely on them to dispute it. That's a backwards system, but once you understand how it works, you can use it to your advantage.

We've already talked about the sheer volume of complaints against Credence Resource Management. Consumer reviews of the company show a pattern of documentation issues. One reviewer on the Better Business Bureau website said, "I have received several phone calls from the representatives of Credence Resource Management using words such as 'failure to comply' and 'will be escalated' and that they 'will have to serve the documents at my workplace or my home.' I find these statements very intimidating and the callers never state clearly what their business is or mention the name of their company."

When you dispute a debt, the collection agency must verify the debt. They need to provide documentation showing that you owe the debt and that you owe the amount they're claiming. Given Credence Resource Management's history, this is where they're most likely to slip up.

Using Their Documentation Issues Against Them

Consumer complaints show that Credence Resource Management often asks for sensitive information — like your Social Security number — before they'll even tell you what they think you owe. When consumers request validation of the debt, Credence Resource Management's standard response includes a generic summary instead of the original contract or payment history. Multiple lawsuits against the company allege that this is not sufficient under the FDCPA.

The company responds to 88.5% of the complaints filed with the Better Business Bureau, but they resolve only 11.5% of them. There's a huge difference between saying you've received a complaint and actually resolving the problem. If Credence Resource Management can't satisfy the Better Business Bureau, how well do you think they'll respond when you force them to verify the debt?

You can get a collection removed from your credit report if the information is inaccurate, incorrect, fraudulent, or if it can't be verified within a reasonable amount of time. Given the history we've discussed, disputing the debt gives you a legitimate chance to get the collection removed. Paying it doesn't.

What Happens if You Ignore a Debt Collector

The Threat of a Collection Lawsuit

Debt collectors use fear. They want you to believe that if you don't pay, they'll sue you. They'll take you to court. They'll garnish your wages. The reality is that most consumers will never see the inside of a courtroom.

Lawsuits are expensive. The debt collection agency needs to hire an attorney. They need to pay court fees. They need to spend time and resources preparing for the case. For most of the debts that consumers owe, the cost of a lawsuit doesn't make sense. Collectors know that. They're relying on you being afraid of the potential for a lawsuit rather than the reality of it.

This doesn't mean you should ignore the problem entirely. It means you should understand the actual risk rather than the risk they're trying to present.

Time is On Your Side

Negative accounts can only stay on your credit report for seven years from the date they first became delinquent. Every month that passes puts you one step closer to the end of that period.

Paying a debt or even acknowledging that it's valid can reset some of those time clocks in some states. That means you might extend the amount of time that a debt collector has to pursue you. This is another reason why it's often better to dispute the debt rather than paying it. You're not admitting that you owe the debt. You're challenging whether the information on your credit report is accurate.

By playing a waiting game and disputing when necessary, time becomes your ally. Collectors work on a constant cycle of accounts. If they can't verify that you owe the debt and you're not giving them any money, eventually they'll move on to the next account.

The Power of Remaining Silent

Remaining silent is a powerful strategy when dealing with debt collectors. Every single piece of information you volunteer can and will be used against you. Every time you have a conversation with a debt collector, it's an opportunity for a trained representative to push your buttons and get you to do something that isn't in your best interests.

By not engaging directly with the collector, you're protecting your interests while we handle the technical work.

Why Fighting a Debt Collector Alone Usually Fails

The Information Gap is Real

Debt collectors do this for a living. They work with consumers in your situation every single day. You might only deal with a debt collection agency once or twice in your entire life. That information gap creates an asymmetry that always favors the debt collector.

Credence Resource Management employs 2,000 people across eight locations worldwide. They have scripts. They have training programs. They have entire legal teams on staff. They know exactly what words to use and which buttons to push to get you to do what they want.

When you try to handle it on your own, you're negotiating blind. You don't know what documentation they actually have. You don't know your rights under the FDCPA, TCPA, and FCRA. You don't know which of their tactics cross the line into something illegal. They're counting on that.

How Debt Collectors Use Urgency Against You

Debt collectors know how to create a sense of urgency. They know how to make you feel like you have no choice but to pay today. They'll create arbitrary deadlines. They'll imply consequences that might not ever happen. They'll do whatever it takes to make you feel like your only option is to pay them immediately.

Every single one of those tactics is designed to prevent you from taking a step back and thinking clearly about your situation.

What Changes When You Have Professional Help

When you work with professionals who deal with debt collectors every day, you flip the information gap around. We know every tactic that Credence Resource Management uses because we've seen them hundreds of times. We know which state and federal laws apply to your situation. We know how to force verification and what to do when they fail to deliver.

Having a professional in your corner also means you don't have to talk directly with the debt collector anymore. No more stressful phone calls. No more feeling pressured to make a decision on the spot. No more accidentally saying something that hurts your case.

Remember that an employee reviewing the company on Trustpilot in May of 2025 said, "Over 80% of the people think it is a scam when the Indian call center calls US citizens." That same employee review said, "The managers do not care about verification; they only care about collecting the money."

You need somebody on your side who can match their level of aggressiveness with actual knowledge and expertise.

Take Control of Your Credit Report

The Bottom Line on Credence Resource Management

Credence Resource Management has a long history of regulatory violations, federal lawsuits, and consumer complaints. They were fined $50,000 by the Minnesota Department of Commerce. They've been named as defendants in over 100 federal lawsuits across 19 states. The Better Business Bureau has received almost 2,000 complaints about the company, with only an 11.5% resolution rate. 59% of the complaints filed with the CFPB involve consumers saying they don't owe the underlying debt.

If Credence Resource Management is listing a collection account on your credit report, the odds are pretty strong that something is wrong with that account. You might not owe the debt. You might not owe that amount. They might not have the paperwork to prove that you owe the debt. The statute of limitations might have expired.

Don't pay them a dime until you explore every other option. Don't let their threats and intimidation tactics force you into a decision that will not only leave that account on your credit report for another seven years, but will also put a dent in your bank account.

What to Do Next

Stop trying to navigate this on your own. The system is rigged against individual consumers, and Credence Resource Management knows exactly how to use that to their advantage.

At FightCollections.com, we specialize in fighting debt collectors like Credence Resource Management. We understand the Fair Debt Collection Practices Act like the back of our hand. We know how to force verification. We know how to identify violations. We know how to pursue removal of collection accounts that can't be properly verified.

Contact us today for a free consultation. We'll take a look at your situation. We'll examine what Credence Resource Management is saying you owe. We'll help you determine the best course of action to get this collection account off your credit report.

You deserve to understand your options before you make any decision that could impact your financial life for years to come. The first step is always the hardest. Once you have the right people in your corner, everything else gets a little bit easier.