When you discover a mystery debt on your credit report, it can feel like a jury delivered a verdict against you before the trial even began.

If the debt collector involved is Paragon Revenue Group, you have officially entered a dispute process where your best defense is knowing your legal rights inside and out.

In this article, we will break down exactly what you can ask for, what you can dispute, and what you can demand in your dealings with this collector. Collectors count on the stress of owing a debt, and their business models are predicated on the leverage that stress provides.

But disputing a debt is a clinical and procedural process rather than an emotional one. Your rights under the law are a reality because lawmakers recognized that the relationship between consumers and debt collection companies is fundamentally unequal.

Who is Paragon Revenue Group?

Paragon Revenue Group is a subsidiary of Jon Barry and Associates, Inc., a North Carolina debt collection agency with a specialty focus on collecting healthcare and medical debts exclusively. The company was founded in 1986. Here is a snapshot of the basic business information for Paragon Revenue Group:

Since Paragon Revenue Group exclusively collects medical debt, you are likely to face hospital bills, ER bills, or other medical accounts from this debt collector.

What the Record Reveals About This Collector

Better Business Bureau (BBB) records show a 247 percent spike in recent complaints against Paragon Revenue Group. As of January 2026, the company has received 294 complaints in the past three years and 118 in the last 12 months alone. In contrast, legal analysis of the company in September 2019 counted 94 complaints in the previous three-year period.

There have been roughly 30 federal lawsuits against Paragon Revenue Group, including the following examples:

Darden v. Paragon Revenue Group

Sterner v. Paragon Revenue Group

Wilbur v. Jon Barry and Associates, filed in September 2024

Paragon Revenue Group customer reviews on the three major platforms are consistent. On the Better Business Bureau platform, the company averages 1 out of 5 stars. On WalletHub, the average customer rating is 1.9 out of 5 stars, with 69 percent of reviewers assigning a rating of 1 star. On Google, the company has an average rating of 1 out of 5 stars based on eight reviews.

Despite being in business since 1986, Paragon Revenue Group is NOT BBB Accredited.

Your Legal Right to Demand Debt Validation

What the FDCPA Requires Collectors to Prove

The FDCPA is clear: the burden of proof in any debt collection action rests on the debt collector, not the consumer. Under FDCPA Section 1692g, any debt collector must provide written validation of the debt within five days of initial contact. That validation must include:

The amount of the debt

The name of the creditor

A statement of your right to dispute

The most common consumer complaint against Paragon Revenue Group is an alleged failure to comply with this requirement. Multiple complaints registered with both the BBB and the Consumer Financial Protection Bureau describe debts that appeared on credit reports before the consumer received any written communication at all.

In December 2025, a complainant told the BBB:

"I was never contacted by this company prior to this account being placed on my credit report. I have never received any written communication or debt validation, as is my right under the FDCPA."

When a medical debt is sold from the original provider to a collection agency—and sometimes to multiple agencies along the way—documentation is often incomplete or entirely lost. This scenario creates grounds for you to dispute the debt because the collector cannot validate a debt without proper documentation.

The 30-Day Dispute Window

Under federal law, you have a 30-day window from the time you receive an initial validation notice to dispute the debt in writing. If you exercise this right within that period, the law requires the debt collector to suspend collection activities until they provide verification of the debt.

The 30-day period is not a suggestion or a courtesy; it is a legal mandate. The problem for many consumers is that they never receive the proper validation notice in the first place, which means the clock may never have legally started.

In a complaint filed against Paragon Revenue Group in January 2026, the consumer reported that:

"The only communication I have received from this company is a text message with a link. I have not received any written communication at all."

A text message with a link is not a valid response to a debt validation request under the FDCPA. In general, credit report information is riddled with errors. According to research by U.S. PIRGs, 79 percent of credit reports contain errors or “serious errors.” In practical terms, this means you would be taking a significant risk against your own interests if you assume any collection is accurate until it is verified.

Understanding Why Payment May Not Be Your Best First Move

The Credit Report Reality

Consumers who are unfamiliar with the FDCPA often believe that paying a collection account is a first step toward improving their credit situation. The reality of how credit reports function is a bit different.

If you pay a collection account, you will change the status of the account on your credit report from “unpaid collection” to “paid collection.” But here’s the thing: the account will still be on your credit report either way. And either way, it will still damage your credit history.

The Fair Credit Reporting Act specifies that collection accounts can remain on your credit report for seven years dating from the original delinquency date with the original creditor. If you pay the collection, the clock does not start over. And if you do not pay the collection, the clock still keeps ticking.

In 2019, a complainant told the BBB that Paragon Revenue Group attempted to collect $28,000 in hospital bills from 2015-2016 that were already “paid and settled” by both the patient’s insurance companies and the patient himself. The complainant alleged that representatives of the company called the consumer “a liar” and threatened the consumer with “negative credit reporting.” The collection account was ultimately canceled after the consumer filed a formal complaint.

The Verification Alternative

Instead of paying the collection immediately, you can exercise your right to demand verification—and shift the burden of proof to where it belongs. When you make a verification request, you are asking the collector to prove three things:

The debt is valid

The collector has the authority to collect it

The amount is correct

If the collector cannot provide the requested documentation, you may have grounds to have the account removed.

The pattern in BBB complaints against Paragon Revenue Group is telling. While the company responds to the vast majority of complaints filed against it, only 90 of 294 complaints have resulted in resolutions that the consumer found satisfactory. In most cases, the company appears to resolve complaints by canceling the accounts in question from collection.

That means the aggressive tactics may not survive a robust challenge. If you know your rights and use them, collection accounts that cannot survive the verification process may simply vanish.

How to Identify Illegal Collection Practices

Illegal Harassment and Communication

The FDCPA states that a debt collector may not harass, oppress, or abuse any person in connection with the collection of a debt. This includes placing repetitive telephone calls to the consumer with the intent to annoy, abuse, or harass; using obscene, profane, or abusive language; or threatening to take legal action they cannot or do not intend to take.

In 2016, a Texas woman sued Paragon, alleging the company called her persistently about a debt owed by her grandmother for over a year, despite multiple requests to stop calling because they had the wrong number.

Debt collectors know that people generally respond to authority. The reminders that collectors may impersonate government agents or threaten to arrest you if you don’t pay your debt demonstrates this. If someone threatens to have you arrested or jail you, or to take your wages or put a lien on your property, they are violating your federal rights if they don’t intend to follow through with that threat.

As one reviewer on the BBB website put it, she called Paragon about a debt they claimed her husband owed, and was told to get a loan to pay it. “When I told her that we couldn’t, she got very mean and nasty with me,” she said. “The health care provider was totally willing to work with us and find ways to pay the bill. Paragon treated us like dirt and like we were beneath them. The lady was trying to force us into something we could not do.”

Illegal Disclosure to Third Parties

Debt collectors may not discuss your debt with anyone except you, your spouse, or your attorney, unless they are trying to locate you. Even then, they are not permitted to state that they are collecting a debt. If a collector talks to a family member, an employer, a neighbor, or anyone else about your debt, they have broken federal law.

Approximately 30 federal lawsuits have been filed against Paragon, including TCPA violations, which govern robocalls and text messages. If you receive robocalls or text messages from a collector without your consent, you may have a claim under the law

About 97 complaints have been closed against Paragon with the Consumer Financial Protection Bureau over the last three years, with about 40 percent related to the incorrect amount of the debt. The CFPB was created in the wake of the mortgage crisis to protect borrowers from bad actors in the financial services industry. The agency regulates a wide array of financial products, including mortgages, credit cards, and yes, debt collection agencies.

Disputing a Debt

Credit Bureau Disputes under FCRA

In addition to disputing a debt directly with the collection agency, you can also dispute a collection account with the credit reporting agencies if it’s on your credit report. Under the FCRA, credit reporting agencies must investigate your dispute within 30 days, and if they can’t verify the information, they must remove it from your credit report.

This is a completely separate process from disputing the debt with the collector. If you dispute with the credit reporting agencies, they will contact the data furnisher to verify the information. If the data furnisher can’t verify the debt within the 30-day window, the credit reporting agencies must remove the item from your report.

You don’t have to communicate with the collection agency at all during this process. Sometimes the best response is no response at all. You don’t have to justify, explain, or negotiate. You have the right to dispute a debt, and once you assert that right, the burden is on the other parties to verify the debt.

The credit reporting agencies must investigate your dispute, and the data furnisher must verify the debt, or the item will be removed. And remember, anything you say can and will be used against you.

Proper Documentation for a Dispute

If you want to dispute a debt, you need to document everything. This includes:

Your credit report with the disputed account circled

Correspondence you have received from the debt collector

Correspondence you have sent to the debt collector

A copy of your dispute letter or online submission to the credit reporting agency

A copy of your dispute letter or online submission to the debt collector

Correspondence from the credit reporting agency

Correspondence from the debt collector

You should also keep a record of every telephone call you make or receive related to the debt, including the date, time, and name of the representative you spoke with, as well as a summary of your conversation.

Use certified mail with return receipt requested. When you understand your rights, document all communication, and follow the process carefully, you begin to level the playing field. Debt collectors are counting on you to not understand the process, and not to follow it. If you follow the steps outlined above, you’ll be ahead of the game.

Google reviewers claim Paragon put items on their credit report that weren’t their debt, and when they called to discuss the problem, they couldn’t get a representative on the phone. Others claim they sent Paragon documentation that proved the debt wasn’t theirs, but Paragon refused to accept it.

When you mail your dispute, use certified mail with return receipt requested, so you have a record that they received it. And when you’re talking on the phone, remember, anything you say can and will be used against you.

If you mail a dispute, the debt collector can’t continue to contact you except to tell you there will be no further contact or to notify you that they intend to file a lawsuit against you. But phone calls don’t offer the same protection. Get everything in writing, and keep everything you receive, along with your response.

Finally, keep a record of every phone call, including the date, time, representative’s name, and a summary of what you discussed. Keep this information along with your copies of correspondence.

The Importance of a Third Party

Illegal Debt Collection

Several law firms, including Lemberg Law, Agruss Law Firm, Consumer Rights Law Firm PLLC, and The Wood Law Firm, offer their services to consumers who are being pursued by Paragon. If you are being called or sued by Paragon, you should call one of these firms immediately.

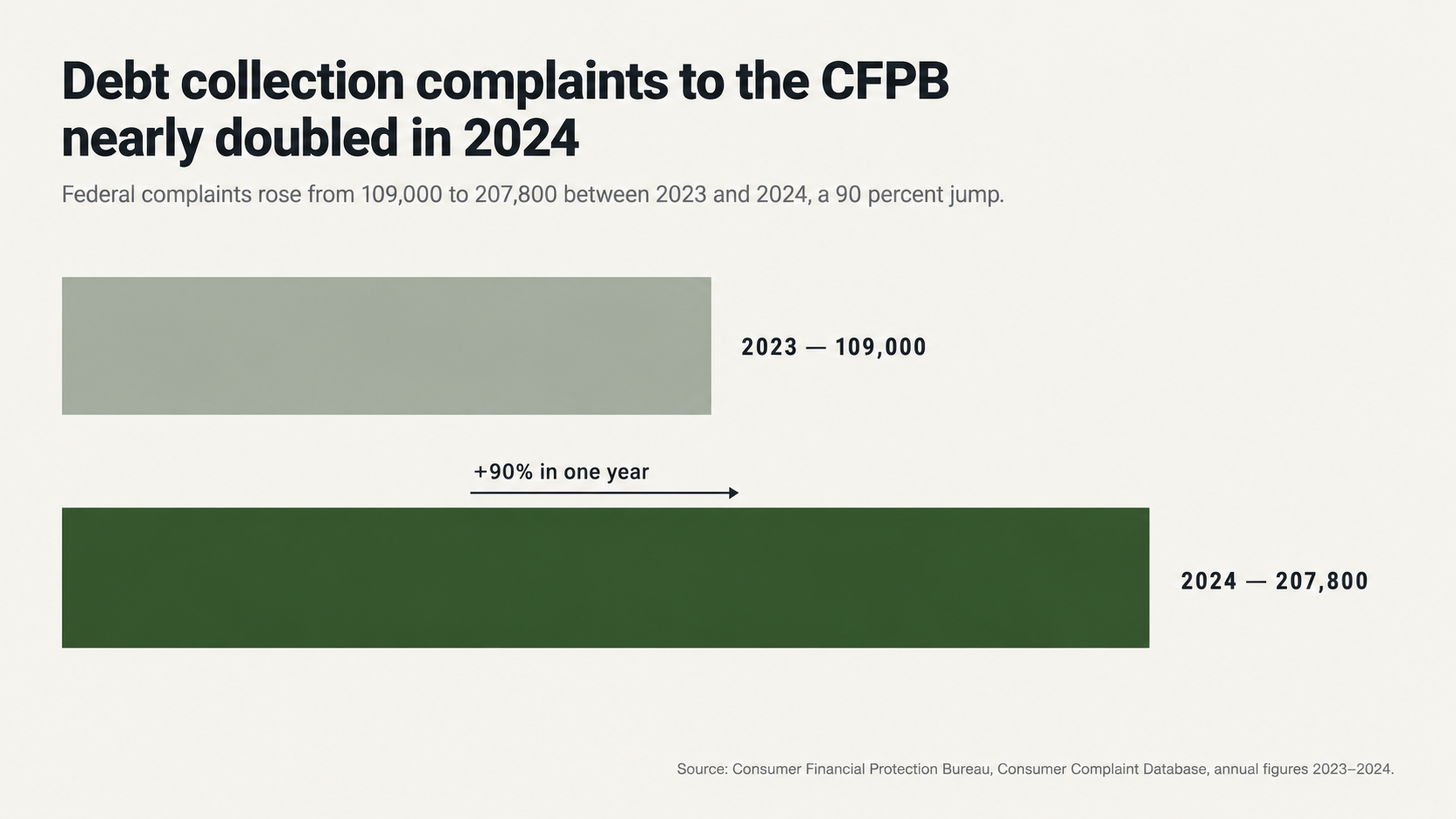

In addition to complaints filed with the BBB and the CFPB, about 30 federal lawsuits have been filed against Paragon. About 109,000 complaints were filed with the CFPB about debt collection agencies in 2023, but that number rose to 207,800 in 2024, a 90 percent increase.

Though debt collection agencies are some of the most complained-about financial products regulated by the CFPB, the agency doesn’t have the resources to pursue every illegal debt collection agency or every complaint filed. Though the CFPB, the FTC, and state attorneys general may file charges against debt collection agencies, unless you’re part of a class action lawsuit, you’ll need to file a private lawsuit to recover damages or get the agency to stop contacting you.

Working with a Professional Credit Repair Company

Many consumers choose to work with a credit repair agency that specializes in disputing collection accounts. In addition to understanding all the documentation required for a proper dispute, these agencies understand the timing, the process, and the laws that govern it.

They know how to determine whether you have a valid case against a collection agency, and the best way to approach the agency to resolve your account. They also understand the documentation required for each step of the process. They know how to approach the collection agency to get the best results for you. And they understand how to communicate with the credit reporting agency to resolve your dispute.

When you work with a reputable credit repair agency, you get the benefit of their experience. This experience comes from thousands of people who have been in your shoes before you. The credit repair agency understands the tactics the debt collection agency may use to get you to pay, and they understand how to use the law to protect your rights and resolve your debt in the best way possible for you.

The most common complaints were about billing and collections problems, which accounted for 35.7 percent of all complaints filed with the agency. Another 21.8 percent were about problems with a service, while 19.4 percent were about problems with an order. All these areas require different strategies and documentation.

For instance, if there’s a problem with your billing or a service, you may need to provide documentation or clarification about the issue. But if there’s a problem with an order, you may need to cancel the service or return a product. In each of these cases, you’ll need to approach the debt collection agency differently, and you’ll need different documentation. But in all cases, keeping detailed records of everything is essential.

If you try to dispute a debt on your own without a good understanding of the law and process, you may end up losing leverage you didn’t know you had. You may inadvertently acknowledge that you owe the debt, for instance. Or you may fail to meet a deadline for filing a dispute or responding to a lawsuit. You may not document your communication properly. And you may not file a dispute in the proper way.

Working with a credit repair agency that specializes in disputing debt collection accounts can help you avoid these mistakes and achieve the best outcome. Instead of trying to navigate this process on your own and risking making a mistake that will hurt your case, why not work with someone who understands the process and the law, and can help you resolve the issue in the best way possible for you?

Keep reading to learn how you can get help now.

Conclusion

Paragon Revenue Group is a debt collection agency with a history of complaints filed with the BBB, as well as federal lawsuits. The company has a one-star rating on every review platform, including Google reviews, where the company averages one star out of five. And if you do a search for Paragon Revenue Group, you’ll find about 30 federal lawsuits filed against the company for illegal collection practices.

With a 247 percent increase in complaints filed with the BBB since 2019, and an average one-star review on every platform, it seems this debt collection agency is counting on consumers not understanding their rights under federal law.

Under the federal Fair Debt Collection Practices Act and the Fair Credit Reporting Act, you have the right to dispute a debt any time you want. And if you do it properly, using federal and state laws in your favor and documenting every step of the process, you may be able to have the debt removed from your credit report and resolved without paying it. Sometimes, exercising your legal rights means you don’t have to pay a debt at all.

Instead of allowing Paragon Revenue Group to push you around and threaten or harass you into paying a debt you don’t owe or can’t afford to pay, why not educate yourself on your legal rights, document every step of the process, and force the debt collection agency to prove you owe the debt or verify it according to the law?

In many cases, debt collection agencies like Paragon Revenue Group don’t have the documentation to prove a debt, so when consumers force them to verify it, they end up removing it instead. Are you ready to learn more about how you can make that happen for you?

Get Help with Your Paragon Revenue Group Account

If you see Paragon Revenue Group on your credit report, you don’t have to deal with it alone.

At FightCollections.com, we specialize in helping consumers dispute debt collection accounts and understand their legal rights. We can help you review your credit report, understand your options for disputing a debt with Paragon Revenue Group, and help you decide the best way to approach the debt collection agency to resolve your account.

Our professionals understand the laws that govern healthcare debt collection agencies like Paragon Revenue Group and their processes. We can help you understand whether you have a potential illegal debt collection claim against Paragon Revenue Group. And we can help you develop a strategy to dispute your debt and resolve your account in the best way possible for you.

You don’t have to pay a debt you don’t owe or can’t afford to pay. You have legal rights that protect you from illegal debt collection practices. Why not exercise them now and resolve your debt today?

Contact us at FightCollections.com to get a free consultation today.