Dealing with a mystery collection account from an agency with a reputation like Vance and Huffman can feel a lot like being accused of a crime you might not have committed.

Thankfully, proving you don’t owe the debt isn’t your responsibility.

A lot of people think it is, which is why so many people end up settling with collection agencies that have no real claim to their money. When you understand that the burden of proof is actually on the collection agency, not on you, you can turn the tables and make them prove that you owe the debt in question.

But who is Vance and Huffman, and what can you do if they’ve added a suspicious collection account to your credit report?

Vance and Huffman, LLC is a third-party debt collection agency and debt buyer based in Virginia. The company buys debts from the original creditor and tries to collect on them.

The numbers don’t look great for Vance and Huffman. According to its profile on the Better Business Bureau (BBB) website, the company has received 847 complaints in the last three years. With only 11 employees (according to its LinkedIn page), that’s a staggering number of complaints per employee. On top of those complaints, at least 13 consumers have filed federal lawsuits against the company for violating their rights under the FDCPA.

The company has an average rating of 1.8 stars out of 5 on Google Reviews and just 1 star out of 5 on BBB. These reviews and complaints paint a picture of a company with which many consumers have had very negative experiences.

Why Is Vance and Huffman on My Credit Report?

Debt collectors often place collection accounts on your credit report without warning. That’s not a coincidence. It’s a strategy meant to intimidate you into paying a debt you might not actually owe, simply because it’s already hurting your credit score. Negative information can be added to your credit report at any time.

All a debt collector has to do is provide information about the debt to a credit bureau, and voilà! You now have a collection account on your credit report. But it’s up to you to dispute it. This is an inherently unfair process.

When a debt collector wants to add negative information to your report, they don’t have to prove anything. They just have to provide information, whether or not that information is accurate or verified.

One BBB complainant wrote in November 2025 that, “there is a collection on my credit report from this company stating I owe over $3000.00 for a debt I paid off over 3 years ago. Due to this I am unable to secure an apt. They placed this on my credit report without contacting me.”

The complainant didn’t receive any kind of notice that Vance and Huffman was going to add a collection account to their credit report. The company simply did it. It’s easy to imagine how frightening that must be, especially if you know you’ve paid a debt in full. Vance and Huffman didn’t even send this consumer a letter before adding the collection account to their report.

How do debt collectors like Vance and Huffman get the wrong person? Debt collection isn’t an exact science. Debt collection agencies and buyers purchase debt portfolios from original creditors. Sometimes the original documentation doesn’t even transfer. That means there’s plenty of room for error, including cases in which debt collectors target the wrong consumers altogether.

One of the most common issues that consumers report in complaints about Vance and Huffman is identity confusion. There have been reports of attempts to collect from the wrong people simply because they share a name with the actual debtor (despite having different Social Security numbers).

One consumer reported to the CFPB that, “I have disputed this debt as not mine with the [credit reporting agency], CFPB and directly with [Vance and Huffman] however the account still appears on my report. The social [security number] they have on file for this account is not mine.” As you can see, there are plenty of reasons why debt collectors might attempt to collect the wrong debts from the wrong people.

What Are My Rights When Dealing with Debt Collectors?

Debt Collectors Must Prove You Owe a Debt

Under the FDCPA, debt collectors must validate a debt when you request they do so. That means they must show you documentation proving not only that you owe the debt but also that they have the right to collect it. If they can’t provide such documentation, they have no basis for their claim. Many consumers who have dealt with Vance and Huffman report struggles to get the company to validate their debts.

One CFPB complaint from 2017 says that the consumer requested debt validation for a debt that was over seven years old and had never been validated. Rather than providing documentation to prove the debt, a representative offered a pay-for-delete deal. That suggests the company can’t validate the debt.

Never pay a debt or provide financial information until you’ve confirmed it’s valid. It’s also a good idea to communicate with debt collectors in writing rather than on the phone, where you might inadvertently admit to a debt or agree to something you don’t want to. Communication in writing creates a paper trail and ensures the collector can’t claim you said something you didn’t.

Federal and State Protections

Many people fear garnishment of wages or bank accounts, but federal and state laws offer significant protections against that. In most cases, consumers have more protection than they think. For example, Social Security benefits, disability benefits, and, in many cases, portions of your wages are completely exempt from garnishment.

In addition to those protections, the Fair Credit Reporting Act (FCRA) ensures that debts on your credit report must be accurate and substantiated. If information on your credit report is inaccurate, the result of identity theft or fraud, or cannot be verified within a reasonable amount of time, you have the right to dispute it and have it removed.

A consumer complained to the BBB in April 2025 that, “Vance and Huffman, LLC has filed a collection account on my personal credit report for a debt that was discharged in my Chapter 7 bankruptcy almost seven years ago. I did not receive any letter from this company informing me of this account nor was I given any opportunity to dispute this account prior to them reporting it.” The consumer’s bankruptcy discharge is a legal protection that a debt collector can’t simply ignore.

Why Paying a Collection Agency Like Vance and Huffman Won’t Help Your Credit

When you pay a collection account, the status of that account on your credit report changes from “unpaid collection” to “paid collection.” But that doesn’t mean the account is removed. You can still expect to see a paid collection account on your credit report for up to seven years from the date of the original delinquency. Unfortunately, the presence of any collection account on your credit report—whether paid or unpaid—is a red flag for lenders. It indicates that you have had serious difficulty paying your debts on time in the past.

Some newer credit scoring models don’t differentiate between paid and unpaid collections. That means you could pay a collection account and still not see much of an increase in your credit score as a result.

That’s why it’s essential to dispute a debt before paying it, whenever possible. If the collection agency can’t verify that you owe a debt or made an error in its report, you may be able to have the account removed entirely. That will help your credit more than simply paying it.

What a Debt Collector Doesn’t Want You to Know

The debt collection business model relies on quick turnaround. Debt collectors buy debts for pennies on the dollar and only make a profit if they can collect. That means the longer they have to spend on a consumer, the costlier that consumer is. It’s always in the best interest of a debt collector to resolve a debt as quickly as possible. That creates an incentive for debt collectors to pursue consumers who are likely to panic and pay a debt without questioning it rather than those who stand up for their rights and demand documentation.

Debt collectors make the most money when consumers are reactive rather than proactive. When you understand your rights and refuse to be pushed around, you cost debt collectors time and money. Patience is a powerful tool in this situation.

In several cases, Vance and Huffman has settled lawsuits in short order when consumers pushed back in court.

For example, in the case of Shelton v. Vance and Huffman, filed in September 2020 in the U.S. District Court for the Southern District of Indiana, the parties reached a settlement agreement just seven weeks after the initial filing. While the terms of the agreement aren’t public, the speed with which the company settled suggests that pushing back in court can be an effective strategy.

How Can I Get a Collection Removed from My Credit Report?

Dispute Inaccurate Information

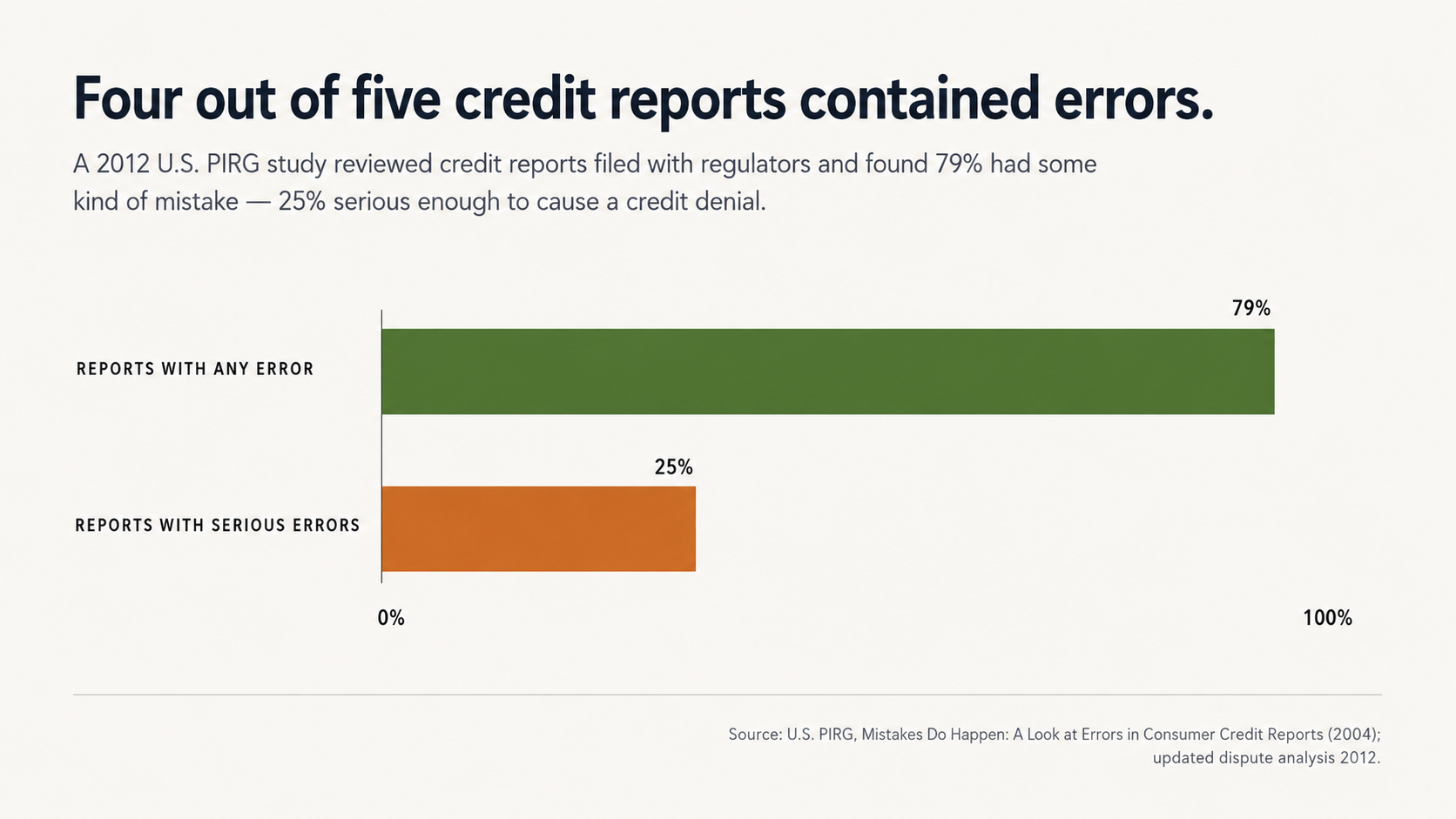

It’s easy to find horror stories about credit report errors and inaccuracies. In fact, a 2012 study by U.S. Public Interest Research Groups found that as many as 79 percent of credit reports contain some kind of mistake or serious error.

When it comes to collection accounts specifically, that might include the wrong balance, the wrong date, the wrong debtor, or a debt that has already been paid or discharged. The dispute process puts the burden of proof on the debt collector rather than the consumer.

When you dispute information on your credit report, the creditor has a limited amount of time to verify the information. If the creditor can’t complete the verification process within that timeframe, the credit reporting agency must remove the disputed information from your report.

But verification requires documentation, not just a statement that you owe a debt. Plenty of debt collectors can’t verify the debts they pursue because they don’t retain the original documentation.

Debt buyers in particular often can’t produce original contracts or payment records for the debts they buy. Vance and Huffman consumers have reported plenty of experiences in which the company was unable or unwilling to verify a debt.

For example, one CFPB complaint from 2017 says that the consumer requested debt validation for a debt over seven years old that had never been validated. Rather than providing that documentation, a representative instead offered a pay-for-delete deal.

That suggests the company may not have the documentation it needs to prove the consumer owes the debt. If you try to dispute a debt on your own, you’re facing off against a company that specializes in debt collection. That means the company has experience with the process, understands the deadlines, and knows the technicalities of the law. The company may even have an in-house legal team or established relationships with outside counsel.

Seek Help of Professional Credit Repair Companies

When you’re navigating the system on your own, you’re at an automatic disadvantage.

Professional credit repair companies help level the playing field. These companies employ people with experience in debt collection and removal. They understand which kinds of disputes are most likely to be successful and how to word your disputes for the best effect. They know when a debt collector is trying to bluff you and when you can apply pressure to facilitate removal.

Additionally, if you work with a professional credit repair company, you can trust the company to meet deadlines and file disputes properly. If you miss a deadline or file a dispute incorrectly, you can undermine even a strong case for removal.

With a professional credit repair company handling the details and keeping track of the process, you can focus your time and energy on other parts of your life while a professional works to repair your credit. You don’t have to face a suspicious debt from Vance and Huffman alone. Help is available.

Contact FightCollections.com today for a consultation. Let us put Vance and Huffman on trial instead of you. Your credit report tells lenders who you are financially. Make sure it tells the truth.