Finding Gurstel Law Firm on your credit report can feel like a gut punch. Your first thought is, "Oh no, they are going to garnish my wages, freeze my bank account, and ruin my credit score." That's what they're counting on.

Debt collection law firms like Gurstel Law Firm P.C. have perfected their ability to leverage your panic, confusion, and willingness to pay now and ask questions later.

But there is one thing you need to know that these companies are hoping you never figure out: you have a lot more leverage in this situation than you realize. Your first step in exercising it is understanding who you are dealing with.

Who is Gurstel Law Firm?

Gurstel Law Firm, P.C. is a debt collection law firm based in Minnesota. They also do business as Gurstel Chargo PA and previously operated as Gurstel Staloch & Chargo PA.

The company has nine offices in Arizona, California, Iowa, Nebraska, Nevada, Utah, and Wisconsin. They employ between 200 and 320 people and generate an estimated $20.9 million in annual revenue. This is not a small-time debt collection agency sending letters and making phone calls hoping someone coughs up a payment.

What the Courts and Consumers Have Learned

The public record on Gurstel Law Firm tells a very disturbing story. Multiple federal courts have ruled that the firm violated the Fair Debt Collection Practices Act (FDCPA) in cases that suggest an ongoing pattern of illegal behavior rather than isolated incidents.

In the 2019 case of Micks v. Gurstel Law Firm, a federal judge granted summary judgment in favor of the plaintiff after concluding that Gurstel continued to garnish wages even after the underlying judgment was vacated. The judge rejected the firm's argument that this was an unintentional mistake. The original judgment was for more than $36,000 and Gurstel kept taking money out of someone's paycheck even after they knew the judgment had been thrown out.

The 2020 Gallagher v. Gurstel case revealed even more egregious practices. The judge found that the firm issued two separate garnishment summonses on the same day for two different amounts, causing a bank to freeze over $4,100 when the actual claim was for about half that amount. The judge said Gurstel had no explanation for why this happened.

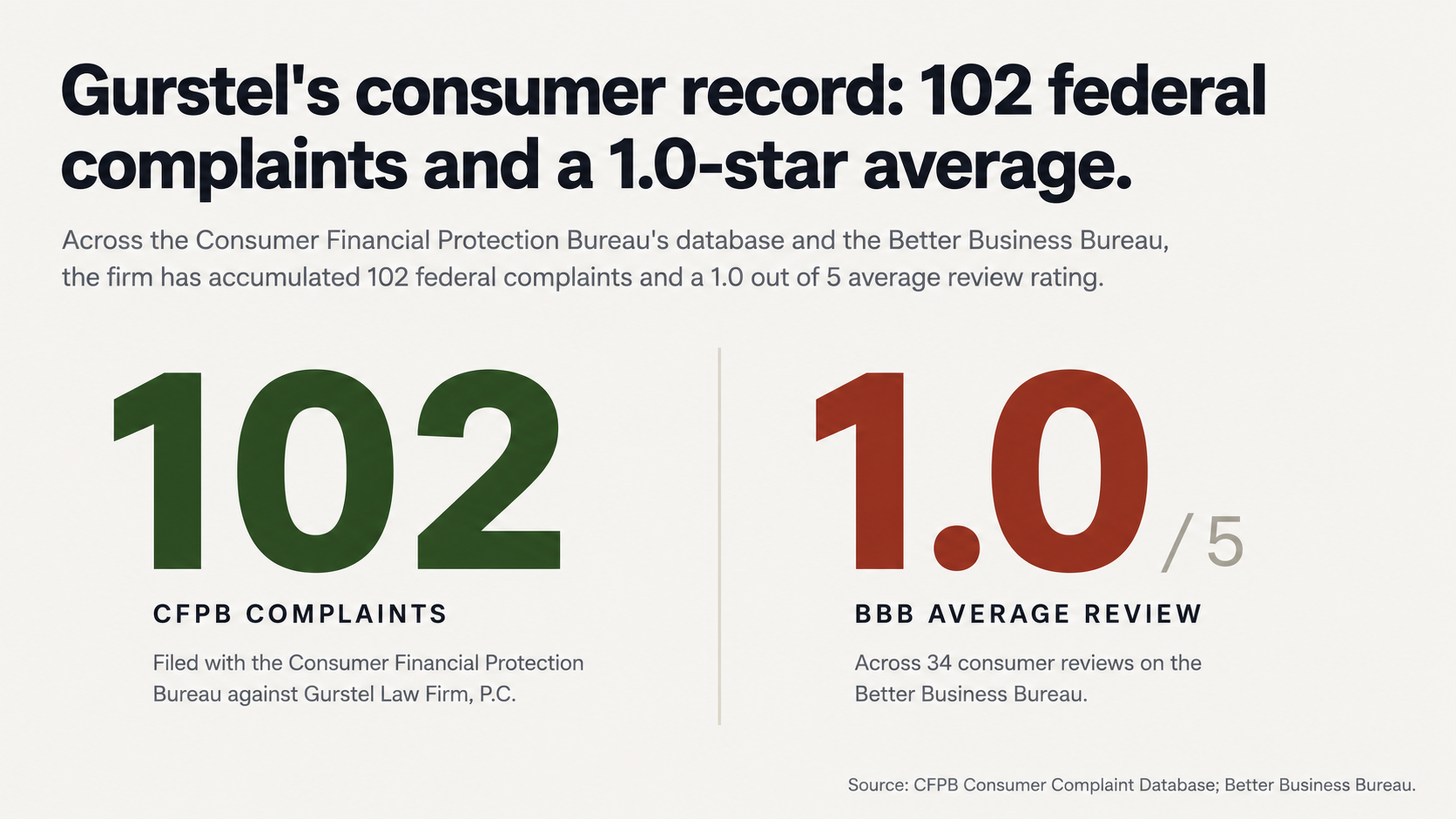

Consumer complaints mirror the same theme. The Consumer Financial Protection Bureau (CFPB) has received 102 complaints against Gurstel Law Firm.

On the Better Business Bureau (BBB) website, the firm has garnered 34 consumer reviews with an average rating of one out of five stars. One consumer review posted in August 2025 claimed that the firm lost a signed payment agreement and then sought a default judgment against someone who had been making timely payments.

What Gurstel Law Firm is Counting On

Your first line of defense against this aggressive debt collection strategy is understanding the assumptions that Gurstel Law Firm is making about how you will react. They are not preparing for a fair fight. They are counting on you to respond in very predictable ways that play right into their hands.

They Expect You to Panic

The very instant you see that a law firm has sent you a debt collection letter, you feel a wave of panic wash over you. This is the intended effect. A debt collector armed with a law license carries threats that run-of-the-mill debt collectors do not. Gurstel knows this better than almost anyone.

Consumer complaints describe process servers who showed up armed with guns on their hips, banging on doors like they were serving warrants. Whether these tactics are legal or not, they are designed for one purpose: to make you feel trapped.

Panic will always cloud your judgment. When you are scared, you are more likely to make promises you cannot afford to keep, admit that you owe a debt that you might not actually owe, or send a check without ever confirming that the debt is legitimate. The best response to this fear is to do nothing until you have professionals advising you.

They Expect You to Pay Without Verifying

The second assumption working against you is that you will accept whatever they claim you owe without question. They send you a letter with a dollar amount on it and fully expect you to believe every digit without demanding any proof.

Consider what can happen when a debt changes hands.

Original creditors sell debt portfolios to debt buyers, who may then sell those portfolios again to another debt buyer. Each transfer creates opportunities for documentation to disappear, account numbers to get switched, and the wrong person to get targeted.

A U.S. PIRGs study found that 79% of credit reports contain errors or serious errors.

Gurstel Law Firm has been accused in federal court of filing affidavits alleging that consumers failed to respond to a lawsuit on the same day they actually received the consumer's response. In the Ness case, Gurstel sought a default judgment while the consumer's answer was in their possession. When the paper trail is this unreliable, why on earth would you pay anything without first demanding that they verify their claim?

They Expect You to Do Nothing

Perhaps the biggest advantage these debt collectors have is that most consumers who receive debt collection letters never respond. They ignore the letters. They dodge the phone calls. They pray that the problem just goes away. This is a dream come true for the default judgment business model.

Minnesota — where Gurstel Law Firm is based — allows debt collectors to serve lawsuits before filing them in court. Consumers then have just 21 days to file an answer or a default judgment can be entered without any judge even looking at whether the underlying claim has any merit. Minnesota consumer attorneys say that failing to meet this deadline almost always results in an automatic judgment without any hearing at all.

Doing nothing is not a strategy. It's a surrender. The debt collector wins by default — literally — because they have set up their entire operation based on the assumption that you will not put up a fight.

Why Disputing is Your First Line of Defense

The information playing field between you and a debt collector like Gurstel is not level. They have files and records and armies of attorneys. You have a scary letter. But there is one area where that playing field can be leveled: verification.

The Documentation Problem

Anytime a debt is sold and resold, there's a good chance the paperwork trail is going to get broken. Original contracts can disappear. Payment records can become incomplete. Assignments of accounts can lack the proper signatures.

One BBB reviewer compared the business practices of Gurstel Law Firm to those of Midland Funding, the debt buyer that was fined $90 million by the CFPB in 2015. The complaint alleged that the company routinely sues individuals using mass-assigned debt portfolios with little legitimate documentation, instead using unauthenticated spreadsheets and generic bills of sale instead of the original paperwork from the original lender.

This documentation vulnerability creates an opening for removal. If a debt collector cannot prove that you owe the debt, cannot prove that they own the debt, or cannot prove that the amount they are claiming is the right amount, you may have the basis for getting the account removed from your credit report. But you'll never know unless someone forces them to prove it.

Error Rates Make Challenging Necessary

Given how often errors pop up on credit reports, it makes no sense to treat every collection account as if it is accurate until proven otherwise. The burden of proof needs to rest with the party accusing the other of owing a debt, not the party being accused.

The Gallagher case illustrates this point perfectly. Gurstel was seeking over $5,200 while refusing to give the consumer credit for $3,800 already paid. Without someone challenging those numbers, that consumer would have ended up paying nearly double what was actually owed.

Disputing is not about trying to dodge legitimate debts. It's about refusing to accept accusations at face value when the evidence shows that debt collectors frequently get it wrong. Every single collection account deserves to be scrutinized because errors are the norm rather than the exception.

The Strategic Power of Professional Intervention

There's a reason why debt collectors would much rather deal directly with consumers instead of a professional. Unrepresented consumers are easier to intimidate, confuse, and manipulate.

Removing Emotional Manipulation from the Equation

One of the reasons to work with a credit repair company is not just about the expertise. It's also about creating a wall between you and the emotional manipulation that debt collectors employ. When you answer your own phone, you expose yourself to carefully crafted scripts designed to evoke feelings of shame, fear, and urgency.

Debt collectors are trained to keep you on the phone as long as possible, to get you to make admissions, and to pressure you into making an immediate payment. Every single phone call is a potential landmine.

A professional intermediary takes all of that emotional manipulation off the table. A debt collector cannot shame someone who refuses to answer their phone calls. A debt collector cannot create a sense of urgency with someone who only responds through formal written communication. The game gets reduced to a simple matter of documentation and legal rights instead of who can endure the most emotional pressure.

Persistence is Harassment in Disguise

What debt collectors call "follow-up" is really just a harassment technique designed to break your resolve. The constant phone calls. The letters with slightly different wording. The ratcheted-up urgency of their demands. It's all designed to do one thing: break your will.

The Isham case against Gurstel Law Firm revealed that the firm continued contacting a consumer even after receiving both oral and written notification that the consumer was represented by an attorney. A paralegal even placed a code in the computer system acknowledging that the consumer had an attorney, yet the contacts continued. The firm also continued contacting the consumer even after receiving a certified letter demanding that all contacts cease and desist.

That's why ignoring debt collection calls and working through a professional makes so much sense. You don't owe them a phone call. You don't owe them access to your emotions. You owe them nothing except what they can prove through proper documentation, and even then that determination should be made through formal dispute procedures instead of phone calls designed to manipulate you.

How Collections Can Be Removed From Your Credit Report

It is possible to get a collection removed from your credit report if the information is inaccurate, fraudulent, unverifiable, or cannot be verified within the allotted timeframe. Understanding those pathways can dramatically change how you approach the problem.

Challenging Unverifiable Information

Credit reporting agencies are required to investigate any disputes and verify the accuracy of information being reported. If a debt collector cannot provide the necessary documentation within a reasonable amount of time, the account should be deleted.

The class-action cases against Gurstel Law Firm reveal common verification issues. One plaintiff reported receiving four separate garnishment notices in the same month stating four different balances that kept increasing, making it impossible to determine what the actual balance might be. Another plaintiff reported receiving three separate notices over the course of nine months, each notice implying that the balance may increase, except that all three notices stated the exact same balance that legally could not increase.

When a debt collector cannot even keep their own story straight, that inconsistency becomes a weapon for removal. But you only learn about those inconsistencies if someone challenges them to prove their story.

The Burden of Proof Belongs to Them

Too many consumers approach these situations from a position of presumed guilt. They see a collection account on their credit report and immediately assume it's their job to prove that they don't owe it. That approach has the presumption backwards.

The debt collector is the party making an accusation. They are the party claiming you owe them money. They should bear the burden of proving every single element of their accusation through documented evidence before it's allowed to damage your credit report.

Paying a collection account may change its status from "unpaid" to "paid" but the account remains on your credit report either way. The damage to your credit history remains. That's why disputing a debt before even thinking about paying it is the smart play. Removal eliminates the problem. Payment just changes the label on the problem.

Conclusion

Gurstel Law Firm has a very profitable business model that relies on your fear and your inaction. Their entire operation is predicated on people panicking, paying debts without verifying them, and allowing default judgments instead of fighting back. The federal court record shows that this particular firm has been found to have violated federal debt collection laws in multiple cases. Consumer complaints document a pattern of questionable tactics and documentation issues.

None of that means you cannot beat them. But it does mean you should not try to do it alone.

Call to Action

If you spot Gurstel Law Firm on your credit report, don't panic, don't call them, and don't pay them a dime until you understand exactly what you're up against. The information imbalance that works to the advantage of debt collectors can be overcome if you have experienced professionals working on your behalf.

FightCollections.com specializes in disputing collection accounts that are in error and helping consumers understand their rights under federal law. Our team understands the documentation vulnerabilities that debt collectors try to hide and the verification procedures that they often fail to follow.

Contact us today for a free consultation to review your credit report and talk about your options. You do not have to face Gurstel Law Firm alone. And you certainly should not concede defeat before the battle has even begun.