Key Information About McCalla Raymer Leibert Pierce LLC

Founding Year: 1982 (merged to form the current entity on February 1, 2017)

Managing Partner: Marty M. Stone

BBB Rating: A+ (though not accredited by BBB)

Google Reviews Rating: Approximately 2 stars

Background of McCalla Raymer Leibert Pierce LLC

The firm was initially established in 1982 in Georgia and, through a merger in 2017 with Hunt Leibert Jacobson P.C. (based in Connecticut), it adopted its current name.

It further expanded by taking over the regional offices of Buckley Madole. McCalla Raymer Leibert Pierce LLC now operates across the United States, from New York to California, primarily dealing with foreclosure, bankruptcy, and debt collection practices.

Consumer Complaints Against McCalla Raymer Leibert Pierce LLC

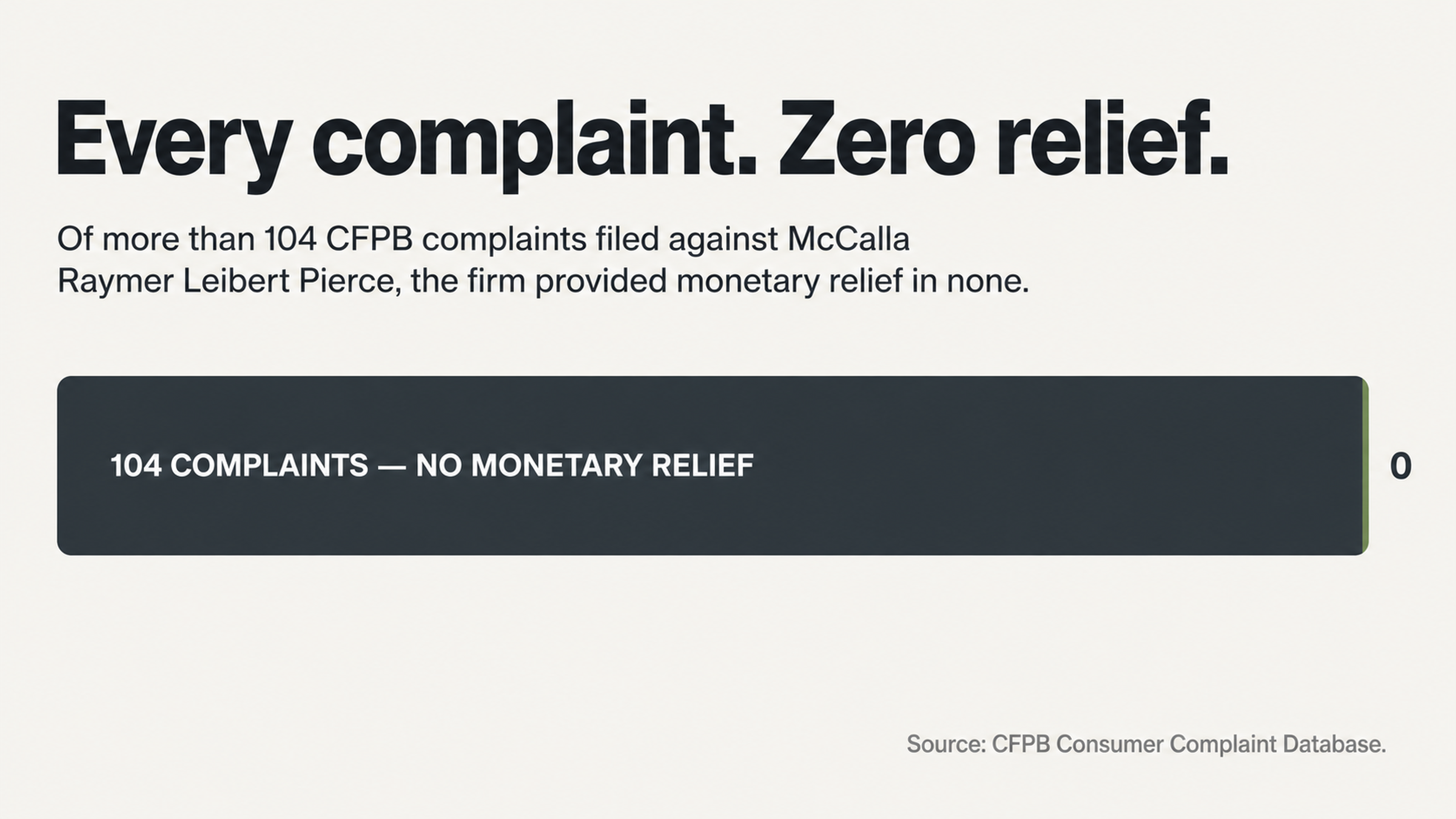

Over 104 complaints have been filed against McCalla Raymer Leibert Pierce LLC with the Consumer Financial Protection Bureau. These complaints include issues related to debt collection practices, foreclosure, and credit reporting errors. In none of the complaints available did the company offer the consumer any monetary relief.

Additionally, the firm was involved in a federal court case, Miller v. McCalla, Raymer, Padrick, Cobb, Nichols & Clark LLC, where in 2000, the Seventh Circuit ruled that the firm violated the Fair Debt Collection Practices Act. The violation was due to a collection letter that failed to properly disclose the amount of the mortgage debt owed.

This court decision established safe-harbor language for mortgage debt collectors, which is still referenced today.

There have also been repeated allegations of the firm retaining surplus funds from foreclosed properties that rightfully belong to homeowners or their estates.

As one complainant stated in a filing with the Better Business Bureau: "I've had funds held up for more than a year because of this law firm. They do not respond in a timely manner. My initial call was met with unnecessary hostility from a secretary who continues to dismiss me when I call and ask to speak with the lawyer who is handling the case."

The Better Business Bureau determined the firm did not make a good faith effort to resolve the matter.

How Credit Reporting Works

Credit reporting is not an impartial process. It is geared towards efficiency rather than accuracy, and understanding how data is communicated from debt collectors to credit bureaus helps clarify why accounts that should not appear on your credit report end up there.

When a mortgage servicer engages McCalla Raymer to collect on a default, the firm reports the account balances, payment history, and collection status codes to the credit bureaus through an automated data feed. The credit bureaus ingest the information with very little scrutiny, because their model requires the fast processing of millions of data points, not careful review of whether those data points are accurate or not.

According to a study by U.S. PIRGs, 79 percent of credit reports contain errors or serious errors. This is not some wild statistic from consumer advocates. This is simply the factual reality of a business model that allows creditor data to enter the credit reporting ecosystem with very little quality control.

The Information Gap That Favors Collectors

Firms like McCalla Raymer have an information advantage over the consumers they are pursuing. They have access to mortgage servicing records, internal case tracking systems, and legal case files. Consumers, on the other hand, are seeing the collection notice for the first time and have no basis for understanding if the information is accurate.

This is by design. The sense of urgency and fear that a collection notice creates is exactly the response that collectors are looking for. When consumers call the firm in a panic and try to resolve the matter as quickly as possible, they almost always give up more than they have to. The best response to that pressure is not to engage in it. It is to calmly and quietly not engage.

Why Paying McCalla Raymer Could Backfire

The Payment Trap Most Consumers Fall Into

The desire to just pay a collection account and be done with it is completely understandable. It is also, in many cases, completely counterproductive. Paying a collection does not make it go away. It merely changes the status of the account from "unpaid collection" to “paid collection," but the account remains on your credit report as a derogatory item for up to seven years.

For a firm whose CFPB complaint record shows zero instances of the company providing monetary relief to the consumer who complained, the incentives here are clear. They benefit from quick resolutions. They have no incentive to make sure the consumer understands the implications of paying the account versus disputing it.

When debt is sold from the original mortgage servicer to a firm that is collecting on it, the paper trail tends to get a little weaker in transit. Payment records become incomplete. The original creditor agreement cannot be found. There are gaps in the chain-of-title documentation. These are not edge cases. They are routine aspects of high volume debt collection, and each gap in the paper trail is a potential avenue for having the account removed.

Why Settlement Is a Gamble You Should Not Take Alone

Settling a debt for less than the full amount owed can go either way. In some cases, a settlement may improve your credit a little bit.

In other cases, it may cause new problems to arise, including the potential that the forgiven debt may be considered taxable income or that the settlement may effectively "re-start" the credit reporting clock on the account. It depends on a combination of factors, including the age of the account, the manner in which the collection is reported, whether the original creditor also updates their records, and how the scoring algorithm interprets the notation.

Without a professional analysis of those factors, consumers are simply guessing in the dark.

How to Get McCalla Raymer Off Your Credit Report

The Dispute-First Strategy

The best way to remove a McCalla Raymer account from your credit report begins with a formal dispute, not a phone call, and definitely not a payment. If a consumer disputes a credit reporting entry through the proper channels, the credit bureau must initiate an investigation. That investigation opens a 30-day timeline for the collector to verify the complete accuracy of everything they have reported.

Here, the operational structure of high-volume law firms works to the detriment of McCalla Raymer instead of to their advantage. A federal bankruptcy judge in Texas issued a 72-page opinion that detailed how the firm's attorneys regularly appeared in court unprepared and unfamiliar with their case files.

The same judge wondered what sort of firm culture would allow attorneys to file false pleadings and then hope the court would just forget about it. If McCalla Raymer cannot manage to maintain their documentation under the scrutiny of a federal court, then the likelihood of their being able to return verifying documentation for every credit report dispute is not very promising at all.

If a collector fails to respond to a credit report dispute inside the allotted 30-day response window, or if the documentation they return contains errors, inaccuracies, or simply lacks necessary information, then the credit bureau must delete the item. This is not a technicality or a loophole; it is the law. The Fair Credit Reporting Act (FCRA) governs credit reporting and outlines the responsibilities of both the bureaus and the furnishers.

Why a Professional Makes a Difference

Do not make your first contact with the collection firm. Before you call them on the phone, respond to a collection letter, or react to any communication you receive from McCalla Raymer, contact a credit repair expert who knows how these firms operate and where their weaknesses are.

Credit repair is a systematic and methodical process that has identified specific soft spots in collection accounts and applies the appropriate amount of pressure in the right places through the correct dispute procedures. Credit repair professionals understand what type of documentation a collection agency must provide, the amount of time they have to do it, and the types of errors or omissions that will force a credit bureau to delete the item.

The history of McCalla Raymer demonstrates why this level of expertise is so critical. McCalla Raymer was at the center of a federal robo-signing scandal in which investigators found that the signature of an attorney on foreclosure documents did not match the man's actual signature, and that a notary seal was applied to a document five weeks before the notary license was issued.

At least eight different people associated with the firm were later identified on published robo-signer lists. These do not sound like the actions of an organization that would keep spotless records.

What McCalla Raymer Is Counting On

The Psychology of Compliance

Collection agencies make their money on the assumption that people will panic when they receive a threatening letter and then simply pay what the collection agency demands. Many consumers view a collection account on their credit report and assume it is legitimate. They assume the amount is accurate. They assume their only choices are to pay or do nothing.

All of those assumptions work in favor of the debt collector, and none of them work in favor of the consumer. McCalla Raymer has 18 offices in 16 states, and it processes cases at an industrial level. That volume is the source of both their income and their liability. When a company is handling hundreds, or even thousands, of accounts every month, mistakes are not a rare occurrence.

They are a statistical certainty. And the consumers who challenge those mistakes are the ones most likely to get results.

The Documentation Problem They Can't Avoid

A different federal bankruptcy court, this one in Alabama, looked at affidavits filed by McCalla Raymer on behalf of Wells Fargo and found a multitude of problems. Some of the affidavits had signatures that weren't dated. Some had the wrong name or title for the person who supposedly signed it. Some had attachments that were added to the document after it was signed.

In one case, an affidavit dated Aug. 25, 2004, stated that a Sept. 1, 2004 mortgage payment was delinquent. That is a statement of fact about something that hadn't yet occurred, contained in a sworn affidavit filed with a federal court.

These are all facts contained in the public record of a federal court proceeding. They point to a history of prioritizing speed and volume over the ability to produce documentation that will stand up to scrutiny.

When that same prioritization is applied to data reported to the credit bureaus, consumers who request verification are pushing against a weak point.

Conclusion: Your Credit Report Is Not the Final Word

A credit report entry from McCalla Raymer Leibert Pierce LLC is a data point. It is not a finding. It can be disputed. It can be investigated. And if the documentation for it cannot meet the verification requirements of federal law, it can be deleted.

This is a company with a history of answered CFPB complaints offering no monetary relief, a landmark FDCPA violation finding, robo-signed foreclosure documents, and a federal judge questioning the accuracy of their court filings. None of that history goes away when they report a debt to a credit bureau. But it is all context that you should keep in mind.

Get Started With FightCollections.com

At FightCollections.com, we know where the soft spots are in collection accounts, and how to build a dispute that puts the burden of proof back where it belongs: on the debt collector. We do it through a methodical process that is guided by the same federal laws that courts have already used to find this company liable.

If you have a credit report entry from McCalla Raymer Leibert Pierce LLC, contact FightCollections.com today for a free consultation. Let us go over your situation, evaluate the debt, and decide on the best course of action.

The worst thing you can do is nothing. The second worst thing you can do is try to handle it on your own.