Are you dealing with debt collection from Sequium Asset Solutions? If so, you're not alone. Many people struggle to sort out collection accounts and fight debt collectors.

Sometimes, the account is a mistake. Other times, you need to verify that it is legitimate before taking any further steps. It is important to understand how to respond to collection letters and how to verify a debt.

In this article, we will look at some things you should know about Sequium Asset Solutions and what steps you can take to clear up a collection account. When a collection account appears on your credit report, it can be frustrating. But you don't have to face it alone. FightCollections.com can help you understand what happened and what you can do to clear up the account.

A Man's Frustrating Story with Sequium Asset Solutions

A man named Marcus was getting ready to apply for a car loan when he decided to check his credit report. He wanted to make sure everything was accurate before his lender pulled his report. When he opened his report, he was dismayed to find a collection account from a company called Sequium Asset Solutions. The account said he owed $847 for an old telecommunications bill.

Marcus was shocked. He had never heard of Sequium Asset Solutions, and he was certain he had paid the telecommunications bill. He wondered how this could have happened. How did Sequium get his debt, and why was it trying to collect money from him? He decided he needed to learn more about the company and the debt it claimed he owed.

Can you relate to Marcus' story? If so, you are not alone. According to a study done by U.S. PIRGs, 79 percent of credit reports contain some type of mistake or serious error. This means that almost 80 percent of people with a credit report may have an error that needs to be corrected.

For people like Marcus, this can be a disaster. A mistaken collection account can make interest rates higher, cause applications to be denied and lead to months of aggravation while the consumer tries to get the mistake corrected.

Who is Sequium Asset Solutions?

Now, let's learn more about Sequium Asset Solutions. It is a debt collection agency with headquarters in Marietta, Georgia.

This debt collection agency primarily deals with debts from telecommunications providers such as:

- AT&T

- Verizon

- Comcast

- DirecTV

The company works as a third-party debt collector and sometimes buys debt for pennies on the dollar and tries to collect the full amount from consumers.

What Do We Know about this Debt Collection Agency?

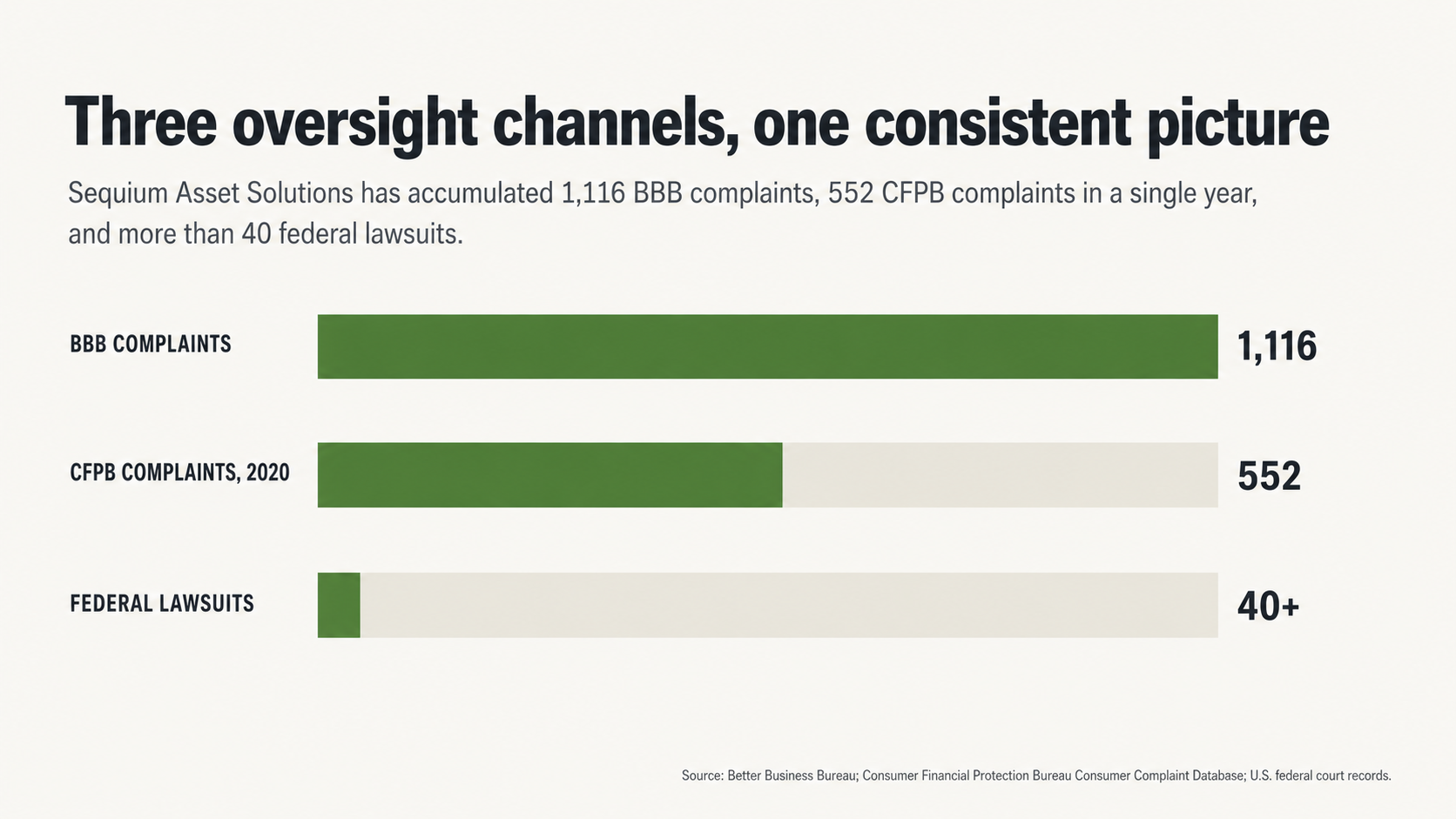

To learn more about Sequium Asset Solutions, let's take a look at some data. The Better Business Bureau (BBB) has received 1,116 complaints about the company. It has given Sequium a C rating and reports that it is not a BBB-accredited business. The bureau has found a pattern of complaints against the company that Sequium has not responded to.

In 2020, the Consumer Financial Protection Bureau (CFPB) received 552 complaints about Sequium Asset Solutions. This made the company the 61st most-complained-about financial company in the United States that year. The most common complaints were about:

- Trying to collect debt that consumers didn't owe

- Failing to provide written verification of a debt

- Reporting incorrect information to credit reporting agencies

More than 40 federal lawsuits have been filed against Sequium Asset Solutions. Most of them allege violations of the Fair Debt Collection Practices Act (FDCPA) and the Telephone Consumer Protection Act (TCPA). Court records in cases like Vandehey v. Sequium Asset Solutions have alleged that Sequium's collection letters failed to properly identify creditors or provide required validation notices. In October 2021, the North Carolina Department of Insurance issued a settlement agreement against the company.

How Did Marcus Discover the Collection Account?

Marcus discovered the collection account the way most people do: when it was too late to do anything about it. He was sitting in a finance manager's office at a car dealership, ready to finalize the purchase of a new vehicle. The finance manager came in, frowning, and told Marcus that his credit score was much lower than he had initially been quoted.

When the finance manager showed Marcus the credit report, he was shocked to see a collection account from a company called Sequium Asset Solutions. The account said he owed $847 for an old telecommunications bill. The problem was, Marcus had never heard of Sequium Asset Solutions, and he was certain that he had paid that telecommunications bill years ago.

Marcus's experience is not unusual. Many consumers only find out about collection accounts when they are applying for a loan or credit card and the lender pulls their credit report. Sometimes, consumers only find out when they check their credit report and see the collection account.

Why Do Collection Accounts Suddenly Appear on a Credit Report?

So, why do collection accounts appear on credit reports without warning? The answer is simple: Because collection agencies can report debts to credit reporting agencies before they have even contacted the consumer. This means that the consumer may not know about the debt until the damage is already done.

Imagine getting a call from a debt collector who says you owe several thousand dollars. This would be surprising and stressful, but at least you would have the opportunity to respond before the debt was placed on your credit report. Now imagine that same scenario, except the debt collector has already placed the debt on your credit report.

This is what happens when a debt collector places a collection account on your credit report before contacting you. Not only does it damage your credit score, but it also puts you in a difficult position. You must respond to the collection account before you even know whether it is valid.

That's what happened to Marcus. When he saw the collection account on his credit report, he had no idea whether it was valid. He had never heard of Sequium Asset Solutions, and he didn't know why it was trying to collect an almost $1,000 debt from him.

The best way to protect yourself from this situation is to monitor your credit report regularly. You can request a free copy of your credit report from each of the three major credit reporting agencies once a year from annualcreditreport.com.

How Debt Collectors Use Fear and Urgency

When Marcus left the car dealership without his new vehicle, he decided to call the number on the credit report. He wanted to see what he could find out about the debt that Sequium Asset Solutions said he owed. When he called the number, he spoke with a representative from the company.

The representative told Marcus that he did owe the debt and that he could pay a settlement that day to resolve the account. Marcus was torn. On the one hand, he didn't think he owed the debt. On the other hand, he was eager to resolve the account and repair his credit score.

The representative from Sequium Asset Solutions was using a tactic called fear and urgency. By telling Marcus that he could settle the debt that day, the representative was trying to scare Marcus into paying the debt without verifying whether he actually owed it.

Fear and urgency are common tactics that debt collectors use to get consumers to pay debts. By preying on the fear that consumers have about their credit scores, debt collectors can sometimes trick people into paying debts they don't owe.

One man who reviewed Sequium Asset Solutions on the Better Business Bureau website said, "They even went so far as to ask me for my bank card, my social security number, address, phone, etc. Funny thing is, a debt collector has NEVER called me one time to collect this debt, they just decided to place something on my credit report."

What are Your Rights When a Debt Collector Calls?

When a debt collector calls you, you have several rights under the Fair Debt Collection Practices Act (FDCPA). Unfortunately, many consumers are not aware of these rights, so they don't know how to respond when a debt collector calls.

One of the most important things you should know is that you have the right to tell a debt collector to stop calling you. You can stop the calls at any time by sending a written request to the debt collection agency. The agency must stop contacting you once it receives your request.

In addition to stopping the calls, you also have the right to request written verification of a debt that a collector says you owe. Before you pay a debt or respond to a collector's request for payment, you should ask for written verification of the debt. This documentation should include:

- The name of the original creditor

- The amount of the debt

- The date the debt was incurred

The debt collector must stop collection activity until it provides you with this verification. If the collector is unable to verify the debt, it must remove the account from your credit report.

Why You Should Not Pay a Collection Account

When the representative from Sequium Asset Solutions called Marcus and asked him to pay a settlement, Marcus was tempted. He wanted to resolve the account and repair his credit score. But his friend told him to wait.

Instead of paying the collection account, Marcus's friend told him why paying could actually hurt his credit score. When you pay a collection account, you are confirming that the debt is valid. In addition, the paid collection account will remain on your credit report for seven years.

Sometimes paying a collection account can even reset the statute of limitations on the debt, allowing the collector to sue you for a debt that is past the statute of limitations. Finally, paying a collection account can keep you from disputing it later if you find out it is invalid.

If you are not sure whether you should pay a collection account, it's a good idea to speak with a credit expert. The expert can help you decide the best course of action and make sure you understand your rights.

How to Dispute a Debt

If you think a debt collector has placed an invalid debt on your credit report, you should dispute it right away. The Fair Debt Collection Practices Act says that the burden of proof is on the debt collector, not the consumer. In the Vandehey class action, plaintiffs alleged that collection letters referenced financial products without naming the actual creditor and directed consumers to pay a client without identifying who that client was.

To dispute a debt, you should contact the credit reporting agency and explain why you think the account is invalid. The agency must investigate and remove the account if the debt collector is unable to verify it.

You should also contact the debt collector directly and ask for validation of the debt. The collector must provide you with documentation that shows you owe the debt. If the collector is unable to validate the debt, it must stop collection activity and remove the account from your credit report.

Why You Need a Professional to Help You

Marcus thought he could handle the collection account on his own, but he ended up needing help from a professional. His friend connected him with a credit expert who could help him navigate the situation.

The expert explained to Marcus that he did not owe the debt and that Sequium Asset Solutions was unable to validate it. With the expert's help, Marcus was able to get the collection account removed from his credit report and repair his credit score.

Debt collection harassment is a real issue, but you don't have to face it alone. FightCollections.com can help you connect with a credit expert who understands how to fight debt collectors and repair your credit report.

What to Do When You See Sequium Asset Solutions on Your Report

If you see Sequium Asset Solutions on your credit report, do not contact the company directly. In addition, do not make a payment on the debt until you have verified that it is valid.

Instead, contact FightCollections.com today for a free consultation. We can help you connect with a credit expert who understands how to fight debt collectors and remove invalid accounts from your credit report.

Don't let fear and urgency get the best of you. Contact us today to find out how we can help.

Summary of Sequium Asset Solutions

Here is a summary of what we know about Sequium Asset Solutions:

- Sequium Asset Solutions is a debt collection agency headquartered in Marietta, Georgia.

- The company collects telecommunications debts and sometimes buys debt for pennies on the dollar and tries to collect the full amount from consumers.

- The Better Business Bureau has received more than 1,100 complaints about the company and given it a C rating.

- In 2020, the Consumer Financial Protection Bureau received 552 complaints about Sequium Asset Solutions.

- More than 40 federal lawsuits have been filed against the company, most of them for violations of the FDCPA and the TCPA.

What You Can Do

If you see a collection account on your credit report from Sequium Asset Solutions, don't panic. Instead, contact FightCollections.com today for a free consultation. We can help you connect with a credit expert who understands how to fight debt collectors and remove invalid accounts from your credit report.

Don't pay a collection account until you have verified that it is valid. In addition, don't let fear and urgency get the best of you. Instead, let us help you understand your rights and connect you with someone who can help.

Contact FightCollections.com today to find out how we can help you fight Sequium Asset Solutions.