If you see an unfamiliar debt collection agency on your credit report, that is a cause for concern.

But if you find that the agency is Revco Solutions, you need to be aware that you are dealing with one of the largest debt collection companies that specialize in healthcare debt. So, let’s learn more about who they are and how they operate.

Revco Solutions is a nationally licensed debt collection agency that has a private equity company as a parent organization and call centers in the U.S. as well as Panama, Tijuana, and Managua. That tells you a little bit about their size and resources but also their weaknesses.

Who is Revco Solutions?

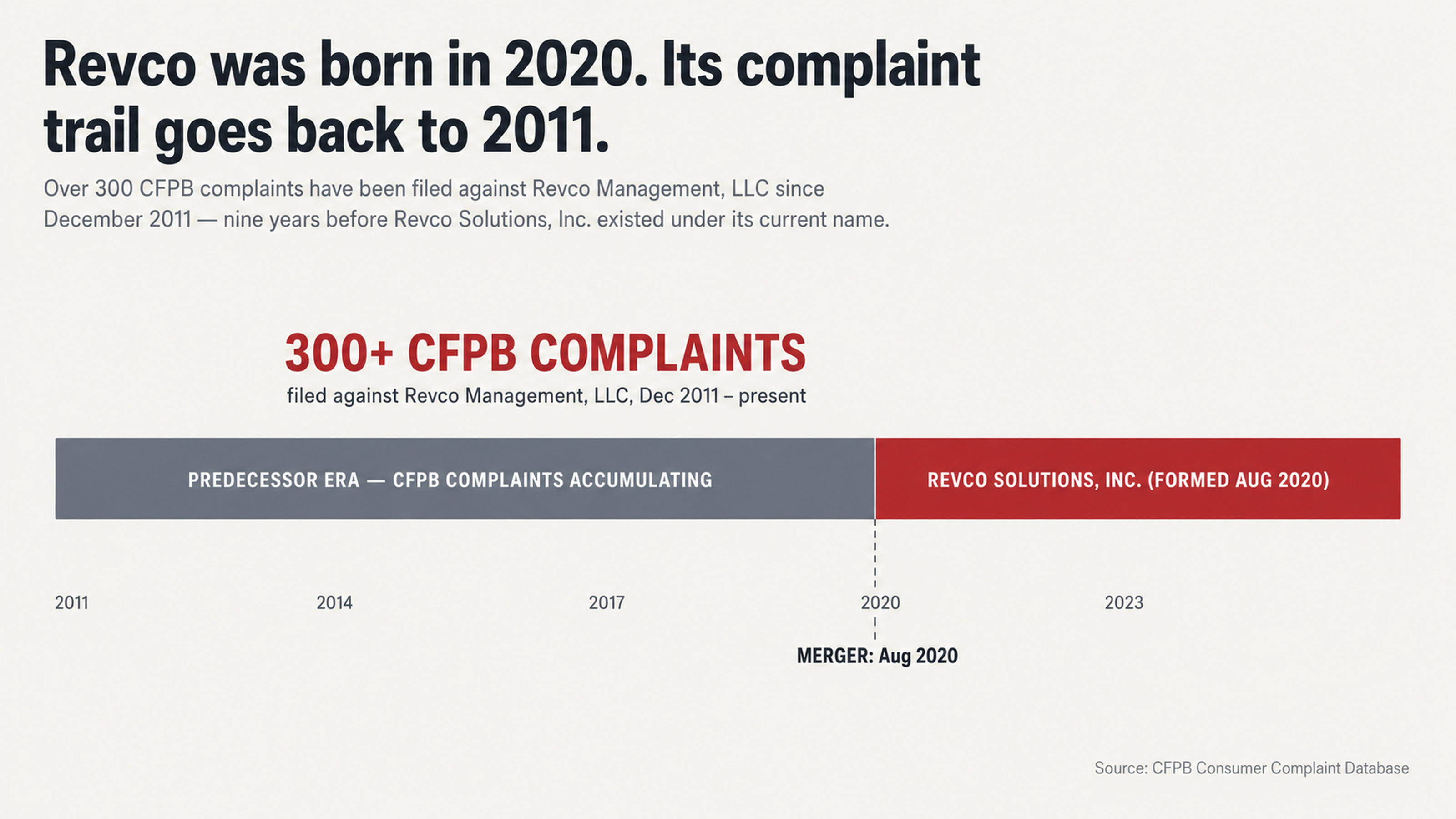

Revco Solutions, Inc. is a debt collection agency that was formed in August 2020 after the merger between Credit Bureau Collection Services (established in 1947) and Professional Recovery Consultants (established in 1979).

They are owned by Revco Management, LLC, which is a portfolio company of Longshore Capital Partners and co-investor LaSalle Capital Group. Being backed by a private equity company means that Revco has a lot of pressure to collect as much money as possible and deliver returns to their investors.

The Scale of Operations

According to their website, Revco Solutions has partnerships with over 4,000 healthcare providers in the United States. These include some of the largest non-profit health systems in the country. They say they have “billions in placements annually” and that they collect not just medical debt but also utility bills, government receivables, telecommunications balances, and financial institution charge-offs.

The company has twelve locations in the U.S. — in Florida, Michigan, Ohio, New Jersey, Nebraska, Indiana, Texas, Colorado, and Tennessee — and offshore call centers in Panama City, Tijuana, and Managua. Clearly, Revco is a big operation and they are capable of calling consumers around the clock.

But despite their claims to be a responsible business, their reputation with consumers is far from spotless. For example, they have a B- rating from the Better Business Bureau, which specifically notes that the company failed to respond to complaints filed against them. Their Google rating is just 1.3 stars, based on 130 reviews.

The Complaint Record Exposed

Federal Complaint Volume

According to the Consumer Financial Protection Bureau's complaint database, there were over 300 complaints filed against Revco Management, LLC dating back to December 2011. That’s a pretty high volume of complaints, especially considering that they have only been in business since August 2020. Most of the complaints fell into the following categories:

Trying to collect debt I don’t owe

Failed to provide a written validation notice

False statements or representation

Debt is not mine

Harassment called me repeatedly

Notifies consumer through other means

Complaints filed with the Better Business Bureau

The BBB reports that they have received 87 complaints in the past three years and 30 in the past year. But perhaps the most damning detail is this, from the BBB’s website: “BBB has not received a response from this business regarding six complaints filed against this business.”

If a business ignores six complaints that were filed through an official channel like the Better Business Bureau, that says a lot about their values and priorities.

What Consumers Are Saying

When you read through the complaints filed against Revco, you see the same themes popping up again and again. For example, here is what one consumer wrote in a complaint filed with the BBB in November 2025:

“I am writing this complaint because I have been receiving repeated and harassing phone calls from this company claiming to be Revco. They call me every day and when I answer, there is only silence. I believe they are harassing me and possibly attempting to defraud me because they will not provide me any information in writing or validate any debt.”

There’s another complaint on the BBB website from a consumer who said:

“They called me as I was going to the hospital for surgery and they kept me on the phone for 45 minutes. I finally had to hang up on her because she was screaming at me on the phone.”

In both cases, you see the same MO from Revco Solutions. They are using phone calls to try to pressure consumers into paying debts they may not owe or may not even recognize. In some cases, they appear to be targeting consumers when they are in a vulnerable state, such as when they are on their way to the hospital for surgery.

Clearly, this is a company that has no qualms about playing hardball with consumers in order to get what they want.

Vulnerable Populations Under Fire

Disabled Veterans Targeted

One theme that emerged from the complaints filed against Revco was the treatment of disabled veterans. In multiple complaints, disabled veterans described how they were being harassed over medical debts that they had already paid — or in some cases debts that had been paid by the Veterans Administration.

For example, here is what one disabled veteran wrote in a complaint filed with the BBB in March 2024:

“I am a Disabled Veteran who was listed as a debtor for emergency ambulance care which had already been paid in full by the VA. Despite the debt being closed out they called me repeatedly including 4 times in less than 5 minutes. They threatened me with bodily harm over the phone.”

The fact that Revco was attempting to collect a debt from a disabled veteran that had already been paid by the VA is a huge red flag. Not only does it suggest that the company has engaged in harassing and abusive behavior but it also indicates that they have failed to do their due diligence and verify the debts they are attempting to collect.

Another disabled veteran filed a complaint with the BBB in August 2024 in which he described Revco Solutions as “Absolutely disgustingly negligent or just straight FRAUDULENT and need to be investigated.” According to the complaint, the veteran had an $1,800 “ER bill that the VA and I for 3 years have been trying to get them to bill to the correct location and they refuse to send to proper VA billing department.”

If a debt collector is attempting to collect a debt from someone for three years when in fact the debt had already been paid, that suggests some pretty lax verification procedures. But it also highlights the fundamental problem with the debt buying business model, which is that it often relies on documentation that is incomplete or simply not available.

If the original creditor has written off the debt and sold it to a debt buyer, chances are that a lot of that documentation is gone. And that creates an opportunity for consumers who know how to protect their rights. If Revco Solutions cannot produce an original signed contract, a complete payment history, and proof that they own the debt, they are in a very weak position. So what can consumers do about this?

Documentation Failures

One of the dirty little secrets of the debt collection industry is that many agencies purchase debts from the original creditor for pennies on the dollar and often do not receive the underlying documentation. When a hospital or utility company decides to write off an account as uncollectible, they sell it to a debt collection agency, which may not receive all of the records for that account.

That means that in many cases the debt collector may not have the documentation to prove that the consumer actually owes the debt or that they have the legal right to collect it. That’s why it’s so important for consumers to understand their rights under the Fair Debt Collection Practices Act (FDCPA), which is a federal law that regulates the behavior of debt collection agencies.

If you believe that Revco Solutions or any other debt collector has violated your rights under the FDCPA, you may be entitled to file a lawsuit and recover damages. You could be awarded $1,000, plus actual damages as well as attorney fees and costs. Don’t hesitate to contact us to learn more about how we can help you.

Ongoing Federal Lawsuits Highlight Revco’s Liabilities

Federal Court Allegations

There is currently pending federal litigation against Revco Solutions. The case was brought by Bundy et al. v. Revco Solutions, Inc. on May 29, 2024, in the United States District Court, Southern District of Ohio, Eastern Division. The complaint alleges that Revco Solutions has violated at least five different provisions of the Fair Debt Collection Practices Act (FDCPA).

The plaintiffs specifically claim that Revco has violated the law with communication with third parties, harassing conduct, false representations, unfair practices, and failure to send a required validation notice within five days. Additionally, the consumers claim that Revco has violated the Ohio Consumer Sales Practice Act (OCSPA).

In the complaint, the consumers claim that Revco applied unauthorized credit card processing fees to their agreed-upon settlement amount, or misapplied funds in a way that resulted in the consumers’ balance being higher than what they agreed to pay.

The complaint even details Revco Solutions contacting the consumer’s daughter three times in a one-minute span. Such rapid-fire contacting of third parties can potentially implicate a number of different provisions of the FDCPA.

The lawsuit seeks actual and statutory damages under the FDCPA, as well as treble and punitive damages under the OCSPA.

Settlement History

A few other federal lawsuits against Revco Solutions have reached conclusions. Kern v. Revco Solutions Inc. was settled in February 2022, with the terms of the settlement being undisclosed.

One of the reasons why companies settle FDCPA cases confidentially is that the settlement does not set a precedent that the company must then follow in other cases, while also getting the consumer to agree to not pursue the claim further.

Most recently, in 2026, there have been at least two cases filed against Revco Solutions: Savino v. Revco Solutions in the Florida Middle District Court and Wright v. Revco Solutions in the Indiana Northern District Court. It appears that the company may be engaging in collection activity nationwide, as there have been lawsuits filed against the company in at least four states: Ohio, Wisconsin, Florida, and Indiana.

Letters requesting the removal of an accurate account from a credit report because you are asking them nicely to do so are not effective. Collection agencies work on a strict profit margin and it is not in their interest to remove accounts from credit reports unless they are legally obligated to do so because the account is either factually deficient or cannot be verified. Letters requesting removal from your credit report are not the path to removing accounts; it is through the dispute process that accounts can be removed.

Why Paying Immediately is Bad for You

The Paid Collection Trap

You may have noticed that when you have an account from a collection agency on your credit report, the account status may say something like, “Collection account,” and may even have a balance or a past due amount. When you pay this balance, the account status on your credit report will change to, “Paid collection,” but the paid collection will still remain on your credit report for seven years from the original delinquency date.

A paid collection can still be damaging to your credit report. Anytime a lender looks at your credit report, they will see that the account went into collection, even if you have since paid it. Some credit scoring models may treat a paid collection as almost equally damaging as an unpaid collection. Because of this, paying an account immediately may not provide you with the credit repair relief you expect. This is why it is a good idea to dispute an account before paying it.

According to a U.S. PIRG study, as many as 79% of credit reports contain an error or a serious error. This means that many credit reports with a collection on them likely have some error, making them an ideal candidate for a credit repair dispute.

The Verification Challenge

When you dispute a collection account on your credit report, the credit reporting agency (CRA) has a legal obligation to investigate the account. The credit reporting agency must then contact the collection agency that reported the account and request verification of the account. The collection agency must verify that the account belongs to you and the amount they are collecting is accurate.

Collection accounts can be removed from your credit report if they contain an error, are inaccurate, are erroneous, are fraudulent, or simply cannot be verified. The thing about debt buyers is that they often lack access to documentation from the original creditor, as they often only purchased a spreadsheet with names, balances, and addresses on it.

Strategic silence can be an effective tool when dealing with debt collectors. Anytime you communicate with a debt collector, you are providing them with more information than they may have had before. Experienced credit repair specialists will know how to communicate with a debt collector without providing them with more information than they already have. This can be important when dealing with a large and well-resourced debt collector like Revco Solutions.

Responding to Revco Solutions

Documentation is Key

If you have been contacted by Revco Solutions or have a Revco Solutions account on your credit report, it is important to save every piece of communication you have with them. Save every letter they send you and make a note of the date and time of every phone call. You can even request that Revco Solutions communicate with you only in writing. This documentation may become very important if you find that the account on your credit report contains an error or that Revco Solutions has violated any of your rights under the FDCPA.

Do not engage in extended phone conversations with debt collectors. Debt collectors are highly trained professionals whose entire job is to get consumers to pay debts. They know which psychological tactics to employ in order to coerce consumers to make a payment.

Phone conversations can be incredibly effective for debt collectors, but can put the consumer in a tough spot. In a phone conversation, the debt collector may employ high-pressure tactics to coerce the consumer to make an immediate payment over the phone.

Written communication, however, provides the consumer with a paper trail and additional time to respond to the debt collector’s request. You should request that Revco Solutions sends you written verification of the debt within 30 days of their initial communication with you.

Federal law requires that a debt collector provide you with verification of the debt, including the amount of the debt and the name of the original creditor. If the collector cannot provide you with written verification of the debt, they may not be able to collect it legally.

Get Professional Help

Taking on a private-equity funded debt collection agency that has twelve offices throughout the U.S. and at least one international call center may not be a fair fight for consumers. Revco Solutions employs debt collectors that are highly trained at pressuring consumers to pay debts. Working with a credit repair agency can help level the playing field and ensure you are treated fairly throughout the entire process.

When working with a credit repair agency, you do not have to directly interact with the debt collector at all. The credit repair agency will handle all communication with the debt collector, so you will not have to deal with harassing phone calls and letters.

Additionally, you will not have to make a high-pressure decision in the heat of the moment, as the credit repair agency will handle all aspects of the process for you.

Credit repair agencies employ professionals that have experience with the dispute process and understand what documentation is required for removals. Removing collection accounts from credit reports is all a credit repair agency does, so they understand the process inside and out. They likely have dealt with thousands of different consumers and dozens of different collection agencies, so they will have a good idea of how to approach your particular situation.

Conclusion

Revco Solutions can be a tough opponent for consumers who are facing a collection account on their credit report. With twelve offices throughout the U.S. and at least one international call center, Revco has the resources to take on even the most stubborn consumers.

However, their history of complaints to the Consumer Financial Protection Bureau (CFPB) and current federal lawsuits against them may provide consumers with the leverage they need to repair their credit.

With over 300 complaints to the CFPB and a 1.3-star rating from consumers, there is evidence to suggest that Revco’s business practices may have crossed the line and violated federal and state consumer protection laws.

Current federal lawsuits against the company claim violations of at least five different provisions of the FDCPA and violations of state law. Some consumers have even reported that Revco attempted to collect on debts that had already been paid by the VA when the consumers were disabled veterans.

Such conduct demonstrates that the company may not be verifying accounts prior to attempting collection and placing the accounts on consumers’ credit reports. Such business practices may create an opportunity for consumers. Disputing the account, requesting documentation, and avoiding making an immediate decision to pay may be consumers’ best option when dealing with Revco Solutions.

With the prevalence of errors in credit reporting and debt collection, many collection accounts cannot survive a proper dispute.

What to Do Next

If you have a Revco Solutions account on your credit report, you do not have to go up against them alone. At FightCollections.com, we specialize in working with consumers to fight debt collectors and remove harmful accounts from credit reports through the dispute process.

Contact us today for a free consultation. One of our experienced staff members will take a look at your credit report, identify any potential errors or law violations, and recommend a course of action moving forward.

The debt collection industry relies on consumers feeling overwhelmed and powerless. Show them that they are wrong. Your credit report is the story of your financial history that you tell to every lender, landlord, and employer who accesses it. Make sure it is the version of the story that you want to tell. Take the first step today.