Are you dealing with Simm Associates? Don’t panic.

They may be calling you at all hours of the day and night, sending you threatening letters, and even making threats about suing you. But you have more power than you think.

The thing about Simm Associates is that they’re a big company. They’ve been around for 34 years and have call centers in multiple countries. They have an army of lawyers who have litigated successfully against 242 federal lawsuits. And they have experience with all the intimidation tactics in the book.

But Simm Associates is counting on one thing: they’re counting on you not to know your rights. They’re counting on you to get scared, to pick up the phone, and to give them your credit card information without asking questions. They’re counting on you to do what’s best for them, not what’s best for you.

But you don’t have to play by their rules. See, 79% of credit reports contain errors or inaccuracies, according to a study by U.S. PIRGs. That means that the collection account that’s hurting your credit score may not even be legitimate. And if it’s not legitimate, you have options that you don’t even know about.

So, who is Simm Associates, exactly?

What is Simm Associates?

Simm Associates is a third-party debt collector. They don’t own any debts themselves, but instead collect debts on behalf of other companies. They have been in business for 34 years and are headquartered in Delaware.

Who Owns Simm Associates?

Simm Associates is a family-owned business, owned by the Simendinger family. The President of the company is Gregory L. Simendinger. They have domestic offices in Delaware, Colorado, and Massachusetts, but also have call centers in Jamaica and the Dominican Republic.

What Are People Saying About Simm Associates?

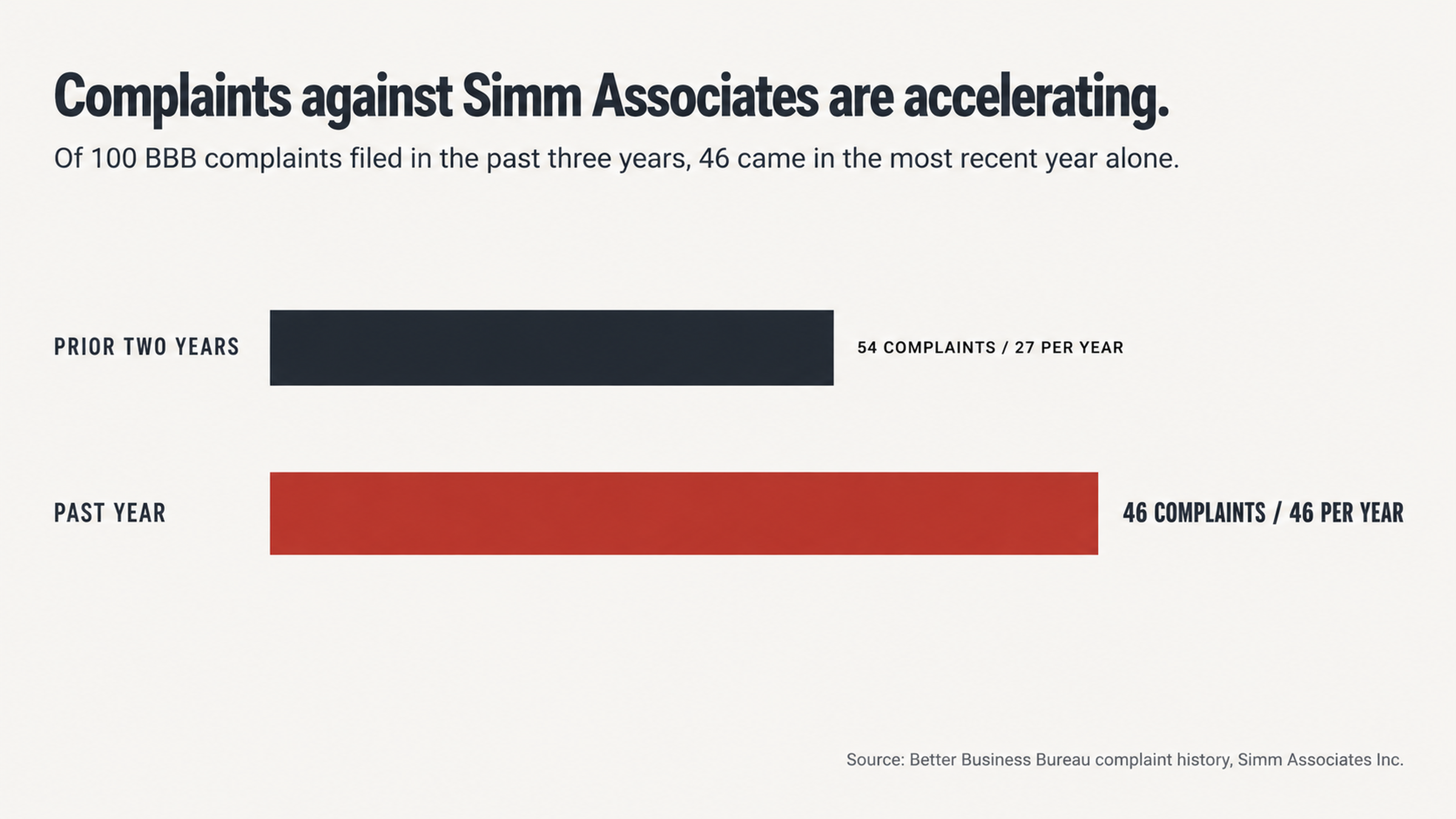

In the past 10 years, Simm Associates has had 342 complaints filed against them with the Consumer Financial Protection Bureau. In the past three years, they’ve had 100 complaints filed with the Better Business Bureau, 46 of which were in the past year alone. Clearly, Simm Associates is not making people very happy.

On the Better Business Bureau website, Simm Associates has a rating of 1 out of 5 stars. On Pissed Consumer, they have a rating of 1.4 out of 5 stars and are ranked 34 out of 232 collection agencies. Consumers rate them as “bad.”

The majority of the complaints against Simm Associates are about the same thing: Simm Associates has tried to collect debts that consumers didn’t owe. Simm Associates called consumers aggressively. Simm Associates didn’t verify debts when consumers asked them to.

In one instance, a consumer wrote the following to the Better Business Bureau:

My wife is 72 and has a lot of health problems. The person she was speaking with was extremely rude and condescending. Now mind you she is recovering from surgery, in a lot of pain, barely slept all night. To add to all of this she gets broadsided this morning by this rude and arrogant vulture who showed no compassion at all and refused to even accept the fact that she has already paid this. ALL OVER $47.

Why Paying First is a Big Mistake

So, what’s the first thing you should do if you’re dealing with Simm Associates? If you’re like most people, your first instinct will be to pay the collection. That’s what Simm Associates is hoping you’ll do, anyway.

The problem with paying first is that it doesn’t fix your credit. When you pay a collection, it changes the status of the collection from “unpaid” to “paid.” But it doesn’t remove the collection from your credit report. That means that for up to seven years, you’ll still have a collection account on your credit report that’s hurting your score.

Some credit scoring models don’t count paid collections against you, but many do. Some lenders use newer credit scoring models, but many still use the old models. So, even if you pay the collection, it can still be holding you back.

So, what should you do instead?

The best approach is to dispute first. If the information on your credit report is inaccurate, mistaken, or fraudulent, you can have it removed. And if it can’t be verified, you can have it removed, too. Why settle for a paid collection on your credit report when you can have it removed entirely?

What Simm Associates Doesn’t Want You to Know

Debt collection is a volume business. Companies like Simm Associates handle thousands of accounts at a time. That means that they can’t spend a lot of time or money on any individual account—especially if it’s a small balance.

So, what does that mean for you?

That means that when debts get sold and resold, the documentation may not follow. The original creditor may not have given Simm Associates all the documentation they need. The debt buyer may have bought a package of debts without verifying all of them.

When you dispute the debt, you’re making Simm Associates prove that they have the right to collect. You’re making them prove that the amount is accurate. And many times, they can’t.

It’s expensive to file a lawsuit. It’s expensive to track down documentation. It’s expensive to verify all of the information on a debt. And sometimes, it’s just not worth it—especially if we’re talking about a debt of $500 or less.

Don’t Answer the Phone

The minute you start getting collection calls, you may be tempted to answer the phone and talk to Simm Associates. Don’t do it.

When you talk to a debt collector on the phone, there’s no paper trail. You don’t have any proof of what was said, what was promised, or what was admitted. Debt collectors are trained to get information and commitments out of people on the phone. They know which buttons to push, which threats to make, and how to get you to start talking before you’ve had a chance to think.

One consumer reported the following experience with Simm Associates:

"From the minute I started talking to him he started raising his voice with me and started calling me a loser that needs to pay my bad debt and that he was going to see me in court. It got so ugly that he was telling me he should come kick my a__."

When you give a debt collector your attention, you’re giving them power. And once you start talking, it can be hard to stop.

The Power of Ignoring Simm Associates

When you ignore the collection calls, you’re taking away Simm Associates’ power. They can’t push your buttons if they can’t get you on the phone. They can’t threaten you or intimidate you if they can’t talk to you.

And ignoring the calls doesn’t mean ignoring the situation. It just means that you’re choosing how you want to handle it. Instead of talking on the phone, handle the situation in writing. That way, you have time to research your rights, talk to a professional, and respond thoughtfully. And if Simm Associates violates your rights, you have the documentation you need to prove it.

Knowing Where You Stand

Debt as a Commodity, Not a Moral Debt

It is a psychological reset to consider this: The debt on your credit report is not a debt. It is a commodity that is bought, sold, and traded like any other financial commodity. These debts are sold as portfolios of charged-off accounts to other companies for pennies on the dollar with the hopes that they can collect enough of the debts to be profitable.

Simm Associates, Inc. is not a debt buyer. They are a debt collector. They collect debts for the companies who buy them. But the concept is the same. The company calling you and asking you to pay the debt may have paid a mere fraction of what they are asking you to pay. The original creditor wrote the debt off their books years ago and never thought about you or the debt again.

This is not about not paying a legitimate debt that you owe. This is about recognizing that a debt collector is not some injured party who is owed money. They are a business that is attempting to make a profit from a claim they bought or were assigned. You should approach the problem from the same business perspective.

What They Have to Prove

Federal law says that you have the right to request validation of the debt. And when you properly assert that right, the debt collector is not allowed to continue collection activities until they provide the validation. That includes proving that they have the right to collect the debt, that the amount is correct, and that the debt is yours.

Simm Associates, Inc. has been party to multiple class action lawsuits that allege violations of the Fair Debt Collection Practices Act (FDCPA) regarding their collection practices. One of the suits alleged that they attempted to collect debts from consumers for debts that were usury (interest rates ranging from 450-840 percent APR) from lenders that were not licensed and thus the debts were void and/or unenforceable.

Another case alleged that they were attempting to collect unauthorized convenience fees ($12.95 per payment) that were not part of the original loan agreement.

These cases illustrate where the vulnerabilities are. Debt collectors attempt to collect debts that they may not have all the documentation for. They attempt to collect fees that they are not authorized to collect. They attempt to collect debts that may have other legal issues. When you properly dispute a debt, they are forced to prove that they can overcome all of those issues or the debt goes away.

Dispute First

Why Professionals Are More Effective

You can attempt to deal with this yourself. Many people do. They send a dispute letter that they found on the internet to the credit reporting agencies and hope that it works. Sometimes it does. Most of the time it does not.

The problem is that debt collectors deal with consumer disputes every day. They know all the tricks. They have canned responses to most common disputes. And they know which ones they have to respond to and which ones they can sidestep on a technicality.

Credit repair specialists have dealt with thousands of these cases and they know which tactics are more likely to work in specific situations. They know how to craft a dispute that the debt collector cannot ignore. And they are in a position to be much more relentless in pursuing the dispute because it is their job, not something they have to do between their job and taking care of their family.

What to Expect Along the Way

When you properly dispute a debt, the credit bureaus have 30 days to investigate. During that time, they reach out to the creditor or collector to verify the information. If they do not get a response back within the allowed time, they are required to remove the item from your report.

Debt collectors work on tight margins. In many cases, they have to decide whether to spend the money to verify a debt that the consumer is disputing or spend the money to attempt to collect a debt where the consumer is not putting up a fight. In most cases, they choose the path of least resistance. The debts that consumers fight get pushed to the back of the line or abandoned altogether.

This is not about manipulating the system to your advantage. This is about asserting your legal right to assure that only accurate and verifiable information is on your credit report. If the debt collector cannot prove their case, they should not be allowed to damage your credit.

Responding to Simm Associates

What to Avoid

Do not call Simm Associates to talk to them about the debt. Do not confirm any personal information over the phone. Do not make a partial payment because you think it will help your case. Do not agree to any sort of payment plan without knowing how they are going to report the account to the credit bureaus.

Do not assume that what they say you owe is the right amount. Do not assume you actually owe the debt. Do not assume that if you pay it, it will help your credit score. Each one of those assumptions could cost you money while failing to solve your problem.

One consumer reported this experience:

“I was illegally contacted and harassed by Simm Associates, Inc. and I do not even owe them anything. They basically told me about this relative’s financial situation in violation of collection practices.”

The lesson here is clear. Debt collectors get it wrong. They contact the wrong people. They break the rules. Do not assume they know what they are talking about.

What to Do Instead

Obtain your credit reports from each of the three bureaus. Determine exactly what Simm Associates is reporting including the amount, original creditor, and relevant dates. Take notes. This is the information you will need moving forward.

Find a credit repair expert who understands how to effectively dispute collection accounts. They will be able to evaluate your situation and develop a customized plan to attack it. They will be able to craft the correct dispute letter and manage the necessary follow up required to get results.

Keep in mind throughout the process that you have more power than the debt collector wants you to recognize. Their business model relies on consumers who do not understand their rights, who do not challenge inaccuracies, and who do not push back. You need to be the consumer who does.

Bottom Line

Simm Associates, Inc. has been in business for more than 30 years. They have been the subject of hundreds of lawsuits and thousands of complaints and are still operational. They are not going to be intimidated or scared by an angry phone call or a consumer dispute letter written in crayon.

But they do operate on an economic model that heavily favors consumers who properly challenge debts. When the cost of validating a debt exceeds the amount they are likely to collect on it, they walk away. And when consumers properly and aggressively challenge debts, they get results.

The debt that Simm Associates is attempting to collect that is on your credit report right now could be an error. It could be something they cannot validate. It could be something that you could get removed. But you will never know unless you challenge it through the proper channels with the proper help.

What to Do Next

Do not let Simm Associates dictate how this goes. Do not assume that you have to pay your way out of this. Do not sit back and wait for it to all blow over because it is not going to.

Contact us at FightCollections.com today for a free consultation. We will look at your report. We will evaluate the Simm Associates collection. And we will lay out your options for resolving the issue.

Our specialists focus on disputing collection accounts and have helped thousands of consumers restore their credit. You have rights. It is time to use them.