Receivables Management Partners, LLC goes by several different names that you might see on your credit report.

In addition to RMP LLC, they use the trade names RMP Services, Collection Associates, and MMS Collections Company. They are all the same company.

The Big Picture: Who Is RMP LLC?

If you’re finding RMP on your credit report, it’s important to understand who you’re dealing with. This is a company that has been on the receiving end of a lot of consumer pushback, and you can learn a lot from their regulatory history that many people don’t find out until they’ve made a costly mistake.

Over the last decade, the CFPB Database has logged over 1,200 complaints against RMP. 171 new complaints were added in the last year alone. The BBB reported 254 complaints against the company in just three years, with 80 of those complaints coming in the last 12 months.

There are over 50 federal lawsuits on the books naming RMP as the defendant, most of which were related to alleged FDCPA violations.

One class-action lawsuit against RMP (Rhoads v. RMP LLC) claims the company sent collection letters that included two different balances: an “Amount Due Today” and an “Original Balance.” The two figures didn’t always match, and consumers weren’t sure which one to pay.

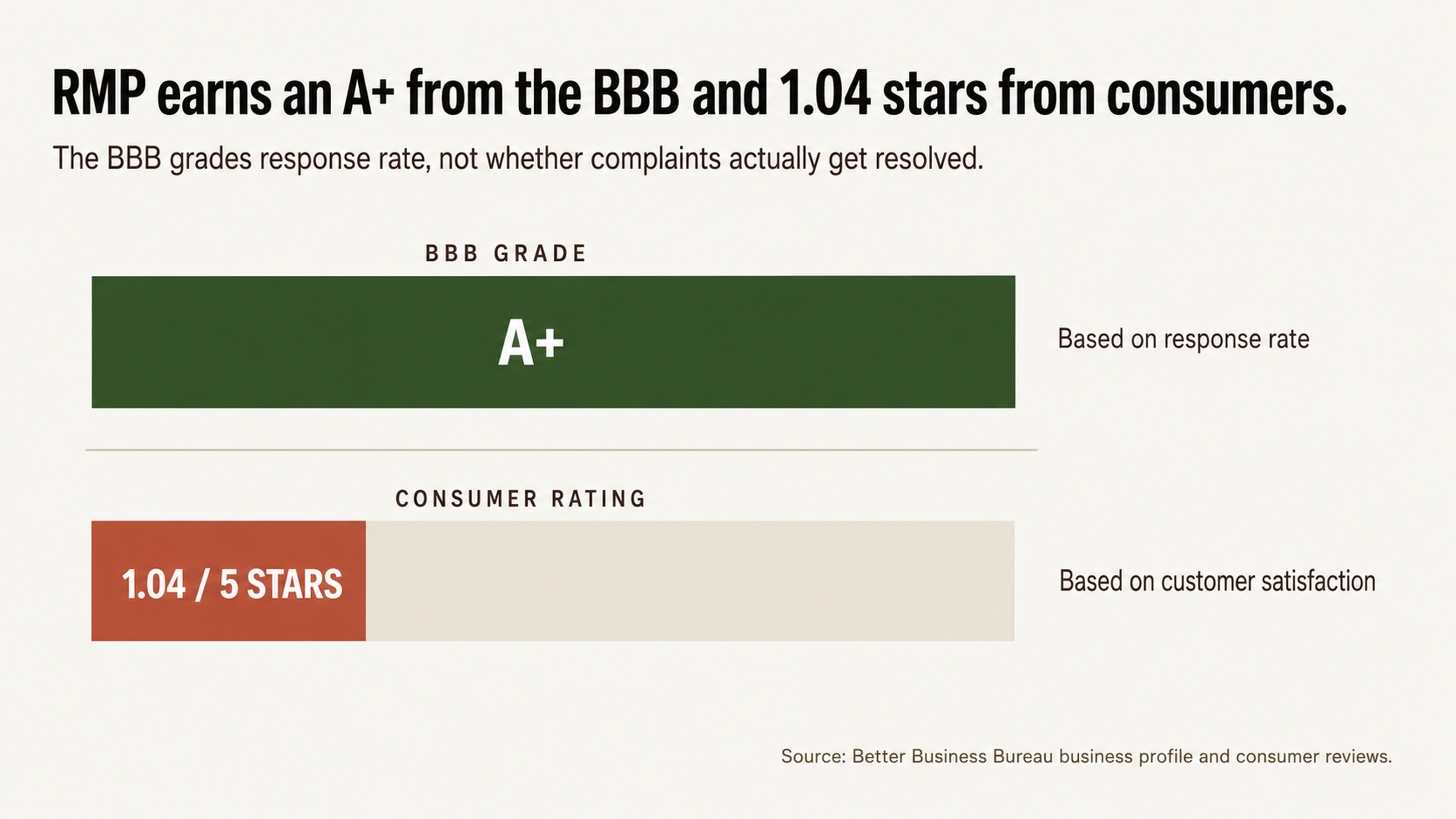

One of the most interesting things about RMP is the disconnect between their official ratings and their consumer review scores. While the company enjoys an A+ rating from the Better Business Bureau, their consumer review score is a dismal 1.04 – 1.4 stars out of 5.

This discrepancy is due to the fact that the BBB grades companies based on their complaint responses, not their customer satisfaction ratings. RMP responds to complaints regularly, but it appears their responses don’t usually resolve the underlying issue in a way that makes consumers happy.

Why You Should Not Pay a Collection Without Disputing It First

If you pay a collection, the status will be updated to paid, but the item will still remain on your report for the full seven years. This is a distinction without a difference for most consumers. If you pay the collection, the item is still hurting your credit score. If you don’t pay the collection, it’s still hurting your credit score. Why would you pay it?

This is why the collection industry makes so much money. They know that if they can trick you into paying right away, they’ll get your money before you realize that it’s not going to improve your credit score.

It’s why every collection caller tries to scare you into paying right now. It’s why they say things like, “If you don’t pay $200 today, we’ll have no choice but to sue you for $500!” (And yes, a collection caller actually told a consumer that, according to a complaint logged with the CFPB.)

In most cases, the caller doesn’t intend to sue you, and they’re just trying to scare you into making a payment. It’s also why they call you over and over again, trying to wear you down until you agree to pay something.

U.S. PIRG did a study and found that 79 percent of credit reports contain errors or disputable items. 79 percent! If you pay a collection before disputing it, you’re assuming that the information is probably accurate, and you’re giving up your best chance to remove it from your report.

If there’s even a chance that almost 8 out of 10 credit reports contain errors, don’t you want to at least verify the information before you pay?

What is a Collection Account and How Long Does it Stay on My Report?

A collection account is a negative item on your report that shows when one of your debts has been sent to a third party for collection. It will stay on your report for seven years from the original delinquency date.

This means that if you had a medical bill that you didn’t pay in 2015, and it was sent to collections in 2016, you’ll have a collection account on your report until 2023. Paying the collection does not change the end date. Having the debt sold to another collector does not change the end date.

The end date is determined by the date that the original delinquency occurred, and nothing that RMP LLC or any other collection agency tells you can change that fact.

Many collection agents will try to tell you that you should pay the collection because it will be removed from your report. Or they’ll say that you should pay it because it will be “paid” instead of remaining open. None of this is true.

Paying a collection account does not improve your credit score. Having a paid collection on your report instead of an unpaid collection makes very little difference, if any.

You should only pay a collection if you’ve verified that it’s yours, you’re sure that it’s accurate, and you’ve determined that it’s better for your credit score to pay it than to dispute it and try to have it removed. But in many cases, disputing the collection and trying to have it deleted is the better option for consumers.

What RMP Does Not Want You to Know

This Is Not a Moral Obligation – It’s a Business Deal

When a collection agency like RMP purchases debt from another company, it means they now own the right to collect it. But most of the time, they didn’t purchase the debt directly from the original creditor.

Instead, they bought it from another debt collector who may have bought it from yet another debt collector. Each time debt is bought and sold, it becomes more and more of a commodity.

This is not a situation where you borrowed money from someone who needs it back. This is a business deal where someone is trying to make money by collecting a debt. The original creditor charged the debt off years ago. You no longer have a relationship with that company, and in most cases, you never will again. This is strictly business.

When debt is sold and resold, the documentation and details of the account can get lost in the shuffle. Often, the debt is sold without a contract or other documentation showing that the consumer ever incurred the debt. Balances can be inflated when fees and interest are tacked on during the collection process. The balance that RMP says you owe may not be the balance that you actually owe.

Communication Issues Can Be a Red Flag

If you have a complaint about how RMP communicated with you, you’re not alone. The company has been accused of everything from calling incessantly to not leaving messages or sending statements in the mail.

One consumer even logged a complaint with the BBB because RMP was only communicating with her via text message instead of sending her a written validation notice as required by law.

It’s worth noting that if you’re dealing with a medical debt issue and you’re only getting text messages, there may be a HIPAA violation in addition to an FDCPA violation. If you’re getting sensitive health information via text message, it’s not a secure communication, and it may not comply with federal privacy laws.

Badges of Dishonor – Understanding RMP’s Ratings and Reviews

RMP is a company with nine offices spread across the country (including offices in Indiana, Illinois, Michigan, Texas, Pennsylvania, and North Carolina). They have a website and a customer service team. They seem like a normal, functioning business.

The problem is that their customer service team seems primarily designed to get money from consumers without adequately addressing their questions and concerns.

RMP has an A+ rating from the Better Business Bureau, but their consumer rating is a dismal 1.04 stars out of 5. The discrepancy is due to the fact that the BBB evaluates the responsiveness of the company rather than the quality of their responses.

As long as RMP answers every complaint they receive, they’ll continue to have a high rating from the BBB, even if they’re not actually resolving the underlying issues to the consumers’ satisfaction.

How to Beat RMP – Silence is Golden

If you’re getting phone calls from a collection agency, the best thing you can do is ignore them. Don’t answer the phone, and don’t call them back.

This isn’t about avoiding the problem because you’re afraid. This is about refusing to engage with someone who has a tremendous amount of leverage over you.

If you talk to a collection agent on the phone, you may inadvertently give them information they can use against you. You may admit that you owe a debt or agree to a payment plan without realizing the implications. The agent may lie to you or mislead you, and you won’t even realize it.

The best thing you can do is hang up the phone and ignore them until you have all the information. Don’t make a payment over the phone, either. Once you’ve given them your payment information, they can charge you for whatever they want, and you may not be able to get your money back.

What You Can Learn from Your Free Annual Credit Report

The federal government mandates that every consumer is entitled to one free credit report from each of the three major credit reporting bureaus every year. Most people treat this as a consumer benefit that they need to monitor every 12 months or so.

But if you have a collection on your report, your free annual credit report is actually a vital tool you can use to gather intelligence and figure out the best way to approach the situation.

When you pull your reports, make note of every detail about the collection account: the balance, the date of the original delinquency, the name of the original creditor, etc. If there are any discrepancies between your reports – for example, if the balance is different depending on which credit bureau is reporting it – make a note of that as well.

Inconsistencies between the three major credit bureaus can be an indication of a reporting error that you may be able to dispute.

RMP reports to the credit bureaus under a variety of names, including: Receivables Management Partners LLC, RMP Services, and RMP LLC. The collection may appear slightly differently on each report, depending on which trade name was used, so make sure you review each one carefully.

A Step-by-Step Guide to Disputing a Collection Account

You should dispute any collection account on your report that contains incorrect, erroneous, fraudulent, or unverifiable information. It’s your right under the Fair Credit Reporting Act (FCRA), a federal law that outlines consumers’ rights as they relate to their credit information.

If you initiate a dispute for one of these reasons, the credit reporting bureau is required to investigate and respond within 30 days. They will reach out to the collection agency and request that they verify the debt. If the collection agency cannot verify the debt within the allotted timeframe, the item must be removed from your report.

Many consumers don’t realize that this is an option, and collection agencies count on that. They know that if they can get you to pay without disputing it first, you’ll never even know if it’s possible to have the item removed.

In fact, many agencies will tell you that you can’t dispute a collection account if you’ve already paid it, which is not true. If the collection is invalid or unverifiable, you can still dispute it even if you’ve paid it.

Why You Should Use a Credit Repair Company to Dispute RMP

The collection industry is big business, and the players involved know how to protect their interests. RMP has 520 employees spread across nine offices nationwide, an in-house legal team that understands their FDCPA obligations, and a system in place that is designed to result in them getting as much money as possible, as efficiently as possible.

But you’re just one person, and you probably don’t have the time, expertise, or experience to go up against a professional debt collector. If you try to dispute RMP on your own, you’re essentially fighting with one hand tied behind your back.

You’re going up against a company with vast resources and a team of professionals who do nothing but collect debt all day, every day. And they’re not afraid to lie to you or mislead you in order to get what they want.

Credit repair companies specialize in disputing collection accounts and other negative items on behalf of consumers. They understand what documentation is required to verify a debt, what types of inconsistencies can help you successfully dispute an item, and how to communicate with collection agencies and credit reporting bureaus in a way that gets results.

If you’re trying to navigate the system on your own, you’re already at a disadvantage. The collection agencies know the rules much better than you do, and they have a lot more experience. They do this every day. You do not.

There’s also another benefit to working with a credit repair company: you’ll have a paper trail that shows you made a good-faith effort to dispute the information. If RMP continues to report the account after you’ve disputed it, you may have grounds for a claim under the FCRA or FDCPA, and your documentation will be essential in building your case.

Documented Consumer Complaints Against RMP

Inconsistent Debt Validation

Many consumers have reported that RMP failed to validate their debts when they requested it.

One consumer even logged a complaint with the CFPB because after they notified RMP that someone was using their identity to incur debt in their name, the company failed to provide a signed agreement, an itemized bill, admission records, medical charge records, and records showing that the consumer had received the services billed.

If the consumer is a victim of identity theft, RMP should have taken steps to verify the information before placing it on their credit report. But apparently, they didn’t, and instead the consumer was left to deal with the fallout.

Another consumer reported a similar issue to the BBB, saying that the company placed several medical collections on their credit report even though they had insurance that covered them for every date of service. The consumer said they were in the process of closing on a mortgage and stood to lose more than $50,000 if the accounts weren’t removed promptly.

In both cases, RMP appears to have failed in their obligation to verify the debts before reporting them on the consumers’ credit reports. This seems to be a pattern with the company.

Debt Balance Inflation

RMP has been accused of inflating debt balances in their collection practices. One consumer logged a complaint with the CFPB because RMP increased the balance on one of their debts by more than 70 percent.

The current balance RMP is attempting to collect is $3,147.51. The consumer’s original bill from the original creditor was $1,836.51. The consumer intends to contest the additional amount RMP has added to their bill.

The consumer’s position is clear: they don’t feel they owe the additional money that RMP is trying to collect, and they’re going to challenge it. And they should! If RMP can’t validate the debt at the balance they’re trying to collect, they shouldn’t be allowed to report it that way.

What to Do When RMP LLC is On Your Credit Report

RMP LLC is a real collection agency with legitimate licensure and nearly four decades in business. But that doesn’t mean they’re accurate, and it doesn’t mean you should pay them before verifying the information.

With 1,200 complaints at the CFPB and 50 federal lawsuits under their belt – not to mention an average consumer rating of just 1.04 stars – it’s clear that RMP LLC is a company to approach with caution.

If you have an account with RMP LLC on your credit report, do not call them and offer to pay. Do not respond to their text messages and voicemails. Don’t let them pressure you into doing something that isn’t in your best interests.

Instead, order your credit reports, pull out your highlighter, and get to work. Look for every account associated with RMP LLC, and make note of all the information. Then pick up the phone and call a credit repair expert who can help you dispute the account and remove the associated negative mark from your credit report.

The collection industry survives on consumers not knowing their rights. They make their money on consumers not understanding the dispute process and not recognizing when a collection agency has overstepped their bounds.

Don’t give them your money. Instead, educate yourself, verify your information, and exercise your right to a dispute. The sooner you start, the sooner you can get on with your life.