Seeing an unknown name on your credit report can send a shiver down your spine. If that name is Nathan & Nathan, P.C., you might feel like your whole world is crashing down.

The sensation in the pit of your stomach is not fear — it’s a perfectly rational response to a system intended to make you feel hopeless. It’s intended to make you feel like giving up. Most consumers who find this law firm on their credit report report feeling embarrassed, disoriented, and willing to do whatever it takes to make the problem disappear.

That’s exactly what the collectors are hoping for. They know that when you act out of fear, you’re likely to make rash decisions that you’ll later regret.

What they don’t want you to know is that you have more control over this situation than you think. You don’t have to rush to respond, and you certainly don’t have to pay them right now. You just need information, a little patience, and a solid strategy that puts you first.

Who is Nathan & Nathan?

Nathan & Nathan, P.C. is a debt collection law firm based in Birmingham, Alabama. Instead of relying on phone calls and letters like most collection agencies, this company uses the courts to pursue consumers — and files lawsuits in several states across the Southeast.

The truth is, there are many things that can be done to challenge the presence of a collection account on your report. The purpose of this article is to educate you about how the credit reporting system really works and how you can take advantage of this knowledge to fight back against firms like Nathan & Nathan.

The Story of Nathan & Nathan, PLLC

What We Found Out about Nathan & Nathan

Nathan & Nathan is a law firm that represents several large creditors including Capital One, Discover Bank and National Collegiate Student Loan Trust (NCSLT). We have reports from consumer protection lawyers that Nathan & Nathan has filed multiple lawsuits against student loan borrowers in the name of NCSLT, seeking over $100,000 in many cases.

This firm is accredited by the Better Business Bureau with an A+ rating. Unfortunately, consumer reviews are a different story with an average rating of 1 out of 5 stars. Of the 11 complaints closed in the last 3 years, only 2 of them were resolved satisfactorily to the consumer, which is a rate of 18%.

The most common complaint closed with BBB is: Customer contacted Nathan & Nathan and received no response from them. In fact, 73% of the complaints against this firm with the BBB were for the same reason.

One consumer left this comment when describing her experience: “They even sent my job a garnishment and my payment wasn't even due until the next week.”

What This Means to You

It is clear that Nathan & Nathan is not very interested in talking to consumers. But this is nothing new for a debt collection law firm. The real question is how does this impact you as a consumer?

The answer is, it puts more power in your hands. This firm has proven to be unresponsive to consumer complaints and requests, but that will not stop them from threatening to sue you if you don’t pay. Keep in mind that you do have rights as a consumer and you should take action to exercise those rights when dealing with this firm.

The Intimidation of a Collection Letter

Did You Get a Collection Letter from Nathan & Nathan?

When you open a letter from a law firm, it can be pretty intimidating, but before you have a heart attack and start making payments without getting all the facts, take a step back and try to understand the situation. A collection letter is designed to scare you into action without giving you all of the information you need.

When a debt collection law firm sends a letter to a consumer, they want to create a sense of urgency and panic so the consumer will make a decision quickly. What happens when you act quickly? You make a mistake.

The thing is, you probably don’t owe the debt, at least not in the amount they say you do. Or, you may have already paid the debt and they are trying to collect it again. The list of possibilities goes on and on, but the point is, you should never act quickly when dealing with a debt collector. A lot of times a collection agency will make threats about suing you if you don’t pay.

So when you get a letter from Nathan & Nathan or any other law firm, remain calm and take time to think about the situation.

What’s REALLY Going On with Your Debt…

Information and power are not always equal. Chances are, the debt collection law firm knows more about the debt than you do. They have access to more information and they know the laws that apply to debt collection. This is a distinct advantage for them, but there are things you can do to even the playing field.

One of the best ways to protect yourself from a debt collector is to use their power against them. When you know how to use the laws in your favor, you can force the debt collector to prove the debt and follow the law. But there is more…

Why Credit Reports are Mostly Wrong

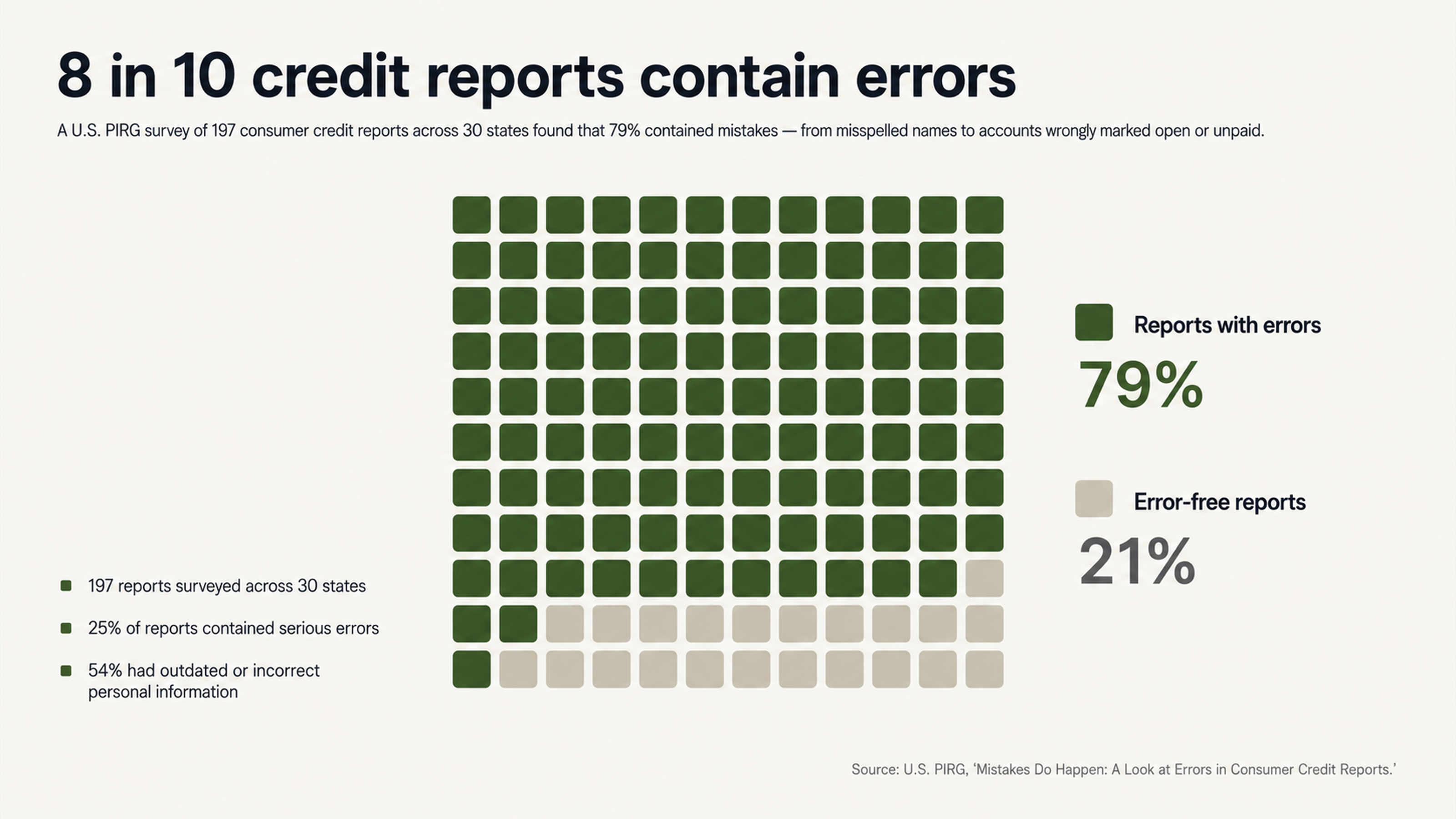

Almost 80% of credit reports contain some type of error. So when a debt collector puts a collection account on your credit report, it may be wrong. In fact, it probably is. When this happens, there are steps you can take to dispute the account and get it removed, but first, you have to understand how the credit reporting system really works.

Credit reports are used to determine credit worthiness. This report contains information about every time you applied for credit, every credit account you have or have had and how well you have managed your credit accounts.

There are three credit reporting agencies that collect this information: Experian, Trans Union and Equifax. Every time you apply for credit, a credit report is generated and the information on the report is used to determine whether you will qualify for the credit and what your interest rate will be.

A credit report contains information from credit grantors, public records and debt collection agencies. When a debt collection agency reports a collection account to one or more of the credit reporting agencies, it is added to your report and used to calculate your credit score. The problem is, most credit reports are wrong.

According to U.S. PIRG, 79% of credit reports contain some type of error. That’s 8 out of 10 credit reports that contain an error. And we aren’t just talking about small errors. Most of the errors on credit reports are significant and can make a big difference in whether you qualify for credit and what interest rate you pay.

But how does this happen?

The answer is simple. Credit reports are generated when information from creditors, public records and debt collectors is reported to the credit reporting agencies. This information is used to determine credit worthiness, but sometimes, the information is wrong. When a debt collector reports a collection account, they may not have the right documentation or they may misrepresent the amount of the debt or the name of the creditor. This is just one way errors can end up on your credit report.

Why You Should Dispute Every Debt

Are you starting to understand why you should dispute every debt that you find on your credit report? It’s because credit reports are wrong most of the time and debt collectors will misrepresent debts to collect money from you. When a debt collector reports a collection account to one or more of the credit reporting agencies, they are stating that you owe the debt. But how do you know if this is true? You don’t, at least not without doing some investigating.

The Fair Debt Collection Practices Act (FDCPA) gives consumers the right to request verification of a debt any time a debt collector contacts them. If the debt collector cannot verify the debt, you don’t have to pay it.

But that’s not all.

Under The Fair Credit Reporting Act (FCRA), you have the right to dispute information on your credit report. When you dispute information, the credit reporting agency has to investigate and verify the information. If they can’t verify it, they have to remove it from your report.

When a debt collector reports a collection account and you dispute it, they have to verify the debt or the account will be removed from your report.

Why Paying a Collection Agency is a Bad Idea

When a collection agency puts a collection account on your credit report, your first thought may be to just pay the account and get it over with. This is understandable. The process of disputing a debt and dealing with a collection agency can be time consuming and frustrating. But paying may not be the best option. Here are some reasons why:

Paying the debt will not remove the account from your credit report. When you pay a collection account, the account status will change from “unpaid collection” to “paid collection”, but the account will still remain on your credit report for 7 years from original delinquency.

A paid collection will still affect your credit score. Paying a collection account will not remove the account from your report and it will still affect your credit score.

You may not owe the debt. We have talked about this before, but it bears repeating. You may not owe the debt that the collection agency is trying to collect. Sometimes debts are sold multiple times and resold to unsuspecting consumers. Sometimes the wrong consumer is targeted. Whatever the case, you shouldn’t pay a debt that you don’t owe.

How the Credit Dispute Process Works

A Guide to Removing a Collection Account from Your Report

Now that we have talked about why you should dispute a collection account from Nathan & Nathan or any other collection agency, let’s talk about how the credit dispute process works. The process is pretty simple, but there are some rules you have to follow and deadlines you have to meet. Here are the steps involved in disputing a collection account:

Step 1: Write a Dispute Letter

The first thing you have to do is write a dispute letter to the credit reporting agency where the disputed account is reported. In the letter, you should clearly identify the account you are disputing and the reason for the dispute.

Step 2: Send the Letter to the Credit Reporting Agency

Once you have written the dispute letter, you should send it certified mail with return receipt requested. This will give you proof that the credit reporting agency received your letter and the date they received it.

Step 3: The Credit Reporting Agency Will Investigate

The credit reporting agency has 30 days from the receipt of your dispute letter to investigate the disputed account. During the investigation, they will contact the creditor and ask for verification of the debt. If the creditor cannot verify the debt, the account must be removed from your report.

Step 4: The Investigation Results

When the investigation is complete, the credit reporting agency will contact you with the results. If the account is removed from your report, you will receive a new copy of your report. If the account is not removed, you will receive an explanation of the results and the reason the account was not removed.

Why the Debt Collector May Not Verify the Debt

Now that we have talked about how to dispute a debt and the steps involved in the dispute process, let’s talk about something that is very important to your success: why the debt collector may not verify the debt.

Debt collection is big business. There are thousands of debt collectors in the U.S. that collect billions of dollars from consumers every year. Most debt collectors don’t have the staff or resources to verify every debt they collect, so sometimes, they just ignore disputes or don’t respond at all.

When a debt collector doesn’t respond to a dispute, you win. The account must be removed from your report. Here are some other reasons why a debt collector may not verify a debt:

They lost the documentation. Sometimes, debt collectors don’t have access to the documentation for the original debt, so they can’t verify it.

The debt is past the statute of limitations. Sometimes, debts are past the statute of limitations and can’t be collected.

The debt was paid. Sometimes, debts were paid, but the consumer was never notified.

The Importance of Patience

What to Expect from the Credit Repair Process

Chances are, you want to repair your credit as fast as you can. There are a lot of companies out there that promise fast credit repair, but the truth is, credit repair is not fast. In fact, it can take several months to a year or longer to repair your credit, depending on how bad your credit is. So why is credit repair so slow? There are several reasons why credit repair is slow. Here are a few:

Credit repair involves disputing information on your credit report. This can take some time because you have to write letters to the credit reporting agency and wait for a response. Sometimes, you have to send multiple letters before the information is corrected.

Credit repair involves the credit reporting agency. The credit reporting agency has to investigate disputes and respond to consumers, but sometimes, they are slow to respond. In fact, the credit reporting agency has 30 days to investigate a dispute, but sometimes, it takes longer.

Credit repair involves debt collectors. Debt collectors have to verify debts when consumers dispute them, but sometimes, they don’t respond at all. When a debt collector doesn’t respond to a dispute, you win and the account is removed from your report.

The key to fast credit repair is patience. You have to be willing to wait for responses from the credit reporting agency and debt collectors. Sometimes, this can take several months, but the end result is worth it. A good credit score can help you qualify for credit and lower interest rates, so don’t rush the process. Instead, focus on doing things right and making sure that your credit report is accurate.

Don’t try to rush the process by sending unnecessary letters or making threats. This will only delay the process and make things worse.

The Benefits of Working with a Credit Repair Company

What You Can Expect from a Credit Repair Company

So far, we have talked about how to repair your credit and things you can do to make the process faster, but there is one more thing we need to talk about: the benefits of working with a credit repair company. A credit repair company can make the process easier and faster. Here are some benefits of working with a credit repair company:

Credit repair companies know the law. Credit repair companies understand the FDCPA and FCRA and how to use them to your advantage. They can help you dispute information on your credit report and deal with debt collectors.

Credit repair companies save time. Disputing information on your credit report and dealing with debt collectors can be time consuming. A credit repair company can save you time and make the process easier.

Credit repair companies have experience. Most consumers don’t understand the credit repair process and may not know where to start. A credit repair company has experience and can help you navigate the process.

Working with a credit repair company may be a good option for you. They can help you understand the credit repair process and make things easier. They can also help you save time and navigate the process.

When to Contact a Credit Repair Company

Are you thinking about contacting a credit repair company? You should. A credit repair company can help you navigate the process and make things easier. Here are some reasons why you should contact a credit repair company:

You don’t understand the process. If you don’t understand the credit repair process, you should contact a credit repair company. They can help you understand the process and make things easier.

You don’t have time. Disputing information on your credit report and dealing with debt collectors can be time consuming. If you don’t have time, you should contact a credit repair company. They can save you time and make the process easier.

You need experience. If you need experience, you should contact a credit repair company. They have experience navigating the credit repair process and can help you.

Summary

Nathan & Nathan is a debt collection law firm that represents several large creditors including Capital One, Discover Bank and NCSLT. If you have received a collection letter from this firm, you should remain calm and take time to think about the situation.

The FDCPA gives you the right to request verification of a debt any time a debt collector contacts you. If the debt collector cannot verify the debt, you don’t have to pay it. The FCRA also gives you the right to dispute information on your credit report. When you dispute information, the credit reporting agency has to investigate and verify the information. If they can’t verify it, they have to remove it from your report.

Don’t pay a debt collector without verifying the debt first. Paying a debt will not remove the account from your credit report and you may not owe the debt.

The credit dispute process is the process of disputing information on your credit report. The process involves writing a dispute letter and sending it to the credit reporting agency where the disputed account is reported. The credit reporting agency has 30 days to investigate the disputed account. During the investigation, they will contact the creditor and ask for verification of the debt. If the creditor cannot verify the debt, the account must be removed from your report.

Patience is the key to fast credit repair. You have to be willing to wait for responses from the credit reporting agency and debt collectors. A credit repair company can make the process easier and faster. They know the law and can help you dispute information on your credit report and deal with debt collectors. They can also save you time and have experience navigating the credit repair process.

Contact us today to see how we can help you!

Are you dealing with a collection agency and need help? Call our experienced team at FightCollections.com. We can help you remove negative information from your credit report, stop harassing collection calls, lower your debt and save money, and improve your credit score