Are you surprised to find a Rausch Sturm on your credit report?

If so, it’s understandable that you’d want to know who they are, why they are reporting something on your credit report, and how you can get them removed.

Finding any kind of collection account on your report can be unsettling, and it’s even more concerning when the collection agency is a law firm that files thousands of lawsuits every year.

Before you can decide what actions to take, it’s helpful to understand how collection accounts get on credit reports in the first place and why so many errors occur. Once you understand how the credit reporting system works and why it seems designed to favor everyone but consumers, you can begin making a plan to address the problem.

For example, did you know that the credit reporting system relies on the assumption that the information reported is accurate? It’s true. In fact, the system is built around the idea that consumers will catch and correct errors rather than the other way around. This is why collection agencies like Rausch Sturm are able to get away with so much.

So, who is Rausch Sturm?

Rausch Sturm LLP is a debt collection law firm based in Wisconsin that represents original creditors and debt buyers in more than 33 states. They don’t work like most collection agencies you might have dealt with before because they are actually a law firm that files lawsuits in order to collect debts.

Rausch Sturm has operated under other names, including Rausch, Sturm, Israel, Enerson & Hornik, LLP. They represent a number of original creditors, including Bank of America, Capital One, Discover Bank, and Synchrony Bank, as well as debt buyers like Jefferson Capital Systems and Portfolio Recovery Associates.

What Do We Know About Rausch Sturm’s Business Practices?

The Consumer Financial Protection Bureau’s (CFPB) complaint database includes anywhere from 142 to 312 complaints depending on the search parameters you use. In 2019 alone, Rausch Sturm had 55 complaints filed against it, which put the company on the list of Top 400 companies complained about to the CFPB that year.

The picture is even more bleak when you look at Rausch Sturm’s Better Business Bureau (BBB) record. Despite being a BBB-accredited business, the company has had 229 complaints closed in the last three years and averages just 1.04 out of 5 stars based on 54 customer reviews on the Better Business Bureau.

Here’s what one customer had to say about their experience with Rausch Sturm:

“This company DOES NOT ANSWER THE PHONE, EMAIL, OR MAIL. I tried to contact them to set up a payment plan and no one ever responded, TO MY MULTIPLE ATTEMPTS. They sued me and STILL DO NOT ANSWER THE PHONE OR CALL BACK.”

Rausch Sturm’s practices have also been called into question by a federal court. In the case Vanhuss v. Rausch Sturm Israel Enerson & Hornik, a federal court in Wisconsin determined that the company violated debt collection laws when it filed a lawsuit against a consumer before the company had verified a debt the consumer disputed. The consumer mailed a dispute letter within the allotted timeframe, but Rausch Sturm sued anyway.

Why Debt Collection Law Firms Like Rausch Sturm Rely on Consumers Not Understanding Their Rights

High-Volume, Low-Accuracy

Debt collection law firms like Rausch Sturm work on very thin profit margins, which means they have to successfully collect or settle a very high percentage of the debts they pursue in order to remain profitable. This is why firms like Rausch Sturm file so many lawsuits and send so many collection letters every year.

In fact, a former managing attorney at Rausch Sturm indicated that in his last month at the company he signed almost 800 lawsuits by himself and was averaging four court hearings per day.

When you are signing hundreds of lawsuits every month and averaging multiple court hearings per day, there is no way you have time to actually review the documentation for each individual case. This is why the business model adopted by debt collection law firms like Rausch Sturm has to involve so many errors.

The Information Asymmetry Business Model

The debt collection industry as a whole is built around the concept of information asymmetry, which is just a fancy way of saying that the debt collection industry makes money because consumers don’t know their rights. When a collection agency contacts you about a debt you supposedly owe, especially when that contact comes in the form of a lawsuit filed by a law firm, it’s natural to feel a bit intimidated.

Debt collection law firms like Rausch Sturm know this and use it to their advantage. They send collection letters and file lawsuits hoping to make you feel so anxious about the situation that you’ll just pay what they say you owe in order to make it all go away. They do this because they know that when you act out of a sense of urgency, you’re much less likely to stop and consider whether the debt is legitimate, whether the amount is correct, or whether the statute of limitations has run.

Your Rights Under Federal Law

The Fair Credit Reporting Act (FCRA)

The FCRA is probably best known as the federal law that regulates credit reporting, but it does more than just establish rules for credit bureaus. It also gives consumers offensive tools they can use to challenge debts and potentially get them removed from credit reports.

For example, did you know that the FCRA requires credit bureaus to investigate any items you dispute within 30 days? It’s true. The FCRA also says that if a credit bureau cannot verify the information it has on file, it must delete that information.

Here’s the important part: The burden in this situation is on the data furnisher (the company that made the credit report), not the consumer. So, if Rausch Sturm puts a debt on your credit report and you dispute it, the company has to be able to show that it has all the documentation it needs to prove the debt is both valid and yours.

If Rausch Sturm cannot produce all the documentation for the original debt, including:

- The original contract you signed with the creditor

- The chain of assignment for the debt

- The current balance owed

…then the credit bureau has no choice but to delete the entry.

The Fair Debt Collection Practices Act (FDCPA)

In addition to the FCRA, consumers also have rights under the FDCPA, a federal law that governs the actions of debt collection agencies. The law establishes what collectors can and cannot do when communicating with consumers, and violations of the FDCPA are not just technical offenses — they provide consumers with grounds for lawsuits.

Rausch Sturm has been sued in 76 or more cases in federal court, with many of those allegations involving violations of the FDCPA. For example, a class action suit called Autry v. Jefferson Capital Systems LLC and Rausch Sturm alleged that the firm regularly sent consumers collection letters that included “false, deceptive, and/or misleading” information about what would happen if the consumer paid the amount it said they owed.

In that case, the plaintiff alleged that Rausch Sturm violated the FDCPA and was seeking up to one million dollars in damages.

Why the “Dispute-First” Strategy Works So Well Against Rausch Sturm

The Documentation Issue

Before you talk to a debt collection agency about payment or settlement, you should always insist that the company conduct a thorough investigation of your account to confirm that it is accurate. There’s a good reason for this: When you pay a debt or discuss settlement, you are essentially acknowledging that the debt is valid.

On the other hand, when you insist the debt collection agency conduct an investigation, you are making the company prove that it has the legal right to collect from you. As noted above, federal courts have found that Rausch Sturm sometimes pursues consumers for debts when it does not have all the documentation it is legally required to have.

For example, in one case a consumer owed Rausch Sturm approximately $4,800, so they requested a copy of the original credit agreement. Rausch Sturm was unable to produce the agreement, and the case was dismissed 67 days later. Defense attorneys in these cases report that, generally, when they request the complete chain of assignment, they are often successful.

Debt Validation Failure Rate

One credit repair company decided to test Rausch Sturm’s process by sending 73 debt validation requests to the company and tracking the responses it received. The company reports that Rausch Sturm failed to validate the debt 40 percent of the time.

This is a remarkable number, and it suggests that almost half of all the debts that Rausch Sturm pursues cannot stand up to scrutiny when consumers insist on validation. When a debt collection agency cannot validate a debt, it no longer has the legal right to attempt to collect it under the FDCPA.

More to the point for consumers who are concerned about their credit reports, though, debts that cannot be validated cannot be verified to the credit bureaus, which means they must be removed. If 40 percent is a reliable estimate of the number of Rausch Sturm debts that cannot be validated, that suggests one of the best strategies for dealing with the company is to dispute any debts it reports.

How the Credit Reporting System Works (and Why So Many Errors Occur)

The System is Fundamentally Flawed

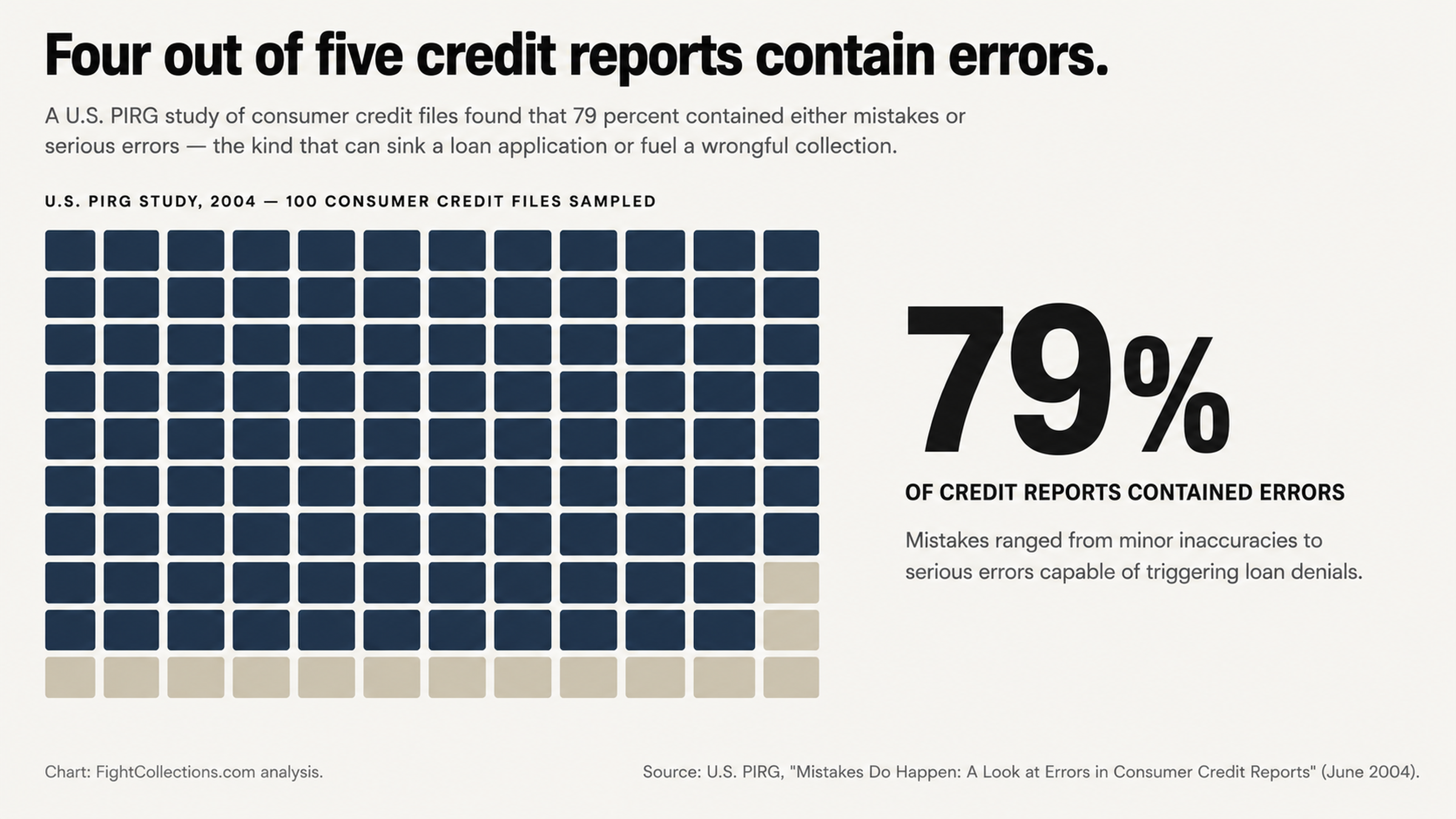

In 2004 a non-profit called U.S. Public Interest Research Groups conducted a study and found that 79 percent of credit reports contain either mistakes or serious errors. This is a remarkable number, and it suggests that the problem is not just with individual credit reports — the system itself is flawed.

The credit reporting system was developed decades ago, and it is not designed to handle the billions of pieces of information that credit bureaus must process every year. There is virtually no human review of any of the information that is placed on credit reports.

Credit bureaus are for-profit companies that make money by selling credit reports and credit scores. This means the bureaus have a financial incentive to process as much information as possible as quickly as possible in order to sell as many reports and scores as they can — accuracy is not the priority here.

When a debt collection agency furnishes information to a credit bureau, the bureau typically accepts what the agency reports and does not conduct any additional investigation to confirm that the information is accurate.

Why Credit Reporting Errors Tend to Become Permanent

Many of the complaints filed against Rausch Sturm with the CFPB involve cases of mistaken identity.

For example, one consumer indicated that Rausch Sturm claimed they owed a debt but that the person the company was trying to collect from had a different first name, a different middle name, a different last name, a different address, a different social security number, a different date of birth, and a different employer.

Despite the fact that the consumer sent Rausch Sturm documents from the court proving their identity and that they were not the person the company was looking for, the company continued to pursue them. Even after the credit bureau confirmed that the consumer was not the right person, Rausch Sturm continued its collection efforts.

In a system like this, errors can persist indefinitely unless the consumer takes action. A debt collection agency can incorrectly report information to the credit bureau, damaging your credit score, and the only consequence is…well, actually there is no real consequence unless you, the consumer, take action to dispute the information.

What’s the Difference if You Pay a Collection vs. Dispute It?

The Problem with Paying a Collection

A lot of consumers assume that if they pay a collection account it will help their credit. Unfortunately, that’s just not true. Paying a collection changes the status of the account on your credit report from “unpaid collection” to “paid collection,” but the collection remains on your report for just as long — seven years from the original delinquency date.

Paying a collection can also cause problems in some states because it restarts the clock on the statute of limitations. This means that if you pay a collection, you might actually be giving the collector additional years to sue you for the remaining balance. When you pay a collection, you’re also confirming that it’s a valid debt, which means you’ll never be able to dispute it later.

BBB complaints suggest that Rausch Sturm has even pursued consumers for debts they’ve already paid. One consumer indicated that Rausch Sturm was garnishing their wages for a debt they paid off three years earlier and that the matter had somehow been reopened so that garnishment resumed.

Why Disputing is Smart

When you dispute a collection account, on the other hand, you force the debt collector to prove that they have the right to collect from you. Given that Rausch Sturm is unable to validate 40 percent of all the debts it pursues, the odds are actually in your favor if you adopt a dispute-first strategy.

It’s also important to note the strategic advantage of ignoring debt collectors in many cases. When you don’t engage directly with a debt collection agency, you can’t accidentally acknowledge that you owe a debt or restart any statute of limitations clock.

You also can’t provide the collector with additional information that it can use against you. In a dispute, all of the information has to flow one way — from the collector to you, not the other way around.

Conclusion

Rausch Sturm is an especially aggressive debt collection law firm that files thousands of lawsuits every year and has hundreds of complaints filed against it with the BBB and CFPB. The company has a 40 percent debt validation failure rate and has been known to pursue the wrong consumers and attempt to collect debts that consumers have already paid.

The credit reporting system is flawed, which means that 79 percent of all credit reports contain at least one error. This suggests that just because there is a collection account from Rausch Sturm on your report, that does not mean the debt is valid or legitimate.

Fortunately, federal law gives you a number of tools you can use to fight back against abusive debt collectors and errors on your credit report. If you have a Rausch Sturm account on your credit report and you’re not sure what to do about it, contact Credit Repair Companies like FightCollections.com today to learn how we can help.

Credit repair specialists understand how debt collection law firms like Rausch Sturm operate and where the flaws are in their processes. Armed with that information, we can help you navigate the dispute process and potentially remove the debt from your credit report.

Don’t pay Rausch Sturm just because you’re not sure what else to do — contact us today for a free consultation and let us help you take the first step toward reclaiming your credit.