Does Alliance Collections keep appearing on your credit report, and are you worried about how it will impact your credit score?

Take a deep breath; this is exactly what debt collectors hope for. They want you to be concerned and frightened. They want you to pay whatever amount is on the screen as soon as possible. They thrive on your anxiety and confusion.

Alliance Collections is a Wisconsin-based debt collection agency that collects medical debts. They assume that once you see their name on your report, you will either pay them right away or wait for the negative report to remain on your report for 7 years. Both scenarios work in their favor.

What they do not expect is that you will know your rights, that you will know how to dispute the report, and that you will take action immediately.

If you know your rights and the appropriate steps to take, this is all the leverage you need. Debt collectors take advantage of consumers who do not know their rights and how to use them. If you do not know how to proceed, debt collectors are winning.

In this article, we will review what you should know about Alliance Collections. We will also walk you through the steps you can take to dispute their claims if you find any inaccuracies on your report.

Who is Alliance Collections?

Alliance Collection Agencies, Inc. is a debt collection company that was formed in 1999 through merger of three predecessor agencies dating to the 1950s. It is currently based in Marshfield, Wisconsin.

What we found

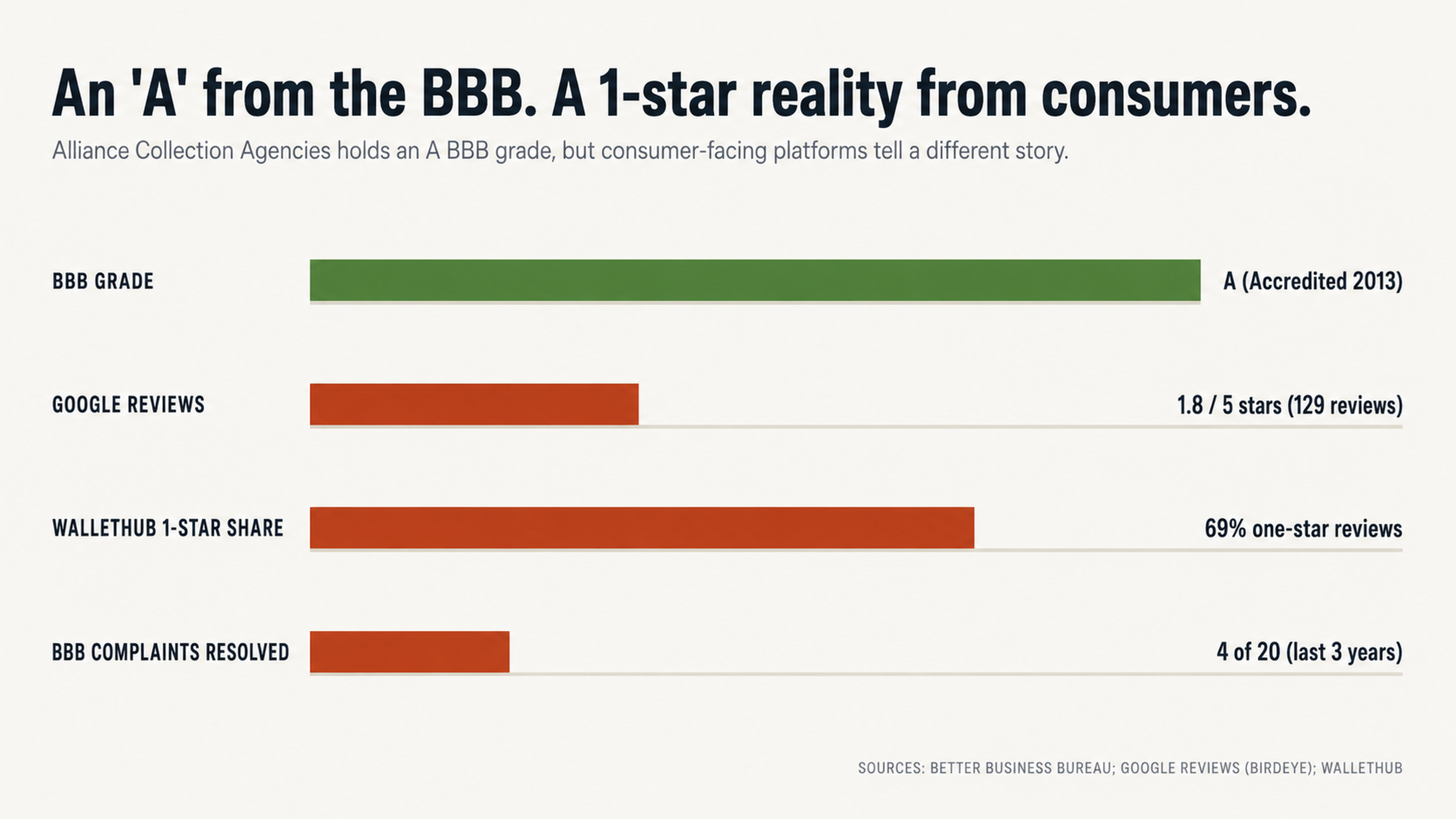

Alliance Collections is also known as RevCycle, Inc. and primarily deals with medical collections. The company president is Dan O’Connell, while the Co-President is Brent Bergman. The Chief Compliance Officer and General Counsel is Edwin Herbert. Alliance Collections is accredited by the BBB and has a rating of A.

Despite their good rating with the BBB, Alliance Collections has had at least 6 federal FDCPA lawsuits filed against them since 2008. In 2017, 2 of these lawsuits were class action suits.

The 2017 class action lawsuit Niland v. Alliance Collection Agencies (Case No. 2:17-cv-00722) alleged that the company was using deceptive language in their collection letters, affecting consumers in Wisconsin. The second 2017 class action against Alliance, Maloney et al. v. Alliance Collection Agencies (Case No. 2:17-cv-01610-NJ), involved three plaintiffs who alleged receiving multiple collection letters with conflicting balance information.

Alliance Collections is licensed to collect debts in all 50 states. They have a Nevada Collection Agency License with number CAD11576.

On review platforms, however, consumers rate Alliance Collections poorly. On Google Reviews (via BirdEye), they have an average rating of 1.8/ 5 stars, based on 129 customer reviews. On WalletHub, 69% of the reviews are 1-star reviews.

Why you should not pay them immediately

The truth is that debt collectors such as Alliance Collections operate on a very thin budget. They buy debts from the original creditors who have written them off as bad debts. Therefore, when you pay them, you are not paying the original creditor; you are paying Alliance Collections. The original creditor does not benefit from the transaction at all.

This business model works for Alliance Collections because most people pay them when they see their name on their credit report. Most consumers do not question what they see on their report; they just pay. The company also knows that most consumers are afraid of the negative report ruining their credit scores. As such, they rush to pay Alliance Collections.

However, when you pay a collection agency without verifying the information they are reporting, you may end up paying for nothing. Paying a debt collector changes the status of the report from ‘collection’ to ‘paid collection’. This means that the report will still be on your report for 7 years from the original delinquency date.

What they hope you will not find out

What Alliance Collections is hoping you will not find out is that you have the right to dispute any information on your report that you find inaccurate or unverifiable. The debt collection industry survives on the ignorance of consumers. Alliance Collections hopes that you do not know your rights so that they can benefit from your ignorance.

Alliance Collections hopes that you will panic at the sight of their name on your report and immediately pay them without questioning the report. This is their model for making money. They hope that you do not know that paying them may not improve your credit score at all.

If they find out that you know your rights and that you are going to dispute the report, they will back off immediately. This is because disputing a collection account is a legitimate way to get the report removed from your credit report. Most debt collectors do not have the necessary documentation to verify the debts they are collecting. Without documentation, the credit bureaus cannot verify the debt, and they have to remove it from your report.

Why this information is not available to you

The main reason you may not have this information at your disposal is that debt collectors know more than you do about debt collection laws and credit report information. They know how to negotiate with consumers, how to intimidate them into paying debts they may not owe, and how to communicate with them.

Most consumers do not have this information. They do not know how debt collection works or how to dispute a report. This lack of information is what debt collectors such as Alliance Collections thrive on.

When the information gap is bridged

However, when consumers have the same information as debt collectors, the whole debt collection process changes. Consumers who know their rights and how to dispute reports will not pay debts without proper verification.

In 2017, 2 class-action suits were filed against Alliance Collections. The suits alleged that the company was sending letters to consumers with deceptive language. According to the suits, the letters indicated that consumers had to fill out a financial assessment form to qualify for settlement offers.

In reality, however, the settlement offers were based on how old the debt was and the amount. Therefore, filling out the financial assessment form was unnecessary.

These tactics are typical of debt collection agencies. They use such tactics to deceive consumers into paying debts they may not owe. However, when consumers know their rights and how to proceed, such tactics do not work.

The error on your credit report

It has been reported that 79% of credit reports contain errors or discrepancies. This is a staggering percentage and one that you should take seriously. When you see Alliance Collections on your report, they may be reporting something that is not accurate.

You may not owe them a debt at all. You may not owe them the amount they are claiming. You may not even know what they are talking about.

Whatever the case, you have the right to dispute any information on your credit report that you find inaccurate or misleading. If Alliance Collections is reporting something about you that is not true, you should dispute it immediately.

What you can dispute

You can dispute any information on your credit report that is inaccurate, incorrect, unverifiable, or misleading. You can dispute information about collection accounts, credit accounts you did not open, accounts with incorrect credit limits, accounts with incorrect balances, and more.

According to the BBB, Alliance Collections has had 20 complaints filed against them in the last 3 years. Out of these complaints, only 4 have been resolved to the satisfaction of the consumer. This is not a good record, and it points to a lot of inaccuracies in reporting.

In March 2025, a consumer filed a complaint against Alliance Collections on the BBB platform. According to the complaint, the consumer had been receiving calls and letters from Alliance Collections claiming that she owed them money.

However, when the consumer contacted her healthcare provider, she found out that she did not owe them any money. In fact, her balance was zero. When she requested an itemized statement from Alliance Collections to clarify the debt, she was told to send an email to a specific email address.

Despite sending the email, however, the consumer did not receive a response. Every time she called Alliance Collections, she was hung up on.

This complaint points to inaccuracies in the information that Alliance Collections is reporting. The consumer does not owe Alliance Collections any money. However, they are calling her consistently and asking her to pay a debt she does not owe.

This can happen to you too. Therefore, when you see Alliance Collections on your report, take immediate action. Dispute the report immediately to avoid any damage to your credit report.

The danger of calling Alliance Collections

Every time you call Alliance Collections, you are putting yourself at risk. When you call them, they will record the conversation and use it against you. They want you to admit that you owe them a debt or acknowledge the debt in any way.

A 2008 federal lawsuit against Alliance Collections (Case No. 3:08-cv-00277-slc) alleged that the company called a consumer up to five times per day, used profane and abusive language, threatened to sue and garnish wages, and disclosed debt information to the plaintiff’s co-worker.

When you call them, they may use high-pressure tactics to get you to pay. They may threaten to sue you or harm your credit score further.

Whatever the case, calling Alliance Collections is not a good idea. The best way to handle them is to send them a letter disputing their claims. This letter should be brief and to the point.

Do not admit that you owe them any debt or acknowledge the debt in any way. Simply dispute their claims and let them know that you will not be contacting them again.

The importance of professional help

Disputing Alliance Collections’ claims can be challenging if you do not know what you are doing. Debt collectors are professionals who know how to negotiate and intimidate consumers into paying debts they may not owe. Alliance Collections received a PPP loan of $795,320 during the pandemic, reporting 108 employees.

When you are disputing their claims, therefore, you need professional help. You need someone who understands debt collection laws and how they work.

A professional will help you craft a good dispute letter and send it to Alliance Collections. They will also follow up on the dispute to ensure that Alliance Collections complies with their obligations.

Most importantly, however, a professional will represent you throughout the process. This means that you do not have to talk to Alliance Collections at all. You can avoid their harassment and intimidation tactics and still get the report removed from your credit report.

At FightCollections.com, we understand how debt collectors work and how to dispute their claims. We have helped many consumers dispute Alliance Collections and other debt collectors and can help you do the same.

We offer a free consultation where we will review your case and advise you on the way forward. We will also represent you throughout the process to ensure that your rights are protected at all times.

Contact us today to book your free consultation.

The timeline for removing a collection account

When you dispute a collection account, the whole process should take about 30 days. This is the amount of time that the credit bureaus have to investigate and verify the debt.

When you dispute the debt, the credit bureaus will contact Alliance Collections and request that they verify the debt. If Alliance Collections cannot verify the debt, the credit bureaus will remove the report from your credit report.

The process of removing a collection account from your report, therefore, should not take more than 30 days. However, this is not always the case.

Sometimes, Alliance Collections may dispute your dispute and claim that the report is accurate. If this happens, the credit bureaus may not remove the report from your credit report.

In such a case, you may have to take further action to get the report removed. You may have to file another dispute or take legal action against Alliance Collections.

Whatever the case, however, removing a collection account from your report should not take more than a few months. If it takes longer than this, you may want to consider getting professional help.

Contact us today to book your free consultation.

Conclusion

Alliance Collections may appear on your report as a collection account. When you see them, you may panic and wonder how they will affect your credit score.

Do not panic. Instead, take immediate action to dispute their claims. If they are reporting something inaccurate or misleading, dispute it immediately.

You can represent yourself throughout the process. However, if you do not know how to proceed, consider getting professional help.

At FightCollections.com, we understand how debt collectors work and how to dispute their claims. We have helped many consumers dispute Alliance Collections and other debt collectors and can help you do the same.

Contact us today to book your free consultation.