If you’re finding this article, chances are you just noticed a collection on your credit report from Financial Recovery Services.

Whether you noticed a large drop in credit score, got denied for a loan, or are simply confused about this debt that shows up on your credit report, we can help. You do have control over this situation, even though the collection agency doesn’t want you to know that.

Financial Recovery Services, Inc. (FRS) is a medium-sized debt collection agency. With multiple call centers across the country and a nearshore site, they’ve been around for nearly three decades, so they’ve had plenty of time to amass resources to collect on debts. Let’s go over who they are and how they operate so you can get back in control of your credit report.

Who is Financial Recovery Services?

Financial Recovery Services, Inc. is a private debt collection company. They’ve been in business since March 1996, and were co-founded by CEO and President, Brian Bowers, along with Wade Davis. Here is their basic contact information:

They collect on a variety of debts, including bank cards, retail accounts, installment loans, fintech debts, auto loans, student loans, and utility bills. They are licensed to collect debts in all 50 states, and are primarily regulated by the Minnesota Department of Commerce.

What is Financial Recovery Services’ History?

FRS is affiliated with a couple of industry associations, including ACA International and the Receivables Management Association International, but what does their actual consumer history look like?

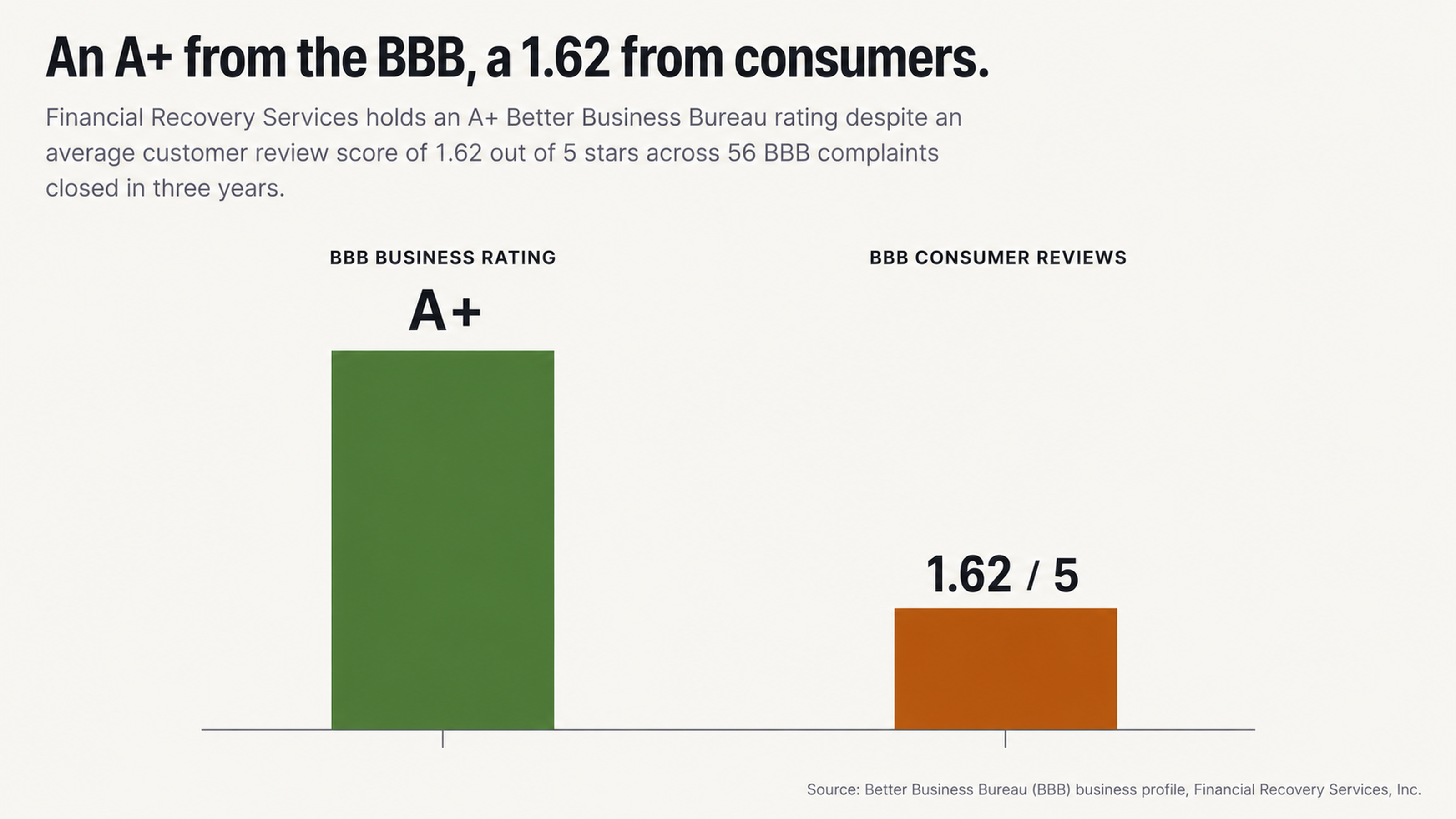

They have been defendants in roughly 390 federal court cases, mostly Fair Debt Collection Practices Act (FDCPA) lawsuits. On top of that, they have a strange disconnect between their Better Business Bureau (BBB) rating and reviews. Despite having an A+ rating with the BBB, they only have an average review score of 1.62 out of 5 stars.

In fact, according to the BBB, they have had 56 complaints closed against them in the past 3 years, with 26 of those being within the past 12 months alone.

These complaints are all relatively similar. They claim that FRS uses aggressive collection practices. One consumer named Karla A. wrote on the BBB in February 2025:

“I’m getting multiple calls a day for months on end now saying I owe thousands of dollars from over 20 years ago on a $100 payday loan that I already paid off. The calls just won’t stop. I have a traumatic brain injury. I’m going crazy with them calling from 6:30 am to 10:00pm, 7 days a week.”

Why is Financial Recovery Services on my Credit Report?

How do they get my Debt Information?

FRS collects debts as both a third-party debt collector and a debt buyer. They’ll collect debts from the original creditor for a fee or commission and sometimes, they buy debts at a discount and then become the creditor. When they purchase debts, they take ownership of them.

There is a risk for consumers when debt buying is involved. When debts are sold from collector to collector, documentation gets lost, and information gets distorted. This makes it easy for them to sue for a debt they have no proof you owe.

FRS is not a scam; it’s a real collection agency. However, being a real collection agency doesn’t make them nice. They call, harass, and abuse until you pay. Their job is to get money from you, even if it isn’t owed.

What is the effect on my Credit Report?

This is where FRS collection accounts can be damaging. A collection on your report can lower your credit score by over 100 points. It can also disqualify you from credit cards, loans, mortgages, and sometimes even apartments. Some employers will even use your credit report when making hiring decisions.

These accounts can stay on your report for 7 years, starting from the original delinquency date. This date will not be reset if you make a payment or if the debt is sold to another agency. If you do nothing, it will still be on your report.

That’s why it’s so important to understand that your end goal should be the removal of the tradeline, not just settling the debt. Your credit report will affect you for years to come.

Should I Pay Financial Recovery Services?

What happens when I Pay FRS?

Paying FRS does not mean they will remove the negative mark from your report. In fact, once paid, the account will show as a paid collection on your report. While this is somewhat better for your credit score, it still has a negative effect.

According to FICO’s credit scoring model, paid collections still affect your credit score. Although, there are some scoring models that ignore paid collections, such as FICO 9 and VantageScore 3.0.

Sometimes, making a payment on an old debt can even reset the statute of limitations, making it a collectible debt again. This is something you want to avoid, so contact an expert if you have an old debt.

Pay for Delete

You may have heard of the term pay for delete. This is where you negotiate the removal of the debt from your report in exchange for payment. This sounds nice, but it isn’t always as great as it seems.

The credit bureaus have an agreement with collection agencies that doesn’t allow the deletion of accurate information for payment. If you negotiate a pay for delete agreement, the agency may not follow through with their end of the bargain. The pay for delete approach also validates the debt, eliminating future dispute options.

Even if they do, you are validating the debt by paying it. Once you’ve paid, you will not be able to dispute it moving forward. It’s best to avoid paying until you have a solid plan.

Why to Dispute Instead of Pay

Inaccuracy of Credit Reports

Credit reports are far from perfect. In fact, research by U.S. PIRGs found that 79 percent of credit reports contain some kind of error or serious error. This could be anything from an incorrect balance to debts in the name of another person who happens to share your name.

One of the reasons that collection accounts, in particular, contain such a high rate of error is the way that debts are sold.

When FRS buys a batch of collection accounts, it is typically given a data file. This data file might be several years old and may have already changed hands multiple times. Often the account numbers have gotten transposed, the balance includes fees that were never properly disclosed, and debts have gotten assigned to the wrong person altogether.

That’s why it’s so important to dispute collection accounts like those from Financial Recovery Services. For example, on the CFPB Consumer Complaint Database, there are currently about 50 complaints against FRS, going back to March 2015. Many of those complaints include allegations of misrepresentation or false or deceptive practices.

Here’s what one consumer who left a review for FRS on the Consumer Affairs website wrote about trying to get the company to validate a debt:

“They have failed to provide me with any information that I requested, despite my repeated requests going back several months.”

Many reviewers reported similar experiences when trying to get debt validation.

Verification of Debts

Under the Fair Credit Reporting Act, when you dispute something that’s on your credit report, the credit reporting agency must conduct an investigation. Part of that investigation includes requiring the company that made the report — the data furnisher — to verify that the information is accurate.

If the data furnisher cannot verify the debt, then the item has to be deleted from your report. (This is one reason that it’s always a good idea to dispute legitimate debts that you know you owe. The furnisher may not be able to verify them, and they’ll be removed from your report.)

The debt-buying model actually works in consumers’ favor here because FRS and similar collection agencies often can’t verify the debts they are collecting upon. When they buy debts that are several years old, for example, they often don’t get copies of the original contracts. They may not have a record of your payments or any communication that you had with the original creditor. And they certainly don’t have proof that they own the debt. They may just have an Excel spreadsheet with your name and a balance due on it.

But that’s not enough to prove the debt is really yours.

Here’s how one reviewer for ComplaintsBoard summed up the experience of trying to get FRS to verify a debt:

“I asked for them to send information about what they are reporting to me because it sounded like a scam and its been well over 6 months and not one thing is sent to me. Either the company is a scam company or they have the WORST business ethics known to man.”

their Better Business Bureau (BBB)

Tips for Interacting with a Collection Agency

Control Information

When a debt collector calls you, he has some information about you. He has your name, maybe your address and phone number, and maybe some details about a debt that you owe. But you have information that he needs, too. And it’s up to you to protect it.

Remember that anything you say to a debt collector can and will be used against you. That includes confirming your identity, admitting that you owe the debt, and giving details about your finances. So even though it’s really tempting to call a debt collector back when you get a letter, don’t. At the very least, don’t give him any information over the phone. (In fact, it’s a good idea to hang up the moment you realize who’s calling.)

One reviewer on the BBB website reported this interaction with an FRS debt collector:

“I would not verify my social for them and asked for what company they were trying to collect a debt for. He said he would not tell me until I verified the last four of my social.”

Don’t fall for it. You don’t have to give a collector your Social Security number, especially not before he’ll tell you what debt he’s calling about.

Know Your Rights

If you do wind up on the phone with a debt collector, understand that you have rights. For example, you can tell a debt collector to stop contacting you entirely. You can also request that he send you written verification of the debt within 30 days of the initial contact.

Financial Recovery Services has been sued multiple times over its communication tactics. For example, multiple consumers reported that the company contacted them about debts that they owed under their maiden names, debts from time periods when they didn’t live in the area the debt was from, and even debts in the names of deceased family members.

Here’s what one reviewer named Charlene S. wrote on the Consumer Affairs website:

“My mother died about 10 years ago and we had closed all of her credit cards and debit cards before she died. I’m getting calls from these people.”

Why You Need Professional Help with a Credit Dispute

Credit Report Disputes Are Complicated

One reason that consumers have a hard time disputing debts on their credit reports is that the process is technical. You have to word your dispute letter just right and send it to the right place. And then you have to follow up in the right way if the credit reporting agency doesn’t make the changes you request.

Financial Recovery Services knows how to work the system. For example, the company successfully defended itself against two appeals in federal court. In Taylor v. Financial Recovery Services, the Second Circuit Court of Appeals and in Jewsevskyj v. Financial Recovery Services, the Third Circuit Court of Appeals, the company demonstrated that it understands the technical requirements of debt collection law and structures its practices accordingly.

If you try to dispute a credit report on your own and aren’t familiar with the law, it’s easy to make a technical mistake that causes your dispute to fail, even if it has merit. A professional credit repair company helps you avoid those mistakes so you have the best chance of removing the items you’re disputing.

Getting Professional Help Levels the Playing Field

When a debt collector is contacting you, you’re at a disadvantage. The debt collection agency has a lot of power and probably knows more about your debt than you do. But if you hire a professional credit repair company to help you with the dispute process, you can level the playing field.

Instead of a giant debt collector pushing around a consumer who doesn’t know her rights, you have two equals facing off. And often, debts that can’t be verified or are inaccurate won’t survive a professional credit repair dispute.

FRS has been sued successfully by consumers in at least 390 cases in federal court. That means that regular people just like you have been able to navigate the system successfully and fight this debt collection agency. With professional representation, you can do the same thing without having to become an expert in federal debt collection law yourself.

Bottom Line

FRS may have a good rating with the BBB, but its low consumer rating and history of complaints to the Consumer Financial Protection Bureau tell a different story. This is a company that consumers distrust and that has a history of problems.

Still, FRS has nearly three decades of experience as a debt collection agency. It’s not going anywhere anytime soon. So if you find yourself facing a collection account from Financial Recovery Services on your credit report, don’t panic. You may be able to get it removed, especially if it’s not your debt or the amount is not accurate.

So always dispute first and never send a payment without investigating first. That’s the best way to protect yourself and your credit report.

Defend Yourself Against Debt Collectors

You have the right to accurate credit reporting. And if a debt collector violates your rights or tries to collect an invalid debt, you have recourse.

At FightCollections.com, we will fight for you to defend your credit report against collections agencies. Start with a free consultation today to go over your credit report and talk about your options.