If you see a strange company name on your credit report, your initial reaction is probably a mix of confusion and panic.

Absolute Resolutions Investments LLC is a Minnesota-based debt purchasing company. They buy batches of charged-off debts from the original creditors and then attempt to collect on them, sometimes filing lawsuits against consumers in the process.

What the Case File Shows

ARI is the sister company to Absolute Resolutions Corporation which is the entity that actually provides collection services. The parent company was originally formed in 2001 and was restructured in 2016 when it was merged with RAzOR Capital. This is a typical practice among debt buyers which can lead to missing paperwork and missing documentation that is helpful to consumers in a dispute.

Over the past 10 years, 98 complaints have been filed with the Consumer Financial Protection Bureau. In the last 3 years alone, 207 complaints have been filed with the Better Business Bureau with 57 of them occurring in the last year. These complaints are not coincidental; they are representative of ongoing business practices that have played out tens of thousands of times.

The Paper Trail Problem

Why Debt Buyers Have a Hard Time with Validation

When the original creditors bundle delinquent accounts and sell them, they are typically only selling the digital information about the debts. The original signed agreement, detailed accounting history, and ownership chain paperwork are rarely included in the sale.

ARI purchases debt portfolios fully aware that they usually don't receive the underlying documentation. This sets up a huge problem with their business model. The Fair Debt Collection Practices Act requires debt collectors to validate debts if they are disputed but the business model of buying debt almost guarantees that they won't have the documentation they need.

Attorneys that have litigated against ARI have indicated that the company routinely cannot produce original contract documentation when they are challenged. The business model relies on volume. Debt buyers that operate on very thin profit margins need to succeed with a high percentage of accounts in order to turn a profit. The economic model incentivizes the company to pursue rapid collection rather than properly validating each account.

Error Rates are High in the Industry

A study done by U.S. PIRGs found that 79 percent of credit reports contained either errors or serious mistakes. When debt buyers purchase portfolios that contain thousands of accounts, the error rate within the portfolio transfers to their efforts to collect. Accounts get assigned to the wrong people, balances contain calculation errors, and debts that were previously paid get reincarnated under new ownership.

The credit reporting industry allows negative marks to be placed on your report without the collector having to prove it is accurate. The burden is shifted to you to dispute the information that should not have been on your report in the first place. The assumption of guilt built into the credit reporting system provides collectors with tremendous leverage until someone challenges them with a formal dispute.

Complaint Trends Tell the Whole Story

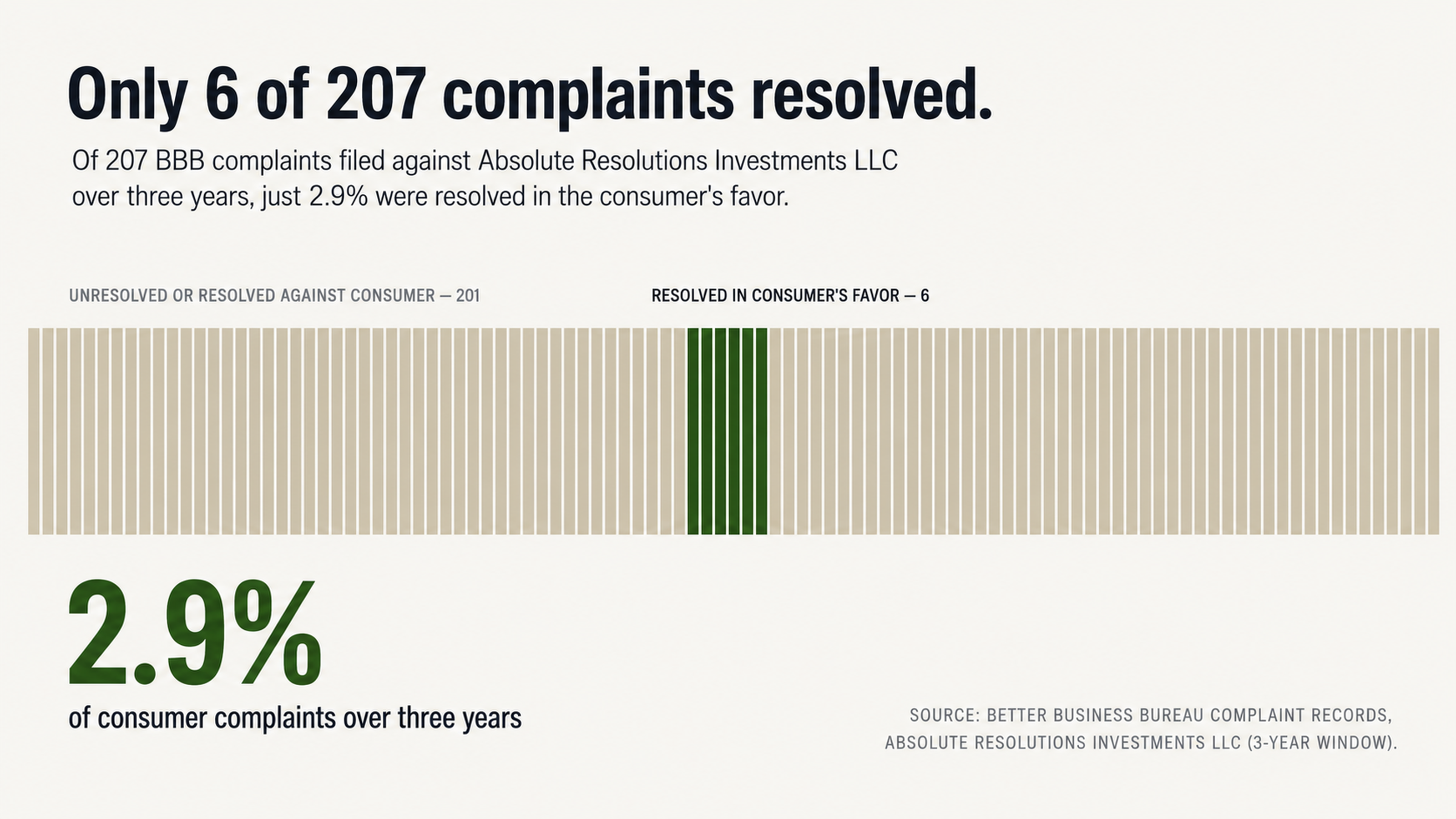

What the BBB Data Shows

The BBB shows ARI with a B+ rating but if you dig into the complaint resolution data, you will see that of 207 complaints filed over the last 3 years, only 6 of them have been resolved in favor of the consumer. The 2.9 percent resolution rate is evidence of a much bigger problem with the way the company is operating.

These complaints aren't just a warning system for consumers that are going to deal with the company in the future. They are evidence of systematic problems that can be used to support a dispute. When a company has demonstrated a pattern of not resolving legitimate consumer complaints, that pattern can be used to determine how the credit reporting agencies should consider the accuracy of information being furnished by the company.

One consumer filed a complaint with the BBB that stated: "I am filing this complaint because Absolute Resolutions Investments LLC is trying to collect on a debt that does not belong to me. They have reported false information, misrepresented the debt, violated numerous federal laws and are now suing me in Jefferson County, Texas for fraudulent and unverified debt."

Similar comments can be seen throughout consumer review websites.

What the CFPB Complaints Show

The most common issues with CFPB complaints include problems with credit reporting and debt validation. Many consumers have complained that the company is reporting the debts to the credit bureaus before they have been notified. Others complain that they requested validation and received a response that does not verify the debt and ARI's right to collect.

One complaint filed with the CFPB details a consumer that was a victim of identity theft: "I contacted the company and advised them this was a fraudulent account. They sent me an identity theft affidavit which I completed and returned. I also filed a police report and a report with the Federal Trade Commission. Absolute Resolutions has denied my claim that this is a fraudulent account and is refusing to review any additional documentation that I have to prove this account is not an account that I opened."

Comments like this are representative of a broader pattern in the data. The patterns indicate that the company is more interested in debt collection than it is in investigating whether the accounts are legitimate. When a debt collector ignores identity theft affidavits and other documentation that proves the account isn't accurate, it shows that they value expediency over accuracy.

Federal Court History

FDCPA Lawsuits

There have been approximately 200 federal lawsuits filed against Absolute Resolutions Corporation in U.S. District Court. Most of the cases involve allegations of violations of the Fair Debt Collection Practices Act. The cases provide a window into what the company is doing to generate the complaints.

In Velez v. Absolute Resolutions Investments, LLC the consumer alleges that the company violated the FDCPA when it sent a collection letter directly to him after they knew he was represented by an attorney.

In D'Amicantonio v. Absolute Resolutions Investments, LLC the plaintiff is alleging violations of the FDCPA, FCRA (failure to properly investigate disputed charges), and false credit reporting (the plaintiff won a court judgment in his favor).

Other cases have been filed in federal courts across the country. Hill v. ARI (Northern District of Illinois), Schmidt v. ARI (Southern District of Ohio), Manfredi v. ARI (Southern District of California), and Papariello v. ARI (Western District of Pennsylvania).

Class Action Lawsuits

The company has been exposed to two class action lawsuits. In October 2018, a proposed class action claimed that Absolute Resolutions Investments along with another company, made deceptive statements about debt dispute rights in collection letters. This is one of the FDCPA requirements; debt collectors must properly disclose dispute rights.

Five months prior, in May 2018, another class action claimed the company improperly identified the original creditors in collection letters. If a debt buyer misidentifies the original creditor, it makes it impossible for the consumer to verify whether the debt is owed or not. The class actions point to practices that, if true, would be clear violations of consumer protection laws.

Consumer Review Data

What the Rating Platforms Say

While the official rating platforms show an average rating, independent review sites are much more negative. Wallet Hub reviewers rate the company 1.6 out of 5 stars with 80 percent of the reviews being only one star. The discrepancy between rating and review is worthy of noting.

One reviewer in September 2024 wrote: "Reporting balances and payments incorrectly. Paid in full nearly 6 months ago and never late, yet they report 30 days late and a balance."

In March 2024 another reviewer wrote: "I was sent proof from the dispute team that clearly shows they are reporting incorrect dates by more than four years."

Perhaps the most disturbing review is from a consumer in March 2023: "ABR did not notify me before they placed this account on my credit report. If they notified me first, it would have been paid. I only found out about this account AFTER they reported it. I offered to pay if they would delete it, but they refused.”

The consumer is describing a practice of reporting debts to the credit bureaus before they notify the consumer. This defeats the purpose of the debt collection laws.

Debt Collection Lawsuits

What the Court Filings Say

ARI files thousands of debt collection lawsuits every year. In Texas, Michigan, Florida, California, Ohio, and Minnesota they are filing most of the lawsuits through Stenger and Stenger, P.C.

One reviewer described it this way: "They use bully tactics (lawsuits 2 days after buying old debt) to force you to pay even if it's not your account."

A consumer filed a complaint with the BBB claiming: "They delivered the documents to my brother. In the document it said I had to respond before a certain date but I was not given any documents but my brother was and I don't live at that address."

The consumer is claiming improper service of process which can be a basis for dismissal and potentially a counterclaim. ARI pursues thousands of lawsuits with the hope that the consumer does not respond to the lawsuit which would allow them to receive a default judgment.

If the consumer does respond and challenges the documentation, several consumer attorneys have indicated that ARI will become more willing to settle the matter quickly in order to avoid the costs of ongoing litigation. This shows that an informed consumer has more leverage in these situations than the debt collector wants them to know.

Your Leverage Points

The 30-Day Clock

If you dispute a collection account with the credit bureaus, they will initiate an investigation with the furnisher of the information. The investigation must be completed within a certain amount of time which is typically 30 days. If the collector cannot respond to the investigation and prove the information is accurate, the credit bureaus must delete or correct it.

This is not a trick or a loophole, it is the system working the way it should. If the information is not accurate, it should not be on your report.

Why Disputing is Better than Paying

Many consumers believe that paying a collection account is the only way to repair their credit. Paying the account will change the status from unpaid to paid but it will still be a negative mark on your report for years to come. You will have paid for the privilege of a cleaner report but the negative mark will still be there.

If you dispute first, you have the opportunity to challenge whether the account should be there at all. If the information is not accurate, is an error, or is fraudulent, there is a chance it will be completely removed. If it is removed, it will leave your report much cleaner than a payment arrangement ever could.

The law, the paperwork requirements, and the economic incentives of the debt buying business all stack in favor of informed consumers that know their rights. Collectors rely on urgency and intimidation to get you to pay quickly before you have time to figure out your options. Silence and the dispute process are the kryptonite of debt collectors.

The Bottom Line

What We Learned

Absolute Resolutions Investments, LLC is a legally incorporated debt collection company that has managed to accumulate over 305 complaints between the CFPB and BBB websites but has not been subject to any regulatory enforcement. The 2.9 percent complaint resolution rate, repeated allegations of failure to validate before credit reporting, and a pattern of filing debt collection lawsuits indicate a pattern of business practices that prioritize efficiency over compliance with consumer protection.

The lack of a regulatory enforcement action is not an indication that the company is operating correctly; it is an indication that the enforcement agencies are outgunned. Consumer complaints and federal lawsuits tell a more accurate story than any rating.

What to Do Next

If you have a collection from Absolute Resolutions Investments, LLC on your credit report, you should not panic. Based on the complaint history and the documentation weaknesses outlined in this report, it is likely that a formal dispute will get results if handled properly.

Credit repair experts understand how to navigate the dispute process effectively. They know what documentation to request, how to properly frame disputes under the law, and when a debt collector has failed to meet their burden of proof. In most cases, hiring a professional will yield better results than if you tried to advocate for yourself.

FightCollections.com fights debt collectors through the dispute process. We understand the weaknesses of the debt buying business model and how to use them to our advantage to represent consumers. If ARI is on your report, contact us for a free consultation where we can discuss the details of your case and your options for potential removal.