Understanding who Medical Data Systems is and how they operate is the first step in addressing an unfamiliar collection account on your credit report.

What Is Medical Data Systems?

Medical Data Systems, Inc. is a debt collection agency based in Florida that specifically deals with medical debt collections. It operates under the trade name Medical Revenue Service and has been in the business of collecting medical debts since 1985.

Here is the basic information about this debt collection agency:

Medical Data Systems Consumer Complaints

Despite being in business for almost four decades, Medical Data Systems has a history of consumer complaints that indicate deeper issues. Over 1,233 complaints have been filed against the company with the Consumer Financial Protection Bureau, making it one of the most complained-about medical debt collection agencies on federal records.

Adding in complaints filed with the Better Business Bureau (BBB), the number of complaints against the company tops 1,500.

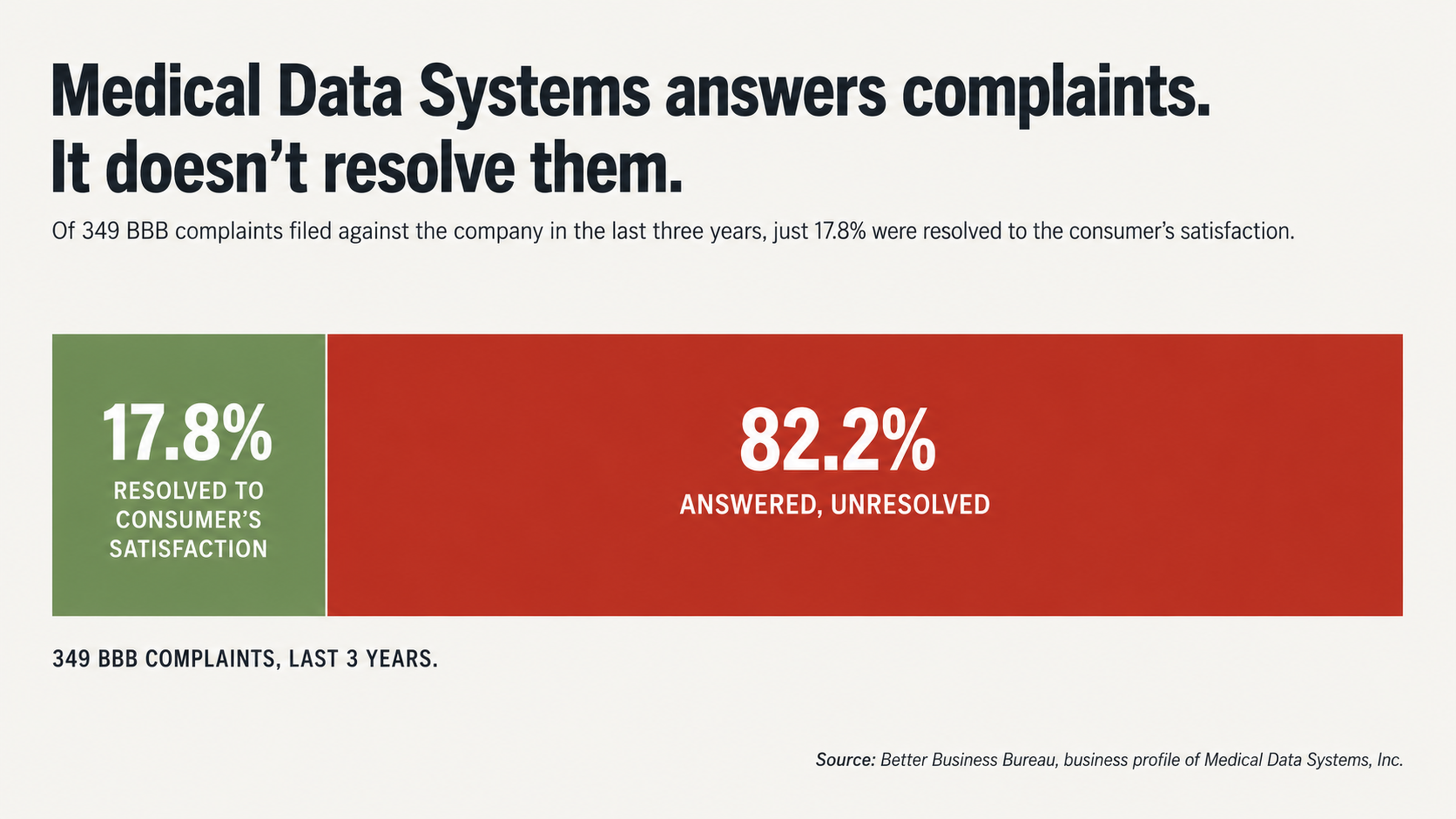

The BBB has issued a formal pattern of complaints notice against Medical Data Systems. This means that the bureau has noticed a pattern of complaints against the company that have not been satisfactorily resolved. Of the 349 complaints filed against the company with the BBB in the last three years, only 17.8% have been resolved to the satisfaction of the consumer.

Over 180 federal lawsuits have been filed against the company for violations of the Fair Debt Collection Practices Act (FDCPA). In some cases, the company has attempted to collect debts that are past the statute of limitations or debts that have already been discharged in bankruptcy.

This history of lawsuits against the company means that it may still be facing legal liability for its debt collection practices.

Why a Medical Debt Collection Shows Up on Your Credit Report

How Medical Debt Gets Assigned to Collection

To understand how a medical debt collection ends up on your credit report, it helps to understand how medical debt gets assigned to a collection agency. If you do not pay a medical bill, the hospital or medical provider may wait 90 to 180 days before assigning the debt to a collection agency.

During this time, you may not receive a bill because the hospital has an incorrect address for you or because of a dispute over insurance coverage. Alternatively, the hospital may have made a clerical error and never sent you a bill.

Medical Data Systems represents more than 600 health care providers across the United States. When a hospital assigns your debt to MDS for collection, the collection agency only receives the information that the hospital provides. In many cases, the information that hospitals provide to debt collectors is incomplete and may contain errors relating to the patient’s identity, billing codes, or amount owed.

A study by U.S. PIRG found that 79% of credit reports contain errors or other serious mistakes. Medical debt is particularly susceptible to errors because of the complexity of the health care billing process and the procedures used for processing insurance claims. The information on your credit report may not accurately reflect what you owe.

According to complaint data that patients have filed against Medical Data Systems with the Consumer Financial Protection Bureau, the information on your credit report may not even be consistent across the three major credit reporting bureaus.

One complainant reported that MDS was showing the same debt as being closed on their Experian and Equifax credit reports, but showing the debt as still open on their TransUnion credit report. Inconsistencies like these can provide you with ammunition to dispute a medical debt.

Information Asymmetry

When you are contacted by a collection agency over a medical debt, you are at an informational disadvantage. The debt collector has access to information about your debt that you may not have, including your billing records, collection software, and attorneys. This information asymmetry allows a debt collector to make claims about a debt that you cannot easily verify or dispute on your own.

The pattern statement that the BBB has issued against Medical Data Systems particularly notes consumers who have requested proof of a debt from the company and received nothing in response.

One consumer who filed a complaint against the company with the BBB reported: “I have attempted to dispute this account with the credit bureaus multiple times, yet Medical Data Systems continues to verify and report information that is incomplete, inaccurate, and unverifiable.” This experience is not unique. Many consumers have reported similar experiences.

Disputing a medical debt collection or verifying its accuracy requires specialized knowledge of the Fair Credit Reporting Act (FCRA) and the Fair Debt Collection Practices Act (FDCPA). There are nuances to the law and strategies for disputing a debt collection that a professional will understand, but which are not intuitive to the average consumer.

Why You Should Not Pay a Medical Debt First

The Psychology of Debt Collection

Debt collection agencies understand that consumers will be more likely to pay a debt if they are under pressure and fearful. This is why a collection agency may contact you about a surprise medical bill as soon as it appears on your credit report. The agency understands that you are concerned about the impact of the debt collection on your credit score and your ability to obtain a loan or credit in the future.

One reviewer on the BBB website described the tactics that Medical Data Systems used in attempting to collect a debt from her: “Scam. My debt was paid in full and then I received a surprise medical bill from you people with ONE MONTH to pay it. They even told me I had another bill which I never knew existed and wanted me to pay all of this over the phone. Denied mailing proof of legitimacy, denied mailing a paper bill so I could keep it on file.”

Instead of paying, the consumer recognized the tactics that the debt collection agency was using and refused to engage with the company.

It is natural to want to pay a medical debt as soon as possible to make the problem go away, but this may not be the best strategy. Paying a medical debt will not remove the debt collection from your credit report. Instead, the status of the debt collection will be updated to show that the debt has been paid, but the negative information will remain on your credit report for up to seven years.

The Pay-for-Delete Fallacy

Some consumers believe that they can negotiate a pay-for-delete with a debt collector in which they offer to pay the debt in exchange for the debt collector removing the information from their credit report. In reality, a pay-for-delete agreement rarely works as promised. A debt collector is under a legal obligation to report accurate information about your accounts to the credit reporting bureaus and is unlikely to agree to delete a debt collection account.

Even if a debt collector verbally agrees to a pay-for-delete, the agreement can be difficult to enforce. In most cases, the debt collection will remain on your credit report for the full seven years, even if you pay. You will have paid money for a debt collection that may have been disputable, but you will not reap any of the promised credit benefits.

Instead of negotiating a pay-for-delete, the better strategy is to dispute the accuracy and verifiability of any information that a debt collector reports to the credit reporting bureaus. You can have a debt collection removed from your credit report if you dispute information that a debt collector reports and the debt collector cannot verify the information.

Your Legal Rights When a Debt Collector Contacts You

Strategic Silence

Under federal law, you have the right to stop communications from a debt collector entirely. You do not have to respond to a debt collector’s letters or return the debt collector’s calls. Ignoring a debt collector is not rude or irresponsible. It is a legal right that Congress built into the FDCPA to protect consumers from harassment.

If you talk directly to a debt collector on the phone or engage in a conversation by mail or email, anything you say can be used against you. If you acknowledge that you owe a debt or provide a debt collector with personal information, you are giving the debt collector more ammunition to use against you if there is a subsequent dispute over the debt.

By remaining silent and refusing to engage with a debt collector, you preserve your options and do not give the debt collector any additional ammunition to use against you.

In testimony before a federal court in the case of Carn v. Medical Data Systems, an executive with Medical Data Systems testified that the company may hold onto debts for years without attempting to collect them and has no intention of filing a lawsuit against consumers.

This testimony indicates that a debt collector that contacts you over the phone may actually be bluffing and has no intention of filing a lawsuit against you.

Why Debt Collectors Rarely Sue Consumers

The Cost of a Lawsuit

Before a debt collector decides to file a lawsuit against a consumer, it conducts a cost-benefit analysis. For most consumers, the cost of filing a lawsuit and hiring an attorney far exceeds the amount of the debt that the consumer owes. Most medical debts are too small for a debt collector to file a lawsuit.

Like most debt collection agencies, Medical Data Systems operates on thin margins. The company’s business model depends on collecting as many debts as possible without expending the resources to file a lawsuit. While over 180 federal lawsuits have been filed against Medical Data Systems for violations of the FDCPA, the company attempts to collect thousands of debts every year. In the vast majority of cases, the company does not file a lawsuit.

If you understand that the economics do not make sense for most debt collectors to sue consumers over a medical debt, you do not have to be afraid of a debt collector’s threats. The language that a debt collector uses in its letters and on the phone is intended to create a false sense of urgency and get you to pay a debt as soon as possible. In reality, the likelihood that you will be sued over a medical debt is low.

According to data from the federal courts, Medical Data Systems has been sued by consumers far more often than it has filed lawsuits against consumers. This is consistent with the business model of most debt collection agencies, which prefer to be plaintiffs in the court of public opinion rather than in a court of law.

Disputing a Debt Collection

Why You Should Dispute Before You Pay

The best strategy for any debt collection is to dispute the information that the debt collector reports before you pay. This is because credit reporting mistakes are common and debt collectors frequently lack the documentation that they need to verify the debts that they attempt to collect.

If you initiate a dispute, the credit reporting bureau has 30 days to investigate. If the collection agency cannot verify the debt and provide documentation to support its claims, the bureau must delete the debt collection from your credit report.

Given the problems that consumers have reported with documentation in complaints to the CFPB about Medical Data Systems, you may find that the company cannot verify a debt and must delete the information from your report.

One consumer filed a complaint against Medical Data Systems with the CFPB and reported: “They continue to report to credit bureau after admitting to a CFPB complaint they didn’t have any documentation and would seek it from the hospital. It’s a bogus debt. They have ignored both dispute and validation letters I sent.” This consumer’s experience suggests that MDS may have a vulnerability when it comes to verification that you can exploit with a well-executed dispute strategy.

The Importance of Professional Help

Your first point of contact should never be the collection agency. Before you have any contact with the agency, consult with a professional credit repair expert who can provide you with a strategy for how to respond. A professional understands the technicalities of the FCRA and FDCPA and how they apply to your case.

There are strategies and procedures buried in the FCRA and FDCPA that a professional will understand but that you may not be aware of. What may seem like a simple dispute may involve technical landmines that you do not anticipate but that a professional will know how to avoid.

Medical Data Systems has a history of failing to verify debts when consumers challenge them to do so. Fully 82.2% of the complaints that consumers have filed against the company with the BBB were answered but not resolved to the satisfaction of the consumer. This suggests that the company’s responses to consumers are often inadequate and that consumers may need professional help to respond adequately.

One consumer left a review of Medical Data Systems on Google in which she reported that in February 2024, she set up a payment plan with the company. Nevertheless, in April 2024, the collection appeared on her credit report. When she called the company to find out why, the representative told her that she would have to pay the account in full if she wanted the information deleted.

This consumer’s experience is another reason why you should get professional help.

How to Remove a Medical Data Systems Collection

A Medical Data Systems debt collection on your credit report does not have to stay there. The company has a history of failing to verify debts when consumers dispute them. Moreover, the majority of complaints that consumers have filed against the company have not been resolved to the satisfaction of the consumer.

Finally, credit reporting mistakes are common and any debt collection may contain errors.

The worst thing you can do is exactly what the debt collector hopes you will do: pay immediately out of fear and urgency. The better strategy is to understand your legal rights, remain silent, and get professional help.

Debt collectors operate on thin margins and rely on consumers not understanding their legal rights to make money. When consumers understand how credit reporting works and know how to enforce their legal rights, the balance of power shifts.

Get Professional Help Now

If you see Medical Data Systems on your credit report, do not contact the company directly. Do not agree to a payment plan over the phone. Do not provide personal or financial information or acknowledge that you owe a debt.

Instead, contact us at FightCollections.com for a free consultation. We understand the particular vulnerabilities of collection agencies like Medical Data Systems and how to exploit them through legal procedures. We have already helped thousands of consumers remove questionable collection accounts from their credit reports.

The debt collection that appeared on your credit report out of nowhere can disappear if you use the right strategy. Contact us today to find out how we can help.