Do you have Prince Parker and Associates on your credit report? If so, you might feel like an unexpected stranger just took a permanent vacation in your financial life.

But this can be a fresh start for you, too. It doesn’t have to define your credit. In fact, with the right approach, this can be the beginning of a brighter credit future.

Here are some effective strategies that have helped thousands of people remove collection accounts from their credit reports.

Who is Prince Parker and Associates?

Prince Parker and Associates is a third-party debt collection agency that has been in business since 1993. Prince Parker & Associates (PPA) is a division of Waypoint Resource Group, LLC. In February 2022, Complete Recovery Corporation of Salt Lake City acquired Prince Parker & Associates. They mainly collect debts for telecommunications companies like AT&T, U-verse, and DirecTV, as well as for medical and utility companies.

Business History:

Years in Business: 30+ years (founded 1993)

Better Business Bureau (BBB) Rating: B (not accredited)

Reputation:

Consumer complaints and lawsuits allege Prince Parker and Associates have engaged in illegal practices

What are the potential consequences of Prince Parker and Associates appearing on your credit report?

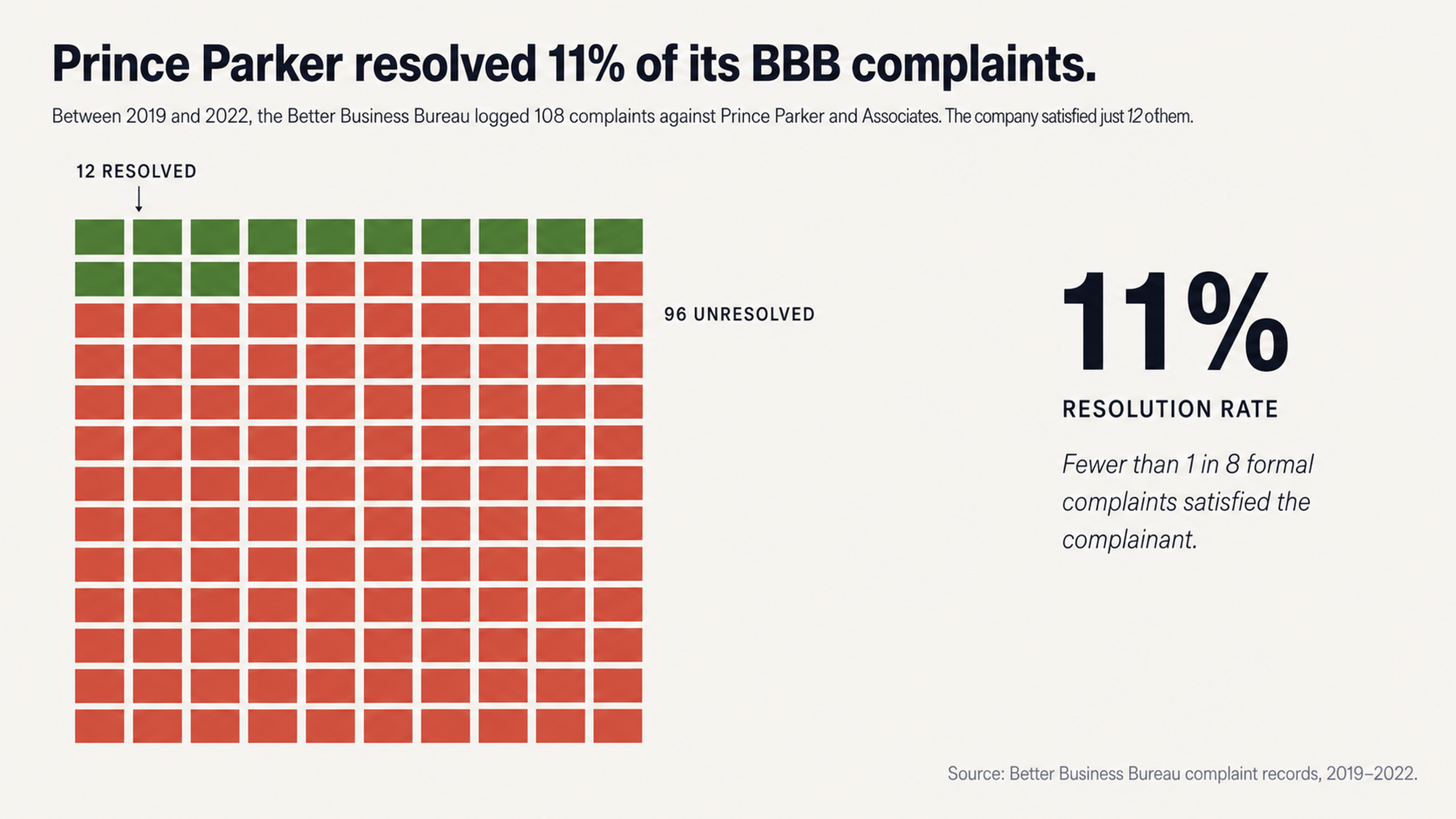

Prince Parker and Associates have a history of complaints and lawsuits that suggest a systematic problem with the way the company operates. Between 2019 and 2022, the Better Business Bureau registered 108 complaints about Prince Parker and Associates. The company was able to resolve just 12 of those complaints (11%).

In other words, fewer than one out of every eight people who took the time to file a formal complaint felt as though the company had resolved the issue to their satisfaction.

What are your rights when it comes to dealing with collection accounts?

It’s essential to understand that a debt collector must verify a debt. This isn’t a privilege for consumers. It’s a right. The Fair Debt Collection Practices Act requires third-party debt collectors like Prince Parker and Associates to validate a debt upon the consumer’s request. It’s also important to note that an estimated 79% of credit reports contain errors or inaccuracies. So, the Prince Parker and Associates collection on your credit report might be among them.

To address a collection account, you’ll need information. Start by pulling all three of your credit reports for free, then review them carefully to identify potential issues with the way Prince Parker and Associates is reporting the debt. Only then can you make an informed decision about what to do next.

You should also know that you have the right to remain silent. One of the most powerful tools a debt collector has is the pressure of a ticking clock. Representatives may urge you to pay a debt immediately, without taking the time to consider your options. But you don’t have to respond to their pressure. In fact, it’s often better if you don’t.

Prince Parker and Associates have been the subject of multiple complaints about the way representatives communicate with consumers.

For example, in September 2025, one man wrote to the Better Business Bureau to complain that a representative claimed to be a state investigator trying to deliver a subpoena. The representative reportedly called his family members multiple times, despite the fact that he asked them to stop. There’s no excuse for that kind of behavior, and you don’t have to engage with anyone who treats you that way.

When you respond to a collection call, or when you give a debt collector your financial information over the phone, you’re at a disadvantage. Everything you say can (and probably will) be used against you. Written communication gives you the paper trail you need, and it helps you avoid the urgency that can come with a phone call.

What steps can you take to dispute a collection account?

The right response to a collection account is almost always to dispute it. Unfortunately, most consumers don’t realize that. Instead, they’ll pay a collection account because they believe that will help to repair their credit.

But the reality is a bit more complicated. When you pay a collection account, it will still appear on your credit report, and the negative mark will still be visible to anyone who requests a copy of your credit report for several more years. Instead of “unpaid collection,” you’ll see “paid collection.” But that isn’t as helpful as you might think.

Disputing the account is a much better approach. When you dispute a debt, the credit reporting agencies must investigate. The collection agency must verify the information they’re reporting. If Prince Parker and Associates can’t provide documentation within a reasonable amount of time, the account could be deleted altogether. That’s not a loophole or a technicality. That’s the law working the way it’s supposed to.

The dispute process is relatively straightforward. You’re basically asking the credit reporting agency to verify that the information they’re reporting about you is accurate, complete, and verifiable. Given that Prince Parker and Associates has faced a federal lawsuit over their failure to verify debts and their failure to properly disclose information to consumers, it’s possible that many of the debts this company is collecting can’t be verified or aren’t accurate.

In 2017, a consumer law firm negotiated a settlement of $2,900 with Prince Parker and Associates on behalf of one client and a settlement of $3,200 on behalf of another client. In both cases, the company was accused of harassment and verification violations.

What are some common violations that can lead to successful disputes?

Most successful credit disputes follow a specific pattern. This isn’t a game of hit-or-miss. This is a systematic process that has been developed over years and through plenty of legal precedent. There are specific things to look for, specific pressure points that tend to work. If you hire a professional credit repair service to help you with the process, you’ll be working with people who understand exactly what those pressure points are.

For example, in June 2017, one consumer filed a complaint with the Consumer Financial Protection Bureau to report that a representative from Prince Parker and Associates disclosed information about a debt before properly identifying the consumer. The representative also reportedly failed to make legally required disclosures. When the consumer confronted the representative about these violations, the representative hung up the phone.

In another complaint, filed with the Consumer Financial Protection Bureau in October 2025, a consumer suggested that Prince Parker and Associates may have allowed a data breach. The consumer reported that he spoke with a representative from the company, and within the hour, he received a call from a scammer. The scammer had all of the same information about the debt that the representative from Prince Parker and Associates had, and the consumer felt as though his data must have been compromised.

The Consumer Financial Protection Bureau didn’t determine whether the company had experienced a breach, but the consumer’s experience is a powerful reminder that you should never give sensitive financial information over the phone to a debt collector.

What can you expect if Prince Parker and Associates threatens legal action?

One of the most common tactics debt collectors use to get consumers to pay up is the threat of a lawsuit. Representatives may suggest that you’ll be sued, that your wages will be garnished, and that you’ll experience all sorts of horrible financial consequences if you don’t pay a debt immediately. But the reality is that most debt collectors very rarely file lawsuits against consumers.

Let’s do the math. Prince Parker and Associates has between 41 and 75 employees, and the company generates about $5.3 million per year in revenue. To file a lawsuit, the company would need to pay court costs, attorney fees, and more. Most of the debts this company is collecting aren’t worth that kind of expense, especially when there’s no guarantee that the lawsuit will be successful.

Debt collectors have to weigh the cost of pursuing a debt against the potential benefit. If the debt is small, it’s just not worth it for the company to file a lawsuit. And even if the debt is larger, the company will need to clear a few hurdles before deciding whether or not to pursue the issue in court. So when a debt collector threatens to sue you, that’s probably just a scare tactic.

It’s also worth noting that many consumers have complained about the tactics debt collectors use to threaten lawsuits. Employee reviews of the company on Indeed average just 2.1 out of 5 stars. The company’s management and culture both score just 1.6 out of 5 stars.

Former employees describe being pushed to meet lofty collection goals, and being told that if you do not make goal you cannot stay here. Another employee said representatives were taught to be rude and disrespectful to debtors no matter what. That kind of culture can help explain why so many consumers report having such negative experiences with this company.

When a debt collector calls and threatens legal action, that’s all it is: a threat. It’s not a promise, and it’s not a guarantee. The company may sue you, but it’s unlikely. And either way, you don’t have to give in to the pressure those representatives are applying. You don’t have to make this decision based on fear.

How can professional help make a difference in removing Prince Parker and Associates from your credit report?

The debt collection business is all about information. The debt collector knows the rules, they know the laws, and they know all the tricks and shortcuts you can use to navigate those laws. Most consumers have never read the Fair Debt Collection Practices Act (and really, who can blame them?). So there’s an information imbalance at play here, and debt collectors exploit that imbalance whenever they can.

For example, Prince Parker and Associates often responds to complaints filed with the Better Business Bureau by saying they cannot find an active account in the name of the complaining consumer. The company uses this as a form letter, even when consumers say they’ve been receiving collection calls about an active debt. There may be no way to know for sure whether or not the company is telling the truth, but the fact that they use this kind of language so often suggests that they might be trying to brush consumers off rather than responding to their complaints in a meaningful way.

Working with a credit repair professional can help level the playing field. These experts know exactly what to ask for, where to look for potential violations, and how to navigate the dispute process efficiently. They know how the system works, and they know how to work the system on behalf of their clients. When you’re trying to remove a collection account from your credit report, that kind of expertise can make all the difference.

Credit repair isn’t rocket science, but it is a process that requires careful attention to detail and a systematic approach. When a collection agency doesn’t respond to a dispute properly, or when the information they’re reporting is not accurate or verifiable, you have the legal right to ask that the account be removed from your credit report. A credit repair professional can help you understand those rights and make sure they’re protected.

Prince Parker and Associates have a history of verification issues, disclosure problems, and communication violations. The company has been sued in federal court for leaving voicemails that don’t properly disclose the name of the company and the fact that they’re debt collectors.

Given this history, it seems likely that at least some of the accounts this company is reporting are not verifiable, not accurate, or not properly disclosed. A credit repair professional can help you identify those potential violations and develop a strategy to dispute them.

Your credit report should be accurate. It should contain only information that you have verified and approved. When a debt collector reports something on your credit report that doesn’t meet those criteria, you have the right to ask that it be removed. Don’t be afraid to stand up for yourself and assert those rights.

What are your next steps?

A Prince Parker and Associates collection account on your credit report doesn’t have to be the end of the world. In fact, it could be the beginning of a brand new chapter – a chapter in which you take control of your credit, once and for all.

So what’s the best way to get started? First, pull all three of your credit reports, and take a good hard look at them. Make sure you understand how the debt is being reported, and look for potential errors or inaccuracies that you can dispute.

It’s also important to ignore those collection calls. You don’t have to respond to a debt collector’s pressure tactics, and you shouldn’t. Instead, focus on documenting everything, and consider working with a professional to help.

Finally, don’t panic. This is a problem that can be solved, and it’s not a definition of your creditworthiness as a consumer. You got this.

Do you need help with Prince Parker and Associates? At FightCollections.com, we know how to navigate this kind of issue. We’ve worked with lots of consumers who have struggled with this exact same problem, and we’re here to help. With our assistance, you could be looking at a cleaner credit report – and a brighter financial future.

Take the first step right now. Contact us at FightCollections.com, and let’s take a closer look at your situation. We’ll help you understand your options, and develop a strategy that can help you achieve your goals.

Don’t wait any longer. The time to start fresh is now.