You requested a copy of your credit report, expecting to see the usual items on the report. Instead, you found an Evergreen Professional listing that you didn’t recognize.

Maybe it’s an old medical bill, an old debt, or maybe it’s something you’ve never seen before. Whatever the situation may be, you’re likely feeling a bit dismayed to see this on the report. This feeling is normal, but you shouldn’t worry about it. Instead, you should focus on how to deal with the Evergreen Professional listing. That’s what matters most.

Evergreen Professional Recoveries is a debt collection agency. Like most agencies, it has racked up its fair share of complaints. In fact, the Consumer Financial Protection Bureau lists more than 150 complaints against Evergreen Professional.

Moreover, the company has been sued in more than 80 federal cases. In 2021, Evergreen Professional agreed to pay a class-action settlement of $100,000 for accessing consumers’ credit reports without a permissible purpose. Knowing these facts about Evergreen Professional can help you decide how to handle the listing on your report.

Who is Evergreen Professional?

Evergreen Professional Recoveries, Inc. is a debt collection agency based in Washington State. If you need to contact the company, you can use the following information:

You can use this contact information to request debt validation. You should not use it to negotiate a payment or discuss the account over the phone.

A History of Complaints and Lawsuits

Evergreen Professional has been a Better Business Bureau-accredited business since 1994. Despite its long-standing accreditation, the company only has a B rating. Most companies with such a long history of accreditation have an A+ rating.

In the last three years, Evergreen Professional has had 45 complaints filed with the Better Business Bureau. In the last year alone, the company has had 20 complaints filed against it. The company’s rating on consumer review platforms is even more dismal. For instance, it only has a 1.4 out of 5-star rating on Google Reviews.

Evergreen Professional also has a history of lawsuits. In June 2021, a federal judge approved a class-action settlement in the case of Rodriguez v. Evergreen Professional Recoveries. The plaintiffs claimed that Evergreen Professional accessed their credit reports improperly while attempting to collect unpaid traffic tickets. The judge approved a settlement of $100,000. Approximately 250 class members benefited from the settlement.

Many of the complaints against Evergreen Professional describe similar experiences. Consumers say that the company calls them from multiple phone numbers, making it impossible to block the calls. Others claim that they receive voicemails in which the company threatens them. The company allegedly tells them that a dispute has been filed in their name and Social Security number.

Still, others say that the company’s billing amounts do not match the amounts that their original creditors billed them.

One consumer expressed her frustration with Evergreen Professional on WalletHub. Marie said, “If I could give them a zero stars, I would. Rude agents-argumentative and downright assholes.”

Why You Might be Able to Dispute the Listing

Missing Documentation and Incorrect Balances

According to a study conducted by U.S. PIRGs, 79% of credit reports contain errors or other serious inaccuracies. This is particularly true for consumers who are dealing with collection agencies. These agencies often buy debt portfolios from other companies or collect debts for multiple clients.

As a result, there may be missing documentation in the chain of custody. When this occurs, it may result in inaccuracies on consumers’ credit reports.

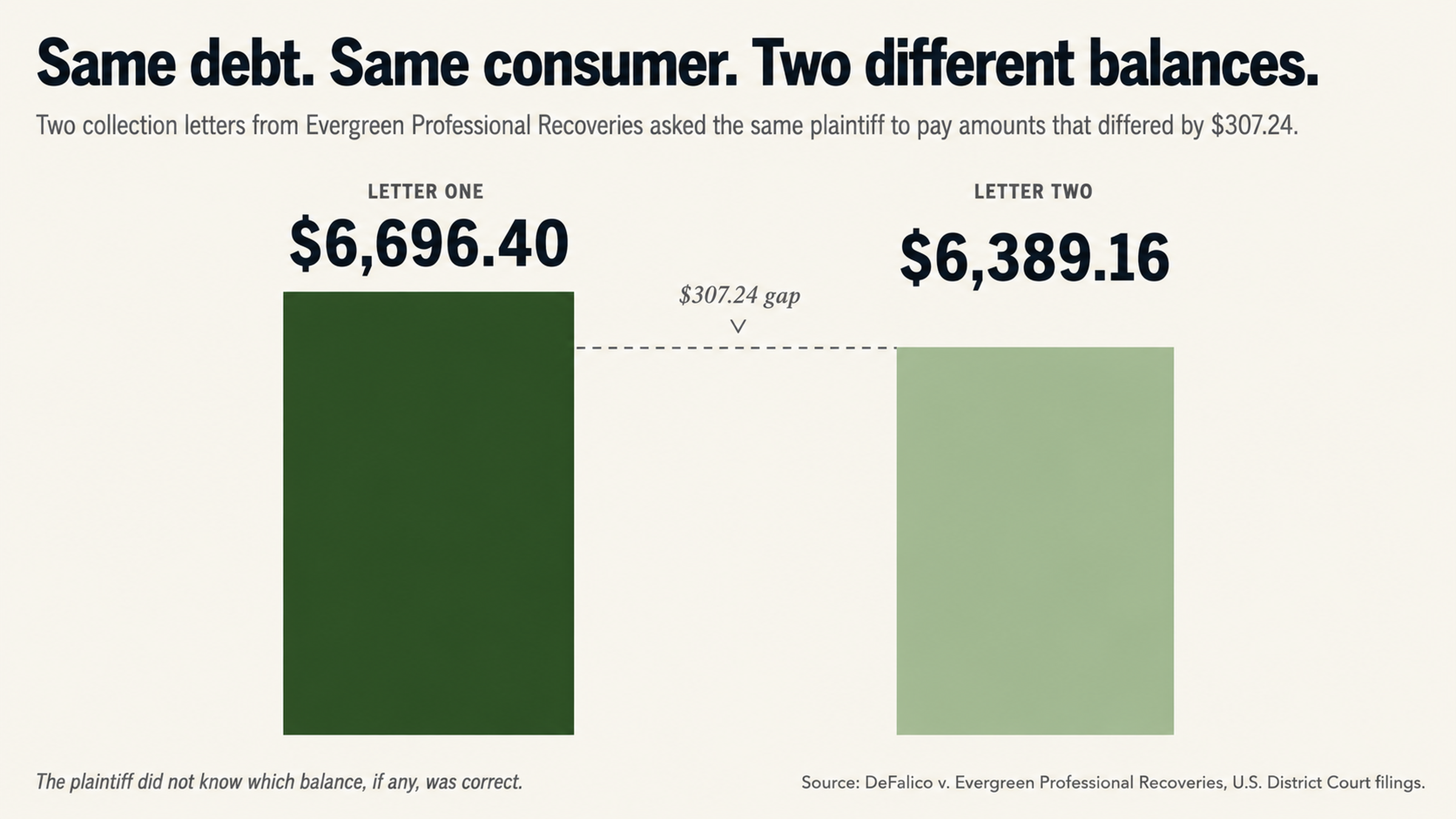

Evergreen Professional’s history illustrates this issue. In one federal lawsuit against the company, DeFalico v. Evergreen Professional Recoveries, the plaintiff claimed that she received two collection letters from the company. One letter said that she owed $6,696.40. The other letter said that she owed $6,389.16. The plaintiff did not know why there was a discrepancy in the balance or which balance, if any, was accurate.

This situation is not unique. Collection agencies operate on thin margins and may not have all of the documentation that they need to validate consumers’ debts. This can cause problems when consumers decide to dispute the listings on their credit reports.

The 30-Day Window for Responding to a Dispute

When you dispute a collection listing, federal law requires the credit reporting agency to investigate the dispute. The agency must respond to the dispute within 30 days. If the agency cannot verify that the information on the listing is accurate, it must remove the listing from consumers’ credit reports.

The burden of proof in these situations is not on consumers.

In other words, you do not have to prove that you do not owe the debt. Instead, the collection agency must prove that you owe the debt and that you owe the amount that it claims you owe. Moreover, the agency must show that it has followed the proper procedures in attempting to collect the debt. Many consumers have successfully removed collection listings from their credit reports because the collection agencies could not meet their burden of proof.

What You Should Not Do If Evergreen Professional Contacts You

Why You Should Not Call Evergreen Professional

If Evergreen Professional contacts you, your first instinct may be to call the number on the collection notice and try to resolve the issue. This is perfectly understandable, but it is not the best course of action. In fact, it may be the worst thing you can do.

When you talk to a debt collector on the phone, you may inadvertently admit that you owe the debt. You may also restart the clock on the statute of limitations. Moreover, you may provide the collector with information that it can use against you.

Collectors are professionals who are trained to negotiate. Most collectors work from a script that is designed to get you to pay as much as possible. You, on the other hand, are likely dealing with a debt collector for the first time. You do not know the script or the applicable laws. As a result, you are at a distinct disadvantage when you negotiate over the phone.

Evergreen Professional has a history of calling consumers from multiple phone numbers. The company also leaves lengthy voicemails that include threatening language. In some cases, the company may pressure consumers to resolve the issue immediately. If you respond to these tactics, you are playing the game on the collector’s turf. Instead, you should communicate in writing. This will give you the upper hand.

Your Right to Remain Silent

If a debt collector is calling you, you have the right to remain silent. You do not have to respond to the collector’s phone calls. In fact, doing so may be a mistake. The Fair Debt Collection Practices Act allows you to request that debt collectors stop calling you on the phone. If you make this request, the collector must stop calling you.

You should make this request for a couple of reasons. First, collection agencies try to create a sense of urgency. The agency may call you multiple times per day in an attempt to get you to pay the debt immediately. The agency may leave threatening messages on your voicemail. The goal of these tactics is to get you to pay the debt without verifying whether you actually owe it. If you respond to these tactics, you may end up paying a debt that is not yours or is not valid.

One consumer who dealt with Evergreen Professional said that a representative of the company told her, “With all due respect the time to do that was before, it is done, too late for that.” The representative said this when the consumer asked if she could make payments on the debt. This type of tactic can only work if you respond to the phone calls. If you ignore them, the tactic has no effect.

Fighting on the Right Battlefield

What the Evergreen Professional Listing Really Means

If you see an Evergreen Professional listing on your credit report, you should know what it really means. The listing is not really about whether you owe money to the debt collector. Instead, it is about the information that appears on your credit report and how long it stays there. This is an important distinction. If you recognize the difference, you can tailor your strategy to address the real issue.

Whether the listing says that you owe $500 or $5,000, it still has the same effect on your credit score. The existence of the listing is the problem, not the amount. With this in mind, your goal should be to get rid of any information on your credit report that is inaccurate, unverifiable, or simply incorrect. Paying the debt will not accomplish this goal.

Evergreen Professional, like many other collection agencies, has a poor rating with the Better Business Bureau. It also has a low rating on consumer review platforms.

Finally, it has many complaints filed against it. The company has these ratings because it does not need your business. Instead, the company collects debts through pressure, not customer satisfaction. Once you understand this dynamic, you can develop a strategy that takes it into account.

Why Paying the Debt May Make Things Worse

If you pay a collection debt, you may expect that the listing will come off of your credit report.

Unfortunately, this is not the case. Paying the debt will change its status from unpaid to paid, but the listing will still be on your report. A paid collection listing is still a negative mark that can affect your credit score. The listing will stay on your credit report for seven years. This seven-year clock starts on the original delinquency date of the debt.

Settling a debt for less than you owe may or may not help you. In some cases, settling a debt can actually hurt your credit score. This depends on many factors, including how the creditor reports the settlement and the age of the debt. Settling a debt is not a guaranteed solution to your problem.

Many of the complaints about Evergreen Professional say the same thing. Consumers who paid their debts still saw listings on their credit reports. One consumer reviewed Evergreen Professional on Google and said, “Charges keep showing up on my credit report even though I pay them through my insurance.” Paying a debt is no guarantee that the listing will come off of your report. On the other hand, you may be able to remove an inaccurate listing by disputing it.

How to Handle an Evergreen Professional Listing

How to Dispute a Collection Listing

You can dispute a collection listing by challenging the accuracy of the information that the debt collector provided to the credit reporting agency. If the collector cannot verify that the information is accurate within a reasonable period, the agency must remove the listing from your credit report. You do not have to actually owe the debt for the listing to remain on your report. The listing will stay on your report as long as the collector can verify the information.

You can remove information from your credit report if it is incorrect, erroneous, or fraudulent. You can also remove information if the collector cannot verify it within a reasonable period. Evergreen Professional has a history of providing incorrect balances and accessing credit reports improperly. The company also has a history of communicating improperly with consumers. For these reasons, you may be able to remove an Evergreen Professional listing by disputing it.

It is important to dispute the listing in the right way. If you dispute it incorrectly, you may actually strengthen the collector’s case against you. The collector may use your dispute as an opportunity to gather any missing documentation. Avoid this outcome by getting help with your dispute.

Why You Need Professional Help

If you have a collection listing on your credit report, you should consider hiring a professional to help you. These professionals understand the Fair Credit Reporting Act and the Fair Debt Collection Practices Act. They know what documentation the collector needs to provide to verify a debt. They also know how to identify errors that the collector may have made. With this knowledge, professionals can help you dispute a listing and remove it from your credit report.

If you try to dispute a listing on your own, you are at a disadvantage. The collector has experience with thousands of disputes and knows all of the tricks that consumers try. The collector also knows how to use the law to its advantage. A professional can help you level the playing field and come out with the best result possible.

Evergreen Professional has been the subject of more than 80 federal lawsuits. This fact suggests that when consumers have the right representation, they can successfully challenge the company’s practices. The same practices that make Evergreen Professional vulnerable to lawsuits also make it vulnerable to disputes. If you have the right representation, you may be able to remove an Evergreen Professional listing from your credit report.

Conclusion

If you see an Evergreen Professional listing on your credit report, do not panic. Instead, use the information in this article to develop a strategy. The company has a history of disputes and lawsuits, and you may be able to remove the listing by challenging its practices.

Do not call the company or attempt to negotiate a payment. Instead, communicate in writing and focus on your credit report. What appears on your report and how long it stays there is what really matters. With the right strategy and a little patience, you may be able to remove an Evergreen Professional listing and improve your credit score.

What You Should Do Next

If you see an Evergreen Professional listing on your credit report, you should not wait to take action. Every day that the listing appears on your report can cost you money in the form of higher interest rates and fees. Every day that the listing appears on your report can also cost you opportunities in the form of denied applications and credit denials.

The professionals at FightCollections.com can help you evaluate your credit report and decide how to handle an Evergreen Professional listing. We specialize in disputing questionable collection listings and have experience with agencies like Evergreen Professional.

Contact us today to get a free consultation. We can review your report and help you decide how to proceed.