The Better Business Bureau has issued a Pattern of Complaints alert against Medicredit. The alert notes the following systemic issues:

• consumers are being contacted for debts that they do not owe

• consumers were not aware that they owed the debt

• requests to have the negative information removed from their credit report have been denied

How Often Are Collection Accounts Incorrect?

A study done by U.S. PIRGs found that 79% of credit reports contain errors or serious mistakes. This fact alone should completely change the way you respond to any collection account on your report.

With this knowledge, does it seem wise to just accept that the collection account is valid? Of course not. All collection accounts should be questioned, and it should be the burden of the collector to prove that the account is valid, not yours.

Has Medicredit Been Found to Have Documentation Problems?

There have been instances where federal courts have found that Medicredit failed to properly document information.

Let's take a look at one of them. In Markakos v. Medicredit, Inc. the 7th Circuit held (in May 2021) that the plaintiff alleged facts that Medicredit sent her collection letters where the amount of debt stated in the letters were not the same. In the first letter, the amount was $1,830.56, and in the response letter it was $407.00. Medicredit also failed to properly identify the name of the creditor (the creditor was listed as an entity that was not registered in Illinois).

These are just the types of problems that you should be looking for to dispute the account.

Should You Just Pay the Account?

What Happens When You Pay a Collection?

Paying a collection account will not remove it from your credit report. When you pay a collection account, the account will now show a paid status instead of unpaid, but it will still remain on your report for 7 years from the original delinquency date.

Many people believe that if they negotiate a pay for delete then the account will be removed. Unfortunately, this rarely works out as planned. Even when the collector agrees to remove the account from your report in exchange for payment, frequently the account will still remain and the consumer has no recourse.

Has Medicredit Continued to Try to Collect from Consumers After the Account Has Been Paid?

In Carroll v. Medicredit, Inc., filed in the U.S. District Court for the District of Nevada, the plaintiff claimed that she settled her hospital debt of $787.95 for a 30% discount in May 2020. After the debt was settled, Medicredit called her three times using an artificial or prerecorded voice to collect the debt (that had a zero balance).

This case illustrates an important point. Paying the debt is not going to guarantee that they will stop trying to collect it. The best bet is to question the validity of the debt before making any type of payment that will ultimately work against you.

Has Medicredit Violated Any Federal Laws?

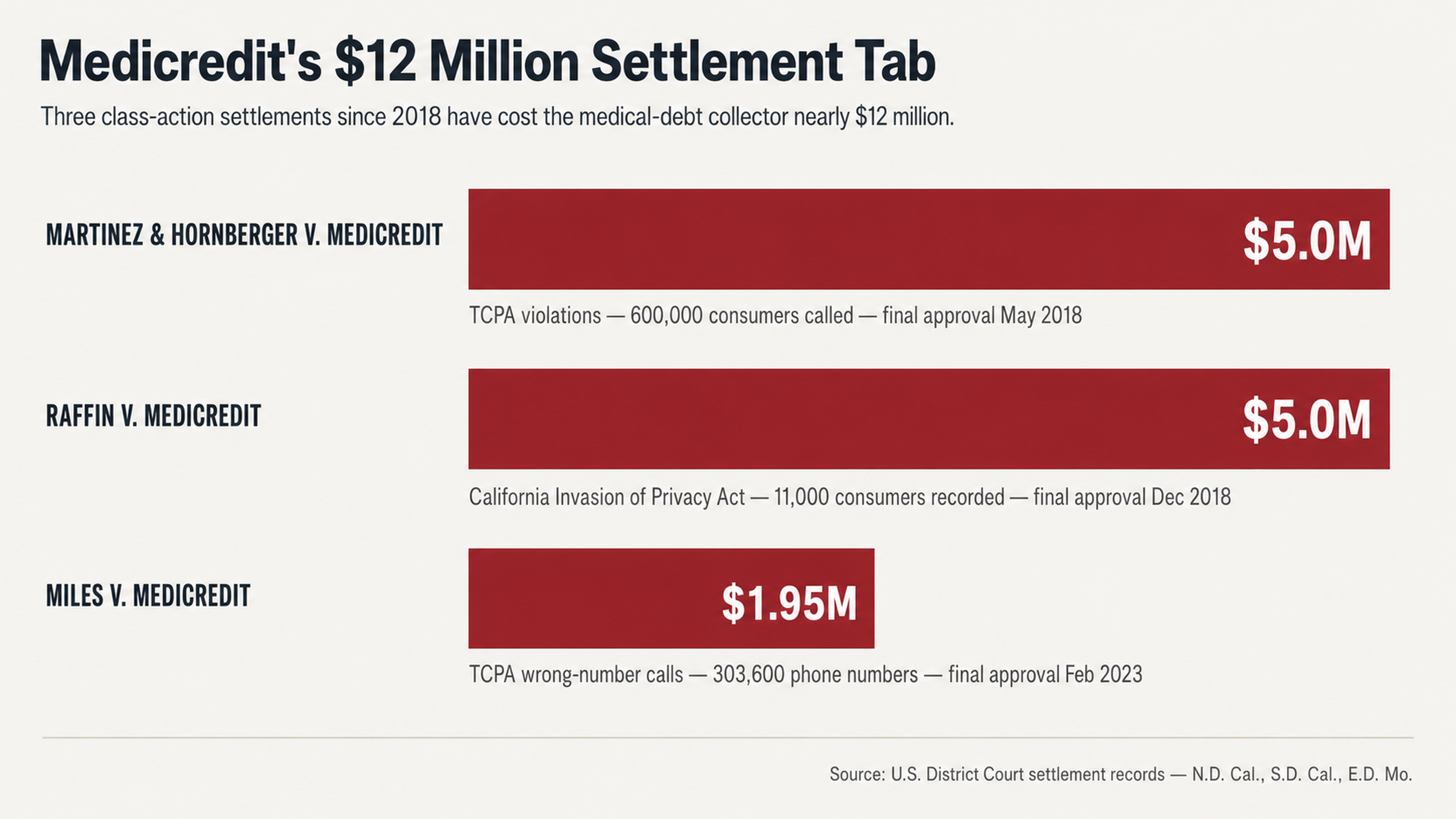

How Much Money Has Medicredit Paid in Settlements?

Does it matter if a debt collection company has paid millions in settlements? Absolutely. Medicredit has paid almost $12 million in three major class action settlements since 2018.

The first class action settlement was in Martinez v. Medicredit Inc. and Hornberger v. Medicredit Inc. The two cases were settled for $5 million (and received final approval on May 15, 2018). The cases claimed that Medicredit violated the Telephone Consumer Protection Act (TCPA) when they made automated and prerecorded collection calls to cell phones (without prior express consent) to 600,000 consumers.

The second class action settlement was in Raffin v. Medicredit, Inc. This case was also settled for $5 million (and received final approval on December 3, 2018). In this case, the consumers claimed that Medicredit violated the California Invasion of Privacy Act when they recorded phone calls with 11,000 California consumers (without their consent).

The third class action settlement was in Miles v. Medicredit, Inc. This settlement was for $1.95 million (and received final approval on February 7, 2023). The class included 303,600 phone numbers that received calls between December 2017 and July 2022 where Medicredit's internal records indicated a wrong number.

If a debt collection company has paid this much money in settlements for violating federal law, how accurate do you think they are when reporting debts to credit bureaus?

These types of settlements should tell you that the company has had issues in the past, and that they may have issues again. If you have received a collection notice from Medicredit and are questioning its validity, these class action settlements should give you some ammunition for your dispute.

What Federal Laws Protect Consumers?

What is the Fair Credit Reporting Act?

What is the Fair Debt Collection Practices Act?

The two major federal laws that protect consumers from debt collection companies are the Fair Credit Reporting Act (FCRA) and the Fair Debt Collection Practices Act (FDCPA). While both of these laws are very powerful tools, they can be tricky to use properly. Understanding the details of the laws and what consumers can and cannot do can be overwhelming for most people.

This is why hiring a credit repair expert can help consumers navigate these laws to their advantage. Credit repair experts understand exactly what a debt collection company can and cannot do, and how to use these laws to help consumers dispute accounts on their report. This is especially important in situations like this where the debt collection company has been known to violate federal laws in the past.

What Are Other Consumers Saying?

What Do the Complaints Say?

Is the collection notice that you received from Medicredit an isolated incident? The Better Business Bureau has reported 203 complaints against Medicredit in the last three years and 56 complaints in the last year alone. The consumers have rated Medicredit 1.2 out of 5 stars.

The majority of the complaints filed against the company (61%) are related to billing issues. The next most common complaint (25%) is service and customer service issues.

While these complaints are concerning, they should not be feared. Instead, use them to your advantage when disputing your account. These complaints are not just disgruntled consumers, but consumers who have had enough of the company and are now speaking out.

What Are Consumers Saying?

While the complaint statistics are helpful, let's take a look at some of the actual complaints to see what consumers are saying. One of the BBB complaints states the following: "They call my number at least 1 time a day. They never leave a message as to what the call is about... These people are cruel and will not stop calling."

In another complaint, the consumer states that the company is calling her after 9 PM. In yet another, the consumer claims that the company called between 3 and 4 AM. One consumer even reports that the company placed over 10 calls in one day.

On ConsumerAffairs, one consumer reports that Medicredit called a family member to try to collect on the debt. The family member's phone number was in no way connected to the consumer that owed the debt.

These complaints should not be used as a scare tactic, but instead as a reminder that you are not alone and that there is help out there. These complaints also show that the company has a history of errors and other issues, and can be used to help your dispute.

What Should You Do?

Why You Should Always Dispute First

If you have received a collection notice from Medicredit, what should you do next? Based on the evidence, you should always dispute first. Collections can be removed from your credit report if the account information is incorrect, erroneous, fraudulent, or if the collector is unable to verify the account information in a timely manner.

Many consumers will call the collection agency and try to resolve the account as quickly as possible. This is exactly what the collection agencies want. They know that most consumers are unaware of their rights, and that they can easily scare them into paying an account. Instead, consumers should always dispute the account first.

Do not call the collection agency. Instead, insist that all communication comes in writing. It is also important to remember that you do not have to respond to their calls. They cannot make you talk to them. Your silence is a powerful tool.

The biggest mistake consumers make when dealing with collection agencies is to communicate with them by phone. Instead, all communication should be done in writing. This will not only ensure that you have a paper trail, but it will also help you to keep the collector at bay.

Why You Should Get Professional Help

Why Should You Hire a Credit Repair Company?

While it is possible to dispute the account on your own, the best course of action is to hire a credit repair expert to help. Debt collectors do this every day. They know the law inside and out, and know exactly how to respond to consumers. Consumers, however, do not.

Credit repair companies understand exactly how to navigate the Fair Credit Reporting Act and Fair Debt Collection Practices Act. They know exactly what to say to debt collectors and what to do to help you dispute your account. This is especially helpful when you are dealing with a debt collector that has a history of violating federal law.

If you have received a collection notice from Medicredit and are not sure what to do, contact us today. We offer a free consultation and are happy to help you dispute the account.

The take away is this: do not be afraid to dispute the account. Use the tools available to you, and don't hesitate to hire professional help if you need it.

In conclusion, finding a collection account from Medicredit on your credit report is scary, but there is no need to panic. Based on the evidence, you should always dispute first. Collections can be removed from your credit report if the account information is incorrect, erroneous, fraudulent, or if the collector is unable to verify the account information in a timely manner.

Medicredit has paid nearly $12 million in class action settlements in just a few short years. They have also been found to have a pattern of complaints with the Better Business Bureau. Based on these facts alone, you should be disputing the account and not blindly paying it.

Instead of asking yourself if you owe the debt, you should be asking yourself if the debt collector can prove that you owe the debt. With the number of errors on credit reports these days, and the fact that Medicredit has a history of violating federal law, it is always best to dispute the account first.

Contact us today for a free consultation. We are happy to help you dispute the collection account from Medicredit.