Seeing "NPAS Solutions" on your credit report can be painful. You may not even know who they are, but there they are, hurting your credit score and jeopardizing your financial future. The truth is, you have more control over the situation than you think.

According to a study by U.S. PIRGs, 79% of credit reports contain errors or disputes. With that in mind, you should think twice before assuming any collection account is accurate and uncontestable. Like most debt collection agencies, NPAS Solutions relies on a system that values speed and quantity over accuracy.

What is NPAS Solutions?

NPAS Solutions, LLC is a debt collection agency specializing in medical debt. They are a subsidiary of HCA Healthcare and were registered as a corporation on October 18, 2011, although their parent company was founded in 1980.

They primarily work with hospitals owned by HCA Healthcare, including:

Medical Center of Plano Medical City Dallas Physicians Regional Medical Center Tulane Medical Center Largo Medical Center

Knowing who's who can help you devise a plan.

Facts about NPAS Solutions

What we know about NPAS Solutions can help you understand how to approach the situation:

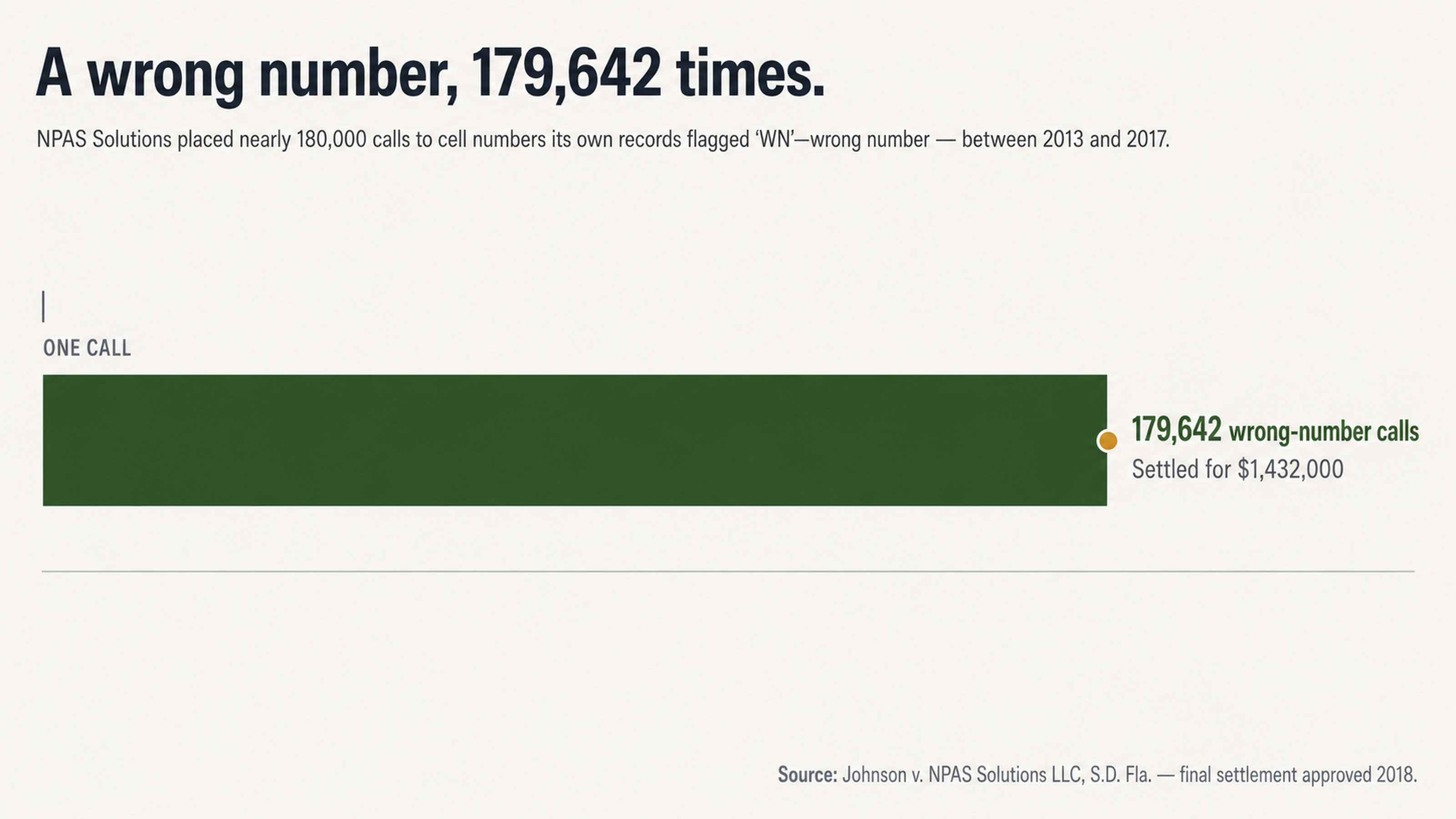

The company paid $1,432,000 to settle a class action alleging it made illegal calls to the wrong phone numbers. In the course of the settlement, it was revealed that NPAS had determined that calls to 179,642 unique cellular telephone numbers were wrong numbers, yet it had made calls to those phone numbers anyway.

According to their page on the federal court's PACER site, NPAS Solutions has been a party in over 20 federal cases.

Attorneys who specialize in consumer law report that they have settled individual FDCPA cases against the company for between $1,800-$2,200, plus attorney fees, for violating various provisions of the FDCPA, including making 12-15 calls a day and calling consumers at work despite their objections.

Despite their A rating from the Better Business Bureau, the average rating from consumer reviews is 1.0 out of 5 stars. In the past three years, the BBB has closed 37 complaints against the company, with 49% related to problems with their billing and collections.

How does NPAS Solutions work?

Once you understand how a debt collection company operates, you can work the system to your advantage. If you know what to expect, you can prepare:

The company is backed by a giant corporation.

As a subsidiary of HCA Healthcare, the largest for-profit operator of hospitals in the country, NPAS Solutions has plenty of resources at its disposal. However, that also means they approach debt collection like an assembly line.

They use several different names.

NPAS Solutions, LLC may show up on your credit report, or you may see NPAS, Inc., National Patient Account Services or Parallon. In one federal court case, the judge found that NPAS Solutions' practice of leaving voicemails identifying the company as NPAS created consumer confusion.

They collect medical debt.

Unlike some debt collectors, NPAS Solutions specializes in medical collections, which can be particularly tricky because of the complexities of medical billing, insurance and financial assistance policies. Many consumers have complained to the BBB that the company seems to have poor communication with the hospital or medical provider that charged them, or with their insurance company.

One veteran complained that he was billed for charges the VA had already paid. Another consumer said her insurance company paid for her treatment in full, yet the company still pursued her for payment.

They aim for quantity over quality.

Debt collectors like NPAS Solutions aim to process as many accounts as possible, as quickly as possible, which can lead to errors. In fact, the company's wrong-number settlement was evidence that calling the wrong phone numbers was not a one-off mistake, but rather a systemic issue. The company called wrong numbers almost 180,000 times.

That means they're likely to make mistakes.

When debt collectors process accounts by the thousands, it's easy to get the wrong person's account, the wrong amount or the wrong paperwork. Any of these mistakes can help your case when you're trying to get a collection removed from your credit report.

They're counting on you not to know your rights. Fortunately, you know better.

Why you should not pay NPAS Solutions

It's tempting to just pay what you owe and move on with your life, but it could hurt you in the long run:

Paying the collection doesn't mean it will disappear.

When you pay a collection account, you'll change the status to “paid collection,” but in many cases the account will still be on your credit report for up to seven years from the original delinquency date. You'll be paying for the privilege of still having a negative account on your report.

Paying could even reactivate the account.

In some cases, paying a very old debt can reactivate it, which could lead to more damage to your credit score.

Once you pay, you have no leverage.

If you pay NPAS Solutions, you've acknowledged that you owe the debt, which means you have no bargaining power. Instead, it's better to focus on getting the account removed.

When you dispute the debt and NPAS Solutions can't verify that you owe it within 30 days, the credit reporting agencies must remove it. If the account is completely removed, there will be no record of the paid collection or continuing damage to your credit report. That's a much better outcome than paying.

Asking nicely won't get you anywhere.

Some consumers have tried writing what's called a “goodwill letter” to NPAS Solutions, asking them to remove the account from their credit report as a courtesy after they've paid. Unfortunately, that rarely works with a debt collection agency.

Collection agencies don't have any incentive to remove accurate, negative information from your credit report, and they certainly don't have a requirement to do so. Most collection agencies follow a standard set of procedures and generally don't offer goodwill deletions.

The customer service representative who receives your goodwill letter probably doesn't have the authority to grant your request, and she probably receives dozens of letters just like yours every month, all of which receive the same form response denying the request.

Instead of spending time and emotional energy on a long-shot goodwill letter, focus on a strategy that's more likely to work.

Your rights when dealing with NPAS Solutions

Knowing your rights under the Fair Debt Collection Practices Act and the Fair Credit Reporting Act can help you navigate the system:

You can block their communications.

You don't have to put up with dozens of calls from NPAS Solutions. You have the right to insist that a debt collector stop contacting you by telephone, and they must abide by your wishes.

The telephone is a powerful tool for debt collectors because it creates a sense of urgency. They want to force you to make a decision on the spot, without taking time to check your records or talk to a financial advisor.

Many consumers have filed complaints against NPAS Solutions saying the company called them multiple times a day and even continued to call after they'd requested that the company cease communication. One consumer reported to the Consumer Financial Protection Bureau that the company was aggressive and rude when he refused to pay. Another told the CFPB that NPAS Solutions was extremely unprofessional and even threatening when they called her and her active-duty military family.

Don't engage.

Your best bet when dealing with a debt collector is to say nothing at all. You don't want to give them ammunition they can use against you, and you don't want to acknowledge that you owe the debt or restart the clock on the statute of limitations.

When you work through the mail and refuse telephone contact, you can ensure that you have a paper trail and force the debt collector to respond through the same channel.

The 30-day clock.

When you first hear from NPAS Solutions, you have 30 days to request validation of the debt. This isn't just a technicality. It's a provision of the FDCPA that the collector may have trouble fulfilling, particularly if it's a medical debt.

To validate a medical debt, the original healthcare provider must have properly assessed the charges. Any insurance must have been properly billed. If you applied for financial assistance, your application must have been properly evaluated. At any point in that process, something could have gone wrong in a way that hurts your case.

Consumers have complained to the BBB that NPAS Solutions ignored their requests for validation and continued to try to collect the debt anyway. That's an FDCPA violation that could be worth up to $1,000 in statutory damages. At least one consumer law attorney has successfully used that strategy to negotiate an individual settlement.

How to remove NPAS Solutions from your credit report

If you want to remove a debt collector from your credit report, you need a strategy:

Dispute the error.

You can remove collections if they contain incorrect, erroneous, fraudulent or unverifiable information. Given that NPAS Solutions appears to have a systemic problem with wrong-party contacts and may have issues with its validation procedures, your best bet may be to dispute the accuracy of what they're reporting.

When you dispute the account, the credit bureau must investigate and verify the information within 30 days. At that point, NPAS Solutions must provide documentation to prove that you owe the debt. If they can't, the credit reporting agency must remove the account from your report.

Their emphasis on processing a high volume of accounts at once may hurt them here. Proper validation requires time and effort to dig through the documentation for each individual account. If NPAS Solutions can't provide that within the allotted time period, they must remove the account.

Pointing out technicalities and paperwork issues is not a technicality. When you make NPAS Solutions prove that its information is accurate and complete, you're holding the company to the same standards they committed to when they chose to operate in the debt collection business. If they can't fulfill those obligations, they shouldn't be allowed to damage your credit report.

Working with a professional.

If you're not sure how to navigate the process, you can work with a professional credit repair agency.

Credit repair experts know which approach is likely to work in your case. They know what to ask for, how to ask for it and how to escalate if the debt collector doesn't respond appropriately within the right amount of time.

That's important because debt collectors are counting on consumers giving up after one or two tries. If you don't have the expertise or the time to dedicate to removing the debt collector, you need to work with someone who does.

In particular, medical debt collection benefits from professional help. To properly evaluate and dispute a medical debt, you need to understand insurance procedures, your rights under HIPAA and how to properly apply for financial assistance.

What seems like a daunting task can be manageable with the right guidance.

Conclusion

You may not recognize "NPAS Solutions" when you see it on your credit report, but the debt collection agency may be all too happy to make your acquaintance. With a history that includes a $1.4 million settlement for wrong-number calls, more than 20 federal lawsuits and dozens of consumer complaints about aggressive communication tactics and failure to validate debts, NPAS Solutions is a company you want to take seriously.

Fortunately, the same federal laws that allowed these consumers to bring their cases also protect you. Whether it's your rights under the FDCPA or FCRA, or simply your right to control your finances without harassment and abuse, you don't have to let NPAS Solutions push you around.

Don't wait any longer. Do you need help with NPAS Solutions?

FightCollections.com is a debt collection agency removal expert and is here to help you through the process of removing NPAS Solutions from your credit report.

Contact us today for a free consultation.