A collection account from Mercantile Adjustment Bureau on your credit report can be frightening. It’s natural to want to pay it off as soon as possible, but that’s rarely the best option.

Before we jump into whether you should pay or dispute this collection, you need to know a few important facts about this company. Then, we can talk about what you can do to get rid of it on your credit report.

What is Mercantile Adjustment Bureau?

Mercantile Adjustment Bureau was a debt collection agency that operated for over 94 years before it closed its doors on August 29, 2025. The company was based in Williamsville, New York, and worked with healthcare providers, utilities, banks, and universities to collect debts.

In October 2021, Australian fintech company Remitter USA acquired Mercantile Adjustment Bureau after the debt collector raised $12 million in capital. However, less than four years later, the company shut down.

What We Know about This Collection Agency

During the last few years of its operation, Mercantile Adjustment Bureau racked up a concerning track record. In July 2023, the Connecticut Department of Banking fined the company $30,000 and prohibited it from conducting business in the state for three years. The company was found to have collected debts without licenses and failed to maintain trust accounts for consumer funds.

Over 80 federal lawsuits accused Mercantile Adjustment Bureau of violating the Fair Debt Collection Practices Act (FDCPA) and the Telephone Consumer Protection Act (TCPA). Consumer law firms say that the company had a history of sending deceptive collection letters, leaving improper voicemails, and continuing to contact consumers after they requested to be left alone. The company is not accredited by the Better Business Bureau and averaged a one-star review from customers.

Myth: You Have to Pay a Collection to Remove It from Your Report

The Truth about Paying a Collection

You probably think that paying a collection will improve your credit, and that’s why it’s so tempting to pay it off as soon as possible. But is that what really happens?

When you pay a collection, it changes the status of the account from unpaid to paid. But the collection will still remain on your credit report for up to seven years from the original delinquency date. And paying the collection does nothing to prevent it from affecting your credit score throughout that period.

Additionally, paying a collection can reset the statute of limitations in some cases. This can give the debt collector more time to collect the debt. And, as you’ve seen with Mercantile Adjustment Bureau, the company has a history of attempting to collect debts from 10 years ago.

One consumer reported to the Better Business Bureau that Mercantile Adjustment Bureau would attempt to collect debts that were a decade old, debts that the consumer did not owe.

Why You Should Dispute First

Research has shown that a staggering number of credit reports contain errors. In fact, according to a study by U.S. PIRGs, 79% of credit reports contain errors or serious errors. This can include accounts that don’t belong to you, incorrect balances, duplicate accounts, and debts that you’ve already paid or discharged.

If there’s an error on your report, you have the right to dispute it and request that it be removed. If you pay first, you’ll give up your right to dispute the debt.

Myth: A Collection Agency Always Has Documentation

In reality, many debt collectors don’t have the documentation they need to collect a debt. When the original creditor sells debts to collection agencies, the documentation may not always follow. In some cases, you may find that the debt collector doesn’t have account statements, a signed contract, or a record of past payments. All they may have is a spreadsheet with your name and the amount you supposedly owe.

When you dispute the debt, the collection agency will have to verify the debt. And in many cases, debt collectors can’t provide the verification you need. This is why it’s so important to dispute the debt before you pay it.

Mercantile’s History

Mercantile Adjustment Bureau’s history shows that the company had a hard time verifying debts. In several federal court cases, the company was accused of failing to identify the current creditor, failing to state the amount of the debt correctly, and failing to provide validation of the debt. These practices were repeated in dozens of cases against the company.

In addition, when the Connecticut Department of Banking investigated the company, they were unable to determine the company’s “financial responsibility, character and fitness.” If the state couldn’t verify the company’s business practices, how can you trust them to verify your debts?

Several consumers reported to WalletHub that the company would attempt to collect debts without explaining where they came from, and the company would refuse to remove disputed debts from credit reports.

Myth: You Have to Respond to Every Debt Collection Call

It’s illegal for debt collectors to harass consumers, and you have the right to limit the amount of contact you have with a debt collection agency. In fact, if you request that a debt collector stop contacting you, they must abide by your wishes.

So why do debt collectors call so frequently? They want to apply as much pressure as possible to get you to pay a debt, and they hope you’ll respond before you have time to think twice.

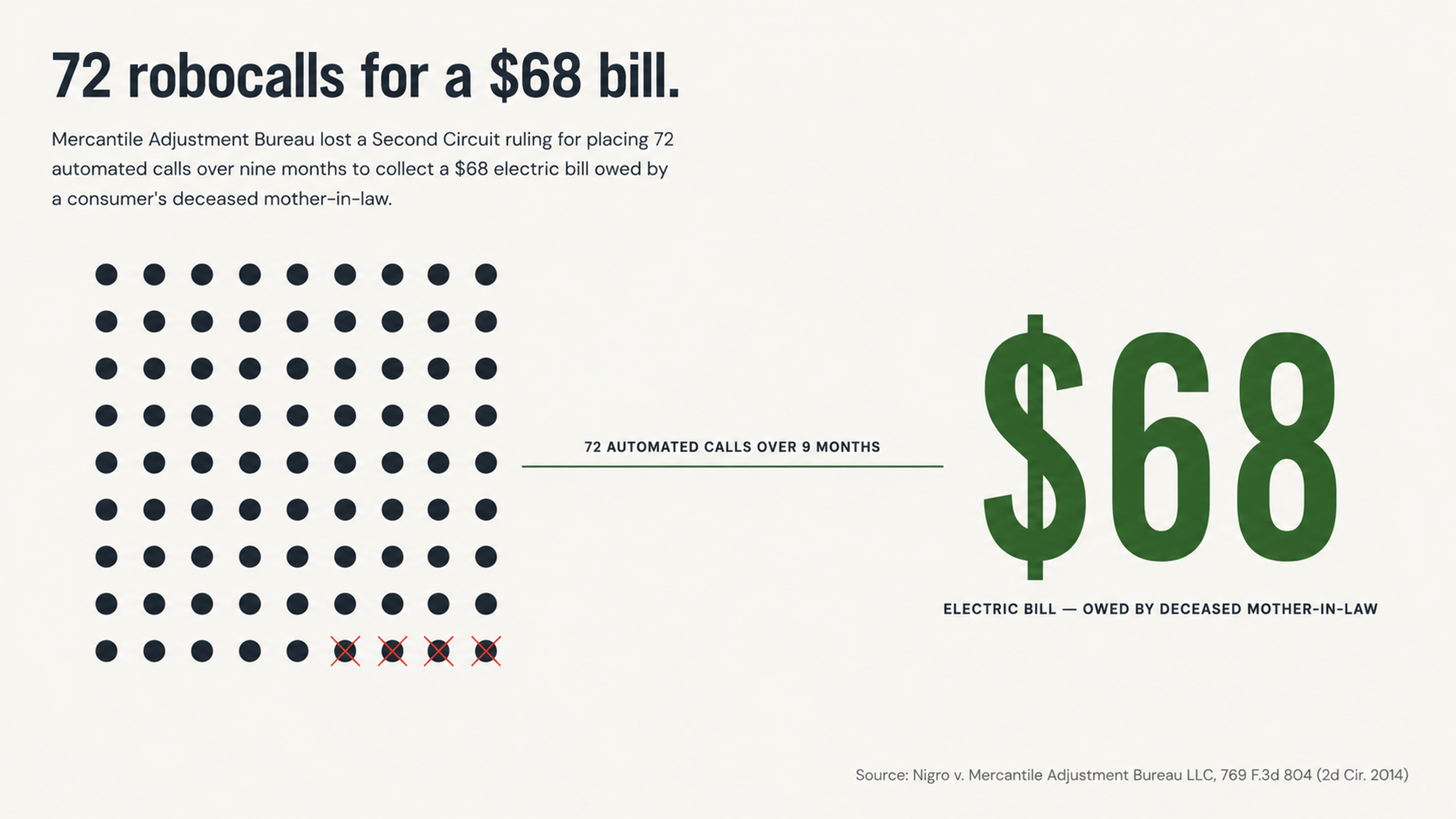

In the case of Nigro v. Mercantile Adjustment Bureau, the debt collector placed 72 automated calls to a consumer over the course of nine months in an attempt to collect a $68 electric bill the consumer’s mother-in-law owed before she passed away. The company lost the case in the Second Circuit Court, but it shows how far a collector will go to collect even a small debt from someone who may not owe it.

Why You Should Ignore Debt Collection Calls

Every time you speak with a debt collector, you give them the opportunity to gather more information from you and pressure you into making a commitment to pay a debt. Debt collectors negotiate debts all day, every day, but chances are this may be the first time you’ve dealt with a debt collection agency.

People have told attorneys at the consumer law firm Graham and Borgese that Mercantile Adjustment Bureau representatives have made “false, serious threats” and used “abusive language” to coerce consumers into paying debts. In other cases, Mercantile Adjustment Bureau representatives have misrepresented themselves as attorneys.

If you don’t answer the calls, you won’t have to deal with these tactics. Instead, work with a credit repair professional who can help you navigate the dispute process and communicate with debt collectors on your behalf.

Myth: Only Fake Accounts Can Be Removed from Your Credit Report

You don’t have to be the victim of identity theft to have an account removed from your credit report. In addition to fraud, you can have an account removed if the information is inaccurate, if you’ve already paid the debt, if the statute of limitations has run out, or if the collector can’t verify the debt within the allotted time period.

Federal law requires credit reporting agencies to only report accurate and verifiable information about you. So if you dispute an account, the credit reporting agency has 30 days to investigate and respond. If the collector can’t verify the debt during that time, the agency must remove the information from your report. Many debt collectors can’t keep up with verification requests because they work on tight profit margins and handle a high volume of accounts.

What Happens When a Collector Can’t Verify a Debt

When Mercantile Adjustment Bureau closed its doors in August 2025, it became even harder for consumers to get verification of debts. People who made payments in the months leading up to the closure are now finding that original creditors have no record of those payments.

In October 2025, one man reported to the Better Business Bureau that he’d agreed to a payment plan with Mercantile Adjustment Bureau in January 2025. He made payments until July 2025, only to discover in October that the company had closed in August. When he contacted the original creditor, they told him he still owed the original amount due because they had no record of the payments he made.

If you’re facing a similar situation, it’s essential to work with a credit repair professional. With the right documentation and timing, you may be able to get the debt removed from your report.

Myth: You Should Always Try to Handle a Collection Yourself

The truth is that debt collectors have a lot more information about the way the system works than you do. Debt collectors deal with thousands of accounts and understand the timing, documentation, and legality of credit reporting.

Most consumers only deal with the credit reporting system when something goes wrong. So when a debt collector calls, it’s easy to get sucked into vague threats and misleading information about your options. One man who reviewed Mercantile Adjustment Bureau on Yelp said the company wouldn’t provide receipts for payments and that it was nearly impossible to get a live person on the phone.

Why You Should Hire a Professional

Credit repair professionals work with debt collectors every day and understand the dispute process. They know what kind of documentation to ask for, how to spot errors in credit reports, and when debt collectors are violating federal law.

Reaching out to a credit repair professional as soon as possible can help prevent the situation from getting any worse. The sooner you start the dispute process, the sooner you can challenge any inaccurate or unverifiable information on your report and potentially have it removed. The longer you wait, the more time the debt collector has to report negative information and attempt to collect the debt.

When you see a collection on your credit report, it’s tempting to pay it and hope it goes away. That’s exactly what the collector is hoping for.

Don’t fall for it. Credit repair professionals can help you navigate the system and come out ahead. It’s always a good idea to do your research and reach out to a credit repair professional who can give you advice based on your individual circumstances.

Conclusion

Mercantile Adjustment Bureau’s history of violating federal law and state regulations is a reminder that you should never assume a debt collector has the right to damage your credit. The company’s unexpected closure in August 2025 left consumers with no way to verify payments or access documentation, and it’s not an isolated incident.

The common myths about paying collections, responding to debt collectors, and assuming debt collectors have the documentation they need all benefit the collector, not you. Paying a collection immediately, responding to every call, and assuming the collector has documentation all put you at a disadvantage before you even start.

Instead, adopt a dispute-first mentality. You have the right to dispute inaccurate information, and errors are incredibly common. You also have the right to request documentation, and collectors frequently don’t have what they need to verify a debt.

So what should you do now?

If you have a Mercantile Adjustment Bureau collection on your credit report, don’t pay it until you understand your options. Don’t respond to collection calls or try to negotiate on your own. In fact, the company’s closure may even work in your favor because it will be even harder to verify accounts.

Contact FightCollections.com today for a free consultation. Our team of experts can help you dispute collection accounts and determine whether the Mercantile Adjustment Bureau account on your report contains an error, can’t be verified, or can otherwise be disputed. You have more power in this situation than you think. Let us help you claim it.