When you pull your credit report and see a new listing on your credit report, you wonder who P&B Capital Group is. You don’t remember them. You don’t have a credit account with them. You’ve never even heard of them.

What happens next is a familiar story for thousands of Americans every year. A debt collector shows up on your credit report. You didn’t know who they were until now. They’re hurting your credit score. You need to get rid of them. They’re calling you and sending letters. You want them to go away.

That’s what they’re counting on.

Who is P&B Capital Group?

P&B Capital Group, LLC is a debt collection agency located in West Seneca, New York. They have been in business since 2004, and they collect consumer debt. Their principals are Sean J. Welch and Ryan Kazmark.

Here’s what you need to know about them:

What We Found

We did some digging to learn more about this debt collection agency. Here’s what we found:

Over 90 federal lawsuits. Almost all of them were for violating the Fair Debt Collection Practices Act (FDCPA). Some were filed in individual court districts, and others were class actions.

145 complaints in the Consumer Financial Protection Bureau (CFPB) database. 92% of them were for debt collection. Many were complaints about them trying to collect a debt the consumer didn’t owe. Others were for harassing phone calls or not validating the debt. Some consumers claimed they were threatening to sue when they couldn’t legally do that.

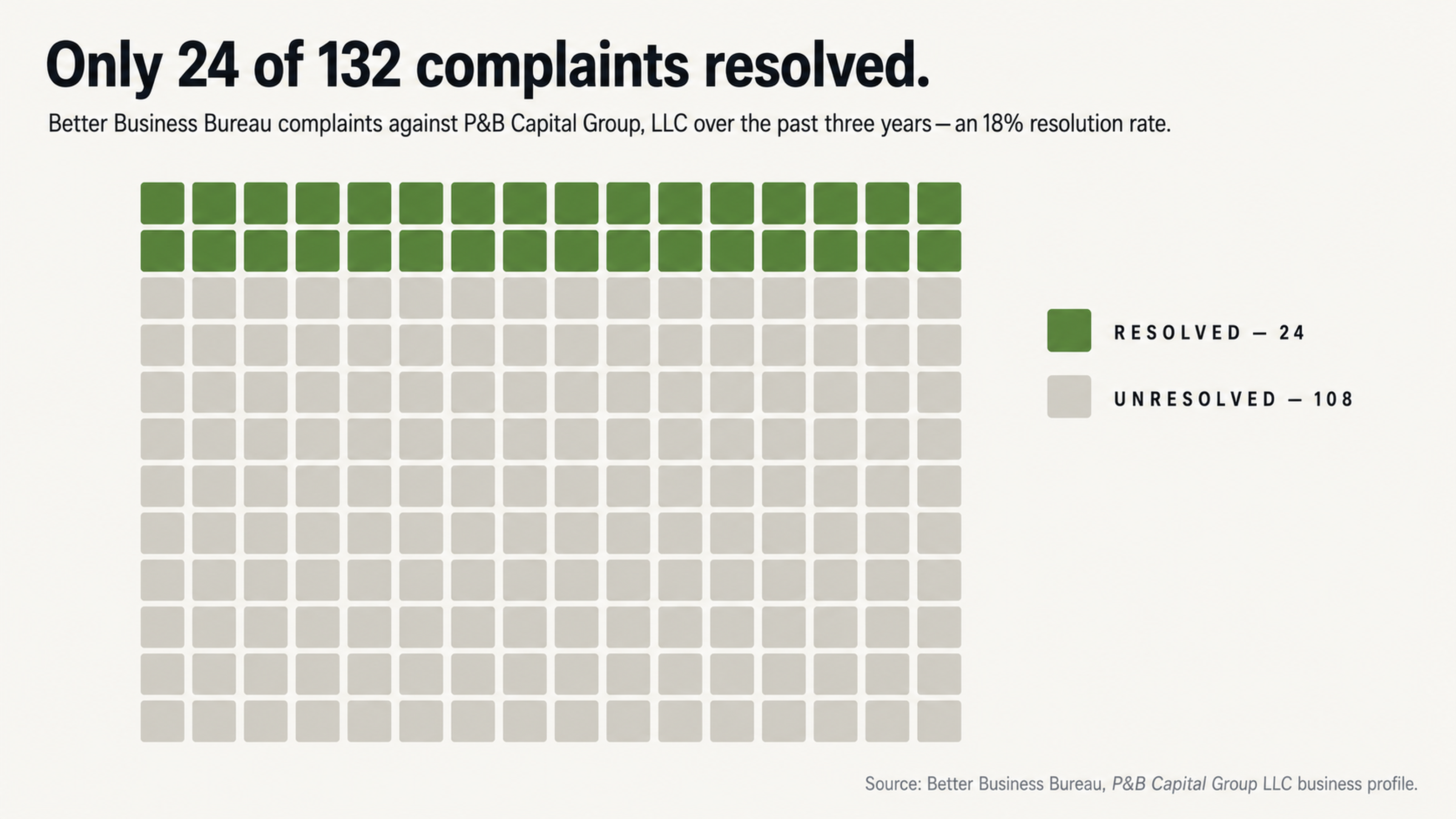

Better Business Bureau (BBB) rating. The company claims to have a good rating with the BBB. Actually, their rating is a B. In the last three years, there have been 132 complaints filed against them. Only 18% of them were resolved successfully. If they were truly concerned about their customers, they would have resolved a lot more than 18%.

Why Is P&B Capital Group on My Credit Report?

They Buy Debt and Try to Collect

P&B Capital Group doesn’t lend money. They buy it. When you miss payments to the original creditor (like a credit card company or medical provider), they might decide to sell your debt to a collection agency. Debt buyers pay just pennies on the dollar for it. They might pay three to five cents for every dollar of the debt. So, if you owed $1,000, they would pay $30-$50 for it. Then, they would try to collect the full $1,000 from you.

Their profit is the difference between what they paid for it and what you pay them. That’s why they do what they do. The problem is that the debt has been sold at least once. Sometimes, it’s been sold multiple times. Each time it’s sold, the documentation might get lost or the details might get mixed up. The collection agency might not have all the information about your original debt.

Are They Affiliated with Landmark Strategy Group?

Yes, P&B Capital Group has a sister company called Landmark Strategy Group. It’s a passive debt buyer, also based in West Seneca. The same people own and manage both companies. Landmark buys portfolios of non-performing debt, then P&B tries to collect it.

This is called vertical integration. They’re making money twice, once when they buy your debt and again when they collect it. There’s no third party verifying that what you owe is accurate. The company buying it and the company collecting it are the same.

That’s why you can’t always trust the information they have.

Why You Shouldn’t Pay P&B Capital Group Directly

You Still Have a Collection Account on Your Report

A lot of people think that if they pay a collection account, it will be deleted from their report. That’s not true. When you pay it, the status will change from “unpaid collection” to “paid collection.” However, it will still be on your report for as long as seven years dating from the original delinquency date.

Paid collections can still hurt your credit score. Future lenders will still see that you had an account go to collections. Although some credit scoring models now treat paid collections better than unpaid ones, the negative impact might already be done. The account is still listed on your report, and that’s hurting your credit.

In some states, when you make a payment on an old debt, the statute of limitations clock starts again. This can give the collection agency a few more years to sue you for the debt. So, making a payment might not fix the problem like you think it will.

Goodwill Letters and Pay-for-Delete Don’t Work

Some people try to negotiate with collection agencies. They send goodwill letters asking the agency to remove the account if they pay it. Others try to negotiate a pay-for-delete. The collection agency will supposedly remove the account from their report once the consumer pays.

In reality, collection agencies rarely agree to these terms. Their entire business model is based on putting accounts on your credit report. When they remove one, they’re giving up their leverage for all the consumers out there who see the agency on their report and feel pressured to pay. There’s no incentive for them to create a policy where payment means the account gets removed.

Instead of spending time writing goodwill letters and asking for pay-for-delete, there’s something better you can do.

Why P&B Capital Group Debts Can Be Removed

Most Credit Reports Contain Inaccurate Information

A study from U.S. Public Interest Research Groups found that 79 percent of credit reports contain errors or grave inaccuracies. This isn’t a simple typo in your name or address. This is accounts that don’t belong to you, balances that aren’t correct, dates that are wrong, or the same debt listed multiple times. The credit reporting system is broken, and that works to your advantage when you know how to exploit it.

When a debt is sold from an original creditor to a debt buyer to a collection agency, the chance of something going wrong expands exponentially. An account number gets entered wrong. A name gets misspelled. A debt you paid gets reported as unpaid. The older the debt, the more likely that documentation has been lost or corrupted along the way.

That environment is great for you when you understand how to take advantage of it. Under federal law, a collection agency must validate a debt it reports on your credit. If it can’t, the account must be deleted.

Collection Agencies Don’t Want to Wait

The debt collection business model is simple: Buy debts for pennies on the dollar, then collect as much money as possible in as short a period as possible. That means companies such as P&B Capital Group invest as little as possible in each individual account. After all, if it takes months of time and energy to collect $50, that’s not worth the effort.

This is a vulnerability you can exploit. If you dispute the account and require validation, the collection agency has to decide how much time and energy to invest. Gathering documentation requires employee time, legal review, and communication with previous creditors who may not even have the information anymore.

Every day the dispute remains unresolved costs the collection agency time. Its entire business model is based on consumers who pay up immediately out of fear or confusion. Consumers who know their rights and use them as leverage turn that model inside out.

Mistakes to Avoid with P&B Capital Group

Don’t Give Them Information

If a collection agency contacts you, it’s possible it doesn’t even have your full identity, or maybe it doesn’t know where you work or how much money you have. Every shred of information you provide becomes a weapon it can turn against you. Don’t confirm your Social Security number. Don’t tell it where you’re employed. Don’t discuss your finances. You’re providing it ammunition it didn’t have before.

Information should only flow one way: from it to you. You have the legal right to demand it prove you owe the debt. You have no obligation to help it make its case. Keep your data footprint as small as possible.

Several reviewers on Consumer Affairs complained about P&B Capital Group calling family members and revealing details about their personal life. The more information you provide, the easier it is for the agency to pull that stunt.

Don’t Call the Collection Agency Directly

It’s tempting to see an unknown collection on your credit report and immediately dial the phone number to demand answers. That’s exactly what the collection agency wants. Phone calls are not recorded. Anything you say can be twisted to acknowledge that you owe the debt. Oral agreements are not written down.

More importantly, calling directly puts you in a purely reactive mode. Trained collection agents know how to create a sense of urgency, how to manipulate your emotional response, and how to use that pressure to get you to agree to something — a payment, an admission of guilt, anything — you’ll regret later.

One CFPB complaint includes a representative from P&B Capital Group threatening to sue before the consumer could finish requesting debt validation, then hanging up the phone.

All communication should be in writing. That creates a paper trail. It allows you to think carefully about what you want to say. And it completely neutralizes the kind of pressure tactics collection agencies like to pull on the phone.

Why You Need a Credit Repair Expert

Asking for Validation Costs the Collection Agency Money

Federal law allows you to request validation of any debt a collection agency says you owe. When you do that, the agency must gather all documentation proving not just that you owe the debt but that the amount is correct and that the agency has the legal right to collect it. That takes time. It takes employee hours. And it may involve records the agency doesn’t actually have anymore.

A credit repair expert knows precisely what to ask for and where to look for holes in the collection agency’s documentation. And an agency won’t invest more money in validating a debt than the debt is actually worth. So if you owe $500 and it’s going to cost the agency $1,000 in legal fees and employee salary to validate it, the agency will just let the debt go. It’s not worth the effort.

That’s why disputing works. It forces the collection agency to decide whether you’re worth the investment of time and resources.

Multiple Disputes Won’t Harm Your Credit Report

Some consumers worry that disputing a debt (or having a professional help you dispute it) will somehow harm their credit report. That’s just not true. The credit bureaus are required to investigate any dispute you file, and the simple act of disputing something does not affect your credit score one way or the other.

Having a professional conduct a thorough investigation of multiple accounts — even if they all deal with the same original debt — does not create additional problems. In fact, it creates multiple chances to uncover errors, discrepancies, or validation issues.

A collection agency must be able to validate any debt it places on your credit report within a reasonable amount of time. If it can’t, the account must be deleted. That’s federal law. And it applies whether the original debt was legitimate or not.

Conclusion

If you see P&B Capital Group on your credit report, you shouldn’t panic. But you also shouldn’t pay it. P&B Capital Group has been sued more than 90 times for violating federal debt collection laws. It’s racked up 145 complaints through the CFPB’s Consumer Complaint Database and another 132 complaints through the BBB, where it has a rating of 1 out of 5 and a resolution rate of just 18 percent.

That tells you this agency has a history of issues and that you can use that to your advantage. Collection agencies make money off consumers who are confused or frightened. It needs consumers who don’t know their rights and who immediately pay any collection account they see without asking questions. That benefits the collection agency. It does nothing for you except put money in someone else’s pocket for a debt you may not even owe.

The better move is to dispute the account and make the collection agency prove that you owe it. Any account with an inaccuracy, any account without proper documentation, and any account the collection agency cannot validate within a reasonable amount of time must be removed from your credit report. And given the frequency of errors in this industry, those odds may be better than you think.

What to Do Next

So what should you do if you see P&B Capital Group on your credit report? The worst thing you can do is nothing. The second worst thing you can do is pay it without first determining whether the account is accurate, whether it has the proper documentation, and whether the collection agency can legally collect it.

Working with a credit repair expert who understands the dispute process and who understands how to navigate the tricky and technical world of federal debt collection law gives you the best chance of getting an inaccurate or unverifiable account removed from your report.

You deserve a credit report that accurately reflects your history and your choices, not one that’s polluted by errors and potentially predatory practices.

Contact FightCollections.com today to explore your options. Our experts specialize in pushing back against collection agencies and helping consumers just like you reclaim their credit reports. The consultation is free, and you’ve got nothing to lose.