Who is Wakefield and Associates?

Discovering a collection from Wakefield and Associates on your credit report is a shock. Most people immediately panic and call the collection agency in order to pay the debt as quickly as possible. That’s the worst possible move.

The debt collection industry thrives on consumers’ confusion and misinformation. Collection agencies like Wakefield and Associates rely on you not knowing your rights, not understanding the credit reporting process, and not being aware of the tools you have at your disposal. The decisions you make in the days after finding a collection will determine whether the account will remain on your credit report for seven years or if it will be deleted.

Wakefield and Associates is a debt collection company based in Colorado that focuses on collecting medical debt. The company works throughout the country and has been in the business since 1986.

The company merged with Revco Solutions in 2024 and has 18 locations across the United States. Despite boasting more than 75 years of experience in health care revenue cycle management, the company has built a questionable reputation with consumers and regulators.

History of legal issues and consumer complaints

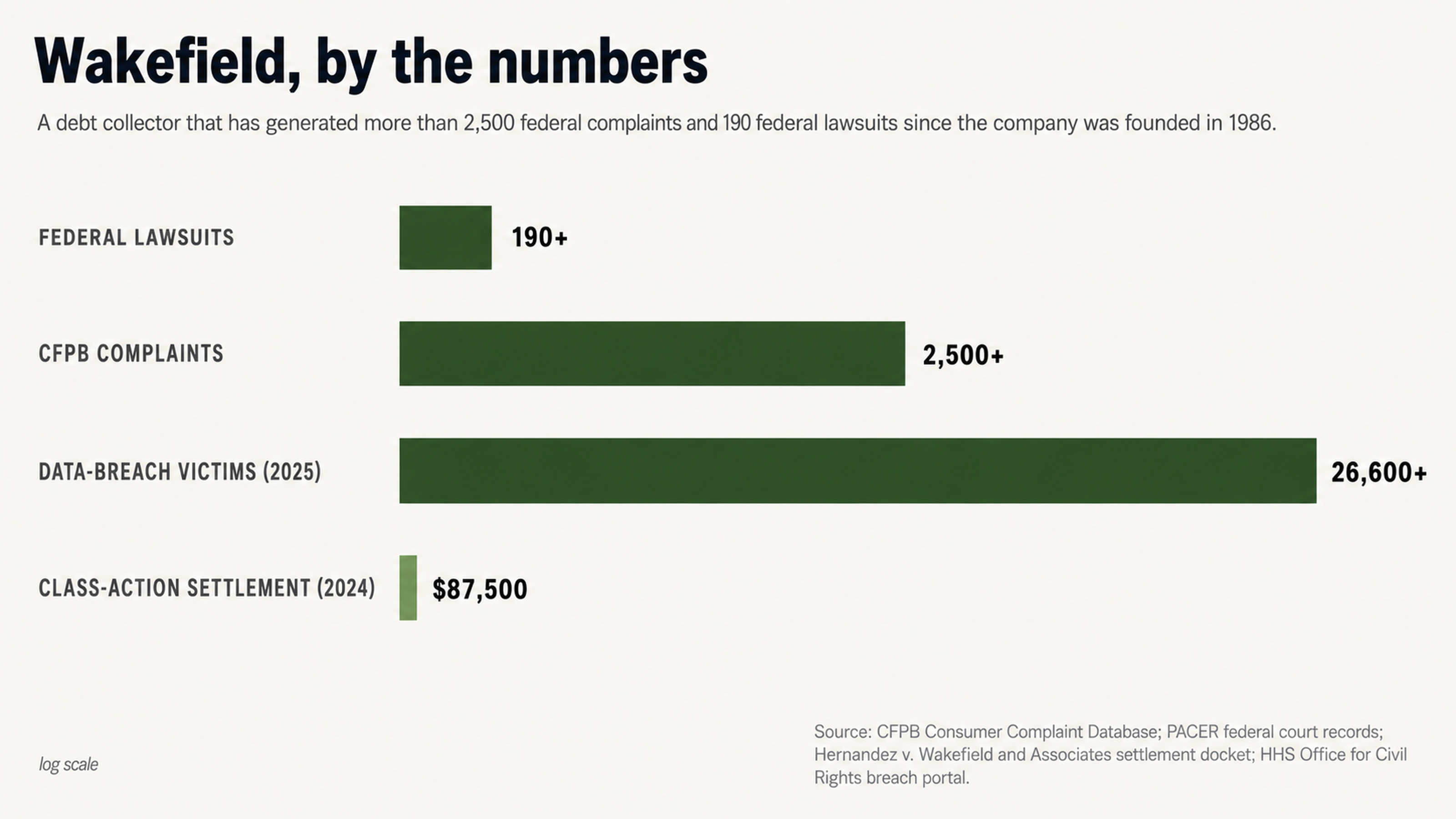

Wakefield and Associates has been sued in over 190 federal cases, primarily for violating the Fair Debt Collection Practices Act. This puts the company on the list of most sued debt collection agencies in the United States today.

The company paid $87,500 to settle a class action in 2024 after it was sued for charging excessive interest on medical debt without a valid contract. The case, Hernandez v. Wakefield and Associates, involved more than 11,000 Florida consumers who received collection letters between April 2022 and September 2024.

But that’s not all. Here’s what Wakefield’s customers are saying about the company:

The Better Business Bureau gives Wakefield a rating of 1.01 out of 5 stars from 73 reviews. Google reviews give Wakefield a rating of 1.3 out of 5 stars. The Consumer Financial Protection Bureau has more than 2,500complaints against the company in its database.

“Payments went missing, money owed to the hospital was never paid. I had a hospital turn an account over to a collection agency. After 3 payments were made to this collection agency. I received a letter from Wakefield and Associates... Payments were never forwarded to the hospital. Hospital account still shows an outstanding balance.” — BBB review

In January 2025, Wakefield experienced a major data breachexposing the personal and medical information of more than 26,600 consumers. The breach included Social Security numbers, financial account information, and protected health information under HIPAA.

Top mistakes consumers make with Wakefield and Associates

Mistake #1: Paying the collection immediately

One of the most common mistakes consumers make is to pay the collection the minute they find it. This seems to make sense. If you owe money, you should pay it, right? But that’s not how credit reporting works.

When you pay a collection, it does not come off of your credit report. Instead, the status of the account is updated to paid. The account will remain on your report for seven years from the original date of delinquency. Paid collections still harm your credit score and still indicate to lenders that you had a serious negative event in your past.

The problem gets worse when you consider the fact that the original creditor probably already wrote your debt off as a loss. When a debt is charged off, the original creditor deducts the uncollectible amount on their taxes. The debt is then sold to a collection agency like Wakefield for pennies on the dollar. You’re paying the full amount for a debt that was purchased at a discount.

Mistake #2: Requesting a pay for delete agreement

A lot of people believe they can negotiate a pay for delete arrangement where the collection agency agrees to remove the account from your credit report in exchange for payment. This almost never works.

Credit reporting agencies have contracts with data furnishers that demand accurate credit reporting. Collection agencies that delete accurate information may lose the right to report to the credit bureaus altogether. Even when a collector agrees to delete an account, they don’t always follow through once they receive payment.

The account will remain on your credit report for seven years regardless of the status. You just paid the collection agency for a promise they probably won’t keep, and the account is still hurting your credit score.

Why you should dispute the account first

The 79% error rate problem

In 2012, the non-profit consumer advocacy group U.S. PIRGs foundthat 79% of all credit reports contained errors or other serious mistakes. This fact alone should change the way you approach every collection account you find on your credit report.

The error could be minor. It could be someone else’s debt. The balance could be wrong because of excessive fees or interest charges. The account could be too old to collect. The collection agency may not have the proper documentation to prove you owe the debt. Any one of these errors gives you grounds for disputing the account and potentially removing it.

In 2024, Wakefield agreed to pay a class action settlement because the company was found to be charging excessive interest on medical debts. If your balance includes excessive interest charges, the balance reported on your credit report is inaccurate and can be disputed under the FCRA.

Documentation failure and verification issues

Collecting medical debt involves a complicated chain of custody. The provider bills you. Sometimes the bill goes through insurance. The provider’s billing department may send the debt to an internal collections department. Eventually, the debt may be sold to a third-party collection agency like Wakefield. At every step, documentation can get lost, damaged, or destroyed.

When you dispute a collection, the credit bureau must investigate, and the collection agency must verify the debt. If Wakefield cannot verify the account within the allotted time limit, the credit bureau must delete the account from your report. In 2024, a federal judge found that Wakefield failed to verify the debt and engaged in conduct that “harasses, oppresses, or abuses” consumers.

Nikkel v. Wakefield and Associates

Most debts are purchased in bulk. Collection agencies may have a spreadsheet with your name and balance due, but that does not mean they have the underlying documentation to prove the debt is valid. They may not have your original contract, your itemized statement, or the chain of assignment that proves ownership of the debt.

Understanding your legal rights

The FCRA and FDCPA

The Fair Credit Reporting Act (FCRA) and the Fair Debt Collection Practices Act (FDCPA) are federal laws designed to protect consumers from unfair and deceptive practices in the debt collection and credit reporting industries.

Under the FCRA, every item on your credit report must be substantively accurate, completely accurate, and verifiable. If any information on a collection account is inaccurate, you have the legal right to dispute the account and force the credit bureau to investigate. If the information cannot be verified, it must be deleted.

Under the FDCPA, debt collectors may not engage in unfair, deceptive, or abusive behavior. This includes misrepresenting the amount of money you owe, threatening to sue when they have no intention of doing so, and failing to validate the debt. Wakefield has been found to have violated multiple sections of the FDCPA in federal court. That means there is a good chance the company violated your rights, too.

Time may be on your side

Every debt has a statute of limitations (SOL). The SOL is the amount of time a lender or debt collector has to sue you in civil court for a debt. Once the SOL expires, the debt becomes time-barred, which means you still owe the money but the debt collector can no longer take you to court over it.

SOLs vary from state to state and debt to debt but generally range from three to six years. Medical debt often has a shorter SOL. The older the debt, the closer it is to the SOL expiring.

In most cases, debt collectors don’t file lawsuits. It costs too much money and isn’t worth the risk. Most medical debts will never end up in court.

When to get professional help

Knowledge is power

The credit repair industry exists because the laws governing debt collection and credit reporting are complicated and nuanced. It’s one thing to know you have rights under the FCRA. It’s something else entirely to know how to use them.

Professional credit repair experts understand the procedural technicalities, the timing deadlines, and the documentation requirements that can make or break a credit dispute. They know which types of errors are most likely to result in a deletion and how to word a credit dispute letter for maximum impact. They know when to file a complaint with a federal regulator and when to file a lawsuit.

Debt collectors prey on consumers who don’t know any better. When you hire a professional credit repair expert, you send a message to the debt collector that you know your rights and you’re willing to fight for them.

The risks of DIY repair

When you try to repair your own credit, you can easily make a mistake that will make the situation worse. You can say the wrong thing on a phone call and reset the clock on the statute of limitations. You can send the wrong type of credit dispute letter and end up with a frivolous claim that the credit bureau ignores. You can make a partial payment that the debt collector accepts as proof that you owe the full amount.

Many consumers who try DIY credit repair end up in a worse position than when they started. They spend months or even years sending letters and making phone calls only to have the credit bureau or debt collector ignore them. By the time they decide to hire professional help, precious time has been lost.

Hiring a credit repair expert from the outset ensures your dispute is handled correctly from the beginning. Every phone call is logged. Every deadline is tracked. Every letter from the credit bureau or debt collector is evaluated by someone who understands the implications of what they’re reading.

The bottom line

Wakefield and Associates has been sued in federal court over 190 times. The company paid a class action settlement for illegal collection practices. It has more than 2,500 complaints with the CFPB. It recently experienced a data breach. Its customer service reviews are abysmal.

This is a debt collection agency with a lot of problems, and there’s a good chance your debt is one of them. Don’t pay it. Don’t call the agency and try to negotiate. And don’t assume the information is accurate just because a debt collector says so.

Do this instead

If you have a collection account from Wakefield and Associates on your credit report, don’t ignore it and don’t pay it. You have a limited amount of time to act, and the sooner you start, the higher your chances of getting the account deleted altogether.

At FightCollections.com, we specialize in fighting debt collectors and helping consumers get questionable collection accounts removed from their credit reports. We understand the FCRA and FDCPA. We understand how debt collectors like Wakefield and Associates operate. And we understand exactly how to challenge them.

Contact us today for a free consultation. We’ll evaluate your credit report, explain your options, and help you craft a strategy for removing Wakefield and Associates from your report once and for all.