Do you have a Collection Account on your credit report from a company called Selip & Stylianou LLP? If so, you might be looking for ways to get rid of it.

It’s like having an unwanted roommate, except you cannot simply evict them. Instead, you have to understand who they are, how they operate, and why this collection account appeared on your credit report.

The first thing most people do when they see a collection account on their credit report is pay the debt immediately to make the problem go away. While that’s an understandable reaction, it can also be the worst possible move.

That’s because even a paid collection remains on your credit report for up to seven years, and making that payment could even revive the debt or start the clock ticking all over again.

So who is Selip & Stylianou LLP? And how can you get this collection account removed from your credit report?

Who is Selip & Stylianou LLP?

Selip & Stylianou LLP is a debt collection law firm based in Woodbury, New York. The company has been in business for over 22 years and was originally founded in 1991 under a different name: Cohen & Slamowitz LLP. The firm was renamed to Selip & Stylianou in January 2015.

Regulatory Problems

The New York-based debt collection law firm has a track record that speaks for itself.

In February 2014, a five-judge panel of the New York Appellate Division publicly censured Cohen & Slamowitz, the predecessor to Selip & Stylianou, for misconduct in six cases. The court found that in each of the cases, the law firm had sued the wrong person, even though it had information indicating that it was pursuing the wrong debtor.

In some cases, the firm froze bank accounts even though it knew that the underlying debts already had been paid.

Between January 2013 and April 2022, the Consumer Financial Protection Bureau received 191 complaints about Selip & Stylianou. The company was ranked in the top 10% of most complained about debt collection companies in the country.

Many of the complaints against Selip & Stylianou allege that the firm froze bank accounts without notice or attempted to collect debts that consumers did not owe. Others claim that the firm seized funds that were exempt from garnishment, such as Social Security benefits.

The law firm also has been sued in more than 95 federal cases, including multiple class actions alleging violations of the Fair Debt Collection Practices Act. In one case, Hallmark v. Cohen & Slamowitz, the court certified a class and awarded $400,000 in attorney fees to class counsel.

How Does the Debt Collection Agency Operate?

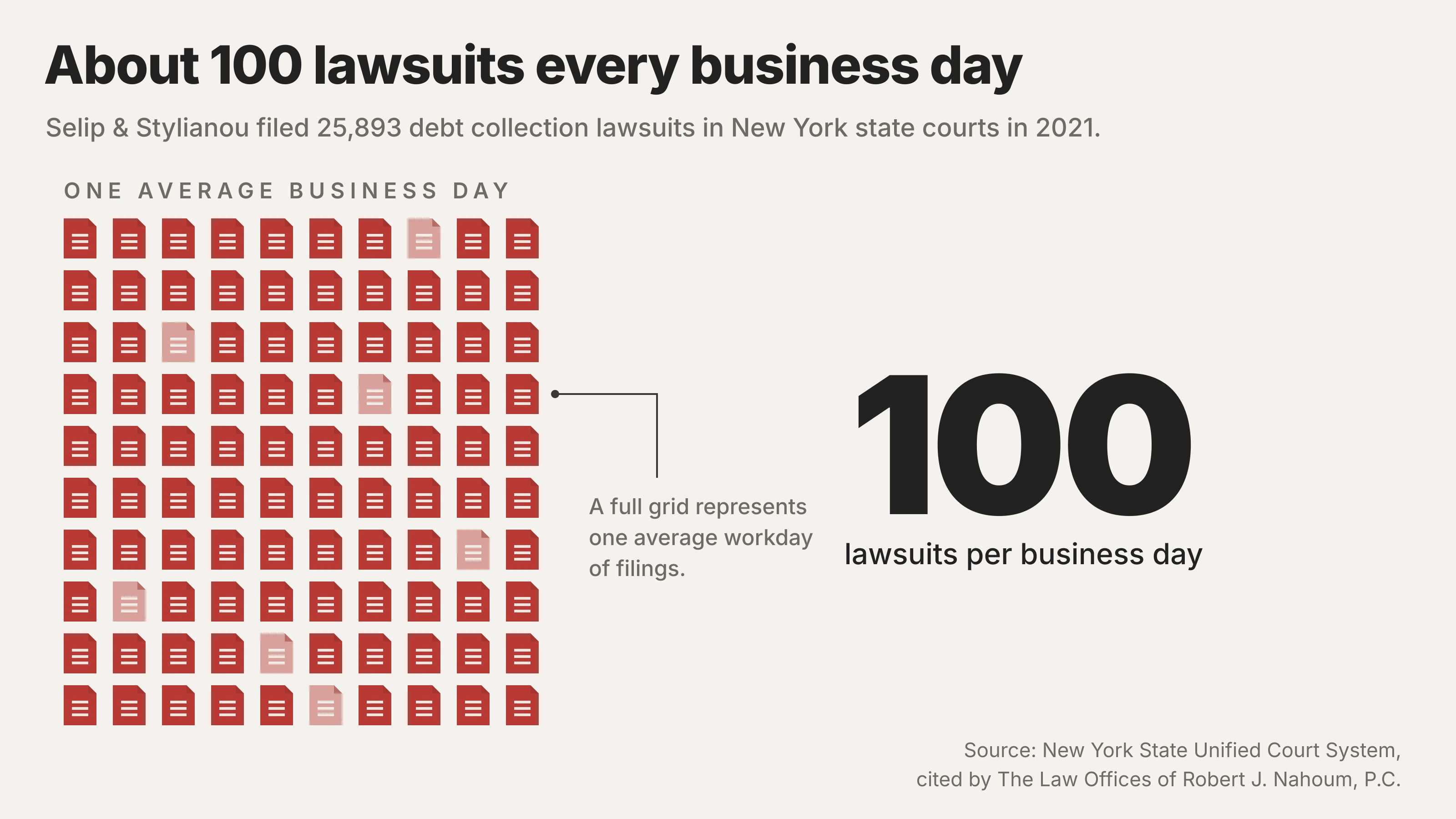

Debt collection agencies like Selip & Stylianou operate on volume. They make money by filing as many debt collection lawsuits as possible and hope that consumers do not show up to court to defend themselves. In 2021, Selip & Stylianou filed 25,893 debt collection lawsuits in New York state courts. That’s an average of about 100 lawsuits per business day.

When a debt collection law firm files that many lawsuits, it is impossible to verify each account. That creates leverage for consumers who know how to use it. Debt collection agencies like Selip & Stylianou thrive on consumers who do not understand their rights and who get intimidated when a law firm comes after them.

So how does the debt collection agency communicate with consumers?

Debt collectors thrive on creating a sense of urgency. They will do whatever they can to make you think that you need to take immediate action or face severe consequences. Consider this complaint filed with the Consumer Financial Protection Bureau: “They misrepresented key information in this case in several documents and provided false information to the court.”

It’s natural to defer to authority. And when the authority figure is a law firm, most consumers are quick to capitulate and pay what they’re asking for. But that dynamic changes when you have professional representation. Once the debt collector realizes that they’re facing off against a credit repair company and not just an individual consumer, they’re far less likely to continue pursuing the debt.

Why Inaccurate Credit Report Information Matters

Did you know that 79% of credit reports contain errors or other inaccuracies? That statistic alone should change the way you approach a collection account on your report. Instead of assuming that the debt is legitimate, you should start with the assumption that it’s incorrect and verify before you do anything else.

The debt buying industry adds another layer of complexity to the problem. When debts are sold from one company to the next, information gets lost or destroyed in the shuffle. Selip & Stylianou primarily works with debt buyers like Midland Funding and Portfolio Recovery Associates. These companies buy packages of debt from other companies, but the packages don’t always include all the information necessary to collect on them.

What Happens When Inaccurate Information Winds Up on Your Credit Report

You may see a collection account on your credit report for a debt that you’ve already paid. You may see an account for a debt that’s past the statute of limitations. You may see an account for a debt that was discharged in bankruptcy. Or you may see an account for a debt that isn’t yours at all.

Consider this complaint filed with the Consumer Financial Protection Bureau: “Cohen & Slamowitz LLP in NY somehow obtained a default judgement against me for $4,700 in county Supreme court. I investigated this claim and found that Slamowitz contends that service was made at an address at which I never lived. I have no knowledge of this debt.”

The New York State court that censured Cohen & Slamowitz found that the company sued the wrong people even when it had reason to know it had the wrong person. Instead of dropping the debt, the company continued to pursue it in court.

How to Remove a Selip & Stylianou Collection from Your Credit Report

When you see a collection account from Selip & Stylianou on your report, do not pay it until you verify that it’s accurate. Instead, start by disputing the account. Paying the account will not remove it from your report. You will still have a collection account on your report even if you pay it. Instead, dispute the account and force the collection agency to verify the debt.

The Fair Debt Collection Practices Act says that consumers have the right to request validation of a debt within 30 days of initial contact. The debt collector must stop all collection activity until it provides you with verification of the debt. If it can’t verify the debt or can’t meet the deadline for responding to your request, it must remove the account from your report.

Requesting debt validation is a great way to get rid of a collection account on your report, but it’s also an offensive strategy. For many debts, the collector can’t provide complete validation. For example, when debts get sold and resold, the documentation doesn’t always follow. You may not be able to get your original contract or payment records. And you may not be able to get documentation showing the chain of assignment as the debt got sold.

Your Rights Under the FDCPA

The Fair Debt Collection Practices Act prohibits debt collectors from harassing or abusing you. It also prohibits debt collectors from using false or misleading information to collect a debt. And it prohibits unfair practices like attempting to collect more than you owe.

You have the right to control how debt collectors contact you. You can stop their phone calls and letters at any time by sending them a cease communication letter. Once you send a debt collector a cease communication letter, it can only contact you in limited circumstances. For example, it can let you know that it made a request or intends to make a request for a court judgment. Or it can tell you that it intends to involuntarily seize your money or property.

Many consumers have filed complaints against Selip & Stylianou, saying that the company contacted them improperly. Consider this review left with the Better Business Bureau: “They taped the summons to my door with blue contractors’ tape, outside with ALL my information on it for the world to see. Never even knew they were there, and I was home. This is highly suspicious and very unprofessional.”

You also have the right to expect that debt collectors will not attempt to collect an improper debt. That includes collecting the wrong amount or attempting to collect a debt that you don’t owe at all. You also have the right to expect that debt collectors will sue you in the right court. Debt collectors can only file a lawsuit in the court where you live or where you signed the original contract.

In some cases, debt collectors make procedural mistakes when filing a lawsuit. For example, in Hess v. Cohen & Slamowitz LLP, the Second Circuit Court of Appeals found that the debt collection law firm violated the FDCPA when it sued a consumer in the wrong court. The court found that filing a lawsuit in the wrong court constitutes a violation of federal law.

Why You Should Work with a Professional

Debt collectors have the upper hand when they’re negotiating with consumers. They do this every day, and they know which tactics work best to get you to pay up. Most consumers only deal with debt collection once or twice in a lifetime. That means debt collectors have far more information than consumers do. But when you work with a professional credit repair company, you get the upper hand. Instead of dealing with a consumer who doesn’t know the system, the debt collector has to negotiate with a company that does.

Credit repair professionals know how to use a debt collector’s information against them. For example, at Collections Relief, we know all about Selip & Stylianou’s regulatory problems, federal court cases, and complaint history. We know the types of documentation requests that are most likely to get results. And we know how to communicate with debt collectors in a way that tells them they’re in for a fight.

Working with credit repair professionals also means that we can use patterns we’ve observed to strengthen your individual case.

For example, we know that Selip & Stylianou operates on volume. The company files thousands of lawsuits every year and counts on consumers not responding to those lawsuits. We know that the company has a history of regulatory problems and has lost cases in federal court for violating the FDCPA. And we know that consumers have filed nearly 200 complaints with the Consumer Financial Protection Bureau.

Conclusion

Selip & Stylianou LLP is a debt collection law firm based in New York.

Instead of paying a collection account from the company, verify that it’s yours. Make the debt collector show you documentation to prove that you owe the debt and that it’s not past the statute of limitations. Don’t give in to the company’s high-pressure tactics, and don’t assume that you owe the debt simply because it appears on your credit report.

Contact FightCollections.com today to find out more about how you can remove inaccurate, unverifiable, or fake debts from your credit report.