When you discover a mysterious debt collection on your credit report, your first reaction is concern.

That concern turns to alarm when you discover that the negative listing is from Frontline Asset Strategies and could remain on your report for years. Before you call the company or send in a check, know that in their initial response, most people make avoidable errors that cost them negotiating power they can never regain.

The business model for third-party debt collectors relies on consumers’ confusion and fear. They know that most consumers are unfamiliar with their rights, unfamiliar with the credit reporting dispute process, and unaware of just how frequently credit reports contain errors.

A study conducted by U.S. PIRGs found that as many as 79% of credit reports contain errors or discrepancies. That simple fact should dramatically influence the way you approach any collection listing you find on your credit report.

This article is a strategy guide that outlines common mistakes that consumers make when they find Frontline Asset Strategies on their credit report. By understanding those mistakes and approaching this process the right way, you may be able to avoid a credit report blemish altogether.

Who is Frontline Asset Strategies?

Frontline Asset Strategies, LLC is a debt collection agency. That means they collect debts that other companies have already written off. This company specifically purchases debts and attempts to collect them. Their offices are located at these addresses and can be contacted at the phone numbers below:

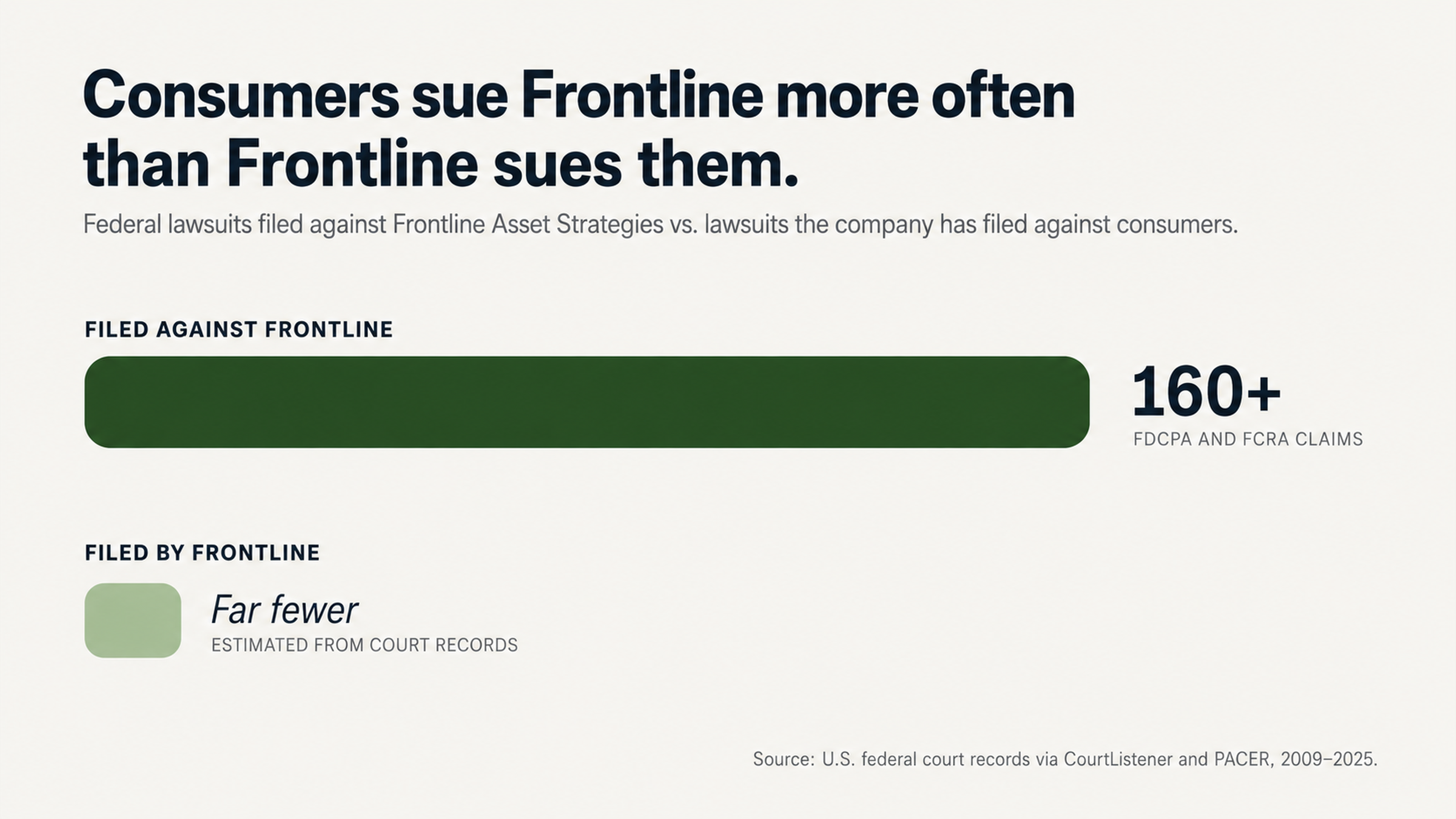

What Their Record Shows

When you research court documents and review databases of consumer complaints, you get an accurate picture of any company. As of this publication date, there have been more than 160 federal lawsuits filed against Frontline Asset Strategies for alleged violations of the Fair Debt Collection Practices Act (FDCPA) and Fair Credit Reporting Act (FCRA). These lawsuits have taken place in New York, Pennsylvania, Wisconsin, Florida, California, Ohio, and Alabama.

They have an A+ rating from the Better Business Bureau (BBB) but an average review of only 1-star out of 5. In the last three years, the BBB has closed 34 complaints against the company. The Consumer Financial Protection Bureau (CFPB) reports that in 2021, there were 46 complaints filed against Frontline Asset Strategies.

This disparity between their official rating and the actual consumer experience should influence the way you approach any debt that they claim you owe.

In late 2024, debts managed by Frontline Asset Strategies began being transferred to Radius Global Solutions LLC. This transfer of debts could have implications for accountability and the continuity of documentation. Both of those factors could help you in the course of disputing the debt that they claim you owe.

Don’t Pay a Collection Without a Dispute

Why You Shouldn’t Pay a Collection First

The single most common mistake that people make when they discover a mysterious debt collection on their report is to pay it without first verifying that it is valid. This reaction seems like the right thing to do, but in fact, it can severely harm your ability to manage the situation effectively.

For one thing, paying a collection doesn’t mean it will be removed from your report. Instead, it will be listed as a paid collection account, and the negative mark will still be viewable by lenders for up to 7 years.

Another reason that making a payment can be a mistake is that it may revive the statute of limitations on a debt that is too old for them to collect. According to some complaints filed against Frontline Asset Strategies, representatives from the company are attempting to collect debts that are 12 to 20 years old — debts that are well past the statute of limitations in most states.

In one complaint filed with the Consumer Financial Protection Bureau (CFPB), one consumer reported being called about a credit card debt from 2012. When the consumer explained that the debt was past the statute of limitations, the Frontline representative acknowledged that fact but still tried to collect the debt.

The debt collection business model is predicated on thin profit margins. When they purchase debts, it is for pennies on the dollar, so they must have a high success rate to remain profitable. This means that they very rarely invest the time and money necessary to pursue small or disputed debts. If you exercise patience and play your cards right, there are times when they simply can’t afford to pursue the debt any further.

The Importance of Debt Validation

Under the FDCPA, before attempting to collect a debt, third-party debt collectors are required to validate the debt. This means that they must be able to provide you with proof that you owe the debt, the amount that they are attempting to collect is correct, and that they have the right to attempt to collect it.

When debt collection agencies purchase debts, it isn’t always possible for them to validate debts because complete records are not always transferred during those sales. In complaints filed with the CFPB, some consumers reported that Frontline Asset Strategies failed to provide validation when asked. In one of those complaints, the consumer writes:

“I told them I didn’t know anything about the debt and he said he would email me a copy of the papers. Never got it. They also call many times a day. I told him I wasn’t agreeing to anything till I see the papers to validate it as I feel it may be a fraud account. But they still call.”

This indicates that Frontline Asset Strategies may not have the validation necessary to pursue many debts, and requesting it may help you resolve the situation.

When you dispute the debt and request validation, they have 30 days to provide it, and during that time, they are not permitted to pursue collection. If they are not able to provide the complete validation during that time, the credit reporting agencies must remove the listing from your report.

Because this can be costly and time-consuming, they may not pursue validation for many accounts.

Don’t Fall for Their Tactics

Pressure to Pay Now

Consumers often report that debt collectors attempt to create a false sense of urgency to coerce them into paying debts immediately. This can involve threatening legal action if the consumer doesn’t pay now or implying that if they wait, the consequences will be more severe. These tactics play on consumers’ fears rather than being based on the reality of the situation.

Consumers have filed complaints against Frontline Asset Strategies indicating that the company uses these tactics. In one review of the company on the BBB website, the consumer reports:

“One day I received as many as 5 calls from them! And when I called back the number the first time a rep hung up on me.”

Another consumer reported that the company called repeatedly and used the same area code in caller ID to trick the consumer into answering:

“They clearly try to trick people by using an area code the same as the person they are calling. Unethical company.”

In some instances, consumers have taken Frontline Asset Strategies to court, alleging that they attempted to coerce consumers by creating false urgency.

In Bonin v. Frontline Asset Strategies, a lawsuit filed in the Eastern District of Wisconsin, the plaintiff alleged that Frontline Asset Strategies sent letters making settlement offers with specific deadlines to create a false sense of urgency where none existed.

By creating these deadlines, the company attempted to coerce consumers into making a decision that benefited the debt collector rather than the consumer.

Don’t Let Them Intimidate You with Third-Party Contacts

Contacting Third Parties is Prohibited

The FDCPA prohibits debt collectors from contacting third parties about your debt except in very specific circumstances. Debt collectors are not permitted to contact your family, friends, employer, or others to discuss your debt with them unless they are attempting to locate you for contact purposes. Even then, there are strict limits on what they can say and do.

Consumers report that Frontline Asset Strategies contacted their family members or others in violation of their FDCPA rights. In one review on the BBB website, a consumer reported:

“Apparently, it’s accepted practice by Frontline Asset Strategy to contact any relative they can find a listed phone number for in their pathetic attempts to collect a debt. Started spamming my phone number in an attempt to reach my sister!”

Another consumer reported that the company called their daughter, who did not even live with them, in an attempt to locate them and collect the debt:

“Then I get a call from my daughter and she said this guy keeps calling her and harassing her wanting to know if she knows me and how he can get in touch with me.”

These actions are prohibited by the FDCPA and could entitle you to damages if you are affected. In some cases, individuals have successfully sued Frontline Asset Strategies for violations of the FDCPA and been awarded damages as well as having the debt they owed deleted from their credit report. One settlement was for more than $3,000.

The DIY Dispute Mistake

Information Asymmetry Favors Collectors

Consumers who attempt to dispute collections on their own are at a disadvantage. Debt collectors deal with thousands of accounts and they know how to respond to a standard dispute letter. They know what type of documentation is needed to verify the account at the credit bureau level and how certain language in a consumer’s dispute letter can provide loopholes.

This is one of the primary reasons a professional will typically have more success than a consumer representing themselves. Credit repair professionals know what documentation is needed, what the laws are, and time-frames in order to have success in a dispute. They know when a collector has not responded according to their legal obligation and how to properly escalate a dispute.

One example is in the class action settlement in the case of Haston v. Resurgent Capital Services and Frontline Asset Strategies. In this case the dispute was about collection letters that stated disputes had to be made in writing. The consumer likely would not have known the letter was not in compliance with federal law but a professional would have seen a pattern in accounts and industries.

One Error Suggests Many

If one collection account has an error or cannot be verified, it would make sense to take it a step further. If Frontline Asset Strategies placed an inaccuracy on your credit report, how many other accounts do you have like this? The same documentation issues and inability to verify likely exist with other debt buyers who use the same practices.

A thorough credit report review after a successful dispute likely shows other items in a similar situation. A consumer who stops with one account is leaving potential improvement on the table. A credit repair professional will review your report in its entirety instead of focusing on individual items.

One consumer reported that their credit score went from the low 800s to the low 700s due to a Frontline Asset Strategies account. The consumer claims they were never contacted prior to the account being placed on their credit report and they did not receive a response to their validation request. If documentation is the issue, it is likely affecting the validation process as well.

The Direct Contact Error

Why Calling Creates Risk

When a consumer contacts a collection agency by phone they are automatically at a disadvantage. The consumer has no recording of the call, statements can be taken out of context and anything you say can be used against you. Any verbal acknowledgement of the debt, promises to pay the debt, or discussion of a payment arrangement can be used against you.

Consumers have documented their experiences when they have contacted Frontline Asset Strategies by phone. One consumer reported that when they told the representative they had retained the services of an attorney and would be happy to provide contact information, the representative refused the information.

This is a red flag and suggests the company is more interested in speaking directly with the consumer instead of abiding by the law.

Another consumer reported that Frontline Asset Strategies attempted to remove funds from their bank account before a payment arrangement was agreed upon. Anytime a consumer gives a collector their banking information over the phone they are taking a risk.

Written Communication Preserves Rights

Any and all communication about a disputed debt should be done in writing, through the proper channels. A written dispute provides a paper trail, starts the clock on a collector’s legal obligation and preserves your rights under federal law.

The 30-day validation period does not start until the consumer receives proper written notification and a dispute will not start the clock unless it is in writing. A credit repair professional will handle the communication on your behalf and ensure everything is done properly.

They understand what verbiage triggers a collector’s obligation and what evidence is needed in order to request the removal of information. This is the difference between a successful dispute and one a collector can blow off.

Removal without paying is a very common outcome if a dispute shows the documentation did not exist, the account could not be verified or there was an inaccuracy. The goal is not to negotiate with a collector but force the credit bureau to remove information that cannot be verified. This will work because federal law says it has to be accurate, not because the collector wants to play nice.

The Lawsuit Fear

Understanding Collector Economics

Many consumers pay a collection account because they are afraid the debt collector will file a lawsuit against them. While the fear is warranted, it is typically more fear than reality. Debt collectors will always do a cost-benefit analysis prior to filing a lawsuit and most consumer debts are not worth the expense.

Court filing fees, attorney fees and time in court can add up quick when debts may not be collectable even after a judgment is awarded. Most of the time it will be more cost effective to dispute a debt than it is to pay it.

The debt collector likely purchased your debt for pennies on the dollar and does not have a lot of motivation to file a lawsuit because they know you are not going to pay. Your knowledge makes you a pain in the butt to the debt collector and they would much rather go after the consumer who does not know their rights.

According to court records, Frontline Asset Strategies has been sued over 160 times by consumers but the company has filed a relatively small number of lawsuits against consumers. This is an industry wide reality. Collecting a debt through the credit reporting agencies is much more cost effective than through the court system.

When Legal Threats Cross Lines

Federal law prohibits a debt collector from threatening to take legal action when they have no intention of doing so. Threats to file a lawsuit in order to scare a consumer into paying a debt is a violation of the Fair Debt Collection Practices Act and can bring statutory damages.

If a debt collector is threatening to file a lawsuit and not following through, there may be illegal collection activity occurring. An experienced consumer advocacy attorney will see this as a pattern with their clients and cases.

Over 160 federal lawsuits have been filed against Frontline Asset Strategies which means when their practices step out of line, consumers and their advocates are taking them to court. These cases have brought individual settlements and class-wide relief due to systematic violations.

When you know your rights, you hold the power. You have more power than you are being led to believe when you are on the phone with a collector.

Conclusion

Frontline Asset Strategies is a perfect example of a collection agency who relies on consumer mistakes in order to make a living. They need consumers to pay without validating, react emotionally to their scare tactics and not educate themselves on their rights. Over 160 federal lawsuits, a growing number of CFPB complaints and reports of failed validations are just a few of the warning signs of a collection agency with vulnerability.

Every single mistake in this guide is a warning sign to the consumer but an opportunity for the debt collector. Paying prior to validating, calling the debt collector, trying to handle it on your own and being afraid of a lawsuit are all mistakes that play right into the debt collector’s hands.

The correct procedure is to dispute the account, hire a professional for representation and review the report as a whole. A collection can be removed if the information is incorrect, erroneous, fraudulent or cannot be verified within a certain time period. This is not an exception to the rule, this is the way the system is supposed to work when a consumer knows their rights.

Take Action Today

If you have a Frontline Asset Strategies account on your credit report, do not make the common consumer mistake that will play right into their hands. Do not call them. Do not pay without validating. Do not try to maneuver through complex federal consumer protection laws on your own.

FightCollections.com is a professional credit repair service who specializes in disputing collection accounts and removing inaccuracies, unverifiable information and errors from consumer credit reports. We understand the documentation issues, failed validations and procedural mistakes debt buyers make and approach every consumer with the knowledge and expertise we have obtained as professionals in the industry.

Contact us today for a free consultation and to understand what your options are and how we can help. Your credit report is the gateway to your financial future, protect it in the same manner a successful dispute would dictate.