The dark cloud of a mystery collection account on your credit report is like a notice from a stranger that they have made themselves at home in your house.

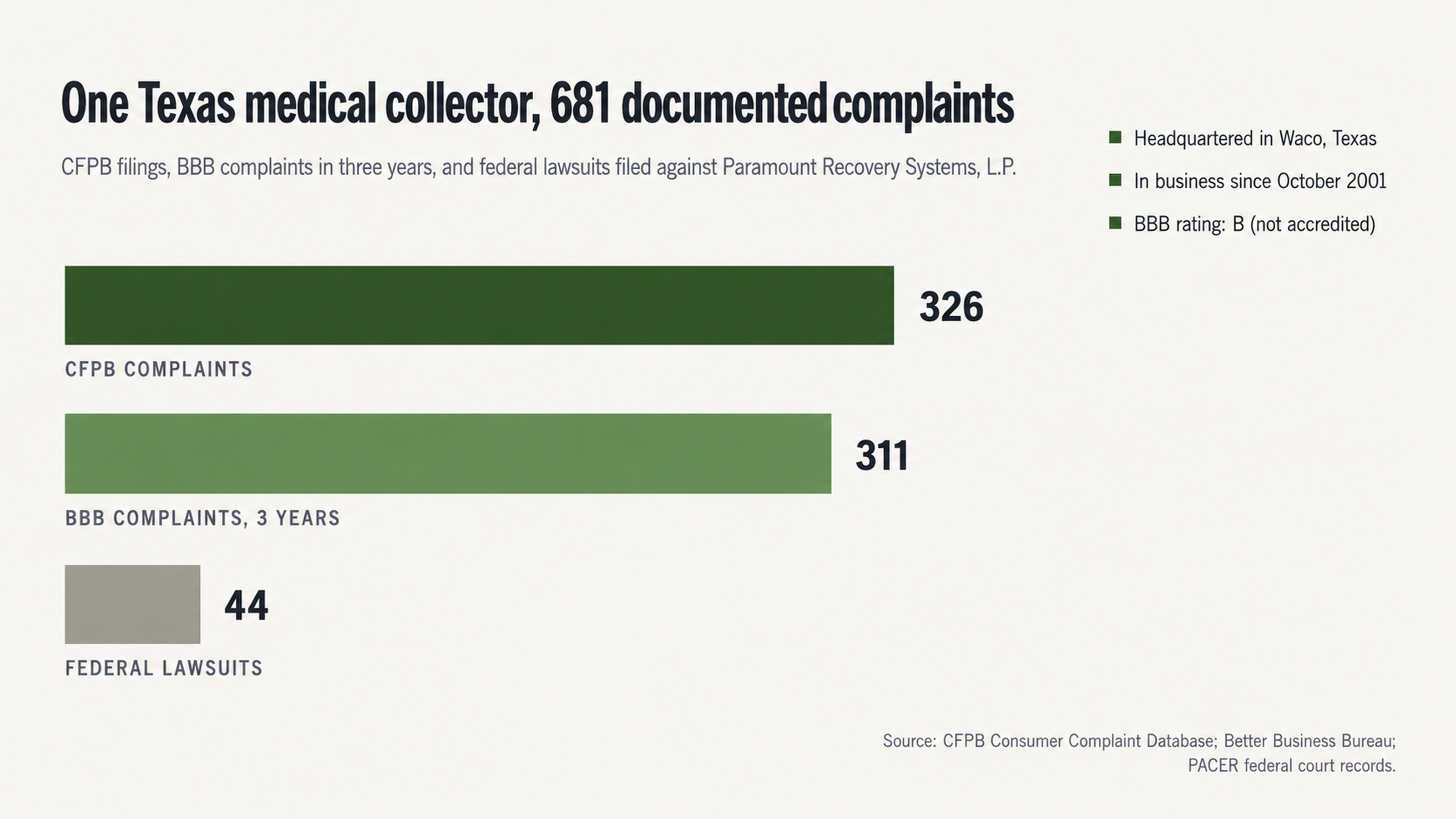

When that stranger is a collection agency named Paramount Recovery Systems, you are dealing with a company that has racked up over 326 complaints with the Consumer Financial Protection Bureau and has been sued in 44 federal cases. Fortunately, collection accounts are easier to remove than most people think.

The basis of the debt collection business model is the belief that whatever a consumer finds on their credit report is true and should not be questioned. This is true of collection agencies like Paramount Recovery.

What they won’t tell you, however, is that the burden of proving every debt they collect is accurate, verifiable, and completely documented lies solely on the shoulders of the collection agency. This article will teach you exactly how to push them to their limits and maybe even get them completely off your report.

Who is Paramount Recovery?

Paramount Recovery Systems, L.P. is a debt collection agency based in Texas that has been in operation since October 2001. This company focuses primarily on collecting debts from consumers related to medical services, including for hospitals, private practices, dental practices, and even emergency responders.

What’s Their Track Record?

Paramount Recovery has received 311 complaints on their Better Business Bureau profile within the past three years and maintains a rating of B. They are not accredited by the BBB. Customer reviews average a rating of one out of five stars.

There have been 44 cases filed against Paramount Recovery in federal court, usually for alleged violations of the Fair Debt Collection Practices Act and the Telephone Consumer Protection Act. Cases like Mills v. Paramount Recovery Systems (N.D. Texas, 4:24-cv-00448) filed in May 2024 indicate that people are still taking this company to court.

Many of the complaints filed against Paramount Recovery follow the same themes. According to one customer who filed a complaint with the BBB:

“I never received a call from them or any emails towards me having $1000 debt. My medical bills have been paid in full. I will never pay something that I have no knowledge of.”

Another customer reported:

“I cannot get in contact with this debt collector. I have called the phone number listed on the collection letter around 20 times over the course of 2 weeks and I have emailed them three times. There is only a busy signal every time.”

What Documents Does a Debt Collector Need?

No collection account can exist without the paper trail that supports it. If that paper trail has holes in it, the entire account is at risk. Once you know exactly what documents a debt collector is supposed to have in their possession, you cease to be a target and you start to be a savvy consumer who recognizes the holes in their paperwork.

The Legal Standard for Validating a Debt

According to Section 809 of the Fair Debt Collection Practices Act, a debt collector must be able to validate any debt they are attempting to collect. This isn’t a nicety that they offer to consumers who demand it. It is a legal obligation that has consequences.

In order to properly validate a debt, a collector needs to have documentation that includes the name of the original creditor, the original account number, the total amount owed along with an itemized breakdown, and evidence that the collector has the legal right to collect on the debt.

If the debt was purchased as part of a debt portfolio, that chain of ownership documentation can be incomplete in ways the debt collector hopes you never discover.

The CFPB has received complaints about Paramount Recovery for both “failure to verify debts” and “failure to provide documentation.” When a consumer disputes a collection account, the debt collector must conduct an investigation and respond within 30 days. If they cannot verify the information, it must be deleted from the credit report.

Common Problems with Documenting Medical Debts

Collecting medical debt creates some unique documentation challenges. Healthcare providers may sell batches of accounts to collection agencies, but the documentation accompanying those sales often does not meet the legal standard.

Common documentation problems associated with medical debt include the absence of an itemized statement identifying the specific services provided, missing copies of a patient’s signed agreement, missing insurance explanation of benefits documentation, and incomplete documentation of the assignment or sale of the account.

As one consumer explained in a complaint filed with the BBB against Paramount Recovery:

“I am a veteran with full VA Medical coverage. Paramount put medical collections on my credit bureaus I had taken off from another collection company. I’ve asked 3 times over the last 2 months for proof and documents of these medical bills. Paramount never sent any documents.”

If a debt collector cannot provide all the documentation they are obligated to provide, they cannot legally verify the debt. That’s not a loophole. That’s the law working the way it is supposed to work to protect consumers.

What’s on Your Credit Report?

In order to effectively challenge a collection account, you first need to understand what’s currently on your credit reports. A study conducted by U.S. PIRGs indicates that as many as 79 percent of credit reports contain errors or other serious mistakes. Collection accounts, in particular, are prone to errors since the information about them has changed hands at least once before it ends up on your credit report.

How to Use Your Annual Credit Report

You are entitled to one free credit report every year from each of the three major credit reporting bureaus: Equifax, Experian, and TransUnion. Rather than treating these annual credit reports as a perk, you should consider them to be valuable reconnaissance that can help you identify collection accounts that you may be able to successfully dispute.

As you review your reports, make a note of every piece of information related to any listing from Paramount Recovery including the date it was reported, the balance they are claiming you owe, the name of the original creditor, and any account numbers that appear in the listing.

If there are discrepancies in the information that appears on each of the three credit reports, it may indicate a data problem that you can exploit during the dispute process.

If a collection account only appears on one or two of the three reports instead of all three, that may be a sign that the collector lacks all of the information they need. If the balance listed differs from one report to the next, that could indicate a failure in verification. Both of these scenarios can provide leverage you can use during a dispute.

Which Collection Accounts Are Most Vulnerable?

Not all collection accounts are created equal. Some practically invite you to challenge them while others may be rock solid. Some common warning signs of a collection account that may be vulnerable to removal include:

- Debts you don’t recognize

- Amounts different from what you believe you owe

- Accounts that have reappeared after previously being removed

- Debts that are nearing the end of their seven-year reporting period

Many of the complaints submitted to the CFPB against Paramount Recovery include allegations related to “old information reappears or never goes away” or “debt is not yours.”

In one complaint filed with the CFPB, a consumer alleged that Paramount Recovery disclosed too much of their private medical information without authorization, which raises questions about the way the company handles sensitive data.

All of these scenarios present opportunities for removal. The only question is whether you will pursue them.

Why You Shouldn’t Pay a Collection

Paying a collection seems like the simplest way to make it all go away, but it is rarely a good idea. In fact, paying can sometimes make your situation worse.

The Hidden Truth about Paying Off a Collection

Most consumers do not realize that paying off a collection changes its status on your report from “unpaid” to “paid,” but does nothing to remove the account entirely. You will still see the negative account on your report for the full seven years.

In terms of your credit score, paying a collection provides zero practical benefit over not paying it. The “damage” was already done when the account went to collection. Paying it simply confirms that the debt was valid and the amount was correct while leaving the derogatory mark on your report.

This creates a paradox in which paying the collection may actually eliminate all of your leverage. Once you’ve paid, you’ve acknowledged that the debt was valid and the amount was correct. Disputing after the fact can become much harder.

The Hidden Dangers of a Debt Settlement

Settling a debt for less than you owe may seem like a reasonable compromise, but there are potential dangers you should be aware of before you proceed. In some cases, settling a debt can help your credit. In others, it may hurt.

One potential risk is that the settlement could be reported to your credit as “settled for less than full balance,” which some lenders treat the same as the original collection. Additionally, if the amount of debt forgiven is over $600, the collector may report it to the IRS as taxable income. That means you could find yourself facing an unexpected tax liability.

Before you consider paying all or part of a collection, you should first ensure the debt collector can provide proof that you owe the debt. If they cannot, you may be able to have the account removed without paying a dime.

Why the Dispute-First Strategy Works

The best strategy for dealing with any collection account is not to panic, pay, or ignore it. Instead, your best bet is a systematic dispute process that forces the collector to prove their case. If they can’t, removal may become your best option.

Why Disputes Succeed

Debt collection agencies do not have a lot of wiggle room in their profit margins, which means they need to resolve cases quickly. When a consumer disputes a debt, the collector must dedicate time and money to the investigation process. In cases where their documentation is not complete, that process can reveal that they do not have the ability to verify the debt.

A close look at Paramount Recovery’s responses to complaints reveals an interesting pattern. The company’s standard response to a BBB complaint often includes the following language:

“The account is closed from our agency and we have requested for our trade line be removed.”

That suggests that when consumers challenge Paramount Recovery, the company frequently decides to retreat rather than engage.

You can have a collection removed if the information is incorrect, a mistake, fraudulent, or simply cannot be verified within the required amount of time. Once you dispute the account, the debt collector has 30 days to investigate and respond. That process typically favors the consumer because the collector often lacks the documentation it needs to meet the deadline.

Should You DIY or Hire a Pro?

There is a major information imbalance between a debt collector and an individual consumer. The debt collector deals with these kinds of disputes all the time and they know exactly how much responsiveness is required to meet their minimum legal obligations. They also know which documentation loopholes they can exploit with carefully crafted language designed to mislead.

A professional consumer advocate who specializes in credit repair can help level the playing field. They understand exactly what documentation the collector needs and the procedural rules they must follow. They also understand which dispute strategies are most likely to get results. What might take you months of aggravating back-and-forth may take a professional only weeks.

Credit repair is a form of consumer advocacy. It gives you someone in your corner who understands how debt collectors operate and how to make them deliver when they fall short of their legal obligations.

Conclusion

If you have an unexpected collection account on your credit report from a company called Paramount Recovery Systems, don’t assume there’s nothing you can do. With 326 complaints filed with the Consumer Financial Protection Bureau, 311 complaints filed with the Better Business Bureau in just three years, and 44 federal lawsuits, this debt collector has already demonstrated its vulnerabilities to consumers who know where to look.

The documentation behind every collection account is only as good as its weakest link. Your job is to find that weak link and apply some pressure. Don’t let them rush you into paying before you have a chance to test whether Paramount Recovery can even prove its case against you.

Take Action Today

If you are facing a collection account from Paramount Recovery on your credit report and you don’t know where to start, contact the specialists at FightCollections.com today for a free consultation.

Our team understands the patterns and vulnerabilities that are commonly associated with debts collected by companies like Paramount Recovery. We know how to apply pressure to their documentation and how to pursue removal if they cannot meet their burden of proof.

Let us review your credit report for you to identify vulnerable collection accounts and talk to you about a strategy for challenging those accounts in a systematic way. You deserve to never hear from Paramount Recovery again.