If you see a strange company on your credit report that says you owe them money, you probably freak out.

Synergetic Communication Inc., aka SynCom, is a debt collection agency out of Houston, Texas, that’s been around since 1996. They collect for original creditors that range from banks to hospitals.

Here’s a basic rundown of what we know about Synergetic Communication:

What the Record Reveals

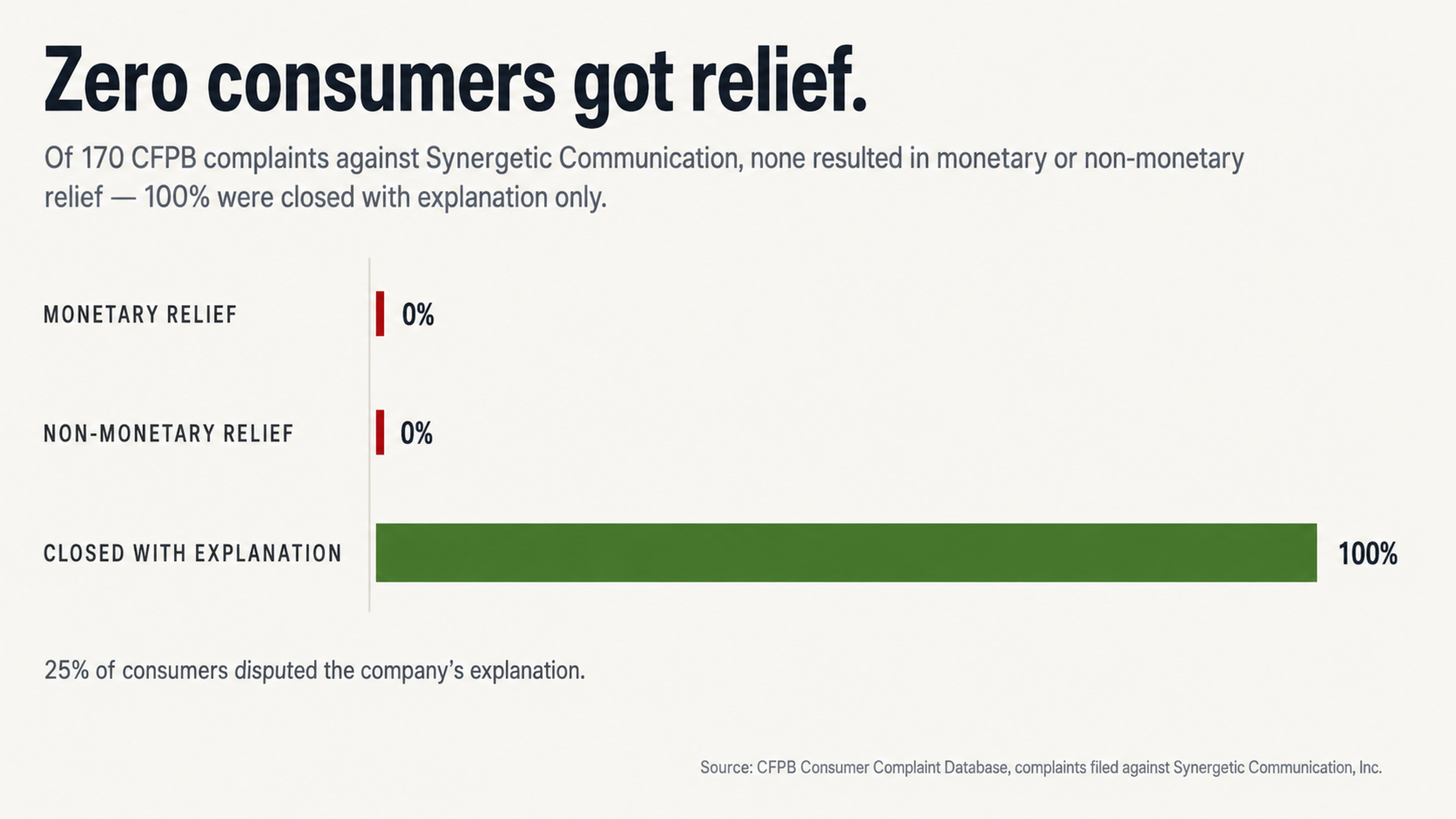

Synergetic Communication says they’re licensed to collect in all 50 states and maintain an A+ rating with the Better Business Bureau (BBB). However, there are 170 complaints about the company in the Consumer Financial Protection Bureau (CFPB) complaint database and 126 complaints with the BBB.

More importantly, the company has a 1.3-star rating from consumers on Google, which suggests that people are extremely dissatisfied with the service they received from the company.

When you pull up federal court records, you’ll find that consumer protection lawyers have filed over 30 federal lawsuits against the company, and some sources say there are as many as 70 cases in the PACER records. At least two class action lawsuits have claimed that the company routinely violates the Fair Debt Collection Practices Act (FDCPA) in its collection letter and communication practices.

We analyzed the CFPB complaint data and found the following information about how Synergetic Communication responded to complaints:

0% of the complaints resulted in relief for the consumer, which means they didn’t offer any monetary or non-monetary relief to the consumers who filed complaints against them. Instead, the company simply used the response of “Closed with explanation,” which means they just explained the company’s position without resolving the complaint.

25% of the consumers disputed the company’s explanation for closing the complaint, which suggests that about one-fourth of the consumers didn’t accept the company’s response as an adequate resolution to their complaint.

What Synergetic Communication is Banking On

They Expect You to Panic and Pay

The debt collection business is a simple game of psychology. When Synergetic Communication places a collection on your credit report or sends you a collection letter, they are banking on the fact that you’ll panic and send them money without asking too many questions. This is exactly what they want you to do.

The entire debt collection industry is predicated on the idea that if you have a debt in collections, you must owe it and should just pay it right away. This is a false narrative. According to a study by U.S. PIRGs, 79% of credit reports have errors or serious errors on them. That means the debt they’re trying to collect from you might not even be yours, might have already been paid, or might be outside of the statute of limitations.

Here’s what the debt collector doesn’t want you to know: even if you pay a collection, it still remains on your credit report as a negative entry. Instead of saying you owe the debt, the entry simply says you’ve paid the debt. The damage to your credit score remains the same, and it still takes 7 years from the date of delinquency to fall off of your report. So paying the collection accomplishes nothing except moving money from your bank account to the debt collector’s bank account.

They Expect You to Answer the Phone

One CFPB complaint said that the company called them at 5:20 am. Another consumer said that the company called them 3-4 times per day for months. A third complaint said that the company called them 4-6 times per day for over a month. We’re willing to bet that this is no accident.

Phone calls are a tool the debt collector uses to their advantage, not yours. When you talk to the debt collector on the phone, you don’t create a paper trail and you may not accurately hear or understand what the other person is saying. The debt collector can use the phone call to create opportunities to trip you up, extract information, and trick you into saying something you didn’t intend to say.

Plus, every phone call gives them an opportunity to apply pressure, use psychology, or even trick you into admitting a debt you may not even legally owe.

There’s nothing a debt collector fears more than a consumer who insists on written communication only. Written communication creates a paper trail, triggers legal obligations, and shifts the burden of proof to the debt collector where it belongs. If you challenge a debt collector in writing, the FDCPA requires them to validate your debt and prove that you owe it. This protection disappears the minute you start talking on the phone.

The Verification Gap: Where Collectors Fail

Collection Letters Under Legal Fire

Multiple class action lawsuits have targeted Synergetic Communication’s collection letters as a potential vulnerability in the company’s practices.

In the case of Chein v. Synergetic Communication (Case No. 1:16-cv-06138), which was filed in the Eastern District of New York in November 2016, the plaintiff claimed that the company sent a collection letter seeking payment of a debt in the amount of $2,827.42 that failed to comply with FDCPA safe harbor language requirements.

Specifically, the plaintiff claimed that the collection letter failed to disclose whether the balance of the debt was accruing interest and failed to state the date on which the balance had been obtained. The plaintiff also claimed that the company failed to disclose that the debt could be subject to the accrual of prejudgment interest, as permitted under applicable state law.

In another class action case, Devitt v. Synergetic Communication (Case No. 2:17-cv-06520), the plaintiff claimed that Synergetic Communication’s collection letters contained a misleading statement of a consumer’s dispute rights under the FDCPA. The plaintiff claimed that the company’s collection letter advised consumers that they must “write to us” in order to dispute the debt at issue.

However, the plaintiff claimed that this language is deceptive because it suggests that a written dispute is required under the FDCPA, which isn’t true. The plaintiff said that this type of language would confuse the least sophisticated consumer.

These two cases suggest that Synergetic Communication’s collection letters may contain technical violations of the FDCPA that you can dispute. If the debt collector fails to properly disclose required information to you, it’s possible that you can dispute the accuracy of the underlying debt information.

The Documentation Problem

Whenever a debt collector pursues a debt, the debt has already changed hands multiple times. The original creditor sells the debt to a debt buyer, and the debt buyer may sell it to another debt buyer, which creates a chain of custody problem. Every time the debt changes hands, the documentation gets weaker, records are destroyed, and the ability to properly verify the debt diminishes.

This creates a giant vulnerability for the debt collector whenever you demand verification of the debt. In many cases, the documentation that’s required to prove a debt is valid and legally owed often no longer exists in the required form. The account statements are gone, the original contract is gone, and the chain of ownership is gone. All the debt collector has is a line on a spreadsheet that says your name, a balance, and a creditor.

Credit bureaus add to the problem because they favor speed and efficiency over accuracy. When a debt collector reports a debt to the credit bureau, the credit bureau typically adds the information to your report without verifying it. This is why 79% of credit reports contain mistakes or serious errors. Instead of scrutinizing data, the credit reporting system simply allows data to flow into it.

Why Payment May Not Be the Answer

The Credit Report Reality

The real battle here is not about your checkbook — it’s about your credit report. The goal is not about whether you owe the debt — it’s about what’s on your report and how long it stays there. Once you realize this, the entire way you approach this problem shifts.

A collection account on your report hurts your credit score whether you pay it or not. While newer credit scoring models like FICO 9 and VantageScore 3.0 ignore paid collections, many lenders still use the older models where paid collections can hurt your score just as much as unpaid collections. The only way to avoid the credit damage is to get the account entirely removed. This can happen in two ways: either the information can’t be verified, or it can be proven to be inaccurate.

This is why the dispute process is so critical. Instead of simply accepting the debt collector’s story and paying because they said so, you challenge the accuracy of the information they’re reporting and force them to prove it. Often, they can’t do that.

The Dispute Alternative

Disputing a collection account shifts the burden of proof to the debt collector and the credit bureau. Under the Fair Credit Reporting Act (FCRA), credit bureaus must investigate and respond to your disputes within 30-45 days. The debt collector must respond with verification or the account gets deleted.

Most people don’t even realize this is an option because debt collectors certainly don’t tell them. The debt collection industry makes money off the assumption that you’ll simply pay. Every dollar they collect is income; every successful dispute is a loss. Their goal is to keep you focused on paying the debt, not challenging whether it’s accurate or not.

This is the foundation of professional credit repair. Instead of negotiating payments that leave the negative reporting intact, the process involves identifying inaccuracies, requesting verification, and challenging anything that can’t be verified. It recognizes that debt collectors often can’t support their claims when challenged properly.

Protecting Yourself from Synergetic Communication

The Power of Written Communication

If Synergetic Communication is contacting you, the best thing you can do is ignore their phone calls and engage in written communication only. Never answer a call from an unknown number. Let all the voicemails go to a voicemail log so you can keep track of them. If you make a response, do it in writing and send it via certified mail with return receipt requested.

Written communication protects you because it creates a paper trail. You can’t get pressured into saying something you don’t want to say, and you can’t misinterpret what the other party is saying. Most importantly, written debt validation requests create specific legal obligations that phone calls don’t.

Former employees have made troubling allegations against Synergetic Communication.

One report from a self-described former employee in 2009 claimed, “They violate the FDCPA and the management (Mike and George) all promote the collectors to violate whenever possible.”

Another report from a self-described former employee in 2018 claimed that the company “misrepresents payment arrangements as settlement agreements” and allows “collectors to work on portfolios of which they’re not licensed.” These allegations suggest why verbal agreements with this company are risky.

Guarding Your Information

Information should only go one way here: from the debt collector to you. Anything you share can and will be used against you. They may use it to find other assets or verify your identity on the debt, or even try to reset the clock on the statute of limitations. If you confirm something as basic as your address or employer, you’ve just made their job easier.

Whenever the debt collector calls, they often ask questions under the guise of routine protocol. If you confirm your date of birth, social security number, or current employer, they now have documentation they may not have had before. In some states, if you verbally acknowledge that you owe a debt that’s past the statute of limitations, you may inadvertently reset the clock so the debt is collectible again.

Many consumers fear lawsuits and wage garnishment, but in reality, this fear is often misplaced. It’s expensive and time-consuming to sue consumers, so it’s often not worth the effort for smaller debts. While a lawsuit is possible, it’s relatively rare. Debt collection agencies prefer to use the phone and credit reporting as leverage because it’s easier and more effective than taking their chances in court.

Take Back Control Today

Ultimately, Synergetic Communication — like all debt collectors — is relying on you to make decisions based on fear and misinformation. They are hoping you’ll answer their phone calls, panic when you see a collection notice, and pay the debt without challenging whether it’s accurate, verified, or even legally yours. If you don’t do what they expect, you can gain the upper hand.

All the evidence suggests that this company has serious issues. With over 30 federal lawsuits, nearly 300 combined complaints on the CFPB and BBB databases, multiple class action lawsuits alleging FDCPA violations, and a 1.3-star consumer rating, there are plenty of reasons to believe this is a company with operational problems that create dispute opportunities.

Whenever a debt collector can’t verify information or has a history of procedural mistakes, the accuracy of the underlying credit reporting becomes a legitimate question.

Of course, navigating the dispute process requires knowledge of federal law, credit bureau policies, and debt collector tactics. Many consumers who try this on their own find themselves outgunned because the debt collection industry is set up to exploit information asymmetry. That’s why professional credit repair exists.

If Synergetic Communication is on your credit report, don’t call them. Don’t confirm any of your information. And don’t assume you owe the debt just because they say you do.

Instead, contact FightCollections.com to explore your options for disputing this account and getting it professionally removed. Your consultation is free, and you deserve to understand your options before you make any decisions that affect your financial future.