If you’ve noticed a McCarthy Burgess & Wolff listing on your credit report, you’re dealing with a collection agency that’s been in business for over 40 years. Knowing who they are is the first step in protecting your consumer rights.

Our Investigation of This Agency

In the three years of data available on the Consumer Financial Protection Bureau (CFPB) complaints database, there are 446 complaints against McCarthy Burgess & Wolff. This ranked the company 172nd out of 2,458 companies in the complaints database for debt collection companies. A persistent stream of complaints like this could be a good indicator for consumers who wish to dispute the debt.

Their clients include major credit companies such as Verizon, AT&T, Capital One, Wells Fargo, and HSN. In the past ten years, they claim to have collected over $1 billion in outstanding debts. The Better Business Bureau (BBB) reports that the company has an A+ rating and a 1.3-star rating based on 164 Google reviews.

At least six class-action lawsuits have been filed against McCarthy Burgess & Wolff for violations of the Fair Debt Collection Practices Act (FDCPA). One such case, Jones v. McCarthy, Burgess & Wolff, resulted in a settlement. A claims website was established for those affected. This history of class-action settlements may be another sign that there is a good basis for consumers to dispute the debt.

The Right to Dispute Any Collection

Why You Should Always Dispute Before You Pay

When any debt collector contacts you or appears on your credit report, you have very specific rights under federal law. The FDCPA and the Fair Credit Reporting Act (FCRA) set up a system where the burden of proof is always on the debt collector. Once you understand how to wield this legal power, you can assert your consumer rights.

According to research by U.S. PIRGs, 79% of credit reports contain errors or other major mistakes. If nearly 4 out of every 5 credit reports contains a mistake, it should not be assumed that a collection account on your report is accurate. By disputing a debt, you are testing to see if the debt collector is actually able to verify that you owe the debt.

When you pay a collection account, it does not impact how long the account is listed on your report. Whether you pay or not, the account will stay on your report for seven years from the original delinquency date. Having a paid collection on your report offers you no real practical benefit in terms of credit scoring over having an unpaid collection on your report (depending on the scoring model used).

What Debt Collectors Are Required to Verify

Under the FDCPA, specifically 15 U.S.C. Section 1692g, debt collectors are required to provide you with verification of the debt within 30 days of first contacting you. During that time, they are not allowed to continue collection efforts until they provide you with the requested verification.

The problem for debt collectors is that they often struggle to provide full documentation, especially for older debts that have been resold multiple times. When you look at the CFPB complaints about McCarthy Burgess & Wolff, you will see a pattern of the company’s struggles to provide the required validation.

“I requested a valid original instrument of indebtedness in its original form with my signature on it; Ms. [redacted] stated she will get an invoice and does not have to verify my signature is on it.”

Another example of the company’s struggles with verification comes from a different consumer complaint.

“McCarthy, Burgess & Wolff, Inc. has completely crossed the line. I paid off the one legitimate invoice I owed to HubSpot Inc., yet they continue to contact me nonstop demanding payment for additional accounts they refuse to verify or provide documentation for.”

If debt collectors are unable to document what they say you owe them, it may be possible to have the account removed from your report.

Known Patterns That Could Help You

Allegations of Third-Party Disclosure

The FDCPA prohibits debt collectors from discussing your debt with anyone other than authorized parties. The BBB has complaints that McCarthy Burgess & Wolff may have violated this portion of the FDCPA by contacting consumers at their workplace.

“A representative named [redacted] went to my workplace and spoke with [redacted], a person I do not know personally but who also works there. Mr. [redacted] told Mr. [redacted] to call him about my debt.”

Another CFPB complaint describes the company reaching out to a family member:

“On XX/XX/XXXX the office of McCarthy McCarthy Burgess & Wolff contacted my mother on her personal cell phone about a purported debt I owed. She immediately stated the name of her company, which intentionally sounds like a law firm trying to make my mother think I was being sued.”

If debt collectors are illegally contacting third parties to discuss your debt, it could be a sign of a larger pattern of behavior that could strengthen your case to dispute the debt.

It’s helpful to understand that if a debt collector is willing to break the law in one way, they may be breaking it in other ways as well. There could be a pattern of behavior that indicates the debt collector is not following all of the required protocols. This could include documentation and verification issues that could make it easier to dispute the debt.

Collecting from the Wrong Person

One of the most egregious errors a debt collector can make is attempting to collect a debt from the wrong person. If this happens, you could dispute the debt and have the collection account removed from your report. There are several complaints that indicate McCarthy Burgess & Wolff may have made this error.

“Firm left me a voicemail. I returned the call. Lady starts asking me questions about what business I called regarding. I told her that I sold all of my previously owned companies 2 years ago.”

Another example of potential identity mix-ups comes from a different consumer.

“I have been receiving phone calls from this company for many months, understanding that I was not an officer nor shareholder of a company I was laid off from in 2022.”

If debt collectors are attempting to collect debts from the wrong people, it’s likely a sign that the company does not have the documentation to prove that the correct person actually owes the debt. This could make it easier to have the debt removed from your report through the dispute process.

Why You Should Stop Answering Their Phone Calls

Why Ignoring Their Phone Calls Could Help You

Debt collectors want to get you on the phone because it gives them the opportunity to ask you questions and apply pressure to try to get you to pay the debt or acknowledge that you owe it. Every time you talk to a debt collector on the phone, you could inadvertently make legal mistakes that damage your consumer rights. It makes sense to ignore their phone calls and block the numbers to stop the harassment.

You are not being rude by refusing to answer their phone calls. You have the legal right under the FDCPA to demand that debt collectors stop calling you on the phone. If you send them a cease communication letter, they are legally required to stop calling and communicate with you only through the mail. This will give you a paper trail that could be helpful if you decide to dispute the debt or file a lawsuit against the debt collector.

When you look at the reviews on the BBB website, you will see descriptions of how aggressive McCarthy Burgess & Wolff can be on the phone.

“This company is viscous and will call you 7 days a week regardless of what time it is. Their representatives are extremely rude.”

You do not have a legal obligation to answer their phone calls or respond to their tactics.

The Original Creditor Does Not Care

When a debt gets sold to a collection agency, the original creditor has already written off the account and moved on. They have already received the tax benefits of a write-off and no longer have a vested interest in whether the collection agency successfully collects the debt or not.

The moral obligation argument that debt collectors try to make about consumers honoring their debts ignores this reality. Collection agencies buy debt portfolios for pennies on the dollar and then attempt to collect the full amount (plus fees). This means that even when they collect partial payments, they are making a significant profit. Understanding this dynamic can help you see why their sense of urgency is really just about their interests and not yours.

If you refuse to talk to debt collectors on the phone, you are not providing them with any information that they can use against you. A professional credit repair expert understands how to communicate with debt collectors through the proper legal channels while protecting your rights throughout the process.

The Dispute Process

How a Professional Disputes a Debt

Under the FCRA, credit reporting bureaus have 30 days to investigate any disputed debt. As part of the investigation, they contact the entity that provided the information (in this case, McCarthy Burgess & Wolff) and ask for verification of the debt. If the debt collector is unable to verify that the information on the debt is accurate, the credit reporting bureau is required to delete or correct the information.

A professional dispute expert can identify the most likely successful grounds for disputing any given debt. This could involve challenging the accuracy of the reported balance, questioning the ownership documentation for the debt, or highlighting inconsistencies in reported dates. Each dispute is targeted at the most likely weaknesses in the debt collector’s documentation.

If you try to dispute debts on your own, you are at a disadvantage. Debt collection companies process thousands of accounts every month. They understand how to respond to credit bureau inquiries in ways that preserve their reporting. Having a professional intervene levels the playing field because the expert understands how dispute procedures and debt collector responses work.

What is Required for a Successful Removal

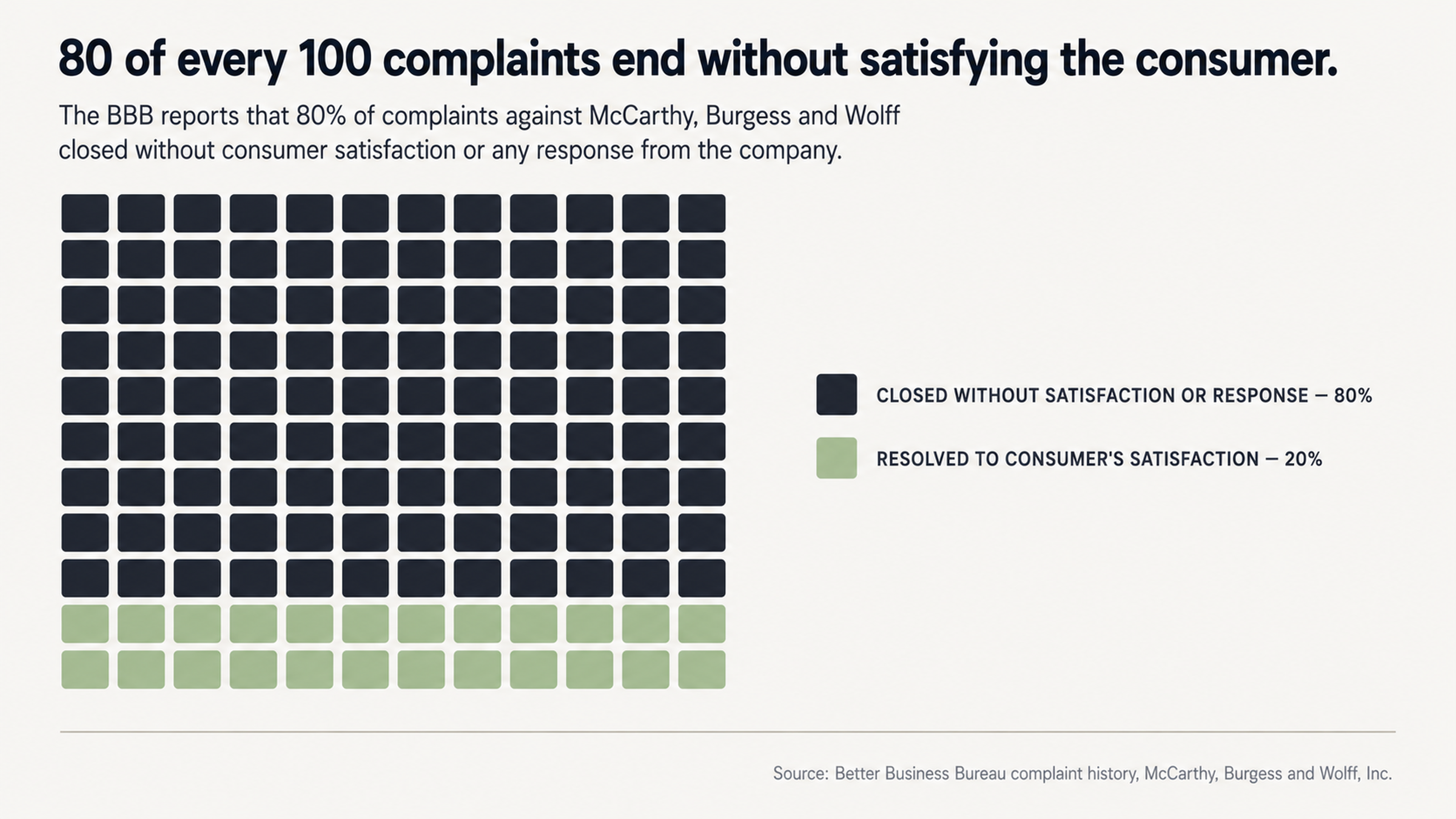

Debts can be successfully removed if the information is inaccurate, erroneous, fraudulent, or if it cannot be verified in a timely manner. The BBB reports that 80%of complaints against McCarthy Burgess & Wolff were closed without a consumer being satisfied with the company’s response or without any response at all. This could indicate that the company struggles to provide adequate documentation of debts in their portfolio.

We also know that there have been several class-action settlements against McCarthy Burgess & Wolff based on alleged violations of the FDCPA. If the courts found sufficient evidence to settle these cases, it could indicate that there are broader documentation or compliance issues that impact the accuracy of debts being reported on credit reports.

It makes sense to address any situation as soon as possible before it escalates further. Although debt collectors may threaten you with a lawsuit, the reality is that most collection accounts never result in any legal action. Getting professional guidance as soon as possible helps you respond strategically instead of reacting emotionally to debt collector harassment.

Protecting Your Report

Your Rights are Your Power

If you see a listing for McCarthy Burgess & Wolff on your credit report, it does not mean you have to accept it or pay it. Under federal law, you have the right to challenge, dispute, and demand verification of any collection account. Based on the complaint history and the history of settling class-action lawsuits, it seems clear that this is a company that may struggle to meet those verification requirements.

For a long time, debt collectors had the upper hand because they understand the system and consumers felt overwhelmed. By accessing professional expertise, you can eliminate that advantage and apply pressure in the proper legal channels. By always disputing before you pay, you are testing whether the debt collector can actually prove that you owe the debt.

Every day that a collection account is on your report, it is affecting your financial options. Disputing through the proper channels gives you the opportunity to have the account removed without the negative side effects of making a payment (which would not remove the account or change how long it stays on your report).

Get Your Free Case Evaluation Today

A free consultation allows you to understand your options without any risk or obligation. Our expert team will review what McCarthy Burgess & Wolff is saying about you and evaluate potential grounds for dispute. We will explain your options clearly so you understand what to do next. This evaluation provides you with the intelligence you need about your situation before you decide how to proceed.

FightCollections.com specializes in advocating for consumers against debt collectors through the credit reporting dispute process. We understand the patterns identified with companies like McCarthy Burgess & Wolff and how to leverage them in a dispute strategy. Our approach always puts your rights first and forces debt collectors to meet the verification burdens required under the law.

Contact FightCollections.com today to start your free case evaluation. Do not let debt collection companies dictate your credit future. Your legal rights are in place to protect you. Use them.