I’d be upset too if I saw a debt from FirstPoint Collection Resources on my credit report when I’d never heard of this debt before.

In fact, this happens to thousands of people every year, and a lot of people’s first reaction is to just pay the collection agency. I’m not saying it’s not tempting, but in the vast majority of cases, it’s a bad idea and will often make the situation even worse.

What collection agencies like FirstPoint Collection Resources don’t want you to realize is that you have the upper hand here.

In fact, according to U.S. PIRGs, 79 percent of credit reports contain mistakes or major errors. If nearly 80 percent of people have errors on their reports, then why would you even consider paying a collection agency without investigating further? The fact is, you shouldn’t.

So, what is FirstPoint Collection Resources and how can you handle a debt from this company?

FirstPoint Collection Resources, Inc. is a debt collection agency based in North Carolina.

Here’s a little information about this company:

This company also does business under the names FirstPoint Information Resources, Mosaic Revenue Solutions, Consumer 1st, and Insight. FirstPoint Collection Resources collects debts for healthcare providers, insurance companies, utility companies, and educational lenders.

Investigating FirstPoint Collection Resources

After a little research, here’s what I found on FirstPoint.

For starters, there are over 600 complaints against this agency in the Consumer Financial Protection Bureau database.

The Better Business Bureau has assigned FirstPoint a C rating, and the company is not BBB accredited. The customer reviews on its BBB page average just 1.25 out of 5 stars. The disconnect between their claimed industry certifications and actual consumer experiences raises questions about operational practices.

In addition, 34 percent of the complaints filed with the CFPB against FirstPoint Collection Resources are about attempts to collect debts not owed to the company. Another 28 percent are about communication tactics. This suggests a pattern of potential abuse here.

Why Would I Need to Investigate?

I know you may be thinking, Why wouldn’t I just pay it? The answer is that paying a collection agency is often not in your best interest. When you pay a collection account, the account status changes to paid. The account remains on your report for seven years from the original delinquency date.

A paid collection is still a collection. Most lenders treat paid and unpaid collections the same on credit applications. You’ll have less money in your pocket and the same credit report. The collection industry wants you to remain ignorant of this. According to various reports from consumers, FirstPoint Collection Resources does not offer a pay-for-delete agreement.

This means even if you pay the full balance, the collection will remain on your credit report. Paying a collection validates the debt in the eyes of the credit bureaus, but paying it does not result in a credit score improvement benefit.

Can I Dispute the Account?

Fortunately, yes. In fact, this is the preferred course of action here. Federal law says every item on your credit report must be accurate, complete, and verifiable. If a collection account does not meet any of these three requirements, the credit reporting agencies must delete it.

If you initiate a dispute, you’re placing the burden of proof on the collection agency and credit bureaus. They have 30 days to investigate and verify the information you’re disputing. If they cannot do so with the proper documentation, they must remove the item from your report.

Keep in mind that collection agencies buy debts in bulk and often receive incomplete records from the original creditor. When they cannot provide the proper documentation to prove they own the debt and the information is accurate, they will have to remove it from your report.

What’s the Investigation Process?

Analyzing the Accuracy of the Account

Before you consider paying or settling a debt with a collection agency, you must analyze the accuracy of the account.

One CFPB complaint against FirstPoint Collection Resources from 2021 states, “Consumer disputed this account that was reporting on their credit report. The consumer sent a certified letter to the collection agency requesting legal documentation regarding the account. The consumer states they never received the initial letter from the collection agency. The collection agency never responded to the consumer’s letter.”

We see this scenario time and time again when looking at the complaints against FirstPoint. The consumer sees the collection account on their report but never received the initial notice from the collection agency.

Under the Fair Debt Collection Practices Act, the collection agency must provide a validation notice within five days of initial communication. Failure to do so may be a violation of federal law.

Are There Gaps in Their Documentation?

The debt collection business model relies on volume and speed. Companies like FirstPoint buy thousands of debts and have a limited amount of time to collect on each account. This creates inherent weaknesses in their documentation process that consumers can capitalize on.

In the class action case Barnhill v. FirstPoint, Inc., filed in the Middle District of North Carolina, the plaintiffs claimed FirstPoint attempted to collect a debt that had been discharged through Chapter 7 bankruptcy.

In 2017, the court denied FirstPoint’s motion to dismiss these claims, stating that the plaintiff had suffered injury due to threats to credit rating, stress, and emotional anguish. More importantly, the court pointed out that FirstPoint’s admission that it operates without a North Carolina debt collection license could mean it is violating state law.

If FirstPoint is operating with a potential licensing issue and attempting to collect a discharged debt, this illustrates the weaknesses of its position if the consumer challenges it.

How Should I Handle Communication from FirstPoint?

You Have the Right to Control the Communication

Many consumers feel they need to answer the calls from a collection agency. They believe if they ignore the calls, it makes them seem irresponsible or guilty. Nothing could be further from the truth. If you block the communication from a debt collector, you are not avoiding the situation — you’re using your legal rights to prevent harassment.

Under the Fair Debt Collection Practices Act, you have the right to demand a collector to cease communication. Once you send a cease communication letter, the collector can only contact you to let you know they are ceasing communication or to let you know of potential legal action.

That’s it. Many consumers report persistent calling from FirstPoint.

One reviewer wrote, “I’ve received calls from them at my place of employment. I have informed them of this and also informed them that since I work for state government all my phone records are public information and can be accessed by anyone via FOIA. I never gave them permission to call my workplace.”

BBB complaints against FirstPoint include allegations of calling elderly family members multiple times in a single day and contacting workplaces. One consumer reported that FirstPoint called their elderly mother three times in one day looking for them, even after providing correct contact information. These documented behaviors may constitute FDCPA violations.

Under the law, a debt collector may not engage in conduct that harasses, oppresses, or abuses any person in connection with the collection of a debt.

Debt collectors cannot call you repeatedly with intent to annoy, abuse, or harass. They cannot contact third parties like family members or coworkers about your debt except in very limited circumstances. They cannot make false statements or threaten actions they have no intention of taking.

If you believe FirstPoint has violated any of these provisions, you may want to speak with an attorney about filing a claim. You may be entitled to statutory damages up to $1,000 per violation as well as actual damages and attorney fees. Remember, the FDCPA is in place to protect you — not the debt collector.

Do I Need to Rush? No You Should Not

No, you do not. In fact, rushing into anything with a debt collector will often work against you.

They will try to use threats of immediate action against you to scare you into paying, but the reality is, time is often on your side here. The credit reporting time limit is set at seven years from the date of original delinquency. So, even if you pay it, the account isn’t going anywhere until the seven-year period is over.

Additionally, if FirstPoint sues you, the lawsuit will also be a matter of public record for seven years. It’s also important to note here that lawsuits are extremely rare on smaller balances. It costs money for a debt collector to pursue legal action, and they won’t do it if the debt isn’t worth their time. So, chances are good you’re safe here. The threat of a lawsuit is just that — a threat.

How Can I Get It Removed?

Your goal with a collection account on your credit report is not to pay it. Your goal is to get it removed. There is a difference here. Paying it will not result in the removal of the account. In fact, paying it may make it harder to remove the account.

So, how can you get a FirstPoint collection removed?

You can do this through the dispute process. A collection account can be removed if the debt collector cannot verify the debt with the proper documentation. You can also remove it if the account is not accurate or verifiable.

If the statute of limitations has expired or if there was a procedural violation in the way your debt was reported, you can also get a collection account removed. Keep in mind here that a professional credit repair expert will understand how to use these situations to your advantage and will know how to properly dispute the account on your behalf. In many cases, hiring a professional will get you a better outcome than trying to handle it on your own.

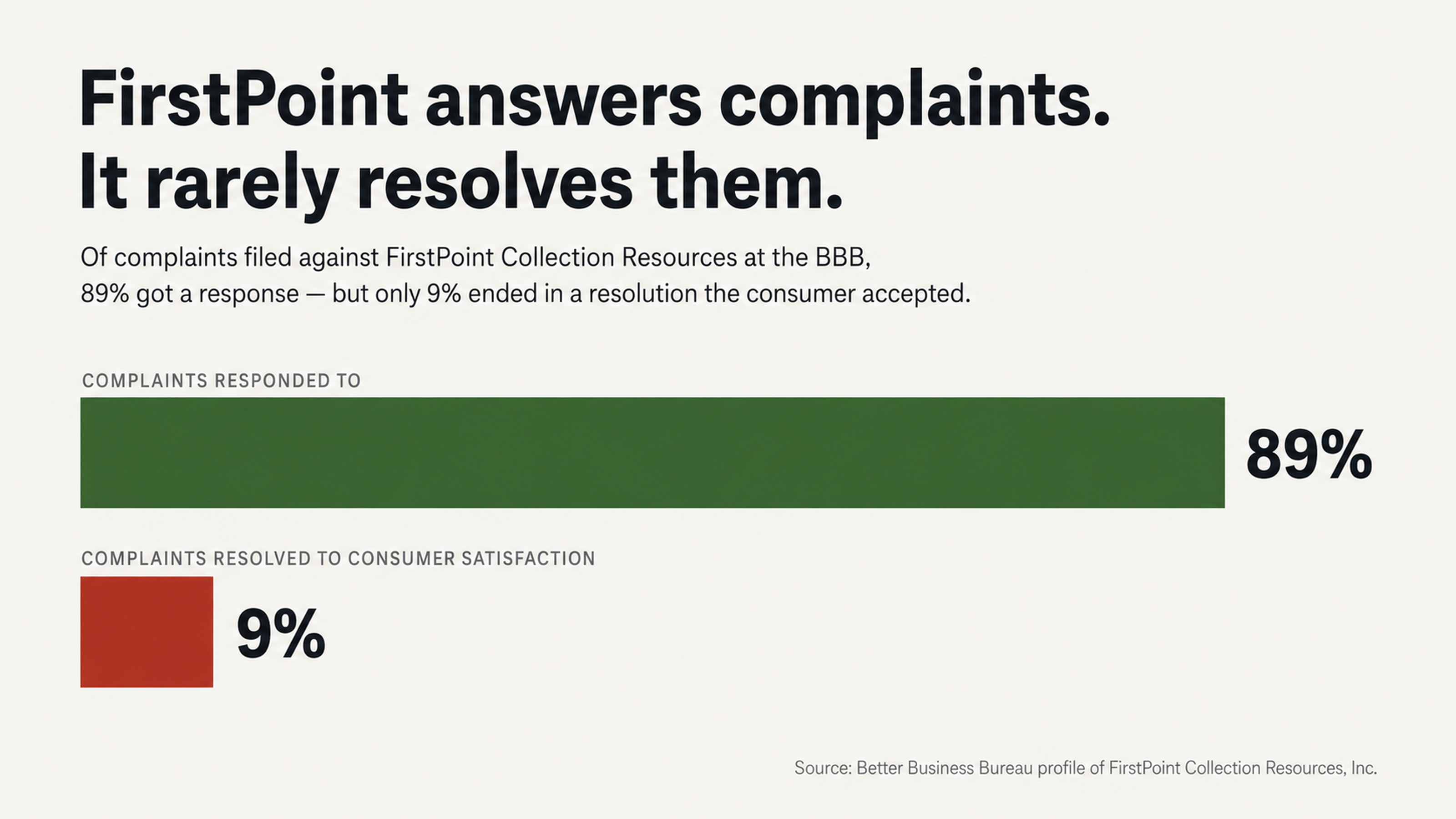

What the BBB Data Says

Unfortunately, navigating a dispute with FirstPoint may not be easy. According to its BBB profile, although FirstPoint has responded to 89 percent of complaints filed against it there, only 9 percent were resolved to the satisfaction of the consumer. This suggests the company is responding to complaints but not resolving the issues its customers are having. This may mean you need professional help to navigate the removal process.

The Bottom Line

Hopefully, this helps you understand the situation a little better if you’re dealing with a debt from FirstPoint Collection Resources. This company has over 600 complaints with the CFPB and has faced federal lawsuits alleging violations of the FDCPA. It also has a C rating with the Better Business Bureau and an average customer review rating there of just 1.25 out of 5 stars.

Over one-third of the complaints filed against it are attempts to collect debts consumers say they do not owe. This is not a company you should give the benefit of the doubt to if you see it on your credit report.

Instead, you should recognize the patterns here suggest potential abuse and challenge their accounts in every way you can. With the proper procedures and knowledge of your rights under the FCRA and FDCPA, you can often get these accounts removed which will help your credit score recover. So, don’t just pay a FirstPoint collection or any collection for that matter without investigating first.

Your Next Steps With FightCollections.com

FightCollections.com specializes in fighting debt collectors through strategic dispute procedures. Our team understands the documentation gaps, regulatory violations, and procedural weaknesses that collection agencies like FirstPoint often have. We use this knowledge to pursue removal of collection accounts from your credit report.

If FirstPoint Collection Resources appears on your credit report, do not pay them without investigation. Do not call them directly.

Contact FightCollections.com for a consultation to discuss your specific situation and explore your options for pursuing removal of this account from your credit file.