If you see General Revenue Corporation on your credit report, you likely felt a surge of panic. The name of the company sounds very official and even somewhat governmental.

This is likely by design. The company has been collecting debt for over 40 years, specifically on student loans and government debt. If you see them on your report, you need to pay close attention.

First, relax. The urgency you feel right now is what collection agencies rely on to get people to pay debts that they have not verified as valid or accurate. The feeling that you owe a debt is leverage. Knowing this fact changes everything.

According to U.S. PIRGs, 79% of credit reports contain errors or inaccuracies. This fact alone should tell you not to accept any collection account on its face. The listing from General Revenue Corporation could be riddled with errors, and if you dispute those errors, you may get it removed.

Who is General Revenue Corporation?

General Revenue Corporation is a debt collection agency that is headquartered in Mason, Ohio.

A Troubling History

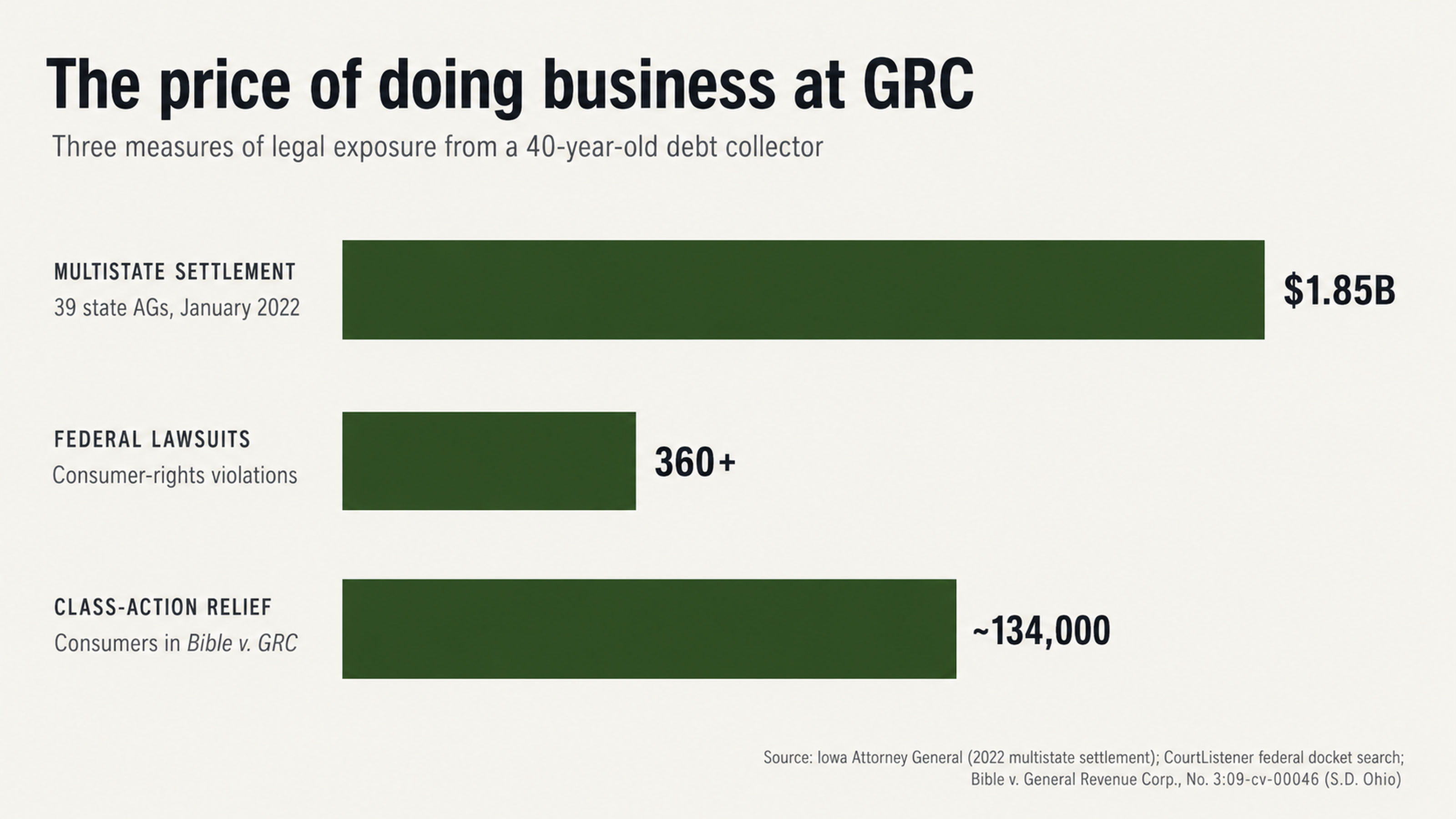

GRC was previously a wholly-owned subsidiary of Navient Corporation. However, in June of 2019, the company was acquired by SinglePoint Group International. The reason this matters is that General Revenue Corporation was named as a defendant in a massive $1.85 billion multi-state settlement that was announced in January 2022.

The settlement was entered into by 39 state attorneys general. The lawsuit named several violations, including:

- Misrepresenting the credit benefits of rehabilitating defaulted loans

- Misrepresenting information about collection fees

- Misrepresenting to borrowers that they needed a permanent inability to work to qualify for a disability loan forgiveness, when, in fact, they did not.

Court records also show that more than 360 federal lawsuits have been filed against General Revenue Corporation for violating consumer rights. Despite this, the company enjoys an A+ rating from the Better Business Bureau. However, the consumer reviews of the company average just 1 out of 5 stars. This discrepancy between the rating and the review is concerning.

Red Flags

There are some specific red flags you should look for when it comes to the General Revenue Corporation listing on your report.

The first red flag is incorrect dates.

When you pull your report and look at the listing from GRC, look at the date of first delinquency. This is the date when the statute of limitations starts for how long the account can remain on your report. If the date is incorrect, or if the account is older than 7 years from the date of first delinquency, you may have a problem.

Another red flag is the open date on the collection suddenly resets, making an old debt appear new. This is illegal. Debt collectors cannot reopen the clock on an account by opening a new collection account on debt that has a statute of limitations or has already aged off.

Finally, check the dates on your report against any documentation you have from the original creditor. If there is a discrepancy between what your student loan servicer reported and what GRC is reporting, you have a problem.

Incorrect account details

The balance may not be what you think it is.

In 2021, an Alabama class-action lawsuit claimed that GRC would determine the amount of collection fees by taking the balance and multiplying it by 25% and then demanding that amount from the consumer without making it clear that the amount was an estimate and not actual costs. In the lawsuit, the plaintiff claimed that the balance on their student loan was $2,450, but GRC added fees that brought the balance to $3,062.50.

If you do not recognize the original creditor, account number, or balance amount, these are all red flags. Debt gets sold and resold, and the information can get lost or distorted along the way. It may be that the account that GRC is claiming is yours was misassigned.

Student loan accounts can be particularly problematic because the servicer may change, and the loans may be consolidated or the school may have closed. All of these things can cause errors with your credit.

Why You Should Never Pay a Collection First

The problem with paying a collection

Many people assume that if they pay a collection account, it will be removed from their credit report, and their credit score will improve. This is not accurate. If you pay a collection, the account will show as paid, but it will remain on your report for 7 years from the original date of delinquency.

A paid collection will still tell any future lender that you had a debt go to collection. Many newer credit scoring models, like FICO 9 and VantageScore 3.0 do not count paid collections against you, but many lenders still use the older models that do.

Paying a collection can cause significant stress for consumers who see this account on their report, and collectors know this. They use this stress to their advantage and try to get you to pay the debt as quickly as possible. If you take the time to verify the debt and review your options, you are far less likely to make a decision that you will later regret.

What happens when you dispute a debt

If you dispute a collection account, the credit reporting agency must investigate the account within 30 days. They will contact the collector and ask for verification of the debt. If the collector cannot provide documentation that proves the debt is yours, is accurate, and not outside of the statute of limitations, the agency must remove the listing from your report.

Debt collectors purchase accounts by the tens of thousands, often with little or no documentation. They may not have the original loan agreement, payment history, or other records that prove their claim. This lack of documentation is one of the primary reasons consumers have the leverage they do.

Federal courts have found GRC to have violated the Fair Debt Collection Practices Act on multiple occasions. In July 2015, a federal judge in New Jersey ruled that the language that GRC used in their standard collection letters was misleading and false under the FDCPA. If they have violated your rights, you may have grounds to have the account removed.

Don't Get Caught in the Phone Call Trap

Why you should not talk on the phone

One consumer complaint to the BBB claimed that GRC called every single living relative of theirs in one afternoon and left messages stating that the consumer was in trouble. Another consumer claimed that GRC called their workplace 8 times in 3 days, including 4 times in 4 hours on one afternoon, despite the consumer's written request to stop calling their workplace.

While these phone calls are certainly harassing and possibly illegal, there is another reason you should not engage in phone calls with debt collectors. Phone calls do not create a record of the conversation. This means that the collector may misrepresent what you have said or misinterpret what you meant. Any agreement you come to over the phone may not be honored later.

Finally, anything you say on the phone can be used against you. You may inadvertently acknowledge a debt you do not owe or reset the clock on the statute of limitations.

The problem with documented communication

While phone calls do not create a record, written communication does. If you communicate with debt collectors only through certified letters with return receipts, you will have proof of every single contact you have with the collector. You will have proof of every letter you send and every response you receive. You will even have proof if the collector fails to respond.

Silence can be your friend in a debt collection. You are under no obligation to answer phone calls, respond to messages, or communicate with collectors at all. In fact, the law allows you to request that the collector send you debt validation in writing, and until they provide it, they cannot continue to collect.

If you have professional credit repair help, the dynamic changes entirely. When the collector knows a consumer has representation, the collector knows that their typical tactics will not work. Instead, the communication will shift to the documentation and the legally mandated procedure.

Knowing Your Rights

FDCPA

The Fair Debt Collection Practices Act is a law that Congress passed because debt collectors were engaging in abusive practices. The law prohibits harassment, misleading and false statements, and other unfair practices. The law says that collectors must provide debt validation if consumers request it and that they must cease communication if the consumer requests it in writing.

General Revenue Corporation has been the subject of a US Supreme Court case involving the FDCPA.

In Marx v. General Revenue Corporation, the consumer alleged that GRC had engaged in harassing conduct, including calling multiple times a day, and had made false threats about garnishing wages. While the court did not rule on the underlying allegations, the fact that GRC was accused of this conduct is telling.

You have the right to request validation of any debt within 30 days of the initial contact. You have the right to dispute any information on your credit report that you believe is inaccurate. You even have the right to sue a collector if they violate your FDCPA rights and potentially be awarded statutory damages.

FCRA

The Fair Credit Reporting Act requires that any information contained in your credit report must be accurate. If you dispute information, the agency must investigate and remove information that cannot be verified. This verification is the primary mechanism that consumers have to correct potentially inaccurate collection accounts.

Credit reporting agencies have 30 days to conduct an investigation, and up to 45 days if you provide additional information during the investigation. If the collector cannot or does not respond, or if they cannot verify the debt, the agency must delete the information. If the agency fails to follow these procedures, they may face legal liability.

In the class-action lawsuit Bible v. General Revenue Corporation, the court ultimately settled the case, providing relief to approximately 134,000 consumers who received collection letters that contained allegedly inaccurate information about the timeframe they had to request a review of their debt. This case is a great example of how systemic problems can affect a huge number of consumers.

What You Can Do

Gather documentation

The first thing you should do is pull your credit report from all three bureaus at AnnualCreditReport.com. Compare the General Revenue Corporation listing on all three reports. If there is any discrepancy between the bureaus, that is a major red flag.

Gather any documentation you have related to the original debt. This may include records of your student loan, payment confirmations, any communication you have received from the school or servicer, or any prior collection notices. If you are missing documentation or if the documentation conflicts, that is a good thing.

Make a note of anything that appears to be wrong, or that you do not recognize or find suspicious. This may include the balance, creditor name, account number, dates, or status codes. Each inaccuracy is a separate basis for disputing the debt.

Why you need professional help

If you try to dispute debts on your own, you are up against a company that does this for a living. General Revenue Corporation services over 9 million accounts per year. They have a system, process, and staff to handle collection. You, as an individual consumer, are at a disadvantage.

A credit repair professional knows the specific language and procedure to use to get results. They know which errors are the most critical, how to word disputes for the best effect, and what documentation to request. They can spot violations that you may miss.

Having professional representation also means that collectors will take you more seriously. Once they know you have an advocate who understands your rights and can enforce them, they are more likely to want to resolve the matter in your favor.

Conclusion

General Revenue Corporation has been around for over 40 years and has a long history that includes a $1.85 billion multistate settlement, over 360 federal lawsuits, and multiple class-action lawsuits that affect hundreds of thousands of consumers. If you see them on your report, you need to pay close attention.

The urgency you are feeling right now is manufactured. Collectors want you to feel stressed so that you will pay them as quickly as possible. If you take the time to verify the accuracy of the listing and understand your rights and options, you are much less likely to do something you will regret later.

Remember, credit reporting agencies must remove items that cannot be verified. The burden of proof is on the collector, not you. Errors in debt collection happen all the time, and those errors can be the basis for getting accounts removed.

What's Next?

Do not let General Revenue Corporation remain on your credit report without challenging them. The dispute process is in place to protect consumers from inaccurate reporting, and professional help can make all the difference.

Contact FightCollections.com today for a free consultation. Our staff specializes in spotting errors, filing effective disputes, and advocating for consumers when they are facing collection accounts. Let us review your case and help you determine the best course of action for the General Revenue Corporation listing on your credit report.

Your credit matters. Do not hesitate to take action to protect it.