Has ARM Solutions surprised you by placing a mysterious collection account on your credit report?

This may have caught you off guard as they have already begun the collection process and designated you as a debtor before you even realized the collection process had begun.

One thing that debt collectors do not want you to realize is that the systems that they employ in order to collect from you are flawed, inconsistent, and sometimes done in a hurry. All of these tactics can be leveraged in your favor.

In fact, according to a comprehensive report published by U.S. PIRGs, 79% of credit reports contain some kind of error, inaccuracy, or serious error. This simple fact should change the way you approach any collection account that appears on your credit report. The issue is not whether you owe the money or not. The issue is whether or not they can actually prove it.

Who is ARM Solutions?

A.R.M. Solutions, Inc. is a California-based debt collection agency that may also be referred to by the alternate names Accelerated Revenue Management and A R M Solutions.

Their Business Practices

The regulatory and complaint history of ARM Solutions paints a troubling picture of a company that consistently violates the rights of consumers. On November 20, 2023, the California Department of Financial Protection and Innovation (DFPI) issued a Consent Order against the company for violating the California Rosenthal Fair Debt Collection Practices Act.

The Consent Order found that ARM Solutions sent text messages to consumers that failed to state the company was a debt collector and failed to state the company’s California license number. As a result of the findings, the company was ordered to pay a $2,500 civil penalty to the DFPI and was issued a Desist and Refrain Order to stop violating the Rosenthal Act.

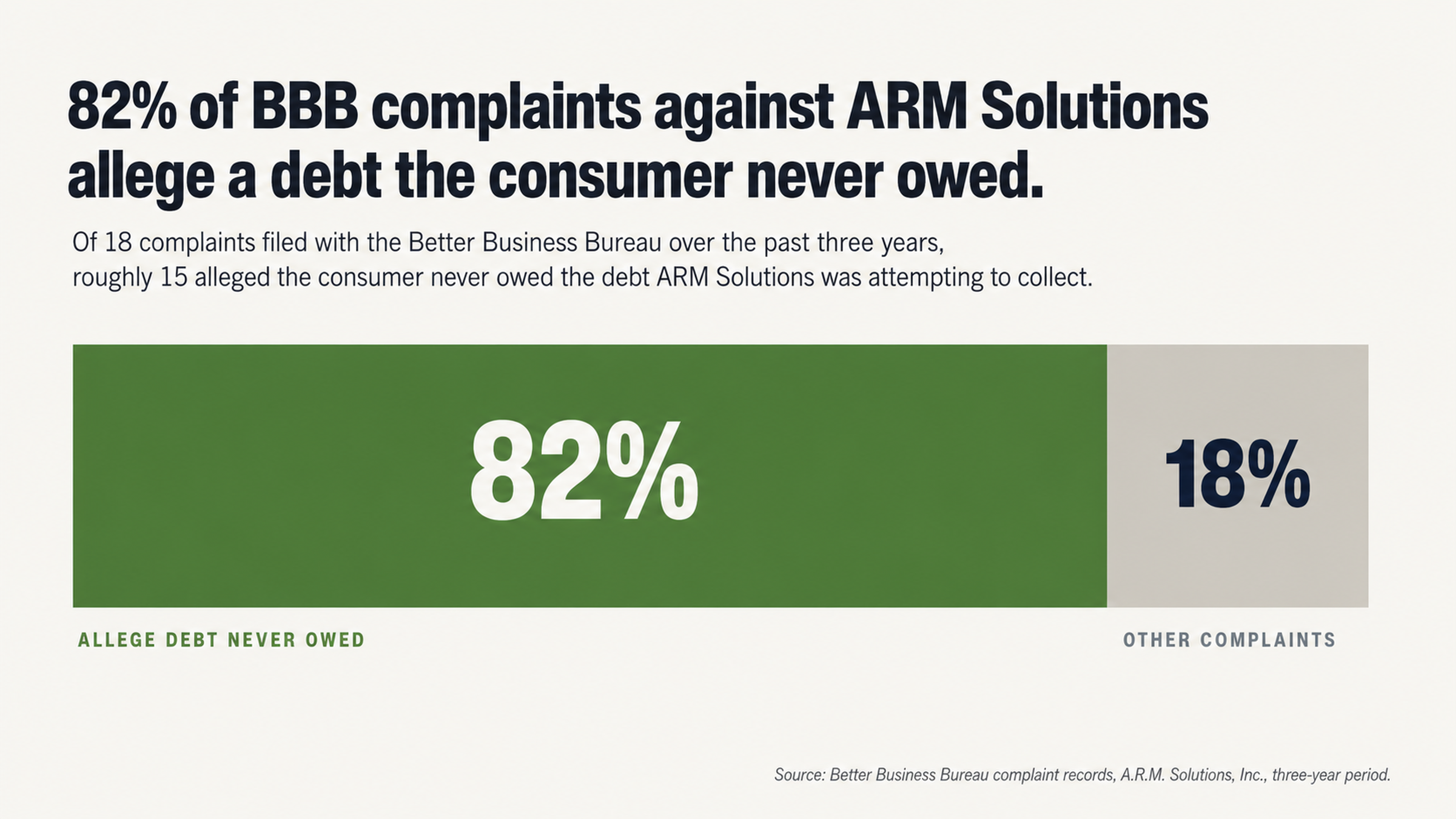

Over the past three years, 18 complaints have been filed against the company with the Better Business Bureau (BBB), with seven complaints closed in the last 12 months. The majority of those complaints (82%) allege the company is attempting to collect a bill they never owed.

Inside an ARM Collection Agency

Why Quantity Trumps Quality

Debt collection agencies like ARM Solutions are volume-based businesses. This means that they collect on as many debts as possible and do not necessarily worry about whether the information on file is accurate or not. Most collectors are paid based on the number of debts they collect on and the number of phone calls they make every day. This creates an environment where collectors are much more likely to pursue a debt without validating it first.

Further, most debt collection agencies experience a high rate of employee turnover and do not take the time to train their employees properly. In addition, when one company purchases a debt from another company, they typically only receive very basic information on the account.

Because of this, when a debt collection agency like ARM Solutions receives a debt from a creditor, they may not receive the full contract that was signed by the consumer. They may not receive the full payment history of the consumer. They may not even receive the name and address of the consumer spelled correctly. They may also fail to receive the correct balance due on the account as well as all of the terms and conditions of the account.

ARM Solutions has been sued in at least three federal cases accusing the debt collection agency of violating provisions of the Fair Debt Collection Practices Act (FDCPA).

In the class action case Jakub v. A.R.M. Solutions, Inc. (Case Number 3:12-cv-06113), filed in the Northern District of California, the plaintiff claimed the company used abusive debt collection practices, attempted to collect amounts not authorized by the agreement, and failed to provide adequate notice and verification of the debt.

The Case for Missing Documentation

When a debt is sold to a debt collection agency, the documentation rarely follows. In most instances, the signed contract between the original creditor and consumer is never provided to the debt collector. The payment history on the account may also be missing. In many cases, all the debt collector receives is a spreadsheet with names, addresses, phone numbers, and amounts due.

This creates a huge problem for debt collection agencies like ARM Solutions. Under the FDCPA, consumers have the right to request verification of a debt at any time within the initial 30 days after they are first contacted. However, verification is only as good as the records the debt collector maintains.

If the original creditor did not provide the complete documentation to the debt collector, they will not be able to provide it to the consumer. An analysis of consumer complaints made against ARM Solutions includes several instances where the company allegedly refuses to validate debts when requested and refuses to cease collection efforts during the validation period as required by law.

These alleged actions are clear violations of the FDCPA.

The Dangers of Paying a Collection

Why You Should Never Pay a Collection First

When a consumer discovers a collection account on their credit report, their first course of action is usually to pay the debt. They believe this is the best way to resolve the account and prevent further damage to their credit report. Unfortunately, this is rarely the case.

When you pay a collection account, you are only changing the status of the account from unpaid to paid. However, the collection will still remain on your credit report for seven years from the original delinquency date. Therefore, paying a collection will not improve your credit score.

In addition, when you pay a collection, you are providing written documentation that you admit to owing the debt. In some jurisdictions, admitting to a debt can reset the statute of limitations on the debt. In others, it can create an admission that may make it more difficult for you to dispute the debt later.

One consumer filed a complaint with the Better Business Bureau against ARM Solutions that claimed they continued to receive text messages attempting to collect a debt even after making a payment in full for the account.

“Paid this account in full on September 20, 2022 and I am still getting text messages to pay the account,” the consumer wrote. “I called ARM Solutions and they claim it has no record of my payment. I have a copy of my bank statement that shows the payment was made and posted to my account.”

The Hidden Dangers of Settling a Debt

When a consumer is contacted by a debt collection agency regarding an outstanding account, they are often told that settling the debt for less than the balance due is the best option for their credit score. Unfortunately, this is not always the case.

When you settle a debt for less than the balance due, the account may be reported to the credit reporting agencies as settled for less than the amount due. This notation can have a negative impact on your credit score depending on the credit scoring model being used.

Before you consider paying or settling a debt with a debt collector, you should always investigate the accuracy of the account first. Paying an inaccurate account will not make the account accurate. It will simply make you poorer while the inaccurate information remains on your credit report.

Patterns in Consumer Complaints Reveal Potential Liabilities

When Debt Collectors Target the Wrong People

A number of complaints filed against ARM Solutions accuse the company of attempting to collect debts from the wrong consumer.

One consumer review left on the Consumer Affairs website claimed ARM Solutions attempted to collect an overdue video rental late fee from the now-defunct video rental chain Hollywood Video.

“My brother and I just received a letter from A.R.M. Solutions saying we owe past due late fees to Hollywood Video,” the reviewer wrote. “How Hollywood functioned was you had to pay the late fees or you could not rent anything. I am outraged that I have to deal with this kind of scam. Hollywood Video has been closed for over two years.”

Another consumer accused ARM Solutions of harassing them to pay for an alarm company contract they claim they never agreed to.

“Alarm company broke into my rental unit, removed the existing alarm control pad, installed theirs illegally and harassed me for payment,” the consumer wrote in their complaint filed with the BBB. “A.R.M. Solutions is now attempting to collect for the same.”

Ignoring Bankruptcy Discharge

Consumers who file bankruptcy are granted protection from debt collectors attempting to collect debts that have been discharged in the bankruptcy. Once a debt has been discharged, the debt no longer exists and attempting to collect it is a violation of federal bankruptcy law.

In some instances, attempting to collect a discharged debt may constitute contempt of court.

On November 7, 2023, a consumer filed a complaint with the BBB claiming ARM Solutions was attempting to collect a debt that had been discharged in bankruptcy.

“Have already notified this company that this debt was included in my Chapter 7 bankruptcy that was discharged on October 23, 2023,” the consumer wrote. “A.R.M. Solutions continues to attempt to collect this debt despite my notification.”

The bankruptcy was originally filed on October 11, 2022, and converted to Chapter 7 on July 13, 2023.

What Collectors Can’t Do

Prohibited Debt Collection Practices

Debt collection laws such as the FDCPA provide consumers with a number of protections against prohibited debt collection practices.

Debt collectors may not harass consumers with threats of violence, arrest, or jail time. They may not threaten to sue a consumer unless they intend to follow through with the threat. Debt collectors may not misrepresent the amount of the debt. They may not misrepresent their company or imply they are affiliated with a government agency or law firm when they are not.

Debt collectors may not discuss a consumer’s debt with a third-party that is not authorized to receive the information. They may not publish the consumer’s name on a bad debt list. They may not make false statements in an attempt to collect a debt.

Debt collectors may not add additional interest or fees to the balance due unless it is authorized by the original contract or permitted by state law. They may not threaten to seize property when they have no intention of doing so. They may not threaten to take an action that is illegal.

Finally, debt collectors may not contact a consumer at work if the collector is aware the employer prohibits such calls.

A review filed on the Consumer Affairs website accused ARM Solutions of refusing to identify itself as a debt collector but continuing to harass consumers who do not owe the debt.

“This company refuse to identify themselves as a debt collector, but will continue to harass people,” the reviewer wrote. “They have called me 9 times in one day on a number never provided to them.”

Another reviewer wrote:

“They will not stop calling and will call multiple times a day from different numbers. When you answer they do not say anything, will not leave a message but keep calling.”

At least four consumer protection law firms currently have an active page on their website to track patterns and problems experienced by consumers when dealing with ARM Solutions.

How Strategic Silence Works in Your Favor

The Psychology of Debt Collection

Debt collectors want consumers to believe they have one option and one option only: pay the debt as soon as possible.

In pursuit of this goal, debt collectors will do everything in their power to scare and intimidate consumers into reacting out of emotion rather than logic. They want consumers to call them now, admit to the debt now, and pay as much as possible now without taking time to evaluate the situation.

However, consumers are under no obligation to speak to a debt collector on the phone, return a debt collector’s messages, or communicate with a debt collector at all. In fact, doing so can weaken a consumer’s position and provide leverage to the debt collector.

Everything a consumer says to a debt collector can and will be used against them. Saying nothing at all preserves the consumer’s rights and forces the debt collector to prove their claims in court.

Consumers who understand their rights under the FDCPA and refuse to play the game by the debt collector’s rules gain a huge advantage in the situation.

Corresponding with a debt collector in writing creates a paper trail. Hiring a qualified debt collection harassment attorney creates accountability. Simply waiting for responses from a debt collector creates leverage.

Challenging ARM Solutions

Why Consumers Should Always Dispute a Debt

When a consumer disputes a debt in writing within 30 days of receiving validation of the debt from the debt collector, the debt collector is prohibited from contacting the consumer until they provide verification of the debt to the consumer.

Further, the credit reporting agencies must investigate a debt that a consumer disputes in writing within 30 days of being notified of the dispute. If the credit reporting agency cannot verify the debt with the information provided by the debt collector, the agency must delete the account from the consumer’s credit report.

Given ARM Solutions history of attempting to collect from the wrong consumer, attempting to collect debts that have been discharged in bankruptcy, and refusing to validate debts when requested, the chances that the information on file with ARM Solutions regarding a consumer’s debt is inaccurate or incomplete is extremely high.

Therefore, challenging ARM Solutions on any debt in their portfolio is a sound strategy that may result in having the account completely removed from the consumer’s credit report without making a payment.

In fact, this outcome is not that rare when consumers challenge debts properly with the assistance of a qualified credit repair expert.

The Importance of Professional Help

Consumers who attempt to dispute a collection on their own often find it is a frustrating process that they are not equipped to handle. Debt collectors and credit reporting agencies know all of the deadlines and procedures for disputing a debt.

In addition, they also know the magic words that must be included in a credit dispute letter to force the agency to conduct a reasonable investigation. Further, they know that most consumers will give up after receiving one or two form letter responses from the credit reporting agency in response to their dispute.

Working with a professional credit repair expert evens the playing field. Credit repair experts understand the Fair Credit Reporting Act and the procedures for disputing a debt. They also know the words and language that must be included in the dispute letter to force the credit reporting agency to conduct a reasonable investigation of the debt.

Credit repair experts also know how to follow up on disputes and force the credit reporting agency to continue investigating the debt until it is completely and permanently deleted from the consumer’s credit report.

The purpose of disputing a debt is not to get out of a legitimate debt obligation but to ensure the information on your credit report is accurate, complete, and in compliance with federal and state consumer protection laws. If ARM Solutions cannot verify the information on file regarding a consumer’s debt meets these standards, the account does not belong on the consumer’s credit report and should be removed.

Conclusion

ARM Solutions, like most debt collection agencies, attempts to collect as many debts as possible regardless of the accuracy of the information on file. The regulatory actions taken against the company by the California Department of Financial Protection and Innovation, the federal lawsuits filed against the company for violating the FDCPA, and the patterns and problems experienced by consumers when dealing with the company all point to an agency that places collecting debts over consumer protection.

However, these same patterns and problems also provide consumers with the ammunition they need to challenge ARM Solutions and leverage them to their advantage.

If you are dealing with ARM Solutions over an account they claim you owe, do not attempt to handle it on your own. Instead, contact a qualified credit repair expert who can provide you with the help and guidance you need to navigate the situation successfully.

Contact us today to learn how we can help you fight ARM Solutions.