There are a few things worse than discovering a collection account on your credit report.

You’ve likely found the collection account by Rent Recovery Solutions on your report for one reason, you noticed that your score had dropped or you were denied credit. The next thing you know is that you’re getting letters and calls from a debt collector like Rent Recovery Solutions that you’ve never heard of before.

What is Rent Recovery Solutions?

According to its website, Rent Recovery Solutions, LLC is a debt collection agency that focuses on collecting debts from apartment renters.

The company was started by Saul Wertzer and has an office in Atlanta, Georgia, as well as another location in Montrose, Colorado. Rent Recovery Solutions is licensed in multiple states including North Carolina, Tennessee, Wisconsin, New York City, Colorado, and Connecticut.

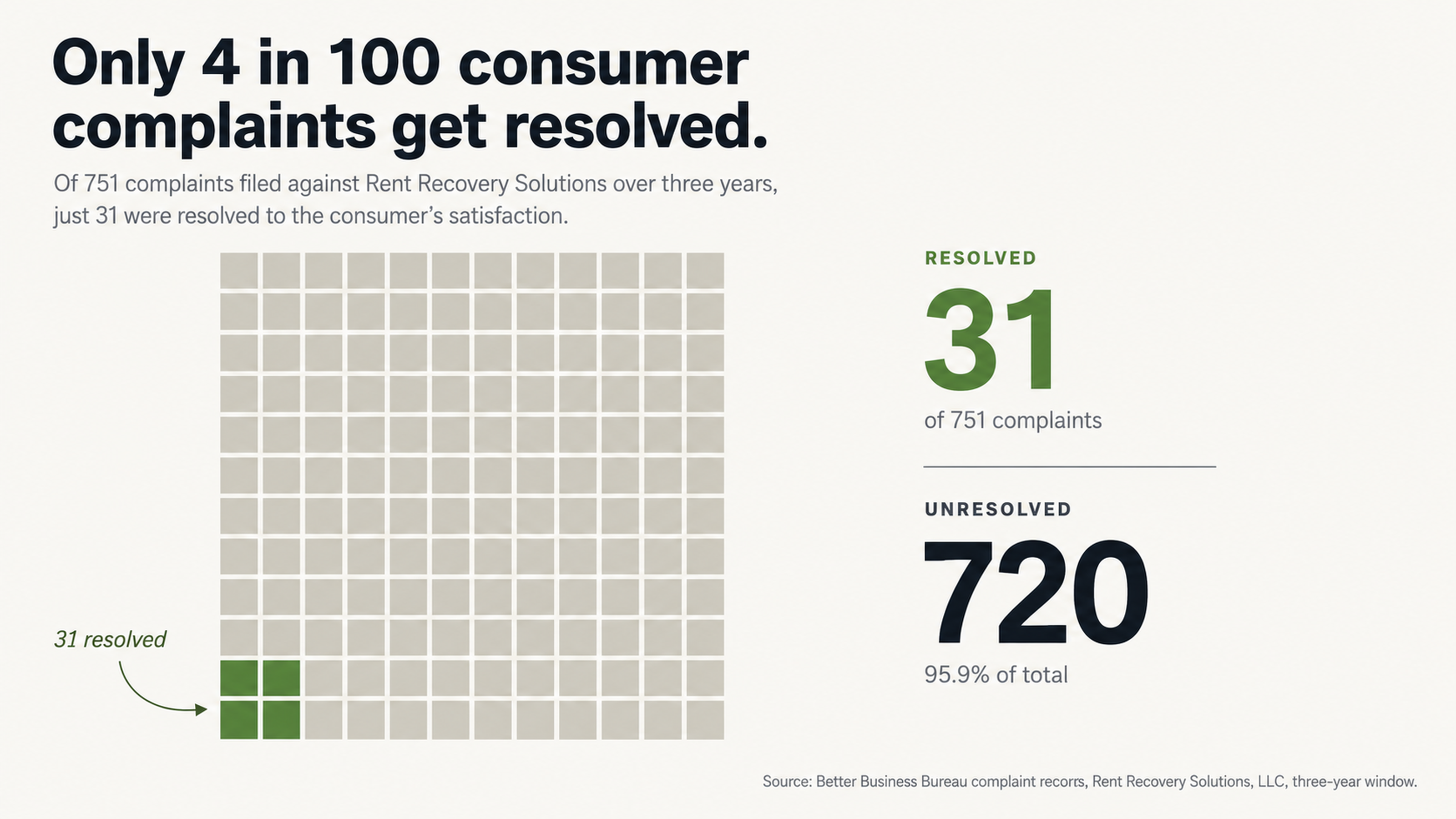

What does the BBB say about Rent Recovery Solutions?

The Better Business Bureau rates Rent Recovery Solutions with a failing F grade. They received 751 complaints in the last 3 years and 193 complaints in the last year. Only 31 of those 751 complaints were resolved to the satisfaction of the consumer. That is a paltry 4.1%. Analysis of complaints reveals approximately half involve debts consumers assert they do not owe.

The BBB reviews speak for themselves. Rent Recovery Solutions has an F rating for a reason.

One of the reviews on the site stated the following:

“They are trying to collect a debt I do not owe. They have placed an item on my credit report without even attempting to contact me by phone or mail to verify if I am the correct party. I have had to have other companies place items on my credit report in the past, and they ALWAYS attempt to contact me first. This company is predatory and does not follow standard business practices. They need to be held accountable for their actions.”

Rent Recovery Solutions was penalized by the Connecticut Department of Banking. According to their report, the penalty was for, “engaging in the activities of a consumer collection agency without obtaining the required license in Connecticut, in violation of Section 36a-801(a) of the Connecticut General Statutes.”

In federal court records, Rent Recovery Solutions has been sued over 140 times. Nearly all of those lawsuits involved violations of the Fair Debt Collection Practices Act. Most of the claims involved failure to validate the debt, misrepresentation, and improper reporting to the credit bureaus. The Beckler v. Rent Recovery Solutions case illustrates this dynamic, ultimately settling for $2,000 plus $9,480 in attorney fees.

How do you beat Rent Recovery Solutions?

Before we discuss what you can do about Rent Recovery Solutions, you first need to know that you are not alone. It can be embarrassing to have a collection on your report, but it is more common than you think. According to research conducted by U.S. PIRGs, 79 percent of credit reports contain mistakes or serious errors. The Fair Debt Collection Practices Act protects you from debt collection harassment and abuse.

Even if you do owe the debt, there is nothing that says you have to tolerate abusive behavior from a debt collector. If the collection is inaccurate or you are not sure if you owe the debt, you have the right to dispute it and have the debt verified.

Why you shouldn’t pay Rent Recovery Solutions.

You may be tempted to just pay the debt and be done with it. While we understand that you may just want to get rid of it, it is not always the best course of action. First, paying the debt is not a guarantee that it will be removed from your credit report. Paying the debt will not help your credit score, and could potentially hurt it.

We recommend that you don’t pay until you have verified that the debt is yours and the information is accurate. Next, we recommend sending a debt validation letter. This letter will request that the debt collector provide proof that you owe the debt and that they have the right to collect it.

Debt validation is governed by federal law, and you have the right to request validation from any debt collector. In this case, you may want to request proof of the original lease agreement as well as any documentation that proves you owe the debt. Once you have requested debt validation, the debt collector cannot legally pursue collection activities until the debt is validated.

At this point, you have several options. If the debt collector cannot validate the debt, they must remove it from your credit report. You can then request a follow-up credit report to ensure the item has been removed. If they can validate the debt and it is accurate, you can either pay the debt, attempt to negotiate a pay for delete, or potentially settle the account.

Turning the Tables on the Collector

Instead of playing the role of defendant in a court case you didn’t sign up for, why not turn the tables on the collector? The Federal law has mechanisms in place that allow you to make the collection agency prove its claim.

Understanding the Dispute Process

When you dispute a collection, the responsibility falls entirely on the other party. The collector must verify that the debt is real, that the amount is correct, and that you’re the correct party responsible for the debt. And it has to do so within a specific time frame. If the collector can’t verify the debt, it has to be deleted from your report.

One of the reasons the dispute process works is because the collection agency often doesn’t have the necessary documents. The very fact that the dispute process works so well is proof that collection agencies can’t verify debts when challenged. And Rent Recovery Solutions likely faces the same challenges. With only 4.1 percent of complaints being resolved, it seems that the company doesn’t always provide an adequate response when consumers file complaints.

The Fair Credit Reporting Act says that credit bureaus have to investigate items that are disputed, and remove any information that can’t be verified. The Fair Debt Collection Practices Act says that collectors have to verify a debt when requested. These two laws together make it so that the onus is on the entity claiming you owe money, not on you to prove that you don’t.

What the Federal Courts Have Already Decided

There have been over 140 federal cases brought against Rent Recovery Services. So there is already precedent for the types of behaviors this company is accused of. The majority of cases brought against the company involve violations of the FDCPA, including failure to validate a debt, misrepresentation, and illegally reporting a disputed debt to a credit bureau.

Given the sheer number of cases, these actions don’t seem like isolated incidents.

In fact, a court case brought in the Eighth Circuit Court of Appeals in 2023 found that the company violated federal law when it reported debts to a credit bureau without verifying them and without noting that they were disputed. These aren’t hypothetical violations — they’re a pattern that has resulted in settlements and judgments against the company.

And that matters for your case because it means there is already legal precedent for the type of violations that may have occurred. If a company has already been penalized for violating the law in a specific way, it seems more likely that it may have done so in your case as well.

Common Tactics and How to Combat Them

Educating yourself about how collection agencies operate is key to recognizing and resisting the tactics they use to apply pressure. These tactics are designed to get you to pay as quickly as possible before you have a chance to research your options.

Creating a Sense of Urgency

One of the main ways collection agencies operate is by creating a sense of urgency. They want you to believe that you need to act immediately or the situation will get worse. They want you to believe that you have no choice but to pay or you’ll face dire consequences.

But this urgency almost always works in their favor, not yours. Every day you go without disputing the charge is another day they have to pressure you into paying.

Creating Fear

The flip side of urgency is fear. The agency wants to scare you into paying by telling you all the things that could happen if you don’t. It may threaten your credit score, a court judgment, or worse.

But before you get too scared, remember that the company is in the business of collecting debts. It makes money every time it successfully gets a consumer to pay. So it has every reason in the world to scare you into paying.

In fact, if you look at Rent Recovery Services’ track record, it’s possible that the fear it is inspiring is out of proportion with the actual risk. The company is aggressive in collecting debts, but when consumers push back, it seems that it isn’t always able to verify those debts.

If you understand that the agency is using fear as a tactic, you can take a step back and breathe. There’s no need to panic simply because you have a collection on your report. You have time to decide how you want to proceed.

The Power of Remaining Silent

Sometimes, the most powerful thing you can do in this situation is to remain silent. You don’t have to talk to a collector on the phone. In fact, it’s rarely in your best interest to do so. You have the right to dispute the debt in writing, without ever speaking to the collection agency.

In fact, every time you talk to a debt collector on the phone, you give it the opportunity to pressure you into paying. You give it the opportunity to extract information from you that it can use later. And you give it the opportunity to get you to say something that can make it harder to dispute the charge later.

If you’re working with a professional credit repair agency, it understands exactly what to say and what not to say. And it understands how to apply the maximum amount of pressure on the collection agency to either verify the debt or delete it. Sometimes, simply having professional representation makes the difference between a charge that the credit bureau deletes and one that it leaves on your report.

Bottom Line

If Rent Recovery Services has placed a collection account on your report, that doesn’t mean you actually owe money. In fact, it could mean the opposite — the company is accusing you of owing money, and it’s up to it to prove that you do.

You didn’t create a system where 79 percent of credit reports contain some level of error. And you didn’t create an industry where debts are bought and sold so many times that documentation is lost. But you can take advantage of the laws designed to protect consumers operating within those systems.

So instead of asking if you can afford to dispute the collection account, the better question is can you afford not to?

Get Help Today

At FightCollections.com, we understand how to put the burden of proof where it belongs — on the collection agency. We understand the dispute process and the types of documentation that collection agencies typically lack. And we understand the intricacies of the various federal laws designed to protect consumers.

So if Rent Recovery Services has placed a collection account on your report, we can help. Contact us today for a free consultation to learn more about how the dispute process works. Don’t let a collection agency push you around. Make it prove its case.