Were you surprised to see a new collection account on your credit report?

When you checked your credit report, you may have expected to see your credit card accounts, maybe your student loan or your car loan, but instead you found a collection account from a company called LJ Ross Associates. You might not recognize the balance, and you might not even remember the original creditor.

Millions of people every year find mysterious collection accounts like this one on their credit reports. When this happens to you, it’s natural to feel a little panicked. You might be tempted to pick up the phone and call the collection agency to find out what’s going on and maybe even pay what you owe so the problem just goes away.

That’s exactly what the collection agency is hoping you’ll do.

Don’t make that phone call just yet, though. Instead, take a deep breath and remember that seeing a collection account on your credit report doesn’t necessarily mean you owe the debt. In fact, it’s possible that you have more power in this situation than you think.

Who is LJ Ross Associates?

LJ Ross Associates, Inc. is a third-party debt collection agency. The company is based in Jackson, Michigan and was incorporated there in October 1992, so it’s been in business for over 33 years.

The company provides collection services in all 50 states, plus the District of Columbia, and it holds a contract with the federal government. This means it collects debts owed to government agencies, as well as private debts. The company specializes in several types of debts, including:

- Utility bills (electricity, gas, water, etc.)

- Telecommunications debts (phone bills, etc.)

- Medical debts

- Government debts (court costs, citations, etc.)

What the Data Says about this Collection Agency

When you look at data from regulatory agencies, court records and consumer complaint databases, you start to see a less-than-flattering picture of this debt collection agency.

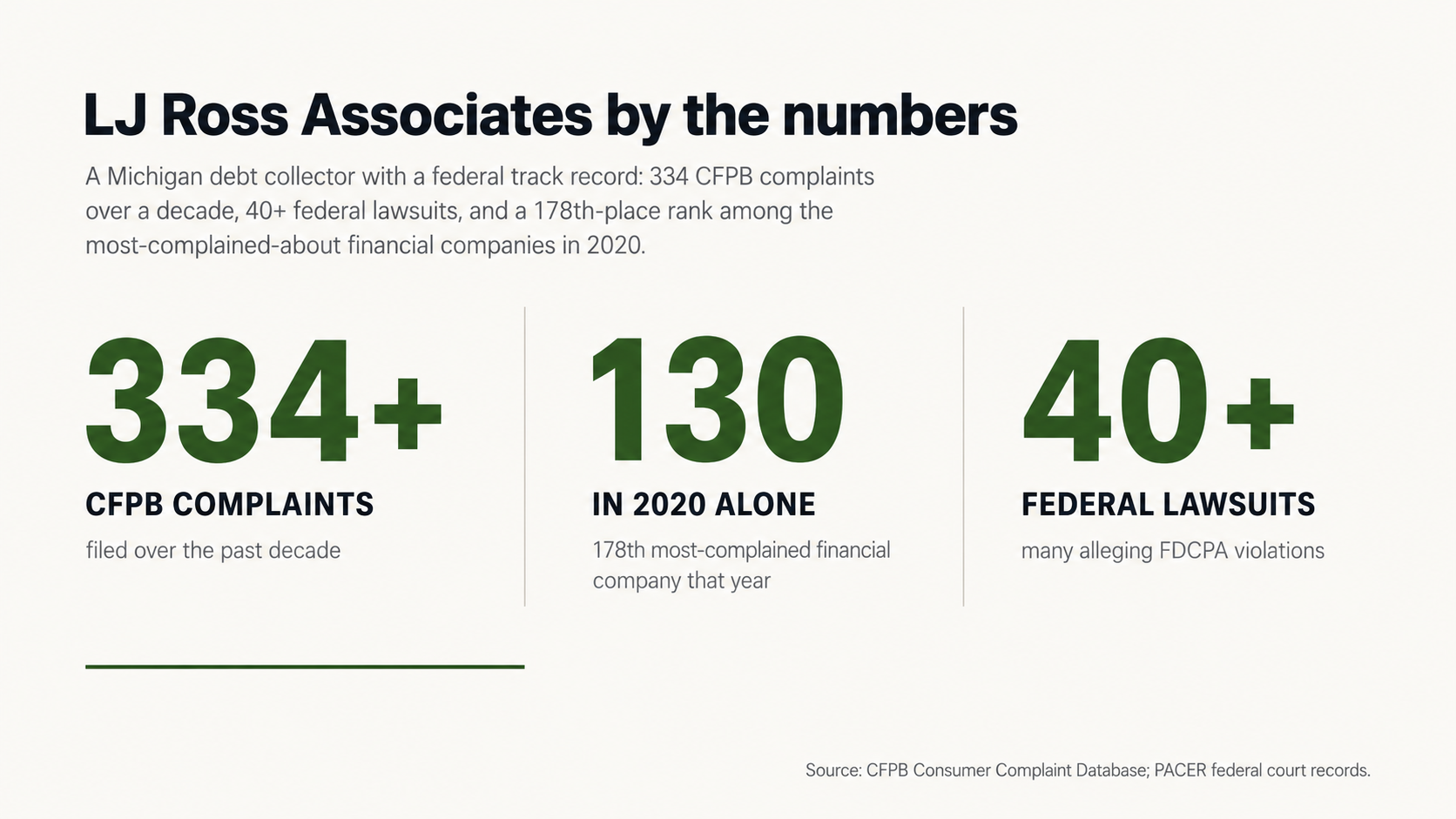

For example, although the Better Business Bureau (BBB) currently gives the company an A+ rating, it has also received 130 complaints filed with the Consumer Financial Protection Bureau (CFPB) in 2020 alone. In fact, according to the CFPB's Consumer Complaint Database, that made it the 178th most complained-about company in the entire financial industry that year.

Over the past decade, the CFPB has received more than 334 complaints about this collection agency.

The company has also been a defendant in more than 40 federal lawsuits, many of them alleging violations of the Fair Debt Collection Practices Act (FDCPA), a federal law that prohibits abusive, deceptive and unfair debt collection practices.

In one of those cases, for example, called Rosen v. LJ Ross Associates, Inc., a federal court ruled that the company violated the FDCPA when it misrepresented the amount that a consumer owed on a debt. As a result, the court entered a judgment against the company.

Why is LJ Ross Associates on My Credit Report?

What Kinds of Debts Does it Collect?

LJ Ross typically collects — or attempts to collect — debts that were originally owed to other companies, such as:

- Utility providers (electricity, gas, water, etc.)

- Telecommunications companies (phone, internet, TV, etc.)

- Health care providers (hospitals, doctors, etc.)

- Government agencies (parking tickets, court costs, etc.)

If you think back, you might remember that you once owed money to a company in one of these categories, but you never paid the bill. Alternatively, you might not remember the debt at all.

Either way, it’s likely that the original creditor eventually sold the debt to a debt buyer, such as LJ Ross Associates. Debt buyers purchase debts for pennies on the dollar, which means they pay the original creditor only a fraction of what you owed and then attempt to collect the full amount from you.

That’s an important point, because it means the collection agency has already made a profit, even if it doesn’t collect anything from you. However, the agency can make a lot more money if you pay up, so it has an incentive to pursue you aggressively.

How Does a Collection Account Affect My Credit?

When a collection account appears on your credit report, it’s considered a derogatory mark, or a negative entry. In and of itself, the presence of a collection account on your credit report can lower your credit score significantly.

That’s true even if the amount of the debt is relatively small. To lenders, a collection account is a sign that you have failed to pay a legitimate bill, so it indicates a higher level of risk.

What most people don’t realize, though, is that simply paying a collection account is not enough to remove it from your credit report. Instead, the status of the account is simply updated to show that it’s been paid, but the account itself remains on your credit report for up to seven years from the original delinquency date.

That means the damage to your credit score can continue long after you’ve paid what you owe.

The Problem with Paying a Collection Agency

Paying a Debt Doesn’t Remove It from Your Report

When you pay a collection agency, you’re essentially acknowledging that you owe the debt and that you’re responsible for paying it. As a result, the collection agency updates the status of the account to show that it’s been paid, but again, that doesn’t mean the account is removed from your report.

Many consumers are dismayed to find that their credit score doesn’t improve very much, if at all, after they pay a collection account — even if they paid hundreds or thousands of dollars to the collection agency.

That’s because paying a collection account does nothing to verify whether the information is accurate in the first place. In fact, studies have shown that up to 79 percent of credit reports contain errors or other serious mistakes.

That means there’s a good chance the collection account on your credit report contains at least some inaccurate information — and that can be grounds for having it removed.

Why Collectors Want You to Pay Right Away

Debt collectors make money when consumers pay up, so they want to create a sense of urgency that pressures consumers into acting quickly. That’s why every letter and phone call from a collection agency is designed to make you feel like you need to respond right away.

In reality, though, you have a lot more power in this situation than the collector wants you to know. So, before you do anything else, take some time to learn about your rights under the FDCPA and other federal laws.

Your Right to Remain Silent

You don’t have to respond to a collection agency’s phone calls or letters, and you don’t have to give a collector any information over the phone. In fact, it’s a good idea to say as little as possible until you have a strategy in place.

Why? Because anything you say can be used against you. For example, if you admit that you owe a debt or that you’re responsible for paying it, that can make it harder to challenge the debt later.

Similarly, if you give a collector information about your income or your bank account, that can make it easier for the collector to sue you or garnish your wages if you don’t pay up.

Why You Should Dispute the Debt

The problem is that debts like this one may change hands several times before they end up at a collection agency. Along the way, paperwork can get lost, and the collector may not have access to all of the information it needs to verify that you owe the debt.

Under the FDCPA, you have the right to request verification of any debt that a collector claims you owe. When you do that, the collector is required to provide you with documentation that proves not only that you owe the debt, but also that the collector itself has the right to collect it.

In some cases, collectors may not be able to provide that documentation. If that happens, the collector may drop the debt entirely, and it may even remove the account from your credit report.

What We Learned from Consumer Complaints about this Agency

A Pattern of Complaints against LJ Ross Associates

When you look at complaints that consumers have filed against this collection agency, you can start to see a pattern. Many consumers say that the company failed to validate debts that it was trying to collect, or that it was trying to collect the wrong amount.

Other consumers say the company was reporting inaccurate or fraudulent information to the credit reporting agencies.

You can find these complaints in several places, including:

- CFPB Complaint Database. This federal database collects complaints about companies in the financial services industry, including debt collection agencies. You can search the database by company name or by type of complaint.

- BBB Complaints. The Better Business Bureau collects complaints about all kinds of companies, including debt collectors. You can search its database by company name to see what other consumers have said about their experience with the agency.

Here’s what one consumer had to say about his experience with LJ Ross Associates:

“This company contacted me with a closeout amount and after I paid it the next day they reported the balance to the credit bureau. Shady business debt agency. I felt really good paying off the debt in the amount they reached out to me regarding. They assured me that was all I had to pay and it would be reported as paid. The very next day I got an alert that lowered my credit score for the balance they agreed to write off.”

Another consumer described getting daily automated calls from the company that, when answered, don’t connect to a live person.

Consumers who have already filed complaints like these can provide valuable insights and lessons for consumers who are facing similar situations.

What to Do When You See LJ Ross Associates on Your Report

Request Validation

If you see a mysterious collection account like this one on your credit report, the first thing you should do is challenge the debt. Don’t call the collection agency to ask if it’s really yours or to try to confirm the amount. Instead, send a written letter challenging the debt and requesting validation.

Under federal law, if you dispute a debt in writing within 30 days after you first hear from a collector about it, the collector is required to stop all collection activity until it provides you with proper validation.

That means the ball is in the collector’s court. Until it provides the necessary documentation, it can’t contact you or report the debt to a credit reporting agency.

Remember that validation is different from verification. To validate a debt, the collector must provide you with actual documentation, such as a copy of the original contract or a statement from your account. The collector can’t simply send you a printout that repeats the information it already gave you.

Many collectors can’t validate debts when consumers challenge them properly, so this strategy can be an effective way to get a collection account removed from your report.

Protect Your Personal Information

When you’re dealing with a debt collector, it’s a good idea to be careful about the personal information you share. Don’t give a collector your bank account information or your employer’s name, for example. Don’t even confirm your address or phone number.

In fact, it’s a good idea to keep the conversation to a bare minimum until you have a clear strategy in place. Here’s what one consumer said about an experience with this agency:

“They REFUSED to give us any information about a possible collection account until we divulged even more personal information. This was despite the fact they already knew who my family were, from our caller ID! I do not trust this company’s insistence on more personal data in the current ID theft environment.”

Instead, insist that the collector communicate with you in writing. That way, you have a paper trail that you can use to build your case if necessary.

Conclusion

If you see a collection account from LJ Ross Associates on your credit report, don’t panic. Instead, remember that you have the right to challenge the debt and to request verification.

In fact, given this collection agency’s history of more than 330 complaints with the CFPB and more than 40 federal lawsuits, plus a pattern of systemic problems documented in consumer complaints, there’s a good chance that the information on your report is inaccurate or incomplete.

Rather than reacting emotionally and paying the debt without investigating, take the time to understand your rights and develop a clear strategy. With a little knowledge and persistence, you may be able to remove this account from your credit report for good.

Take Control of Your Credit Report

Challenging a collection account on your credit report requires some specialized knowledge, including information about your rights under the FDCPA and the Fair Credit Reporting Act (FCRA).

Although you can dispute accounts on your own, working with a professional can make it easier and improve your chances of success.

At FightCollections.com, we help consumers deal with abusive debt collectors and remove errors from their credit reports. If you have a collection account from LJ Ross Associates on your report and you’d like to explore your options for removing it, contact us today for a free consultation.

Why You Should Work with a Professional

When you’re dealing with a collection agency, you’re up against professionals whose only job is to get money out of consumers like you. That means you need professional representation of your own.

Credit repair specialists understand the laws and the loopholes that collectors use. They know what documentation to request and how to word a dispute letter for the best results. Most importantly, they know that many collectors can’t verify debts when consumers challenge them properly.

So if you see an account from LJ Ross Associates on your credit report and you’re not sure what to do, don’t give up. Instead, contact us today to learn more about how we can help.