The moment you notice an unfamiliar collection account on your credit report, you feel a knot in your stomach.

If the account is from KLS Financial Services, know that you are dealing with a debt collection agency that has attracted over 130 consumer complaints to the Consumer Financial Protection Bureau (CFPB) since the company’s inception in 2017. Before taking any action, recognize that the choices you make over the coming weeks will determine whether this collection account hurts your credit for a half-decade or disappears forever.

The debt collection industry profits from information asymmetry. The debt collection agencies know all the rules, while most consumers have no idea how the process works and end up making reactive decisions governed by emotion rather than strategy. This article will give you a tactical playbook for dealing with a KLS Financial Services collection.

Who is KLS Financial Services?

KLS Financial Services, Inc. is a third-party debt collection agency based in North Carolina. The company primarily focuses on collecting medical and commercial debts for original creditors. Here is some basic information about KLS:

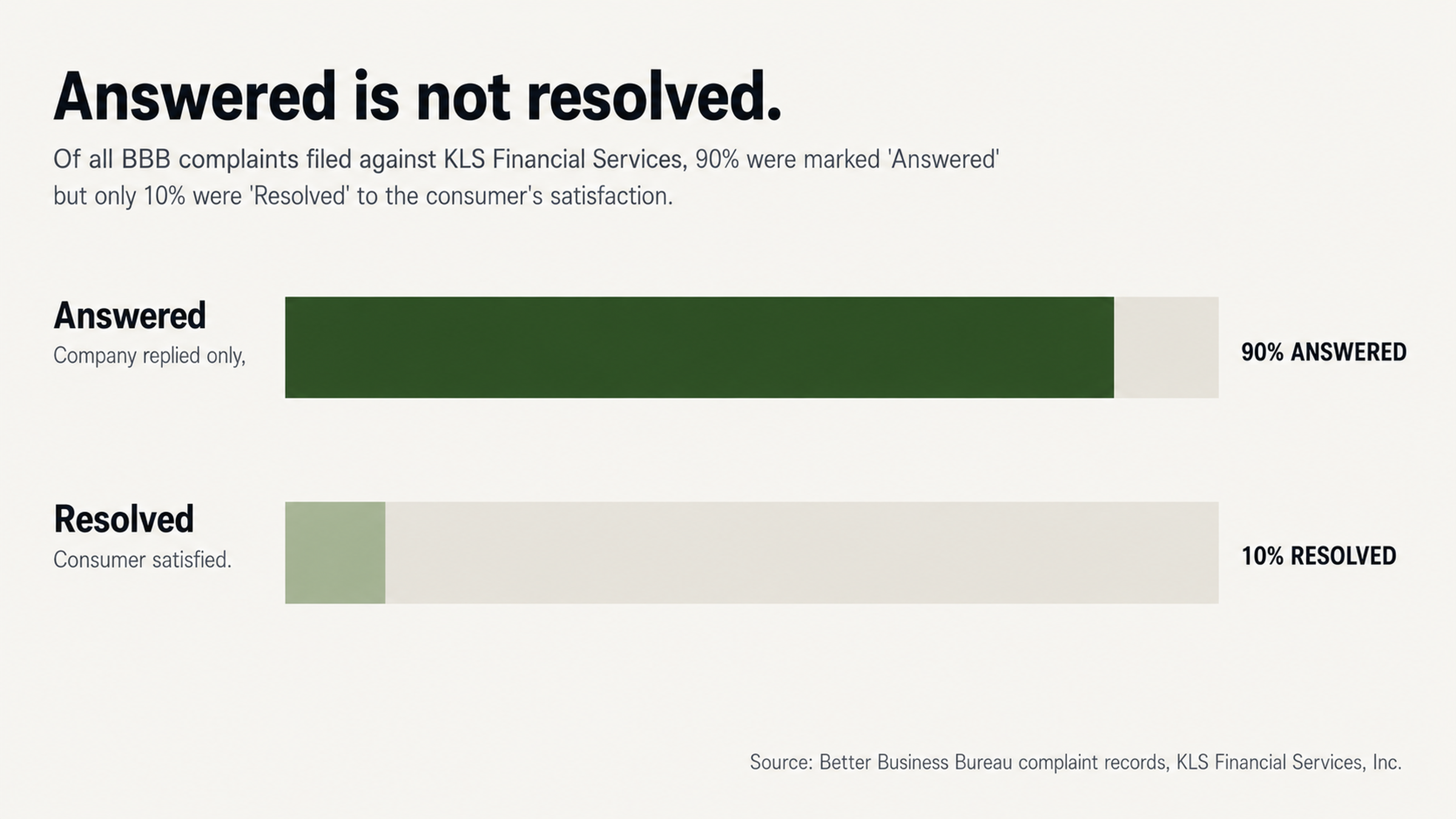

What the data says about this collector

Despite maintaining an A+ rating with the Better Business Bureau (BBB), a deeper dive into KLS Financial Services data reveals troubling signs. The company has registered corporate branches in Florida, Louisiana, South Carolina, and Connecticut, expanding its debt collection activities to multiple states.

Analyzing the consumer complaints filed with the BBB against KLS Financial Services reveals a significant disconnect between the company’s accreditation status and actual consumer outcomes.

Of all the BBB complaints filed against KLS, 90% are classified as merely “Answered” while only 10% are classified as “Resolved”. The difference between these two classifications is important because “Answered” means the company replied to the complaint while “Resolved” means the complainant confirmed that the issue was resolved to their satisfaction.

The trend in BBB complaints against KLS Financial Services also appears to be going in the wrong direction. The company has received 45% of its three-year total for BBB complaints in the most recent year alone, indicating that the issues with this debt collection agency may be getting worse as the company becomes more aggressive in pursuit of debt collection.

Why this matters to you

A collection account will hurt your credit. Knowing that KLS Financial Services has a history of poor consumer outcomes and appears to be getting more aggressive in debt collection makes it even more critical that you approach this process strategically.

What it means for your situation

Before diving into the specific steps you should take in response to a KLS Financial Services collection, recognize how the guilty-until-proven-innocent nature of the credit reporting system places you at a disadvantage. When KLS Financial Services places a collection account on your credit report, they do not need to prove anything. The account simply goes on your report, hurting your credit score, and will remain unless you take action to dispute it.

A study by U.S. PIRGs found that 79% of credit reports contained either errors or serious errors. This means that there is nearly an 8 in 10 chance that the information in the collection account on your credit report is wrong, whether it is the amount, dates or even if you are the right person.

Consumers reviewing KLS Financial Services consistently mention a failure in the debt validation process. As one reviewer on WalletHub said, “These people are very unprofessional and rude. I’m not sure I have an account with them other than what they claim and I was trying to find out if I’m a victim of identity theft or not. They couldn’t give me any information although I gave them the information they needed to verify my identity.”

The information flow principle

Every piece of information you give to a debt collector is a weapon they can use against you. Your phone number gives them a way to call you repeatedly. The name of your employer opens the door for them to attempt to garnish your wages. Even confirming that you are who you say you are can be used against you.

Smart consumers understand that information should only flow one way: from the debt collector to them. You have the right to demand verification of a debt. You have no obligation to confirm your employment, discuss your finances or engage in any conversation that is not required by law.

This is also why it is a bad idea to talk to a collection agency directly. Every conversation is an opportunity for them to gather more information from you while providing as little information as possible in return.

Why you should dispute before you pay

Paying a collection seems like the right thing to do. It is natural to want to take care of a problem and move on with your life. However, paying a collection is often a mistake.

When you pay a collection, you are changing the status of the account from “unpaid collection” to “paid collection”. However, in most cases, the paid collection remains on your credit report for the full 7 years from the date of the original delinquency.

Having a paid collection on your credit report still tells future lenders that you had an account go to collections. In many credit scoring models, paid and unpaid collections are treated the same, so paying it off may not even help your credit score. It also just cost you money and you gave up your leverage to get it deleted.

If you dispute the collection first, you may get it completely removed. If the collection is an error, inaccuracy or they cannot validate it in time, the account can come off your report entirely. That is a much better outcome than paying it.

What makes a collection removable?

A collection can be removed from your credit report for several reasons. The information may be incorrect or inaccurate. The debt may be fraudulent (e.g. identity theft or mistaken identity). The collector may not be able to validate the debt within the allotted time.

KLS Financial Services has a history of issues related to debt validation. Multiple consumers have filed complaints indicating that the company failed to provide the original contract or written verification as requested. As one complainant on BBB said, “I am not liable for this debt. I do not have a contract with KLS Financial Services, Inc. They did not provide me with the original contract as I requested it.”

If a debt collector cannot provide the documentation to validate a debt, the credit bureaus must remove it. This is not a loophole or trick. It is just the mechanism that exists to ensure the information on your credit report is accurate.

Action plan

Here is your step-by-step action plan for a KLS Financial Services collection:

Step 1: Get everything in writing

Before you do anything, get a copy of your credit report from each of the three major credit reporting bureaus (Equifax, Experian and TransUnion). You can get these reports for free at AnnualCreditReport.com. Go through each report line by line to identify how KLS Financial Services is reporting the collection account.

Make a note of any discrepancies in how the account is being reported on each of the three credit reports. Some consumers have filed complaints against KLS indicating that the company reported different dates to different credit bureaus and then told them it was an issue with how the credit bureaus reported the information. These discrepancies can be helpful in building your dispute.

Make copies of everything. Take screen shots of the collection account. Save all correspondence. This is all documentation you will need to build your dispute.

Step 2: Know your rights

Federal law provides a number of important protections against debt collector abuse. The Fair Debt Collection Practices Act (FDCPA) prohibits harassment, threats and deception. A debt collector cannot threaten to have you arrested or claim to be a government official. They cannot engage in conduct intended to abuse or harass you.

The Fair Credit Reporting Act (FCRA) requires that the information on your credit report be accurate and verifiable. When you dispute an account, the credit bureaus must conduct an investigation and the debt collector must verify the debt. If they cannot verify the debt within 30 days, the account must be deleted.

These are your rights regardless of whether you actually owe the debt. The purpose of these laws is to protect the integrity of the credit reporting system by verifying the information on your report.

How a professional makes a difference

The knowledge gap

Debt collectors deal with disputes every day. They know exactly what type of response is needed to satisfy the technical requirements of the law without providing any meaningful information. They know how to keep a collection account on your credit report even when they do not have much documentation. When you try to handle it on your own, you are taking on professionals who have heard every argument before.

A credit repair professional evens the playing field. They understand the language that must be included in a dispute letter, the types of documentation that strengthen a case and the process for escalating a dispute if the credit bureau does not respond adequately. There is no harm having a professional submit multiple disputes on the same debt because an accurate investigation does not generate another negative mark on your credit report.

KLS Financial Services has been the subject of a federal lawsuit including Nicholson v. KLS Financial Services, Inc. in the Southern District of Indiana and Diaz v. KLS Financial Services, Inc. in the Western District of North Carolina. A professional with knowledge of the company’s litigation history and patterns of complaints can use that information to build a stronger dispute.

Permanence of a deletion

Once a collection account is successfully disputed and deleted from your credit report, it typically will stay deleted. In most cases, a debt collector does not have the mechanism to get a reinserted and generally lacks the incentive to invest the time to try and put an account back on your report after it has already been disputed.

That is what makes disputing a collection account worth doing even if you are not sure of success. If you are successful, the account will be gone. If you pay it, the account will still be on your report for several more years. The potential benefit of getting the account deleted far outweighs the cost of disputing it properly.

The key is making sure that you do it right the first time. A weak dispute can be dismissed without additional review but a strong one forces the debt collector or credit bureau to respond.

What to expect

Timeframe and responses

When you submit a dispute to the credit bureaus, they have 30 days to investigate and respond. During that time, they will reach out to the debt collector and request verification. The debt collector must then provide documentation to support their claim or the account must be deleted.

KLS Financial Services has responded to complaints filed with the CFPB by saying, “responded to the consumer and the CFPB and chooses not to provide a public response”. This lack of transparency extends to the dispute process where they may or may not provide verification information in response to your dispute.

Be patient. The 30-day window for investigation generally works to your advantage because debt collectors operating on thin margins must weigh the cost of responding to your dispute against the potential benefit of collecting the debt. In many cases, they will simply delete the account rather than spend the time to validate it.

What to do when they continue collection activity

You may continue to get calls or letters from KLS Financial Services during the dispute process. Do not feel like you need to respond. In fact, the less you engage with a debt collector during a dispute, the better.

If they are harassing you, document everything. Write down the date, time and nature of every call. Debt collectors are not legally allowed to harass consumers and if you can demonstrate a pattern of abusive behavior, you may have additional grounds for a claim under federal or state consumer protection laws.

Keep in mind that debt collectors rely on your fear and urgency to get you to pay a collection account quickly without disputing it. The more time you take to understand your options and make a smart decision, the less leverage they have.

Conclusion

A KLS Financial Services collection on your credit report is not a fait accompli. The company’s history of failing to validate debts, its increasing rate of complaints and its low rate of resolving problems for consumers all suggest that a smart dispute strategy can get this account removed.

By understanding that you do not need to prove anything for a collection account to go on your report, that paying is not always the answer and that removal is a possibility, you can approach this process from a position of strength rather than fear.

The process is pretty straight-forward. Gather your documentation. Understand your rights. Dispute before you pay. Consider professional help when needed.

Do not let a collection account dictate your credit for half a decade. At FightCollections.com, we specialize in disputing invalid collection accounts from your credit report. We understand the history and patterns of debt collectors like KLS Financial Services and use that information to help consumers in your shoes.

Contact us today to schedule a free consultation and discuss your specific situation. Our team of professionals can help you navigate the complex process of disputing collections and support you as you work to clean up your credit report.

The sooner you start, the sooner you can move on with your life.