Are you tired of dealing with the debt collectors at Dynamic Recovery Solutions? Want to know how to get them off your back? You’re in the right place.

Who Is Dynamic Recovery Solutions?

Dynamic Recovery Solutions, LLC (DRS) was a third-party debt collection agency based in Greenville, South Carolina. They acted as both a contingency collector and a debt buyer, working on behalf of large debt buyers like LVNV Funding, LLC, Jefferson Capital Systems, LLC, and Cavalry SPV I, LLC.

If you’ve seen this company name on your credit report, the first step to getting rid of it is to know what you can request, dispute, and demand.

Here’s what public records tell us about this agency:

What the Record Reveals About This Collector

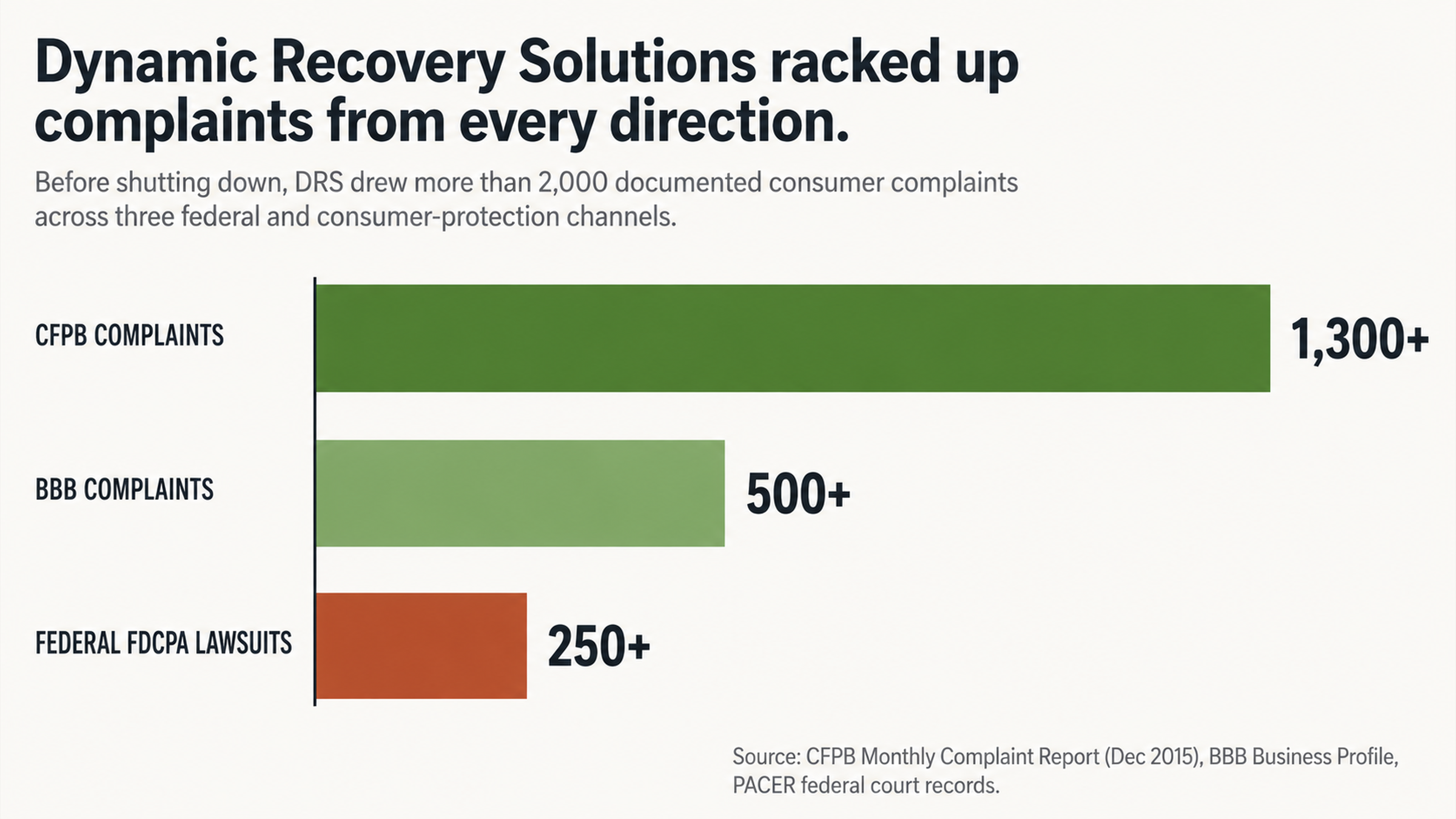

Dynamic Recovery Solutions racked up over 1,300 complaints in the Consumer Financial Protection Bureau’s (CFPB) complaint database, making them one of the most complained-about debt collectors in the country.

As of December 2015, DRS ranked number 16 out of 2,458 debt collection companies for total CFPB complaints. The top complaint category was “attempts to collect debt not owed,” with consumers reporting that they never had the account in question, had already paid the debt, or had discharged the debt through bankruptcy.

In addition to federal complaints, the company faced more than 250 federal lawsuits, with the vast majority alleging Fair Debt Collection Practices Act (FDCPA) violations.

In the class action case Park v. Dynamic Recovery Solutions, the court preliminarily approved a $130,000 settlement in August 2023 after finding that DRS sent misleading collection notices on time-barred debts without disclosing that partial payment could restart the statute of limitations.

Consumers also filed over 500 complaints through the Better Business Bureau, which ultimately assigned DRS an “Out-of-Business known or suspected” designation.

Most notably, after the complaints stacked up, the DRS website now redirects to Shepherd Outsourcing, LLC, a new entity incorporated in March 2021 under the same CEO, Eric Bergelson. Shepherd Outsourcing currently holds a BBB A+ rating and RMAI certification, essentially allowing the operation to continue collecting debts for the same creditors under a clean public profile while the old entity’s phone lines return errors and its customer portal sits offline.

Your Legal Rights When Dealing With Dynamic Recovery Solutions

Federal Protections That Apply to Every Consumer

When a debt collector contacts you, you have a specific set of rights under federal law that do not rely on whether the debt is valid. The Fair Debt Collection Practices Act (FDCPA) says that collectors cannot use deceptive, abusive, or unfair practices when attempting to collect. The Fair Credit Reporting Act (FCRA) says that every item on your credit report must be accurate, complete, and verifiable.

Under the FDCPA, you have the right to receive written notice of the debt within five days of initial contact, the right to dispute the debt within 30 days of that notice, and the right to demand that the collector cease communication entirely.

Under the FCRA, you have the right to dispute any item on your credit report that you believe is inaccurate or unverifiable, and the credit bureau must investigate within 30 days. These are not suggestions or courtesies. They are enforceable legal obligations that collectors must follow.

What You Are Entitled to Request: Requesting Debt Validation From DRS

Anytime you discover a collection from Dynamic Recovery Solutions on your credit report, you have the right to request validation of that debt. This is a formal process requiring the collector to provide documentation that proves the debt is legitimate, accurate, and currently collectible. It should include:

- The original contract with the creditor with your signature

- A detailed payment history to show how the current balance was determined

- Proof that DRS has the legal right to collect the debt

Do not make the mistake of thinking these are defensive actions. Instead, they’re offensive challenges that place the burden of proof on the debt collector. Debt buying and third-party collection agencies purchase accounts in massive portfolios. These portfolios may contain tens of thousands of individual account records and come with very little documentation.

When a consumer challenges the debt, the collection agency must respond by providing the requested documentation or end their collection efforts. Often, especially with very old debts or accounts that have been transferred through multiple agencies, the requested documentation does not exist. It was never part of the portfolio sale.

How to Dispute a DRS Collection Account

The Effectiveness of a Validation Letter

Don’t view a debt validation letter as simply a response. View it as an attack on DRS to produce the documentation that proves they actually have the right paperwork for the account they are reporting against your credit profile.

As outlined by the FDCPA, upon a written dispute by you within 30 days of the initial contact letter, the third-party collector is legally required to cease collection efforts until they have provided a legitimate validation of the account.

Given the number of complaints against DRS for attempting to collect debts for items that were never purchases, debts that were previously paid, and debts that were discharged in bankruptcy, any account that DRS places on your credit report is questionable. Debt collection agencies acquire accounts at an average of 4 cents on the dollar.

This means that any paperwork that may or may not have been provided with the account could be incomplete, outdated, or even lost. A validation letter forces this information to the surface. If DRS cannot provide a copy of the original agreement with the original creditor, proof of a transfer of ownership, and a complete accounting of payments, they have not fulfilled their responsibility.

An unverified account is an account that you can dispute with the credit bureau and potentially have removed from your credit report.

Why You Shouldn’t Speak

If DRS calls you, they are calling to get more information. Every word out of their mouth is aimed at confirming who you are, admitting that the account is yours, and gaining as much information as possible about you that they can use to their advantage. If you are speaking to them freely, giving them this information, you are giving them power that you cannot take away.

You may feel bad for not responding when a collection agent calls, but don’t. These people are trained to make you feel that way. They are trained to make you feel like you are doing something wrong by not speaking with them and giving them what they want. They will threaten to sue you, tell you that you will owe more money if you don’t pay now, or tell you that the settlement offer they have given you will expire if you don’t act quickly.

DRS consumers have reported being called from over 26 different phone numbers, being contacted at their workplace, being contacted through family and friends, and even receiving robo-calls that alternate between a “first attempt” to contact and a “final attempt” to contact. All of these actions are aimed at getting you to respond so that they can gain information from you.

The reason that DRS wants you to speak with them is because information is power. In almost all collection calls, the agent on the other end of the phone has more information than you do. They have your name, an account number, and a balance. What they may not have is proof of any of it.

Keeping your personal information to yourself and only allowing a professional credit repair expert to communicate with them on your behalf keeps the control of the situation in your court. It puts the burden back on DRS to prove their claim, which they many times cannot do.

Why You Need Help

The Job of a Credit Repair Company

If you try to handle a credit repair issue on your own, you will need to know and understand your rights under both federal and state law, you will need to properly word correspondence, you will need to understand the timeline for responses and actions, and you will need to make sure that you are interpreting responses correctly and not inadvertently admitting to something that may damage your claim.

A simple admission of the debt on a recorded line could cost you an otherwise open-and-shut case. Missing a deadline could mean forfeiting rights that you didn’t even know that you had.

A professional credit repair expert will understand the process and the procedures that must be followed for each potential collection account. They will know what to look for to find errors, omissions, or simple violations of regulation that will become the grounds for removal of the account.

Given a debt collection company like DRS, which was the subject of over 1,300 complaints filed with the Consumer Financial Protection Bureau and over 250 federal lawsuits prior to ceasing operations, it is likely that the accounts are not entirely accurate, properly documented, or entirely valid.

Working with a professional means that the emotional leverage often used by collection agents is neutralized. Intimidation, confusion, and time sensitivity are the currency of the debt collection industry. Someone who communicates with these firms for a living is not intimidated, confused, or operating under an artificial time constraint, which helps to ensure a better outcome.

The Dispute Process That Works

A successful dispute process starts with a comprehensive review of all three of your credit reports to isolate every potentially disputable item. For collection accounts, the analysis goes beyond whether you recognize the debt to whether every legal aspect of the account is being reported in accordance with FCRA standards.

Disputes are submitted with specific supporting documentation that speaks directly to the defect(s) in the account. The credit reporting agency has 30 days to investigate, and if the collection firm cannot verify the account with the proper documentation, it must be deleted from your report.

Now that DRS is classified as out of business by the Better Business Bureau, with disconnected phone lines and an inactive website, it is worth questioning whether the company can fulfill verification requests within the requisite 30-day window.

Time is of the essence. Uncontested collection accounts on your credit report are impacting your ability to find housing, gain employment, and qualify for credit. Though the direct threat of a lawsuit from a collection company is statistically low, the impact of an unresolved collection account is very real and very much ongoing.

The sooner you initiate the dispute process, the sooner you can have questionable items addressed.

The Road to Removing Dynamic Recovery Solutions From Your Report

Over the course of its existence, Dynamic Recovery Solutions amassed a legacy that includes more than 1,300 complaints filed with the CFPB, in excess of 250 lawsuits, and hundreds of complaints registered with the Better Business Bureau before shutting its doors and resurrecting under a new moniker.

Consumers who made payments to the firm are now saying they are unable to reach the company or access records of their payments. The collection accounts that DRS placed on credit reports across the nation did not simply disappear when the company did.

If you find that Dynamic Recovery Solutions is on your credit report, you have the legal right to challenge it. You have the right to request documentation. You have the right to dispute any information that you find to be inaccurate. You have the right to have accounts that cannot be properly verified removed from your report. You do not have to go through that process alone.

Contact the team at FightCollections.com today for a free consultation. We will obtain copies of all three of your credit reports, identify every item that you may have reason to dispute, and manage the entire process for you.

Your credit report should accurately reflect your true credit history, not the claims of a debt collection agency that was unable to keep its own house in order.