If you’ve noticed a collection account on your credit report from Velo Law Office, you’re not the only one.

This Michigan debt collection law firm has been doing the rounds, pursuing consumers in multiple states since 2010. Some have complained about their aggressive behavior.

What You Should Know About This Company

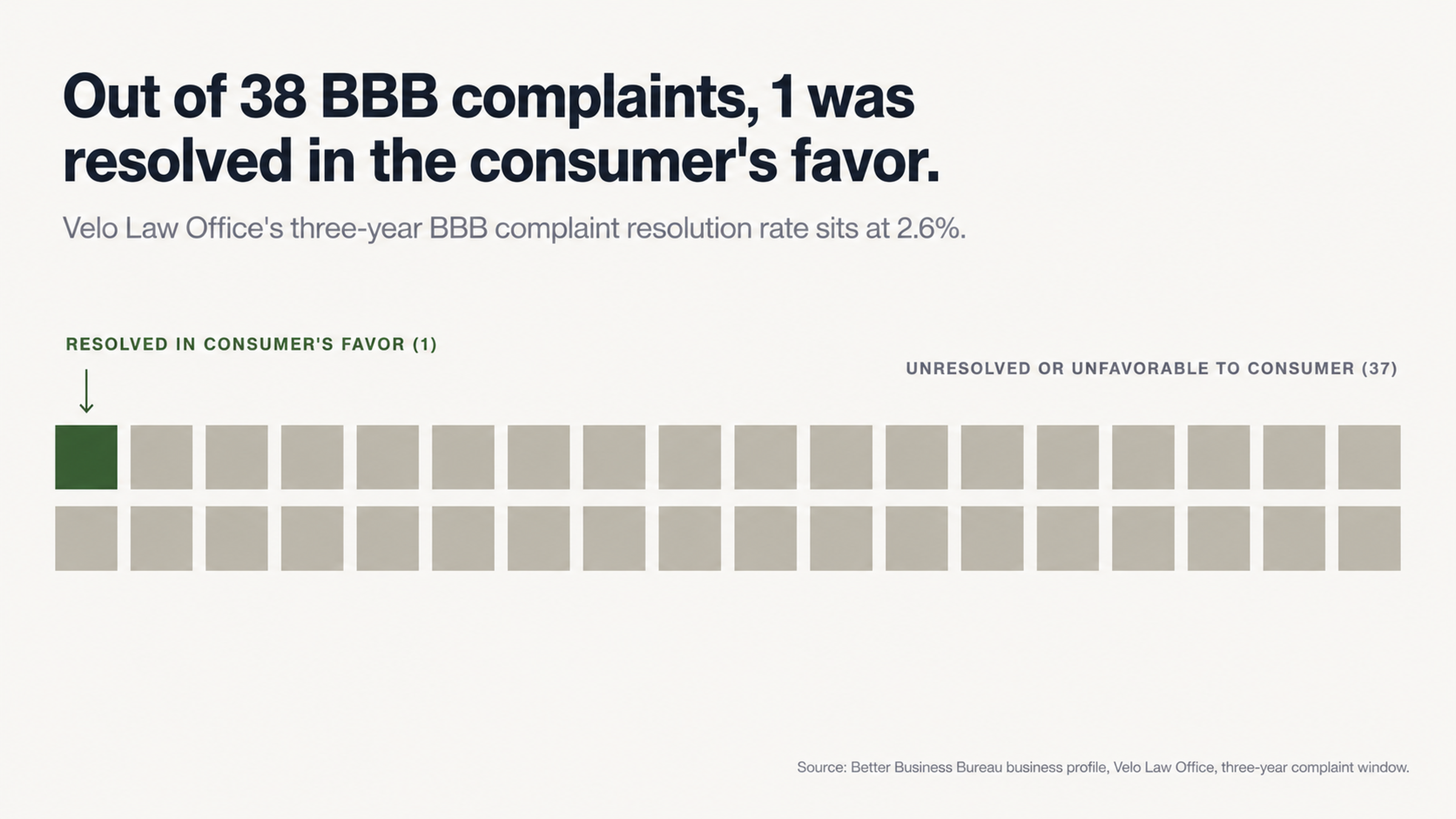

The history of Velo Law Office is an important context for you to consider as you decide how to respond. According to the Better Business Bureau, there have been 38 complaints about Velo Law Office in the past three years. Only about 2.6 percent of these complaints were resolved in the consumer’s favor.

Velo Law Office has a Google rating of 1.6 out of five stars, based on 305 reviews.

On January 12, 2023, the Michigan Court of Appeals ruled in the case of Huff v. Velo Associates (Case No. 357975) that Velo Associates, PLC was liable for $17,085 in damages for violating Michigan’s Regulation of Collection Practices Act. Specifically, Velo Law Office sued on a paid contract and inaccurately represented the amount of interest.

The presence of complaints and a court judgment against this company are not merely cautionary tales for potential future clients. They are evidence of systemic issues with this company’s operations that you can cite when disputing this account on your credit report.

What You Need to Know

The Informational Disconnect

When Velo Law Office contacts you or puts an account on your credit report, they are counting on one thing: You don’t know your rights. The debt collection industry is built around an informational disconnect. The debt collector understands their rights under the law, they understand the credit reporting process, and they understand which psychological buttons to push to get you to do something that isn’t in your best interest.

What you might not know is that once you understand your rights, the law is largely on your side. The Fair Credit Reporting Act (FCRA) and the Fair Debt Collection Practices Act (FDCPA) establish a number of procedural and documentation requirements that debt collectors frequently fail to meet.

But knowing your rights and understanding how to enforce them are different things. The specialized knowledge it takes to navigate these regulations isn’t intuitive and involves a number of non-obvious strategies and procedural technicalities. That’s why DIY approaches to resolving a debt collection dispute frequently yield suboptimal results, even when you have a solid case.

Why You Shouldn’t Rush to Pay

The first thing you might be tempted to do when you see Velo Law Office on your credit report is pay the collection agency and make it all go away. That’s what they’re hoping for. The problem is that paying a collection changes its status from “unpaid” to “paid,” but the account remains on your credit report for seven years from the date it first became delinquent.

Many consumers believe that if they pay a debt collection agency, they can have the account removed from their credit report. This process is sometimes called “pay for delete.” It rarely works as advertised. The credit reporting agencies have contracts with data furnishers that prohibit them from simply deleting accurate account histories, even if you pay.

According to U.S. PIRG, 79 percent of credit reports contain errors or other serious inaccuracies. Before you pay, your best bet is to verify that the information on your report is accurate, complete, and verifiable.

The Dispute Process

Why Disputes Work

The FCRA requires that every item on your credit report be accurate, complete, and verifiable. When you dispute an item, the credit reporting agency must conduct an investigation, and the data furnisher must respond within a reasonable period of time. If it can’t verify the information you’re disputing, the law requires that it be deleted.

Velo Law Office does business under a number of different names, according to the legal disclaimers on its website. These names include: Velo, Velo Law, Velo Law Office, Velo Group, Velo Collect, VLO, Seventeen Fifty Capital, and Velo Legal Services, PLC. This creates the potential for documentation and reporting discrepancies.

Many of the debts that collection law firms like Velo Law Office pursue have been purchased from the original creditor. In the process of transferring debts, documentation can become incomplete or corrupted. The collector may not have access to the original contract you signed, a complete record of the payments you made, or other documentation establishing a clear chain of title.

Before You Do Anything

Evaluate the Situation

Before you do anything else, evaluate the situation. Obtain your credit reports from all three bureaus and review how Velo Law Office is reporting the account. Take note of any discrepancies in the dates or amounts or any errors in the account number.

Ask yourself whether the debt is really yours. Is the amount correct? Has the statute of limitations expired? Are there any errors in the way the account is being reported? Any inaccuracy, error, or unverifiable information is grounds for a dispute.

Don’t call the debt collection agency and ask questions or attempt to verify the information. Any contact you initiate can restart the statute of limitations clock, confirm your identity and address, and give the debt collector ammunition for its collection activities. Your silence is a source of leverage in this process.

Step 1: Gather Your Documents

Start by gathering your documents. You’ll want everything you have related to the account, including your credit reports with the Velo Law Office account noted, any communication you’ve received from the debt collection agency, and any documentation you have related to the original debt.

If you have records showing payments you made to the original creditor, this is especially important. One complaint to the Better Business Bureau in August 2025 said that the consumer had made payments for six years on county jail fines, but the company was still dinging the consumer’s credit.

In February 2025, another consumer complained that Velo Law Office still had taxes garnished even though the underlying debt had already been paid. That’s why it’s crucial to have thorough documentation of your payment history.

Make a file containing copies of everything. If this dispute escalates, you’ll need documentation of your position and the history of your correspondence.

Step 2: Initiate a Formal Dispute

Your next step is to initiate a formal dispute with the credit reporting agencies. But the way you word your dispute and support it with documentation makes a difference. Generic dispute letters almost always result in boilerplate verifications that don’t change your status.

Effective disputes point out specific inaccuracies, cite relevant regulations, and demand specific documentation. They use the procedural technicalities of the FCRA and FDCPA to maximum advantage, putting as much pressure as possible on the data furnisher to verify the account or delete it.

This is where intervention from a professional can make a real difference. Credit repair specialists understand how to craft a dispute that takes advantage of the weaknesses in a collection account’s documentation chain.

Understanding Debt Collector Tactics

The Urgency Tactic

Debt collectors use urgency and fear to get consumers to react without thinking the situation through. Velo Law Office, like many collection law firms, files lawsuits and seeks garnishments as part of its collection activities. We’ve seen multiple complaints from consumers who say they were served with a summons but never received notice of a hearing.

In December 2024, one consumer filed a complaint with the Better Business Bureau saying that Velo Law Office placed a $1,700 hold on a bank account without ever contacting the consumer beforehand. The consumer said they were never served or mailed any court papers prior to the action.

This is a common tactic. Recognize it for what it is. While you shouldn’t ignore a legitimate lawsuit, you shouldn’t let a manufactured sense of urgency force you to pay a disputed debt without verifying the information.

The Settlement Tactic

Here’s something debt collectors don’t want you to know: When it offers to settle a debt for less than you owe, it’s admitting that the amount it says you owe isn’t a fixed or even necessarily accurate number. If a debt collector is willing to accept 50 cents on the dollar, then the number it originally claimed you owed was either inflated or is a negotiable number rather than a hard and fast obligation you owe.

We’ve seen complaints filed with the Consumer Financial Protection Bureau from consumers who requested debt validation from Velo Law Office, only to have the company provide documentation showing a different amount than the one it claimed in the lawsuit.

This is just one example of the ways the debt may not be accurately documented. That creates an opportunity for you to challenge the amount the debt collector says you owe.

You have more power in this situation than you think you do. The economics of the debt collection industry mean that firms like Velo Law Office are operating on razor-thin margins and need to resolve accounts as quickly as possible. When you dispute an account, it becomes more expensive for the collector to pursue than an account where the consumer simply pays.

If They Make You a Settlement Offer

What a Settlement Offer Means

If Velo Law Office contacts you during the dispute process to make a settlement offer, don’t take that as a sign that you should abandon your dispute process. In fact, you should take it as a sign that Velo Law Office may not be able to verify the full amount it says you owe, or that continuing to pursue you will be more expensive than settling.

Don’t abandon your formal dispute process simply because a debt collector makes you a settlement offer. Instead, continue to pursue your formal dispute through the proper channels.

Any negotiations should be handled by a professional who understands how to structure an agreement that protects your interests. A verbal promise means nothing. A payment plan that doesn’t include commitments about what the credit reporting agencies will be told may leave you in a worse position than you were in the first place.

The Problem With Your Credit Report

Even if you settle with Velo Law Office, the collection account will remain on your credit report as a paid collection. That will continue to damage your credit score. Some consumers have found that settling a debt actually hurts their credit scores in ways they didn’t anticipate, simply because it updates the date of last activity on an old negative account.

That’s why the dispute process can be a better option. If you’re successful, you can have the negative account removed from your credit report altogether. If you settle, you’ll still have a paid collection account dragging down your credit report.

Conclusion

What You Can Do

Velo Law Office has been the subject of a state court ruling that found the company liable for violating Michigan’s Regulation of Collection Practices Act, 38 complaints to the Better Business Bureau over the past three years with only 2.6 percent of those complaints resolved in the consumer’s favor, six federal lawsuits filed by consumers, and a 1.6-star rating from 305 Google reviewers.

These complaints and court rulings aren’t just warnings to other consumers. They’re evidence of systemic problems that you can cite in a dispute.

So what can you do? Don’t panic. Don’t contact the debt collector. And don’t rush to pay. Instead, document everything. Evaluate the accuracy of the information being reported. And initiate a formal dispute through the proper channels.

The FCRA and FDCPA establish a number of procedural and documentation requirements that debt collectors frequently struggle to meet. The 30-day window for investigating a dispute typically plays to the consumer’s advantage when they understand how to use it.

Get Help With Your Credit Report

Dealing with Velo Law Office requires specialized knowledge about the weaknesses in its documentation and procedural requirements under federal and state law. That’s exactly what credit repair specialists provide.

At FightCollections.com, we specialize in disputing collection accounts through the proper dispute process. We understand the technicalities of the FCRA and FDCPA and how to use them to maximum advantage when constructing an effective dispute. That lets us put as much pressure as possible on the data furnisher to verify or delete a questionable account.

If you’re seeing Velo Law Office on your credit report, you have options. Contact FightCollections.com today for a free consultation to discuss your situation and learn how professional dispute resolution may help you get this account removed from your credit report.