Have you been “hit” with an unfamiliar collection account from FCR Services?

When you see FCR Services as the source of the account, you need to know that this debt collector has a history of consumer complaints, CFPB investigation, and federal lawsuits. Knowing who they are is the first step to taking back control of your credit report.

When you have any collection account on your credit report, it harms your credit score. That impact will remain for 7 years, from the original date of delinquency, even if you pay the account. This is why simply paying a collection account just updates the account status from “unpaid” to “paid” but still leaves the account as a credit score detractor on your report.

Did you know that, according to U.S. PIRG, 79% of credit reports contain errors or other serious issues? This means that FCR Services may have reported the account on your credit report with errors, which would allow you to have the account deleted entirely. You just need to know how to use your rights to challenge the account.

Who is FCR Services?

FCR Services is a trade name for FedChex Recovery, LLC. They are a debt collection agency based in California. FCR Services is known for collecting NSF checks, textbook rental fees for colleges and universities, medical bills, and utility bills. They have multiple websites, including fcrcollectionservices.com, fedchex.com, and paymybook.com. Their estimated annual revenue is between $6.4 and $7.6 million.

History of Regulation

FCR Services has been the subject of a CFPB investigation.

On November 20, 2019, the Consumer Financial Protection Bureau issued a Civil Investigative Demand to FedChex Recovery to determine if the debt collector ignored warnings that debts were the result of identity theft and if they disregarded consumers’ requests to cease contact. They were also investigating if the debt collector failed to correct information they provided to credit reporting agencies.

FedChex attempted to have the investigation dismissed, but the CFPB denied their request in January 2020.

On June 20, 2019, Connecticut regulators issued a Consent Order to the company after determining that FCR Services was operating in the state under an unregistered assumed name. During the investigation, regulators found that the company had sent collection letters to consumers in the state using an assumed name that was not registered with the licensing authority. The violation could have resulted in a penalty of up to $100,000 per violation, but the company paid a $2,500 civil penalty instead.

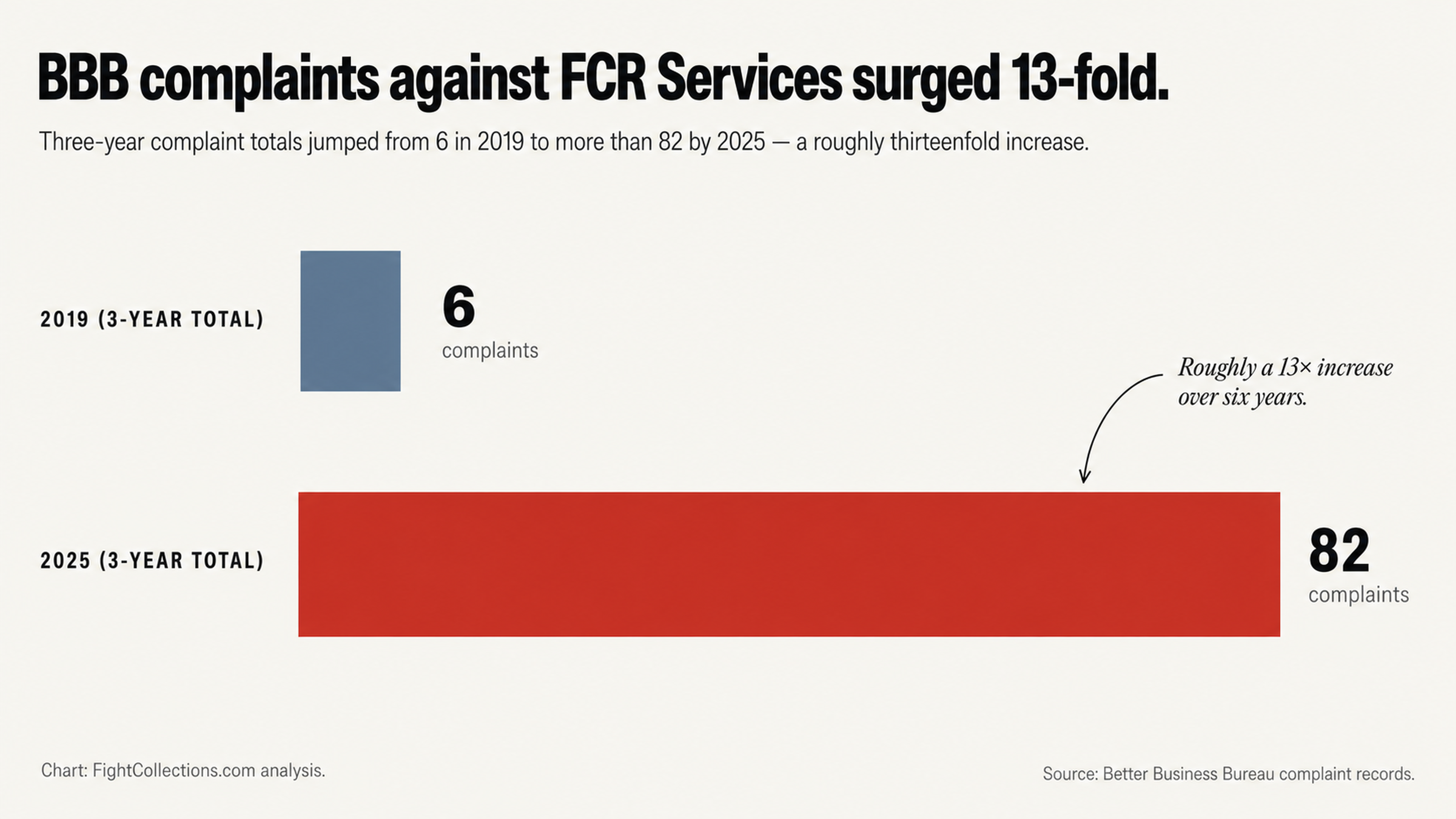

Finally, it is worth noting that the number of complaints filed against FCR Services with the Better Business Bureau has increased dramatically.

In 2019, the company had 6 complaints filed over a three-year period. By 2025, the number of complaints filed in a three-year period increased to over 82. This is roughly a 13-fold increase in the number of complaints that consumers have filed against FCR Services.

How FCR Services Works

What Do They Collect? How Do They Operate?

FCR Services is primarily a debt collector for colleges and universities. Specifically, they collect debts related to textbook rental programs through college bookstores. In addition, they collect medical debt, utility bills, and NSF checks. Understanding what they do and how they operate is crucial to your ability to effectively challenge them.

Debt collectors work on very tight profit margins. This means that every month that a debt remains in collections is another month that the debt collector is not earning the profit they need. This means that they often do not have the time or resources to verify that the information they have about a debt is accurate and complete, especially if you force them to do so.

Many of the complaints filed against FCR Services indicate that the company contacts consumers very frequently. In one response to a complaint filed with the BBB, FCR Services indicated that they had sent a consumer 4 text messages, 9 emails, and attempted to call them 22 times.

Clearly, the company is relying on a strategy of simply wearing the consumer down. In many cases, consumers who are facing collection calls will pay a debt simply to get the phone to stop ringing.

Fee Issues

Federal court records show that FCR Services has been sued repeatedly for allegedly adding collection fees to consumers’ debts without permission. In Spencer v. FEDChex Recovery LLC, a class-action lawsuit filed in the Southern District of Texas, the plaintiffs claimed that the company added a $30 collection fee to a textbook rental debt of $117.41. The fee represented a 26% fee that the plaintiffs said was not permitted by the underlying contract or by law.

There have been similar lawsuits filed in at least six other states, including Illinois, Pennsylvania, California, Florida, and Georgia. In each of those cases, the plaintiffs alleged that FCR Services added a fee of 25% to 30% to educational debts. If FCR Services added a fee to your debt without your permission, you may have grounds to dispute the entire debt.

Why Paying FCR Services May Not Be a Good Idea

Why Paying the Debt May Be a Huge Mistake

When you see a collection account on your credit report, your first instinct may be to just pay the debt and move on. However, doing so may be a huge mistake. Paying a collection account does not mean that it will be removed from your credit report. Instead, it will simply be noted as “paid,” and will remain on your report where it will continue to harm your credit score for the full 7 years.

One of the reasons that debt collectors are able to coerce consumers into paying debts is that consumers are under stress. When you are facing financial issues, you may not be in the best position to make rational decisions about how to proceed. Debt collectors understand this and will often use every tool at their disposal to coerce consumers into paying a debt. This may include calling repeatedly or sending threatening letters.

Just ignoring the debt collector and waiting for them to get tired and go away can often be an effective strategy. One of the reasons that consumers end up paying debts is that they do not understand their legal rights. Under the FDCPA and FCRA, consumers have substantial rights that allow them to challenge unfair and inaccurate credit reporting.

However, most consumers do not understand these rights, which means that debt collectors can often simply run right over them.

Under the FDCPA, debt collectors are required to verify the debts that they are attempting to collect. This means that they must be able to show that you owe the debt, that the amount they are attempting to collect is accurate, and that they have the legal right to collect the debt.

In many cases, especially when debt collectors are collecting on purchased debt, they may not have access to all of the information they need to meet this burden.

Multiple consumers have filed complaints indicating that FCR Services failed to provide them with written verification of debts. In one complaint filed with the BBB, a consumer indicated that the company had called her using a robocall but that she had not received any written communication from the company despite nearly a year of calls.

Under the FDCPA, debt collectors are required to provide written notice to consumers within 5 days of initial contact. If FCR Services is failing to meet this obligation, consumers may have grounds for disputing the debt.

If the debt collector cannot verify a debt or if they fail to respond to a request for verification, the consumer may have grounds to have the account removed from their credit report entirely. The burden of proof is on the debt collector, not the consumer, which is why many consumers find it effective to always dispute a debt first.

The Real Story of Consumers’ Experience with FCR Services

Reading Between the Lines of Consumer Reviews

FCR Services has an A- rating from the Better Business Bureau, but the company has an average customer review rating of just 1.11 out of 5 stars. This discrepancy is a good illustration of how consumers need to read between the lines when evaluating reviews of debt collectors. The BBB rating is based on the company’s complaint response process, not its customer service. Consumers who are dealing with debt collectors like FCR Services need to understand how to effectively use those complaints to their advantage.

One consumer said: “They violate state Statutes of Limitations for debts. They have been harassing me for 9 years for a false debt.”

Another consumer reported: “FCR Collection Services have been abusing their rights and violating collection laws and statutes by calling, texting, and emailing me between 4 to upwards of 17 times per day for a supposed textbook debt.”

These stories from other consumers can provide valuable insight into the ways that FCR Services may be violating consumers’ rights.

Common Issues

We have evaluated complaints filed against FCR Services on multiple platforms and have identified several common issues, including:

Failure to provide written verification of the debt, as required by law

Attempting to collect debts that the consumer has already paid or disputes the validity of, often related to textbook rental

Attempting to collect debts using excessive contact, which may constitute harassment under the FDCPA

Attempting to collect debts outside of the applicable statute of limitations

Adding unauthorized fees to debts

A reviewer on ComplaintsBoard reported: “I have received robocalls from FCR Collection Services for almost a year. They are calling to leave voicemails stating I owe them money for a textbook rental. I owe them nothing. I have not received any written communication from this company, just robocalls.”

This consumer’s experience illustrates several potential violations of the FDCPA in a single consumer’s experience.

An expert in the credit industry has pointed out that FCR Services gets such negative reviews because of its aggressive tactics. While those tactics may help the company rake in the dough in the short term, they also increase its exposure to liability in the long term. That is good news for consumers who know how to assert their rights.

Getting FCR Services Off Your Credit Report

Why You May Need Professional Help

Removing a collection account from your credit report requires a strong understanding of federal and state consumer protection laws. It also requires that you understand how to effectively format your disputes and when to file them. Making a mistake could not only mean continued damage to your credit report, but may also strengthen the debt collector’s position.

Working with a professional credit repair expert can help you effectively navigate the process and meet all necessary requirements. In addition, because credit repair experts work with these laws on a daily basis, they understand exactly which documents to request and how to word your disputes for the best possible outcome.

Filing multiple disputes and/or inquiries on the same debt will not “hurt” your credit report any more than the collection account already has. This means that allowing a professional credit repair expert to investigate and challenge the account does not put you at any additional risk while greatly increasing the likelihood of a successful removal.

You can get a collection removed from your credit report if it contains incorrect information, is erroneous, is fraudulent, or if the collector cannot verify the information within the legal time limit.

Given FCR Services’ history of regulatory actions, federal lawsuits alleging that the company is adding unauthorized fees to consumers’ debts, and complaints alleging that the company is violating consumers’ rights, there is a good chance that at least some of the information FCR Services has reported to the credit bureaus about you is incorrect or cannot be verified.

Getting Started Now

Do you need to remove a collection account from FCR Services from your credit report? The longer you wait, the more damage the account will do to your credit score. Start by clicking here to schedule a free consultation today.

Conclusion

FCR Services has a history that includes a CFPB investigation, a state regulatory action, federal lawsuits in at least six states, and a 13-fold increase in the number of complaints consumers have filed against the company over a recent six-year period. The company has been accused of adding unauthorized fees to consumers’ debts and is the subject of repeated accusations that it is violating consumers’ rights.

Given this history, if FCR Services has placed a collection account on your credit report, there is a good chance that the information it has reported is incorrect or cannot be verified, which would allow you to have it removed.

Paying a collection account will not remove it from your credit report and may not even be necessary if the information is incorrect or cannot be verified. Challenging the debt is usually the best course of action.

What’s Next?

If you have a collection account on your credit report from FCR Services, it is essential that you take action as soon as possible.

At FightCollections.com, we specialize in challenging collection accounts and using federal consumer protection laws to identify errors and verification issues that can support removal of the accounts. Our specialists understand the history and practices of companies like FCR Services, and they can help you navigate the process.

Request your free consultation now to allow us to evaluate your situation and develop a strategy that is tailored to your needs. You do not have to face FCR Services on your own. Let us evaluate your situation and develop a strategy that is tailored to your needs.

Why not take the first step today toward removing FCR Services from your credit report?

Contact FightCollections.com today to allow us to help you determine how we can help you meet your goals.